Quarterly publication / April 2026

Analyses and data as of 04/21/2026.

Marketing communication for professional investors in accordance with MIFID II.

MARKETS OVERVIEW

MARKETS IGNORE THE WAR

The closure of the Strait of Hormuz should concern investors given the crucial importance of this passage for oil and gas trade. Conversely, the announcement of negotiations between Iran and the United States, though fruitless at this stage, immediately triggered an equity rebound. War-related losses have been erased. The oil shock has had limited impact on activity according to initial surveys, so the economic recovery is not in question in Europe. In the United States, the weakening of household consumption since autumn is a point of concern, but AI investment is preventing a sharp slowdown. China, highly exposed to the Gulf, seems to be accommodating higher oil prices thanks to its energy mix and export capacity. Downward revisions to growth and inflation are ultimately modest.

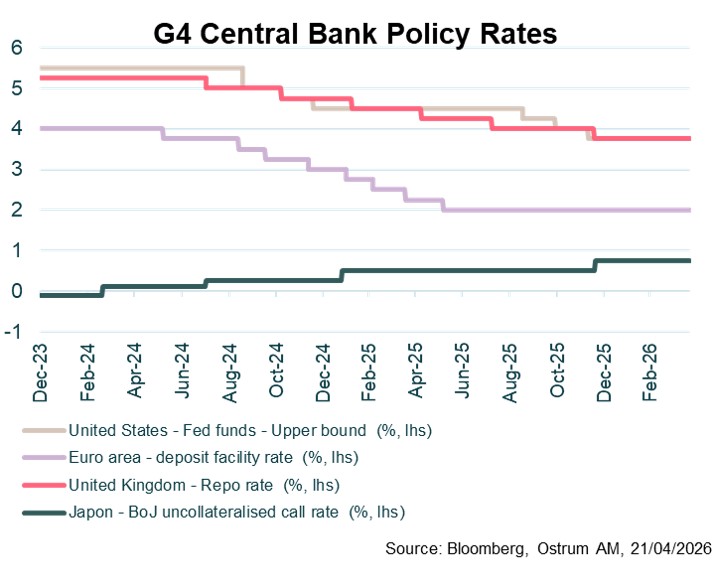

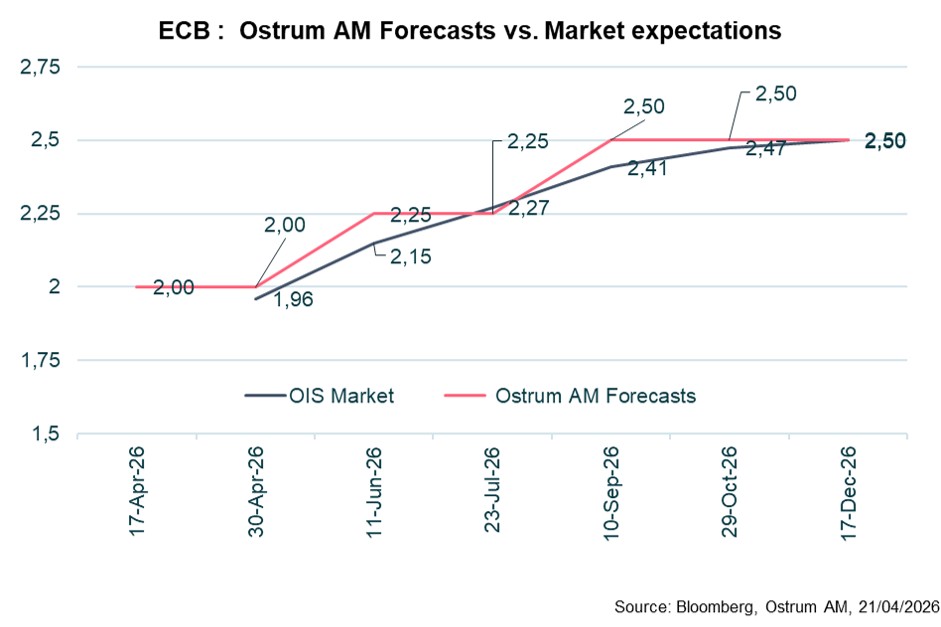

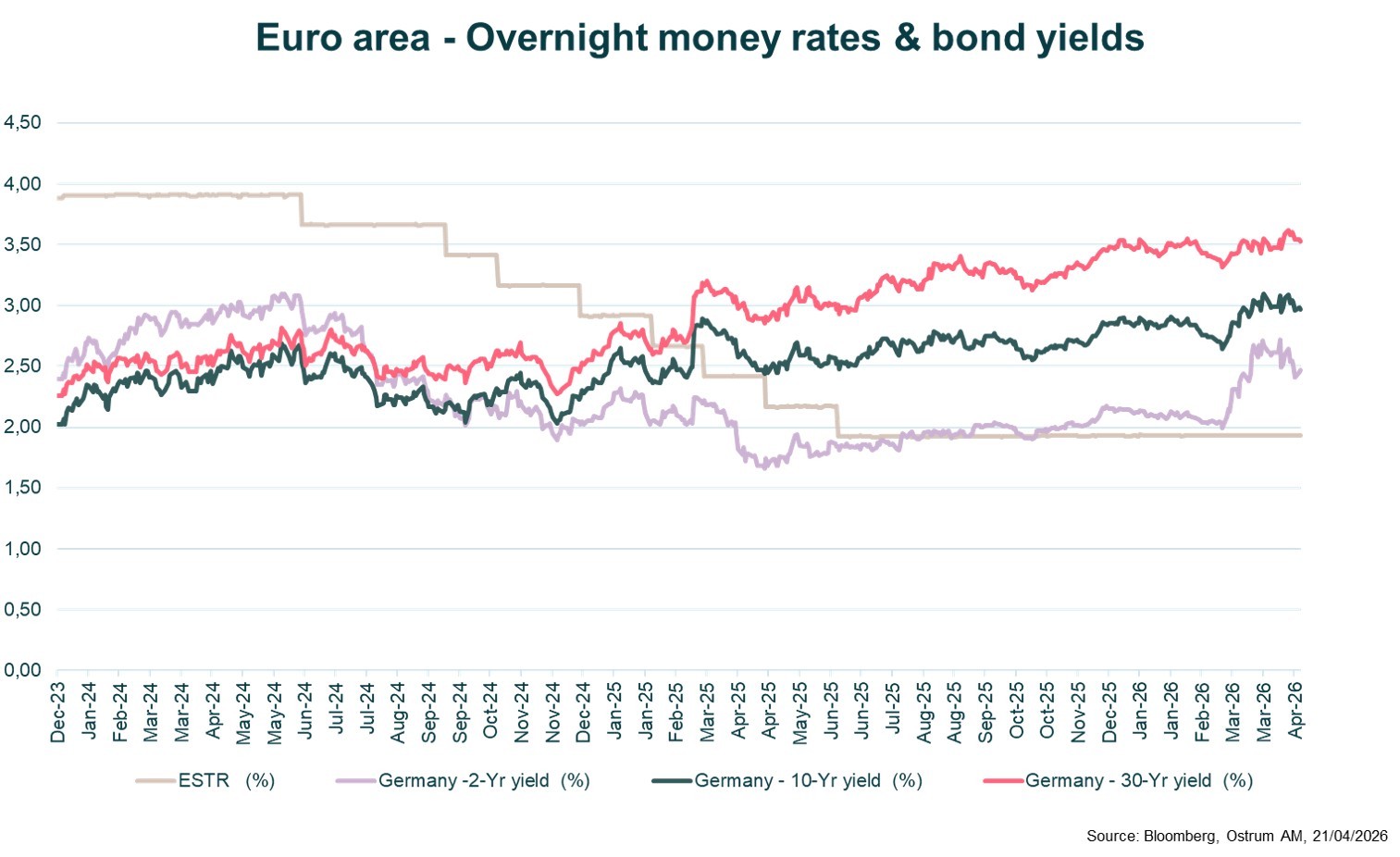

In this context, the ECB appears determined to raise rates twice, validating ex-post the rise in market expectations. This is a free option for the ECB, which is concerned about guaranteeing the stability of inflation expectations.

