Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Listen to podcast (in French only)

(Listen to) Aline Goupil-Raguénès’ and Zouhoure Bousbih’s podcast:

- Review of the week – Financial markets guided by headline news;

- Theme – ECB's vigilance towards energy shock risks.

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: ECB's Vigilance Towards Energy Shock Risks

- The ECB meeting was particularly awaited given the sharp rise in energy prices linked to the conflict in the Middle East. Expectations were not focused on the decision regarding rates, with a status quo broadly anticipated, but rather on the ECB's apprehension of risks and the tone of the press conference;

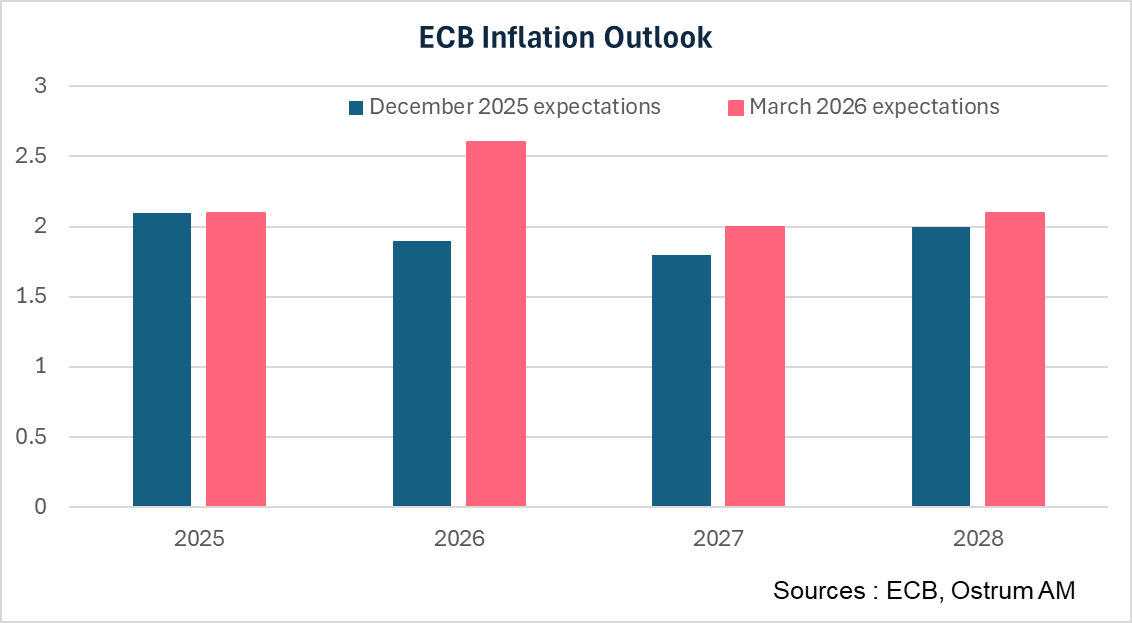

- The ECB proved to be very reactive by incorporating information up to March 11th into its forecasts. Growth prospects were thus revised downwards and those concerning inflation significantly upwards for 2026: an average of 2.6%, before returning to 2% as early as 2027. Given the uncertainty, two alternative scenarios were published;

- The tone of the press conference proved to be balanced, with the rise in energy prices generating both downside risks to growth and upside risks to inflation. The ECB considers itself well-positioned to face the uncertainty and shows determination to ensure price stability in the medium term. It will be very attentive to the emergence of potential indirect and second-round effects on prices;

- In the most likely scenario of a temporary rise in inflation linked to a supply shock, the ECB is expected to opt for a prolonged status quo while maintaining a firm tone to anchor inflation expectations well.

The Reactive ECB: Forecast Revisions

The conflict in the Middle East has led to a near closure of the Strait of Hormuz, a crucial chokepoint for 25% of global oil exports and 20% of liquefied natural gas (LNG) exports, and strikes on the energy infrastructure of Gulf countries. This has resulted in a sharp increase in the price of oil and liquefied natural gas, with risks of supply disruptions and value chain disturbances. Unlike the Fed, which also met last week, the ECB was very reactive to the energy shock, as it revised the forecasts it had initially finalized on March 4th. ECB teams produced new projections incorporating data up to March 11th. These are based on an average oil barrel price peaking at $90 in the second quarter of 2026 and a liquefied natural gas price peaking at €50/MWh on average over the same period, before declining in subsequent quarters, in line with energy commodity futures markets.

