Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Summary

Listen to podcast (in French only)

(Listen to) Axel Botte’s podcast:

- Review of the week – A new hope for crisis resolution;

- Theme – The U.S. central tank is loaning barrels in last resort.

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: The U.S. central tank is loaning barrels in last resort

- The closure of the Strait of Hormuz has created the largest oil crisis in modern history, with over 14 million barrels per day shut in and cumulative Gulf production losses exceeding 1 billion barrels since February 2026;

- The crisis has accelerated OPEC's fragmentation, with the UAE deciding to leave the cartel to pursue higher production capacity (targeting 5+ mb/d by 2027), potentially triggering a market share race that could undermine the organization's pricing power;

- The United States has emerged as the "oil lender of last resort," releasing 172 million barrels (40%) from its Strategic Petroleum Reserve and achieving record net exports of 5.9 mb/d to help stabilize global markets. However, inventory drawdowns are unsustainable beyond a few months;

- Despite oil price volatility and geopolitical risk premiums of up to $33/barrel, the impact on broader financial markets has been relatively muted, though short-term inflation expectations remain elevated.

Oil Crises, Government Policies and the Future of OPEC

The war in Iran will have both short- and long-term consequences.

In February 2026, the U.S. and Israel launched strikes against Iranian nuclear and military sites after weeks of unsuccessful negotiations. Iran responded by attacking tankers and oil and gas facilities in several Gulf countries, causing Brent crude to surge past $100 a barrel and remain elevated. Attempts at peace talks in Pakistan collapsed in April, and on April 12, the U.S. Navy declared a blockade of Iranian ports. As a result, the Strait of Hormuz—a vital waterway through which roughly 20% of the world’s oil is transported daily—remains effectively closed.

This supply shock represents not only a short-term crisis but also a potential turning point for global energy security, with lasting implications for strategic petroleum reserves, supply chain diversification, and the geopolitics of energy trade. Clear transitions from historical crises to current events help illustrate the significance of these developments.

Oil crises have consistently triggered more significant, long-lasting transformations than the immediate disruptions they caused. The 1973 Arab oil embargo led to the creation of the Strategic Petroleum Reserve and decisions to reduce petroleum dependence. The 1979 revolution in Iran spurred the development of clean-energy industries and influenced consumer choices, industrial investments, and government policies in ways that persisted long after the crisis subsided. Just as previous oil shocks prompted long-term shifts in energy policy, the current blockade of the Strait of Hormuz should serve as a catalyst for accelerating clean energy adoption and supply chain diversification.

The current crisis, with the blockade of the Strait of Hormuz, has sent crude oil prices soaring. In contrast to China’s push for renewable energy technologies, the U.S. administration’s agenda has prioritized oil and gas and reduced support for clean energy initiatives. This U.S. industrial strategy appears extremely short-sighted. Diversification away from oil should be a strategic imperative. The technological landscape of clean energy today is vastly more advanced and cost-competitive than during previous crises. Solar and wind power are not only economically viable but, importantly, cannot be embargoed or blockaded.

Against this backdrop, the Organization of the Petroleum Exporting Countries (OPEC) is facing a major challenge. OPEC’s strength lies in the ability of its members to bear the financial costs of withholding barrels from the market by imposing quotas on individual member countries. The United Arab Emirates (UAE) is disproportionately affected by this strategy, producing well below its capacity. This unequal burden has become a source of friction, creating a "frenemy" relationship with Riyadh, the historical pillar of the organization. The UAE has decided to leave the cartel (Indonesia, Qatar, Ecuador, and Angola also left the organization for various reasons). The UAE has the financial means and geological endowment to produce much more oil at relatively low costs and build new export infrastructure to bypass the Strait of Hormuz. The UAE projects to raise output to more than 5 mb/d by 2027. Therefore, once equilibrium is restored in the oil market, a race for market share will likely erode OPEC’s pricing power further. The UAE’s exit from OPEC could prompt other members to reconsider their participation, potentially undermining the cartel’s ability to coordinate production and stabilize prices, which may lead to increased volatility in global oil markets.