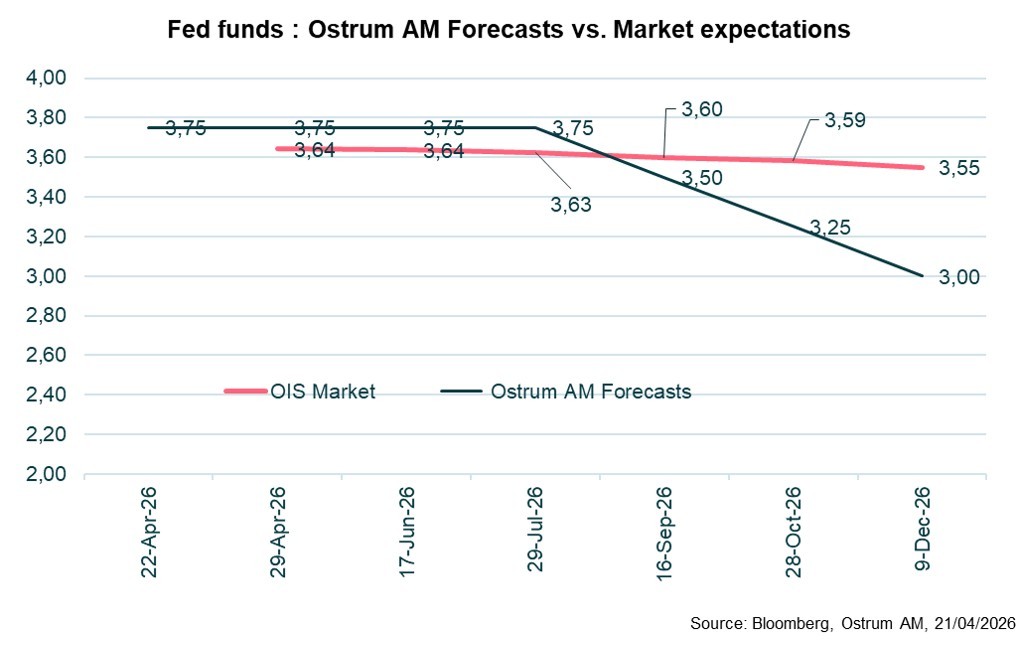

The Fed will maintain monetary status quo while remaining attentive to labor market developments. The handover between Jerome Powell and Kevin Warsh suggests that rate adjustments will not occur before the end of the year. In the markets, the initial shock did not trigger a drift in long-term inflation expectations, so long-term rates have remained moderate.