Significant upward revision to 2026 inflation outlook ahead of rapid moderation

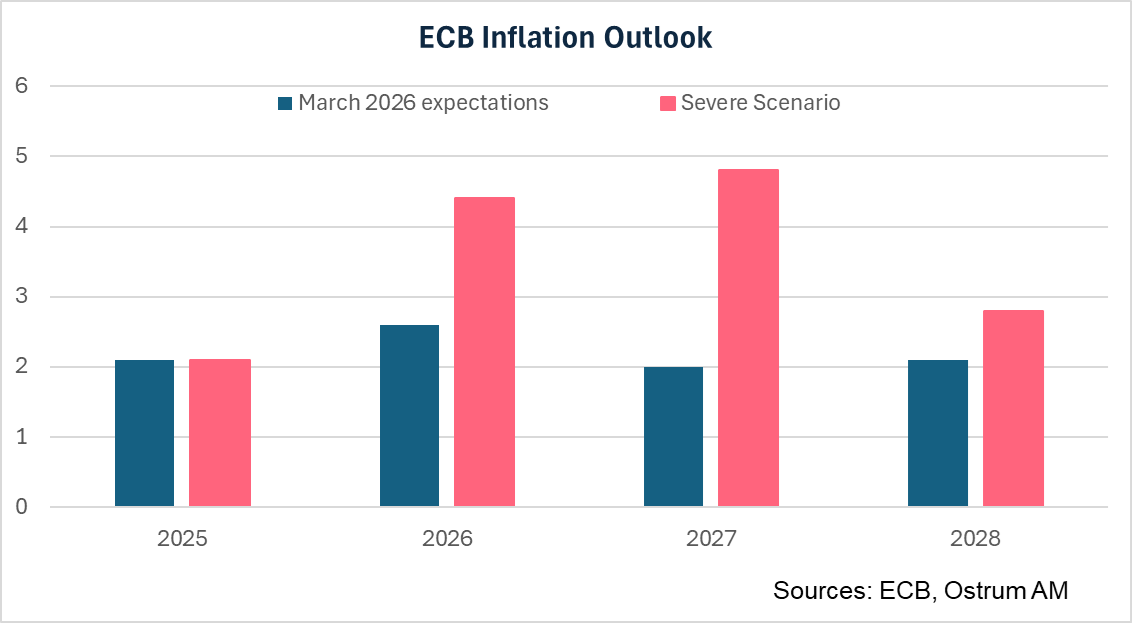

Inflation prospects were thus revised significantly upwards for 2026 compared to those published in December. Inflation is expected to average 2.6% compared to the 1.9% forecast in December. This is the result of the sharp rise in energy prices, which is expected to push inflation to 3.1% in Q2 before returning to 2.8% in Q3.

Inflation is temporary as it is expected to return to an average of 2% in 2027 due to a negative base effect on inflation related to energy prices. It rises again to 2.1% in 2028. This is a result of the rise in carbon prices linked to the implementation of the new quota exchange system. It would contribute 0.2 percentage points to inflation.