Global Oil Market Crisis: Record Supply Disruptions and Inventory Drawdowns

The Iran crisis has created an unprecedented supply-demand imbalance, with cumulative Gulf production losses exceeding 1 billion barrels and more than 14 mb/d (million barrels per day) currently shut in due to the closure of the Strait of Hormuz, according to the IEA monthly report. Global oil supply has plummeted to 95.1 mb/d in April, compared to an average of 101 mb/d before the crisis. However, producers in the Americas (United States, Canada, Brazil, Guyana, Venezuela, etc.) increased supply by over 600 kb/d (thousand barrels per day) since the start of the year. In addition, the utilization of bypass pipelines around the Strait of Hormuz—such as routes via Saudi Arabia to the Red Sea or via Oman—helped to reduce the shortfall in global supply.

While supply disruptions have been severe, the resulting price increases have also led to notable shifts in global demand patterns. Demand has declined in response to higher prices. Global oil consumption may contract by 420 kb/d in 2026, which is fully 1.3 mb/d below pre-war IEA projections. The petrochemical and aviation sectors bear the brunt of the impact. Refiners have dramatically reduced operations. Chinese seaborne crude imports collapsed by 3.6 mb/d from February to April as cutbacks were widespread in Asia.

The oil market is projected to stay in deficit until the final quarter of 2026, even assuming a resumption of Strait flows from Q3. However, supply recovery is expected to lag demand normalization, due to refinery infrastructure damage. A U.S.-led loosening of export restrictions (Russia’s seaborne oil) will have a marginal positive impact.

The U.S. as the oil lender of last resort

No one can print oil barrels like Central banks print money.

According to the International Energy Agency (IEA), global oil inventories are depleting at a record pace. Observed stocks declined by 129 million barrels (mb) in March and 117 mb in April. On-land stocks dropped by 170 mb in April alone, while OECD countries saw their stocks plummet by 146 mb. This represents a combined drawdown of 250 mb over March and April, equivalent to 4 mb/d.

Amid these rapidly declining inventories, the U.S. oil industry has emerged as the supplier of last resort in the current war-torn oil market. While oil producers cannot provide physical barrels instantly, the shale revolution has enabled the United States to dramatically increase its oil exports, transforming it from a net importer of petroleum products to a major exporter. In April, U.S. net exports of crude and refined products averaged a record 5.9 mb/d, a significant jump from 3.3 mb/d a year prior.