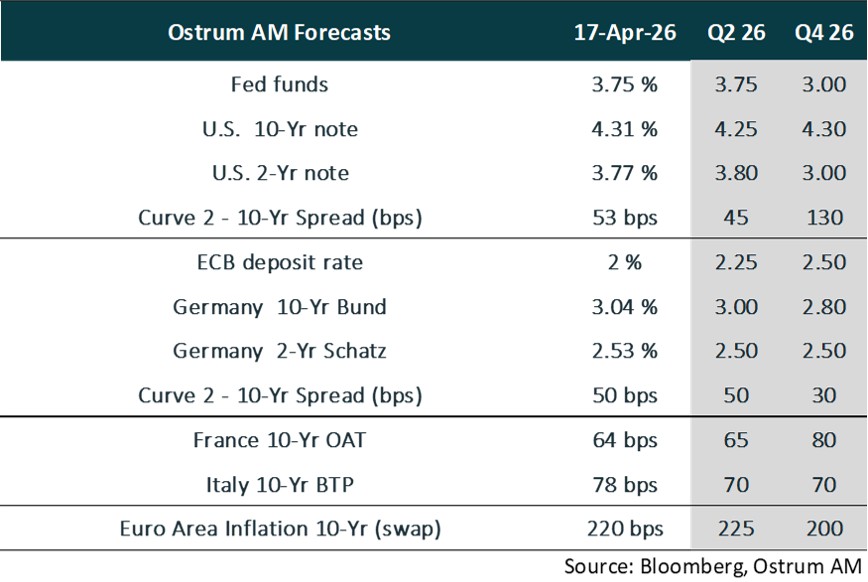

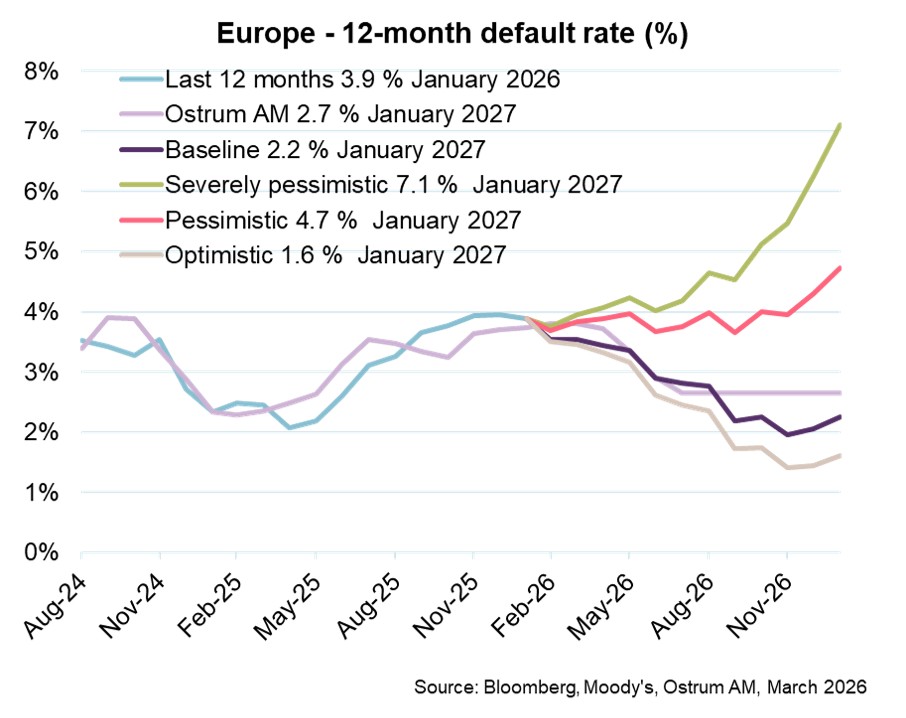

Our year-end projections of 4.30% on the T-note and 2.80% on the Bund have not changed. Market resilience is impressive. Sovereign and credit spreads have already erased the Iranian crisis, and the valuation problem will arise again, including on high yield. The default rate remains low, although it is worth monitoring the impact of the U.S. private credit market. On equities, earnings revisions are modest, and even upward in the United States thanks to the energy sector. The equity rebound will continue.

KEY INDICATORS

3 MONTH OUTLOOK ON BOND MARKETS

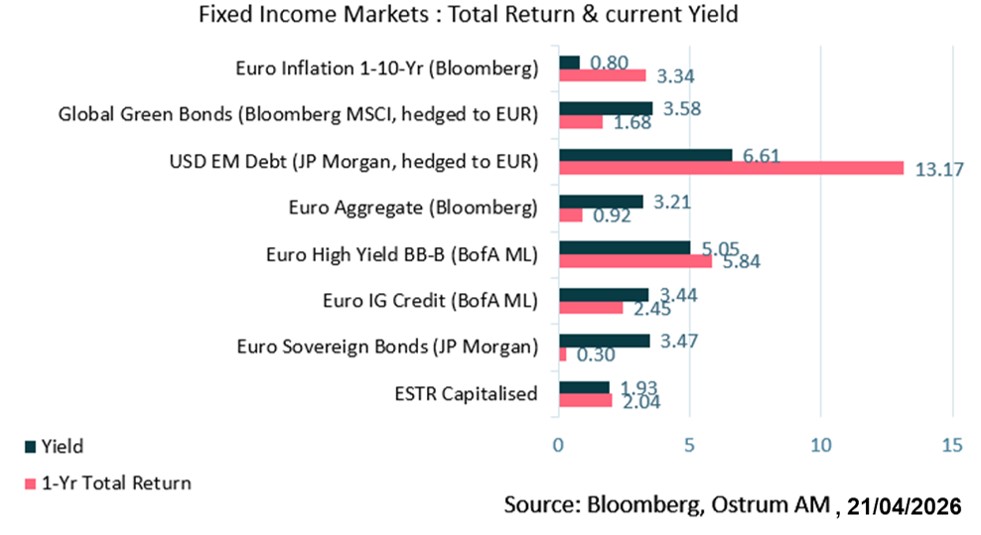

FIXED INCOME RETURNS & PERFORMANCES

GROWTH & INFLATION

GROWTH

- U.S. growth weakened at the end of the year with the shutdown and a stalled labor market. Rising oil prices are weighing on household consumption, but AI investments continue to stimulate activity.

- According to surveys, the eurozone is experiencing a moderate recovery despite the oil shock.

- In China, domestic demand is showing some signs of stabilization. Investment remains under pressure due to the policy of reducing overcapacity. The blockade of the Strait of Hormuz is creating difficulties for supply chains beyond oil.

INFLATION

- In the United States, the CPI now incorporates rising energy prices (3.3% in March). Core inflation remains stable at 2.6%.

- In the eurozone, inflation stands at 2.6% in March. Price adjustments are expected to continue, with the HICP likely to approach 3% in Q2. Excluding volatile items, inflation has stabilized around 2.3% over the past year.

- In China, inflation is recovering from very low levels. The CPI stands at 1%. Producer price deflation is moderating thanks to rising metal prices and anti-involution measures.