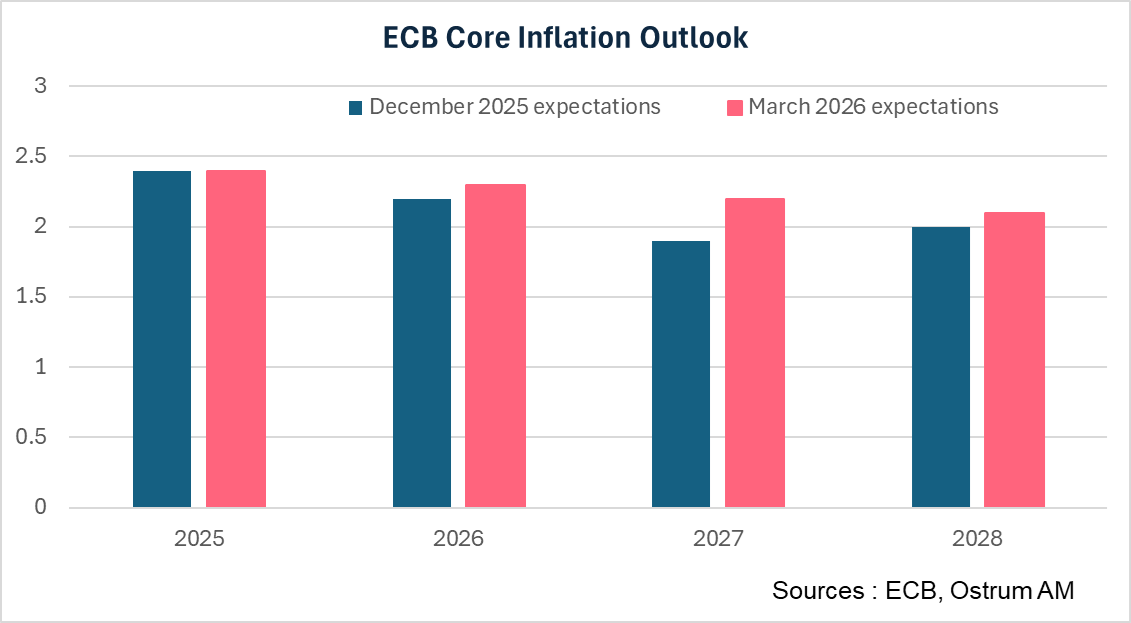

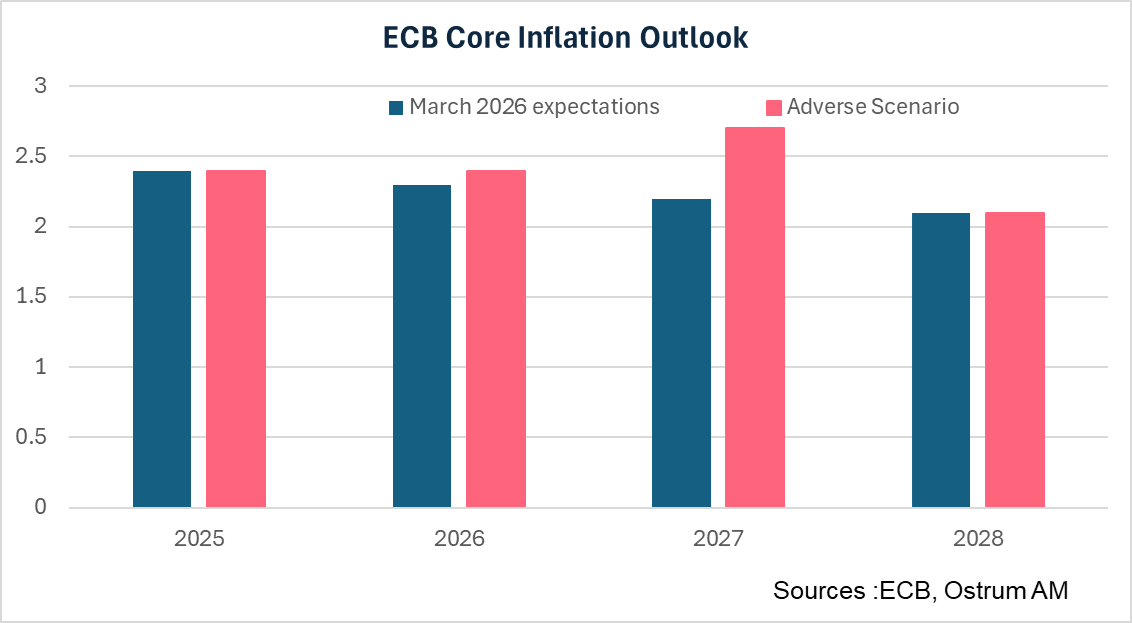

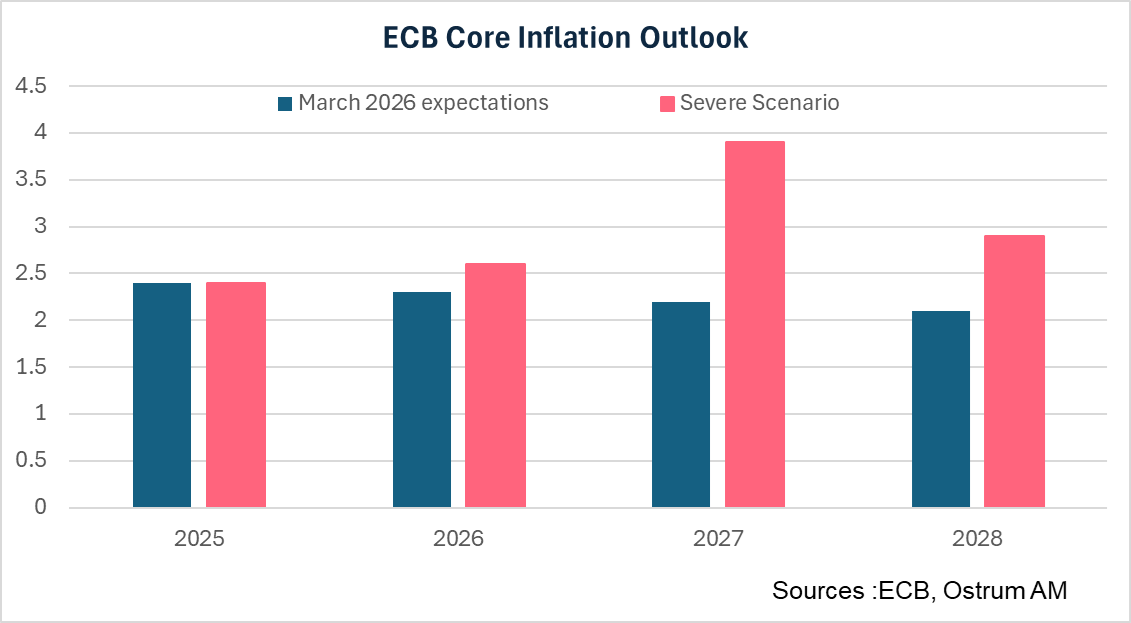

The impact on core inflation is limited. It was revised slightly upwards to 2.3% in 2026 (compared to 2.2% anticipated in December) and 2.2% in 2027 (compared to 1.9%), and 2.1% in 2028 (compared to 2%).

Downward revision of growth prospects:

Growth has been revised downwards in the short term. The sharp rise in energy prices and higher uncertainty will weigh on household consumption and business investment in the 2nd and 3rd quarters. Domestic demand will remain the driver of medium-term growth, supported by a labor market expected to remain resilient and increased public spending on defense and infrastructure, particularly in Germany.

Growth has thus been revised to an average of 0.9% in 2026 (compared to 1.2% anticipated in December), 1.3% in 2027 (compared to 1.4%), and unchanged in 2028 at 1.4%.

The ECB publishes 2 alternative scenarios given the high uncertainty

Medium-term prospects are uncertain and will depend on the duration and intensity of the conflict and how the rise in energy prices is passed on to inflation and growth. The ECB has thus published two alternative scenarios assuming much higher energy prices and a different adjustment period towards the baseline scenario. They are developed for illustrative purposes. No probability is attached to them, and they do not incorporate the implementation of monetary or fiscal policies other than those included in the baseline scenario.