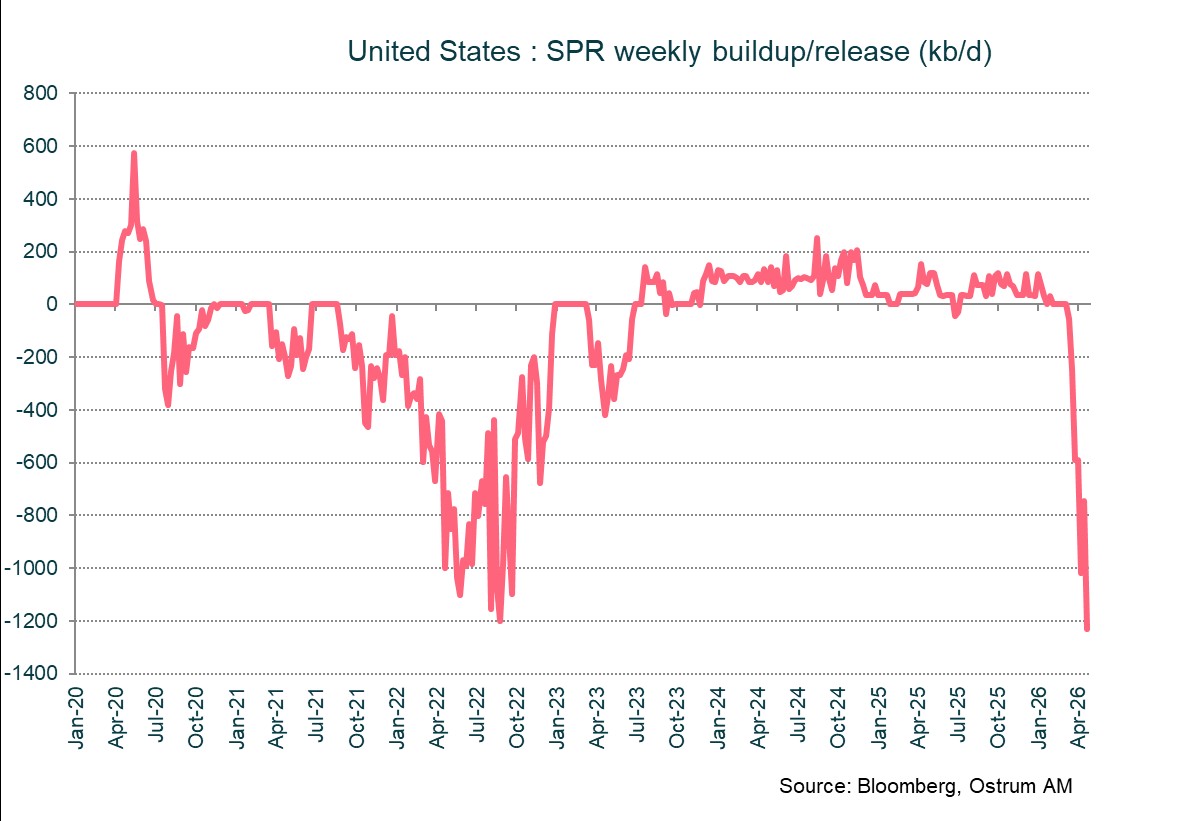

As U.S. exports surge, the strain on domestic reserves becomes increasingly apparent. The critical question is not whether the U.S. can sustain these export levels indefinitely, but whether it can maintain them long enough to help stabilize oil prices and facilitate a diplomatic resolution with Iran. Sustained U.S. exports play a key role in international negotiations by easing global price pressures, which can foster an environment more conducive to diplomatic engagement with Iran and support efforts to de-escalate regional tensions. To support these record-high exports, the United States is releasing oil at an unprecedented rate. In March, the U.S. committed to loaning 172 million barrels from the Strategic Petroleum Reserve (SPR)—about 40% of its reserves—in collaboration with European allies and other major oil-consuming nations, aiming to mitigate global supply disruptions and maintain market stability. Recently, releases from the SPR have reached as much as 1.23 mb/d, a substantial increase compared to 2022 rates. This high flow rate means that about half of the increase in U.S. net exports is being offset by drawing down the SPR, with these barrels making their way to international markets and underscoring the scale and urgency of the current situation.