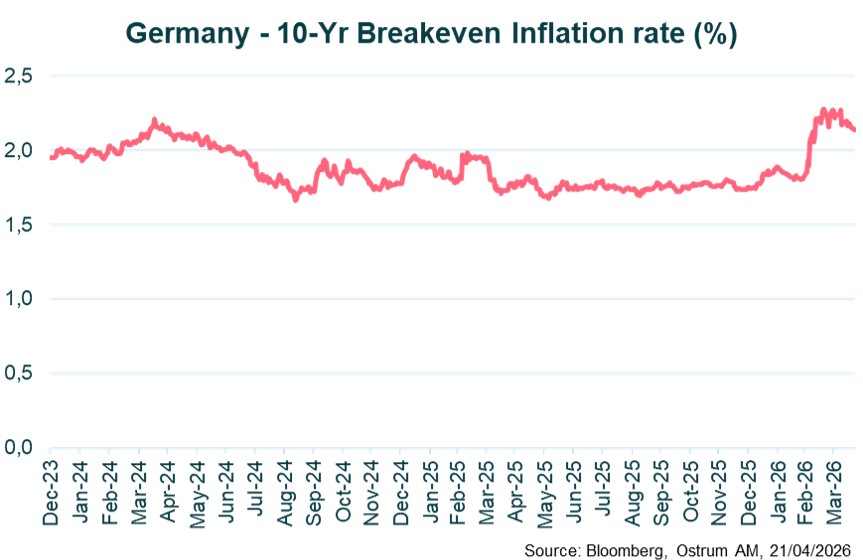

Eurozone inflation: Long-term inflation expectations have increased due to the oil price shock. This inflation risk premium is expected to diminish in the second half of the year.

CENTRAL BANKS RATES

MONETARY POLICIES

FED AND ECB CAUTIOUS GIVEN UNCERTAINTY SURROUNDING ENERGY SHOCK

Fed easing postponed

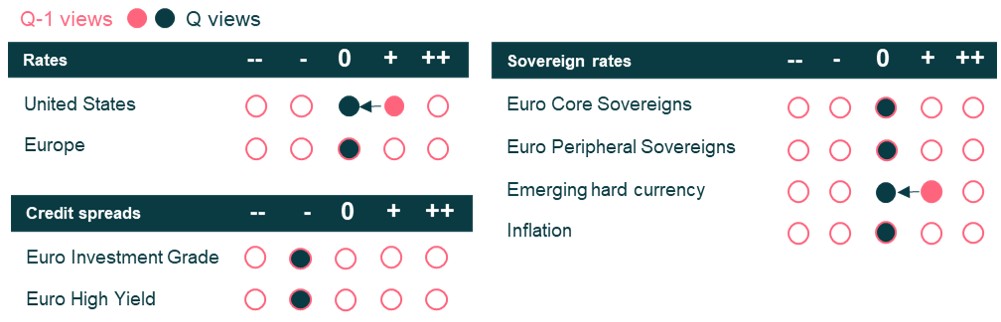

The Fed left its rates unchanged for the second consecutive time on March 18. Growth forecasts were slightly revised upward to 2.4% from 2.3% for 2026 (Q4/Q4), as were inflation projections (2.7% versus 2.4%). The unemployment rate is expected to remain at 4.4% (unchanged). FOMC members continue to anticipate, on average, one rate cut this year and another in 2027. The Fed Minutes revealed a committee divided on how to respond to sustained high energy prices. Most members believe a rate cut would be necessary to support the labor market, while several lean toward raising rates to counter higher inflation. We believe the Fed should prioritize the continued deterioration of the labor market and cut rates three times this year, starting in September.

The ECB is expected to raise its rates to well anchor inflation expectations

At the March 19 meeting, the ECB left its rates unchanged and proved highly reactive by incorporating data up to March 11 in its forecasts, thus integrating part of the energy price increases linked to the Middle East conflict. Inflation was thus significantly revised upward for 2026 (2.6% versus 1.9% anticipated in December) before returning to 2% in 2027 and 2.1% in 2028. Growth was revised downward for 2026 and 2027 (0.9% and 1.3%). The ECB also published two alternative scenarios due to high uncertainty. On March 25, Christine Lagarde stated that if the energy shock resulted in a significant but not overly persistent overshooting of the inflation target, a monetary policy adjustment could be justified, especially since not reacting could pose a communication risk. The memory of inflation is moreover recent, unlike in 2022, which could generate more significant second-round effects. For these reasons, we believe the ECB should raise its rates by 25 basis points in June and September to demonstrate its unconditional determination to bring inflation back toward the 2% target in the medium term.