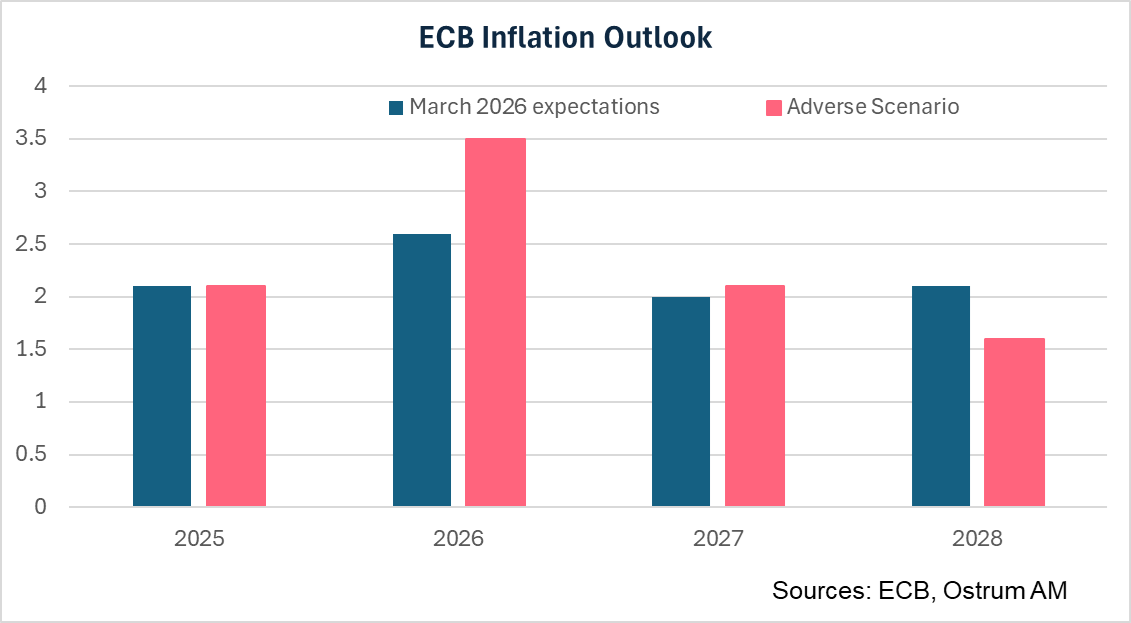

The Adverse Scenario

This scenario is based on oil prices peaking at $119 per barrel in the second quarter of 2026 and gas prices peaking at €87 per MWh over the same period. They converge towards the baseline scenario's assumptions by the third quarter of 2027. Increased uncertainty and international spillovers are more unfavorable.

In this scenario, inflation reaches an average of 3.5% in 2026 before returning to 2.1% in 2027 and settling at 1.6% in 2028. This would reflect "disinflationary pressures stemming from the rapid normalization of energy prices that year." Second-round effects are more significant. Core inflation would reach 2.4% in 2026, 2.7% in 2027, and 2.1% in 2028.

Higher inflation translates into lower growth in 2026 and 2027 compared to the baseline scenario (0.6% and 1.2% respectively), and conversely, higher growth in 2026 (1.6%).

The Severe Scenario

In the severe scenario, oil prices peak at $145 per barrel in the second quarter of 2026, and gas prices peak at €106 per MWh over the same period. Subsequently, they decline much more slowly and remain significantly above the prices assumed in the baseline and adverse scenarios throughout the projection horizon. Uncertainty is higher, as are indirect and second-round effects.

The impact on inflation is much stronger and more persistent: 4.4% in 2026, 4.8% in 2027, and 2.8% in 2028. Indirect and second-round effects on prices are more significant. Core inflation is estimated at 2.6%, 3.9%, and 2.9% respectively over the three projection years.

Higher uncertainty and much higher inflation translate into significantly weaker growth in 2026 and 2027: 0.4% in 2026, 0.9% in 2027, before a rebound to 1.9% in 2028. The latter results from stronger demand linked to wage increases that adjust to higher inflation.

Risks are judged to be balanced

The energy shock constitutes a downside risk to growth and an upside risk to inflation, especially in the short term in both cases.

In response to a question posed during the press conference, Christine Lagarde strongly emphasized that today's situation was very different from that of 2022, when energy prices had risen sharply following the outbreak of the war in Ukraine triggered by Russia.

Inflation was much higher in 2022: 6% compared to 1.9% in February 2026, with medium-term inflation expectations of 2%. This was notably due to a demand catch-up effect as economies reopened after being largely shut down during the Covid-19 crisis.

The labor market situation was also very different from today, with labor tensions and shortages in certain sectors, particularly services. Employees' bargaining power was thus greater. Today, the labor market is solid, and wage growth is slowing in line with the past moderation of inflation.

A caveat, however. Christine Lagarde pointed out that inflation expectations depend heavily on households' and companies' memory of inflation. In 2022, this memory was distant, whereas today it is more recent. 'Consequently, the reaction function they will adopt in terms of investment, wage negotiations, and consumption will be informed by a stronger memory of the inflation that was high and that we have managed to bring back to 2%.'

The ECB is determined to ensure that inflation stabilizes in the medium term

The ECB no longer states it is in a comfortable position but rather well-positioned and well-equipped to face uncertainty. Christine Lagarde refers to this as the 'three times two': inflation is close to 2%, medium-term inflation expectations are at 2%, and interest rates are at 2%, 'so target, target, and broadly neutral.'