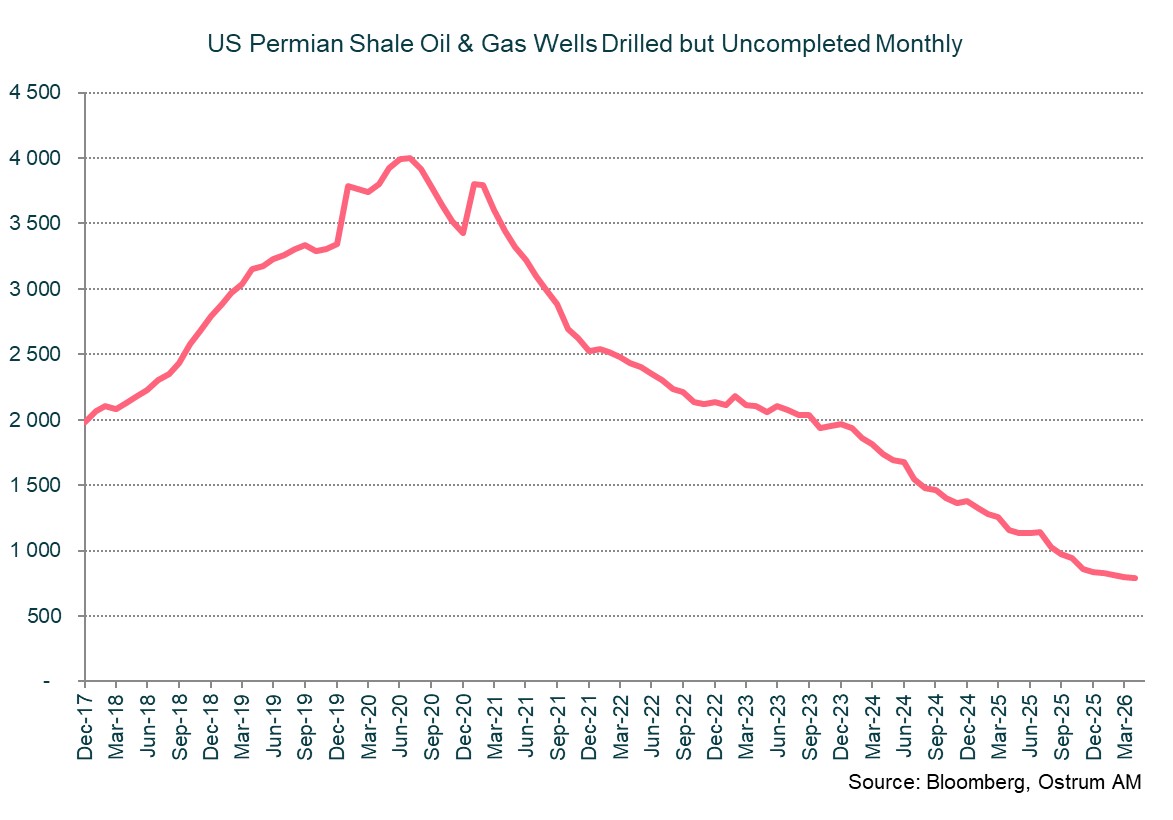

The impact of this increased supply chain pressure is evident in the physical oil market, where the premium of U.S. West Texas Intermediate (WTI) crude over Dated Brent has narrowed considerably, and the total cost for WTI landing in Europe has dropped substantially. So far, the SPR has released approximately 31 million barrels, but further significant releases could push SPR levels to their lowest since the early 1980s. If this trend continues, the SPR could fall to just 10 days of consumption—an uncomfortably low threshold. While U.S. shale producers can ramp up output by tapping drilled-but-uncompleted wells, additional barrels will take months to reach the market. As a result, the U.S. may have to rely more on commercial inventories to maintain current export levels as the SPR is depleted. Unless the standoff with Iran is resolved soon, concerns about shrinking inventories in the oil market will only intensify.

Decomposing Oil Price Movements

Geopolitical risk premium has halved to $15 since Mid-April. Mind deteriorating fundamentals.