INTEREST RATES INDICATORS

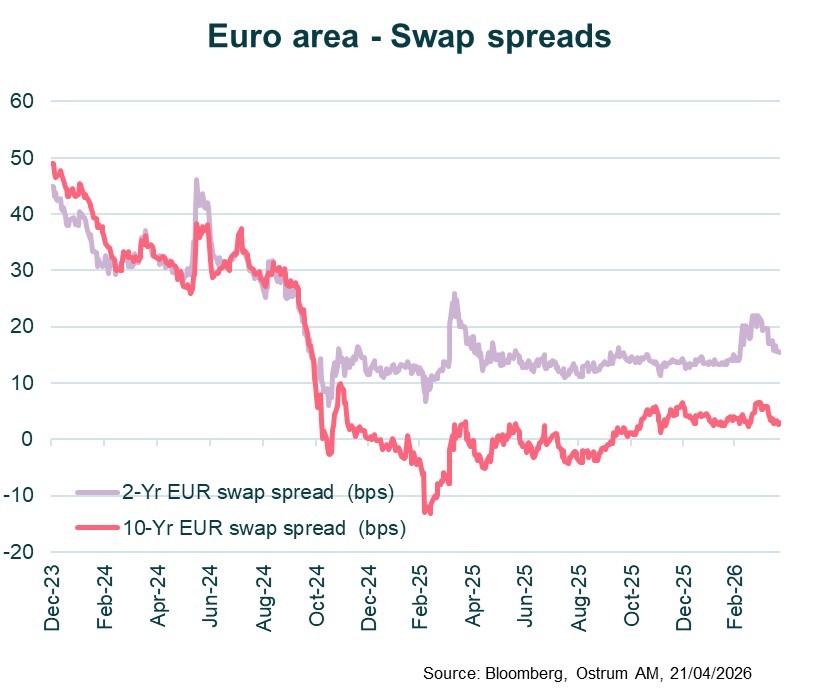

EURO SOVEREIGN BONDS

- U.S. Rates: The inflation shock complicates the Fed's task. We anticipate monetary easing to resume towards the end of the year.

- European Rates: The ECB is expected to hike twice by the end of the year to anchor inflation expectations. The 10-year Bund yield is projected to fluctuate around 3%.