The ECB is determined to ensure inflation stabilizes at 2% in the medium term. It does not provide forward guidance on its monetary policy actions, repeating that decisions will be made meeting by meeting based on the data. The Governing Council will pay particular attention to developments in commodity markets, supply bottlenecks, firms' selling price expectations, demand indicators (PMI, consumer confidence), and wage monitoring indicators. The ECB will thus be very vigilant regarding the emergence of indirect and second-round effects that could weigh on medium term inflation expectations.

Conclusion

The energy shock linked to the conflict in the Middle East has led the ECB to significantly revise its short-term inflation outlook upwards and its growth outlook downwards. After peaking in Q2, energy prices are expected to moderate in the baseline scenario, in line with expectations from energy commodity futures markets, to average 2% in 2027. The ECB emphasizes the high uncertainty, as forecasts depend on the duration and intensity of the conflict and how it impacts inflation and the economy. In the central scenario of a temporary rise in inflation linked to a supply shock, the ECB is expected to opt for a status quo in 2026 while adopting a firm tone to firmly anchor medium-term inflation expectations. It should not rush to raise its rates, as suggested by some central bankers, at the risk of repeating the mistakes of 2011. The ECB had then raised its rates twice in response to rising energy prices, which generated a recession and led the Central Bank to quickly backtrack.