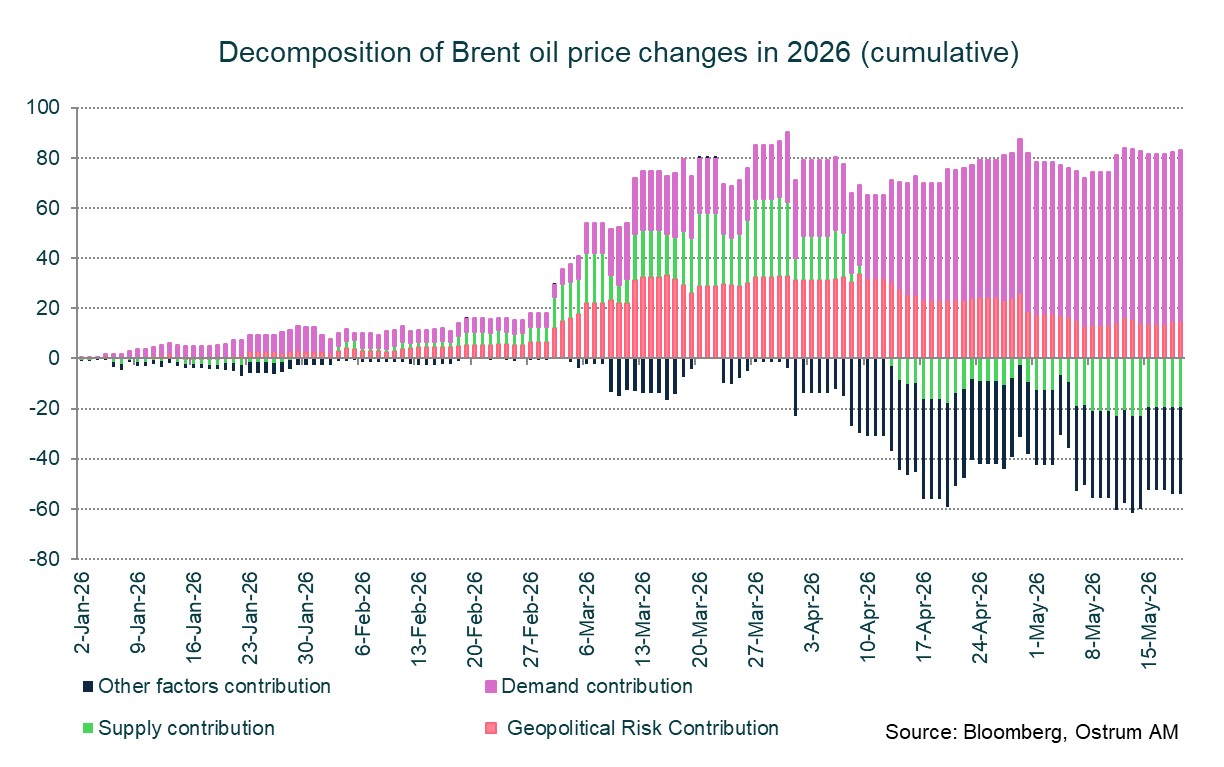

Oil prices are notoriously difficult to model or forecast because they are highly sensitive to numerous factors—including supply and demand fundamentals, the level of available stocks, and geopolitical risks. Additionally, we are not even digging into the complexities of different oil grades: heavy oils have higher density and viscosity, making them harder to refine, while light oils are easier to process; sweet oils contain less sulfur and are more desirable for refining compared to sour oils, which have higher sulfur content; total acid content also affects oil quality and pricing. Prices can fluctuate dramatically in response to changes in these fundamentals and risk factors. Using a model developed by Bloomberg, the cumulative change in Brent oil prices from the start of 2026 can be broken down into supply, demand, and risk components—where higher supply tends to lower prices, and higher demand pushes prices upward.

According to these calculations, the geopolitical risk premium pushed oil prices up by as much as $33 per barrel by mid-April. After the U.S. imposed a ceasefire—albeit a fragile one—the premium receded to $15. Supply constraints, such as reduced output from major producers and logistical bottlenecks, also raised prices by approximately $30 per barrel until the end of March. Demand factors, despite some evidence of demand destruction, have gradually become more prevalent in determining oil prices since mid-April. The release of strategic reserves increased available supply, which helped ease upward pressure on prices. Similarly, alternative transport routes allowed more barrels to reach the market, mitigating shortages caused by geopolitical disruptions. Additionally, the easing of sanctions on Russian oil contributed to lower prices.

The Oil Shock’s Spillover Across Financial Markets

Since the conflict in Iran began, financial markets have reacted strongly to changes in oil prices. Typically, higher oil prices increase inflation expectations and prompt central banks to consider raising interest rates. This leads to higher bond yields and puts downward pressure on both stock and credit markets. When oil prices fall, equities tend to recover and bond yields decrease.