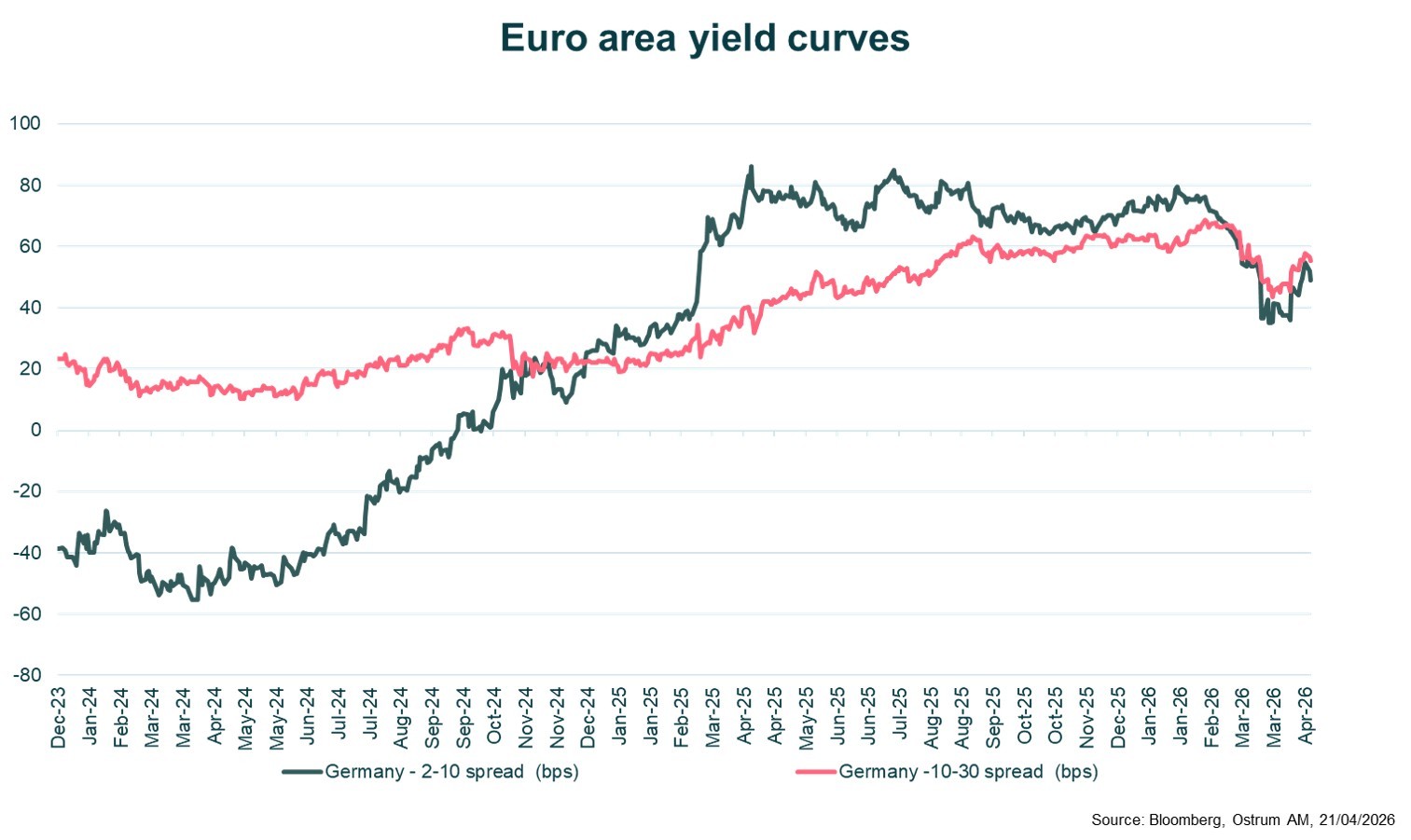

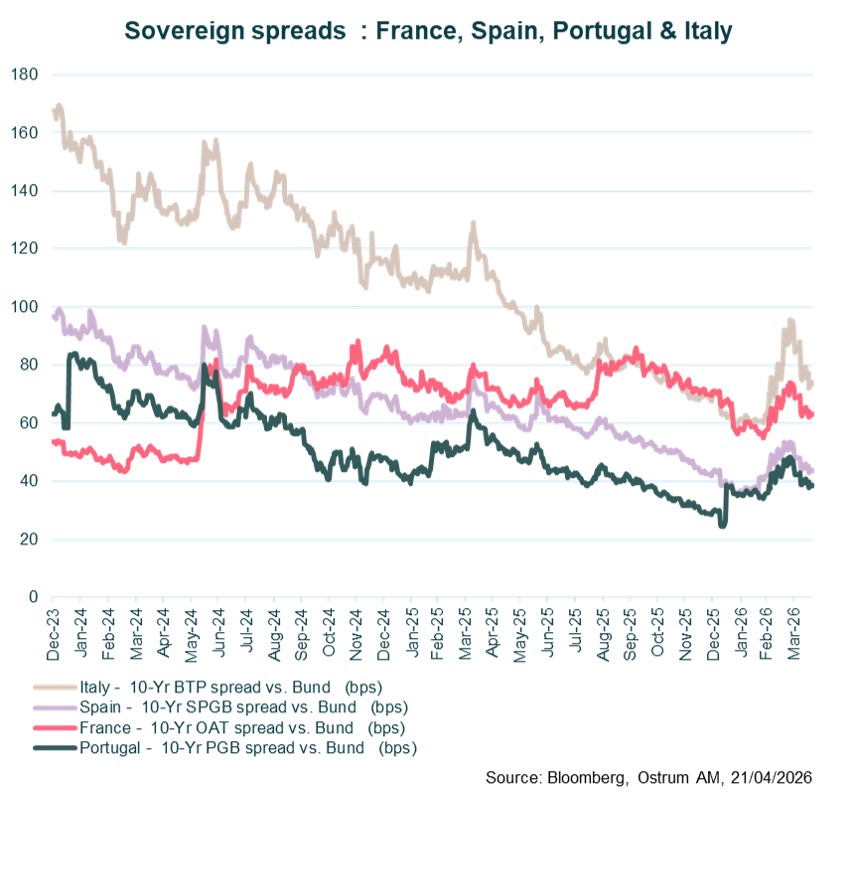

- Sovereign Spreads: Sovereign spreads are modestly higher amid the Iranian crisis. However, political risk in France is expected to weigh on OATs later in the year. Italy's spread is likely to resume tightening, reversing its recent underperformance.

- Broad market decline: The Euro Area All Maturities index posted -0.64% in Q1 2026, reflecting challenging conditions across European sovereign debt markets with widespread negative returns.

- Maturity class divergence: Short-term bonds (1-3 years) showed relative resilience at -0.44%, while medium-term segments (5-10 years) suffered the worst performance (-0.88% to -0.89%), and long-term bonds (10+ years) recovered to -0.45%.

- Core vs peripheral divide: Netherlands was the only positive performer at +0.05%, with core countries (Germany -0.31%, Ireland -0.19%) significantly outperforming peripheral nations, highlighting persistent credit risk differentials within the Eurozone.

- Southern Europe weakness: Peripheral countries experienced severe underperformance, led by Italy (-1.52%) and Greece (-1.44%), while Portugal (-0.78%) also lagged, indicating heightened geopolitical risk concerns in Q1 2026.