Aline Goupil-Raguénès

Chart of the week

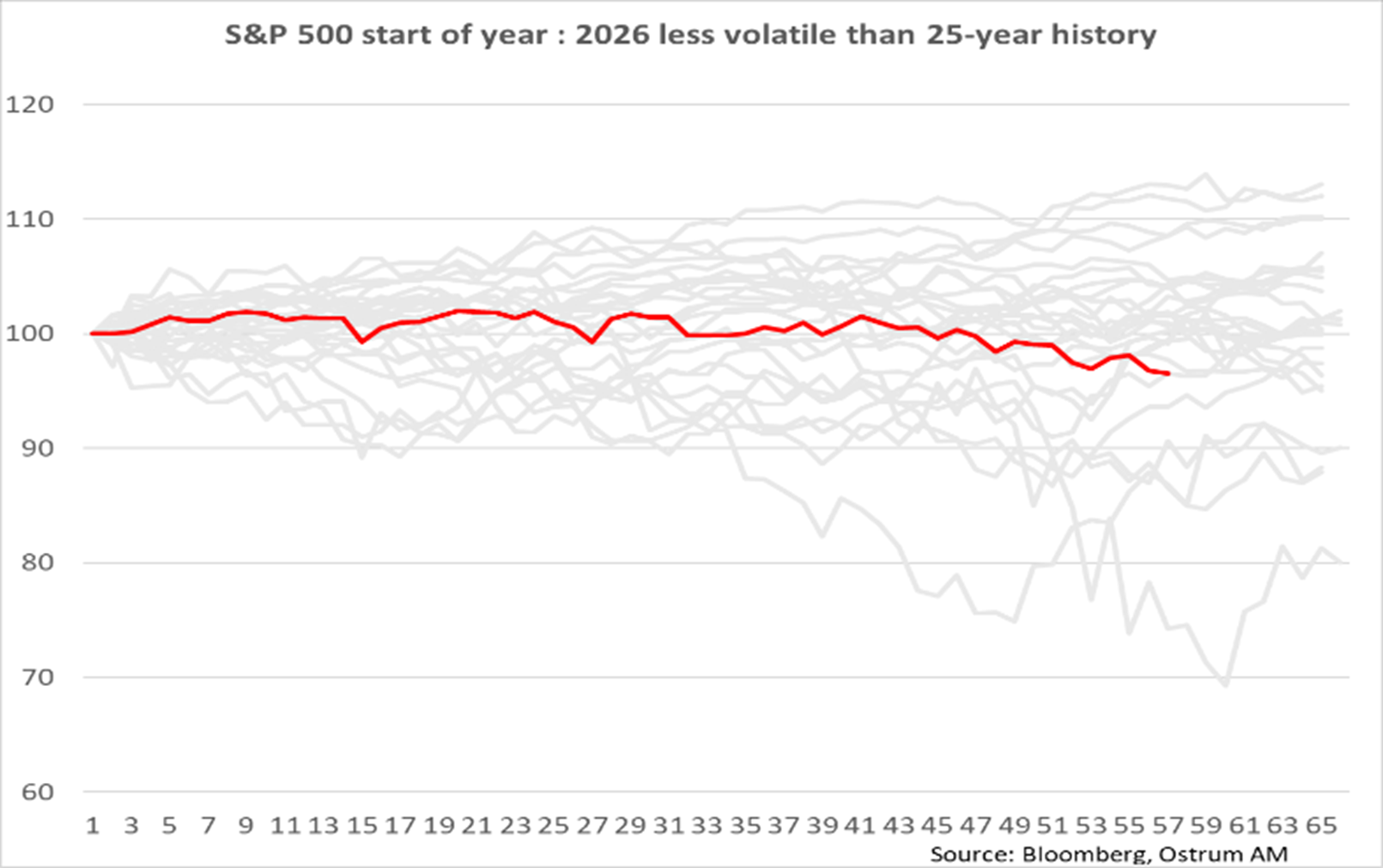

Despite the intense geopolitical sequence and a stagnant labor market, the S&P 500 has been trading in a largely sideways channel since the beginning of the year. This trajectory is particularly benign when viewed over a 25-year historical context (1st quarters). While strong Q4 2025 earnings initially supported the market, fears linked to the private credit market and the risks posed by AI could have triggered a more significant downturn. It appears many investors have hedged their risks in advance, thus limiting selling pressure.

Figure of the week

54

The crisis in the Gulf has resulted in a premium of $54 between the barrel exported from Oman and Brent crude, with Brent itself being $14 more expensive than U.S. WTI.

Market review:

- Iran crisis: Strikes on energy facilities fuel volatility.

- Central Banks: Widespread status quo, but vigilance maintained against inflation.

- Bonds: Sharp yield curve flattening; extreme volatility in Gilts.

- Equities: Rising interest rate expectations shake markets.

Central Banks' Overreaction Risk Amidst Energy Shock

Markets appear to be testing the resolve of central banks to rein in inflation stemming from the oil shock. The specter of 2022 looms large, but concerns are also being voiced about a repeat of the errors seen in 2011.

Iranian strikes targeting LNG production facilities in Qatar have eliminated 17% of global production. The damage is substantial, and reconstruction could take three to five years. Hopes of circumventing the Strait of Hormuz via Saudi Arabia, Iraq, and Turkey have been dashed by these targeted attacks. While several countries have offered security guarantees for the strait, tensions remain high. Central banks are escalating their concerns over inflationary risks, and revised projections for policy rates are weighing on risk assets. The dollar is appreciating with every resurgence of tension.

The past week was dominated by central bank meetings. The Fed maintained its rates, citing upside inflation risks (projected at 2.7% by end-2026), and even revised its growth forecasts upward despite labor market fragility. The U.S. economy is, however, less exposed to this crisis due to its energy surplus. The FOMC is expected to hold steady for several months before resuming monetary easing. In the Eurozone, the ECB acknowledged the inflationary risk by responding to rising inflation breakevens. Some policymakers have suggested tightening as early as April, but the current situation differs significantly from 2022, when an expansionary policy mix, pent-up consumer demand post-COVID, and multiple shocks created an explosive inflationary cocktail. The ECB must avoid overreacting. The memory of 2011 also haunts markets: two rate hikes in response to rising oil prices led to a bond market crash. While there is no banking crisis today, the potential for policy errors remains. The BoE voted unanimously to hold rates, retracting an accommodative bias that had been in place for months. Markets have priced out two rate cuts, now anticipating three hikes in 2026. The significant portion of variable-rate debt in the UK economy could lead to an early slowdown in activity. Andrew Bailey's efforts to temper expectations of monetary tightening are therefore understandable. The Bank of Canada, following weak employment figures, appears to be among the most dovish, alongside the Riksbank, given low inflation in Sweden. Conversely, the RBA is reinforced in its rate-hiking cycle initiated in February and continued in March. The BoJ's stance remains enigmatic, but committee member votes suggest a hawkish bias for April. Amidst this energy shock, equity markets saw a sharp decline towards the end of the week. The market seems to be testing central banks' commitment to curbing price pressures. Expected rate hikes are translating into higher long-term yields, causing a significant flattening of yield curves. The T-note is heading towards 4.40%, the Bund has breached the 3% mark, and the Gilt is struggling to stabilize around 5%. Amidst the storm, the 30-year Bund remained stable over the week at 3.53%. Sovereign spreads are once again under pressure. The BTP is particularly affected, likely due to its greater reliance on natural gas. Credit spreads are widening moderately, reacting less severely than equities or volatility.