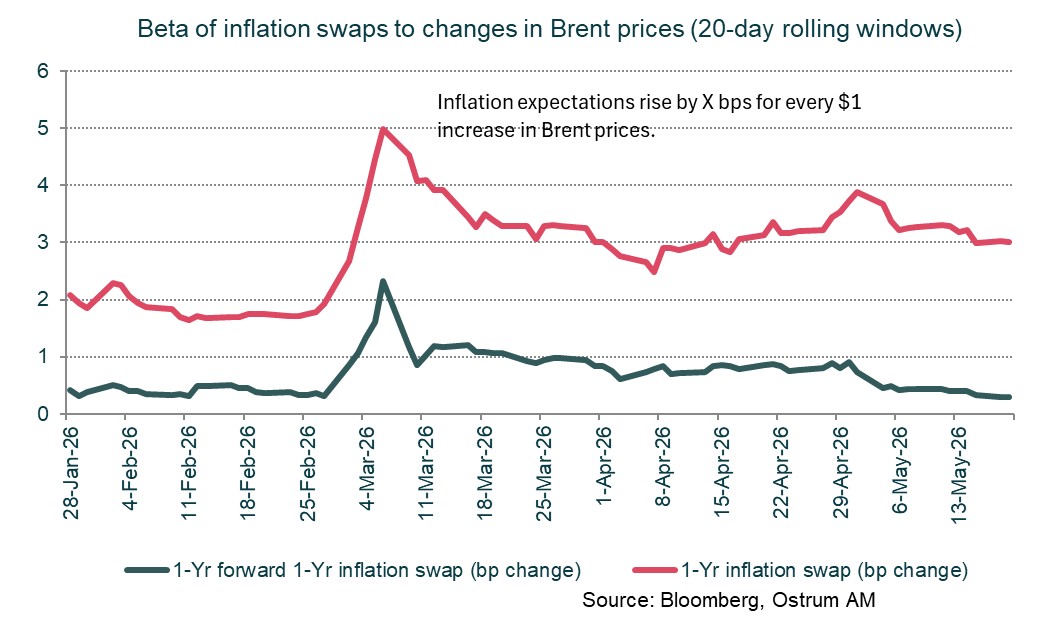

To measure how European assets respond to oil price changes, we analyzed their daily sensitivity during rolling 20-day periods. One key metric is the 1-Yr inflation swap, a financial derivative that reflects market expectations for inflation over the next year. Another is the 1Yr-forward-1Yr inflation swap, which forecasts inflation for the year starting one year from now. We also examined yields on the 10-Year Bund, Germany’s government bond, as well as the Euro Stoxx 50 (a leading European equity index) and the iTraxx XOVER index, which tracks credit risk in European high-yield (riskier) bonds.

Oil price movements have had a pronounced effect on short-term inflation expectations. For example, the 1-Yr inflation swap rose by up to 5 basis points for every $1 increase in Brent crude prices at the start of the war. This sensitivity, known as beta (a measure of how much one variable changes in response to another), has decreased since its peak but remains about 1.5 times higher than before the conflict. This sustained volatility suggests that traders may be using oil futures to hedge against inflation, compensating for limited activity in inflation-linked bond markets.

Initially, markets expected the oil shock’s effects on inflation to last, but the sensitivity of the 1Yr-forward-1Yr inflation swap has returned to pre-war levels. This indicates that investors no longer anticipate a prolonged inflation impact from the initial spike in oil prices. Bund yields have risen in response to higher oil prices, though short-term yields increased more sharply due to changing policy rate expectations. The euro yield curve has flattened, meaning the difference between short-term and long-term yields has decreased. Before the war, higher oil prices tended to steepen the curve, suggesting stronger growth prospects. Now, supply shocks signal inflation and possible monetary tightening, which can slow economic growth.

For equity markets, higher crude prices have led to poorer performance. During periods of peak risk aversion, every $1 rise in oil prices resulted in a 0.5% drop in the Euro Stoxx 50 index. The impact on the iTraxx XOVER index has been less pronounced; its sensitivity to oil price changes has reverted to pre-war levels, indicating that credit risk in high-yield European bonds is no longer directly linked to oil price volatility.

Conclusion

Over the past three months, the war in Iran has resulted in a global oil output loss totaling 1 billion barrels. To offset the impact on crude prices, both commercial and strategic oil inventories have been aggressively drawn down, providing a temporary buffer against supply shortages. However, this pace of reserve releases is unsustainable, highlighting the immediacy of the situation since oil cannot be produced on demand. So far, the market response has been relatively benign. If the conflict persists, these stabilizing factors may diminish, and market sentiment could shift rapidly, leading to heightened price volatility and potential disruptions across financial markets.

Axel Botte

Chart of the week

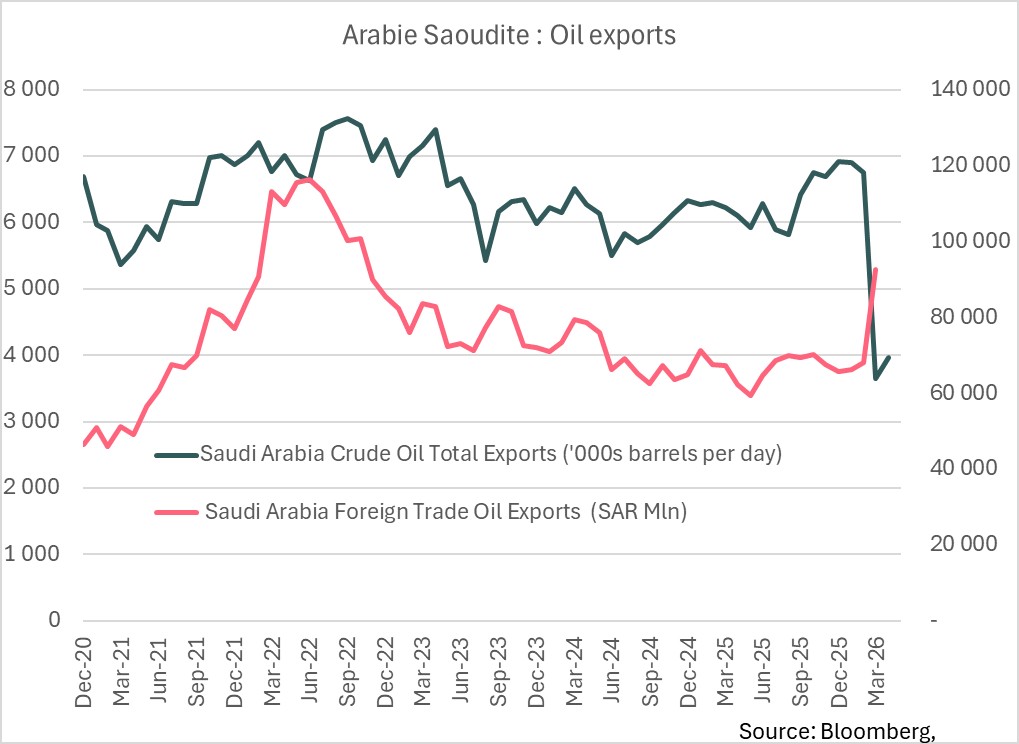

Saudi Arabia stands out from other Gulf countries thanks to its pipeline leading to the port of Yanbu on the Red Sea, which allows it to continue exporting its crude oil despite the blockade of the Strait of Hormuz.

Its crude exports reached nearly $25 billion in March, a three-year high and a 37% year-on-year increase. In March, Brent averaged $99, representing more than a 40% increase since the outbreak of the Middle East conflict on February 27, explaining this strong growth.

However, the country has had to revise down its ambitions for the SAUDI VISION 2030 project as budget prospects are rapidly deteriorating. The Kingdom has borrowed more than $10 billion since the beginning of the year, representing half of the total debt issuance for 2025.

Figure of the week

39.6

39.6%, the weight of technology in the MSCI Emerging Markets index, which now exceeds that of the U.S. MSCI (36%).

Market review:

- Iran-U.S.: A draft agreement is under negotiation in Doha ;

- Oil: Brent plunges below $100, driving inflation expectations lower ;

- Rates: Bund below 3%, Gilt yields down 28 bps on the week;

- Equities: 6% rise in Europe driven by cyclicals and technology.

A New Hope for Crisis Resolution

An agreement to extend the ceasefire and reopen the Strait of Hormuz appears to be under negotiation under Qatari auspices. Despite a lack of information regarding the contours of the deal, oil has already plunged below $100, benefiting risk assets and long-term rates.

The prospect of crisis resolution resurfaced last week. Equity markets rebounded while long-term rates, under pressure since the oil shock began, eased. The knee-jerk market reaction will likely face uncertainties regarding the actual negotiations, but as has often been the case over the past three months, optimism prevails. Market-priced inflation expectations have retreated, in contrast to household surveys (3.9% for 5-10 years according to the University of Michigan poll). The next phase will concern Fed policy amid a delicate transition between Jerome Powell and Kevin Warsh.

In the United States, April's FOMC minutes served as a reminder that several committee members considered high inflation would require monetary tightening. Despite his vote at the last meeting, Christopher Waller now declares himself in favour of removing the accommodative bias embedded in April's statement. This change in tone is significant as it came just hours before new Fed Chair Kevin Warsh was sworn in. This augurs difficult discussions on U.S. monetary policy direction. Warsh will want to build consensus ahead of Jackson Hole, which often foreshadows fourth-quarter monetary decisions. Inflation remains too high. Activity is harder to read given growth is dominated by artificial intelligence spending. Housing remains abnormally weak, with recent tensions in long-term rates maintaining strong pressure on residential investment. Labour market signals remain ambiguous, though ADP weekly data appears to confirm improvement over the past two months. In Europe, PMIs indicate a sharp contraction in French services activity, though this must be qualified by other surveys (notably INSEE).