Axel Botte

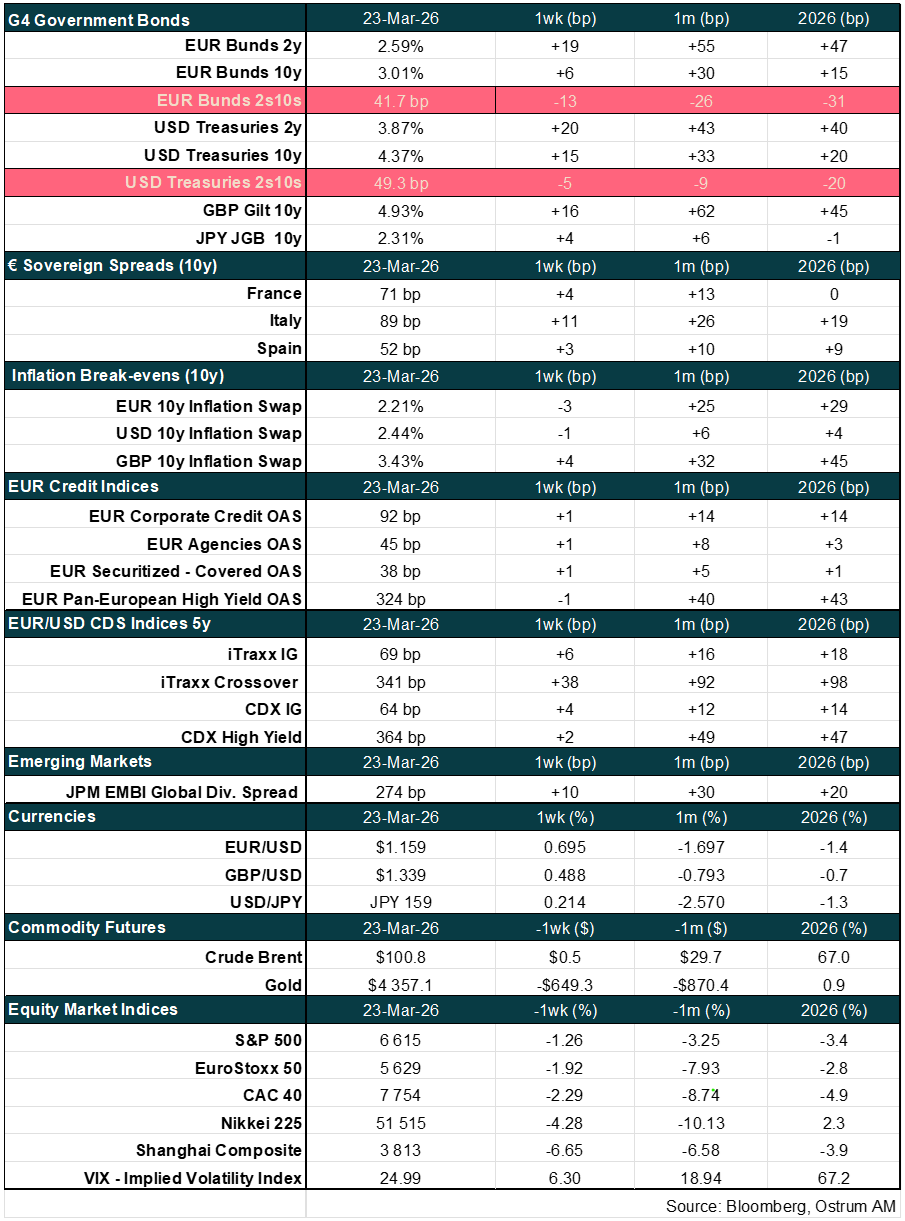

Main market indicators