European equities (+3 to 5% across indices) and Asian markets (Japan +7%, Korea +4%) have rebounded sharply, with these two regions being the primary beneficiaries of any potential Strait of Hormuz reopening. Earnings revisions have also turned more favourable in recent weeks, including in Europe where growth inflected downward in the second quarter. With oil's retreat, chemicals, industrials, and transport stocks gained around 6% on the week, surpassed only by technology's 10% advance.

In bond markets, crude's collapse immediately triggered a revision in short-term inflation expectations (-28 basis points on the 2-year inflation swap). The Bund returned below 3% (2.95%, down 20 basis points on the week), accompanied by the Gilt (-28 basis points), which extended the rally following more favourable April inflation data (including services CPI at 3.2%). JGBs also benefited from the global brightening. The T-note underperformed, constrained by the FOMC's restrictive posture. Meanwhile, sovereign spreads tightened, notably Greek and Italian debt (-5 basis points on the week). Credit widened inconsequentially alongside falling rates, while high yield struggled to keep pace with equities.

Axel Botte

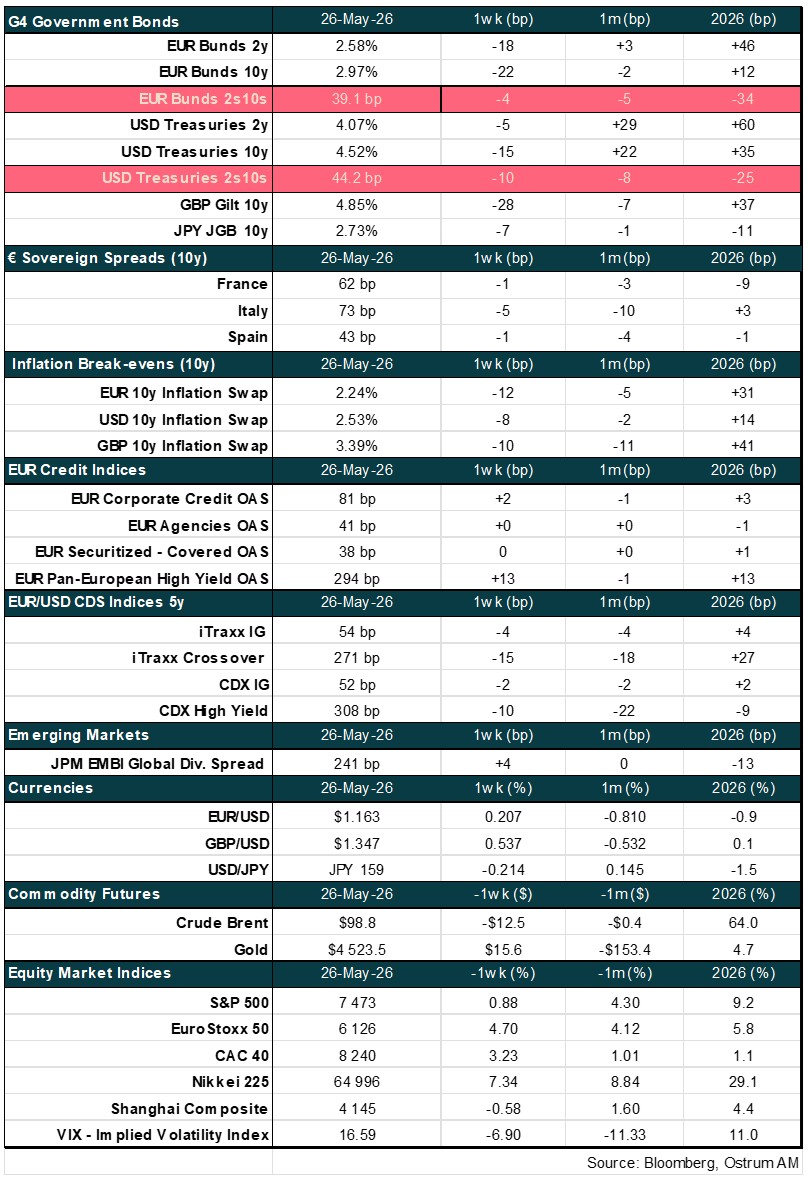

Main market indicators