EMERGING BONDS

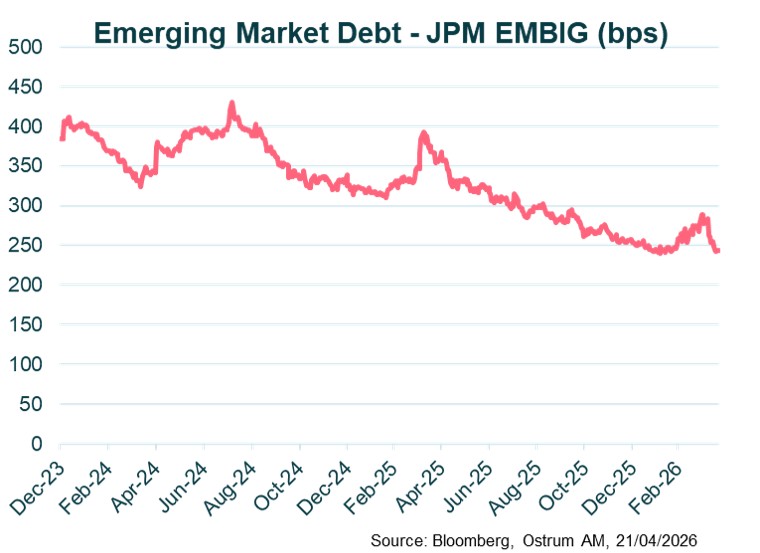

The EMBI Global Diversified (EMBIG) is showing resilience amidst the Iranian crisis. The trend of spread tightening is expected to resume.

Asset class convergence

- Broad market decline: The EMBIG index fell -1.26% in Q1 2026 with spreads widening 14 bps, reflecting deteriorating sentiment toward emerging market debt amid challenging global conditions.

- Asset class convergence: EM High Grade (-1.27%) and High Yield (-1.28%) bonds performed similarly poorly, while Next Generation EM bonds (-0.75%) showed relative resilience, and US Treasuries (+0.04%) provided modest positive returns.

- Duration effect dominance: Short-term 1-3 year bonds (+2.10%) dramatically outperformed all other maturities, while long-term 10+ year bonds (-2.70%) suffered the worst losses, indicating significant yield curve steepening pressures.

- Credit spread divergence: Only short-term bonds experienced spread tightening (-13 bps), while all other maturity buckets saw spreads widen between 14-35 bps, highlighting investors' preference for shorter-duration EM exposure during risk-off periods.

CREDIT INDICATORS

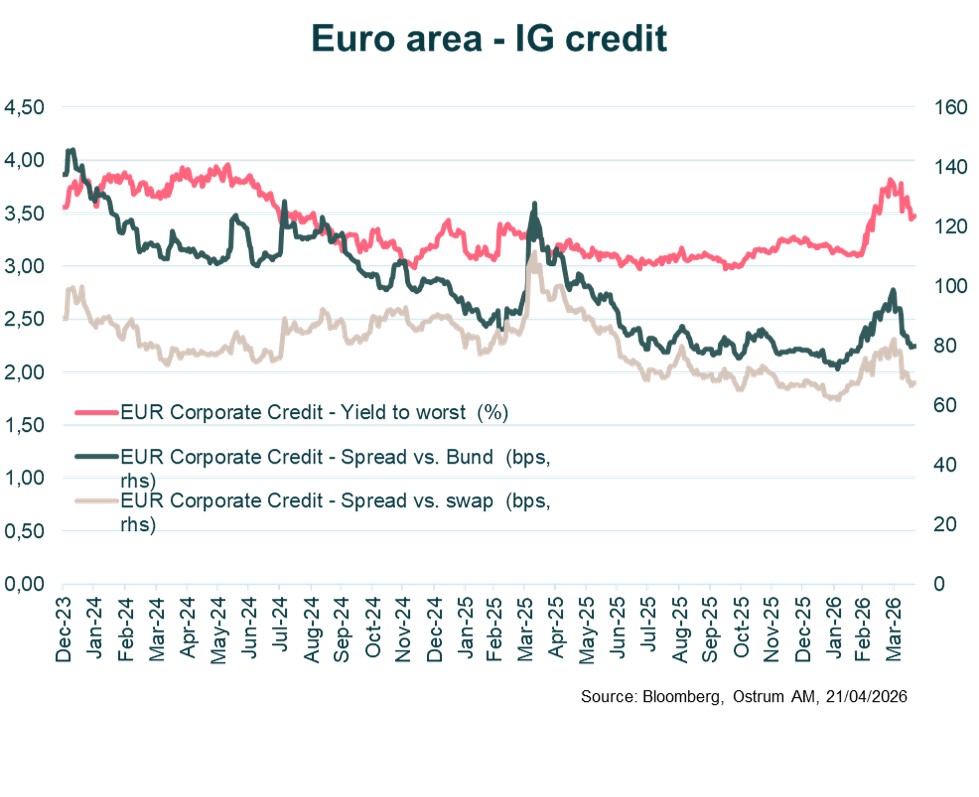

EURO INVESTMENT GRADE CREDIT

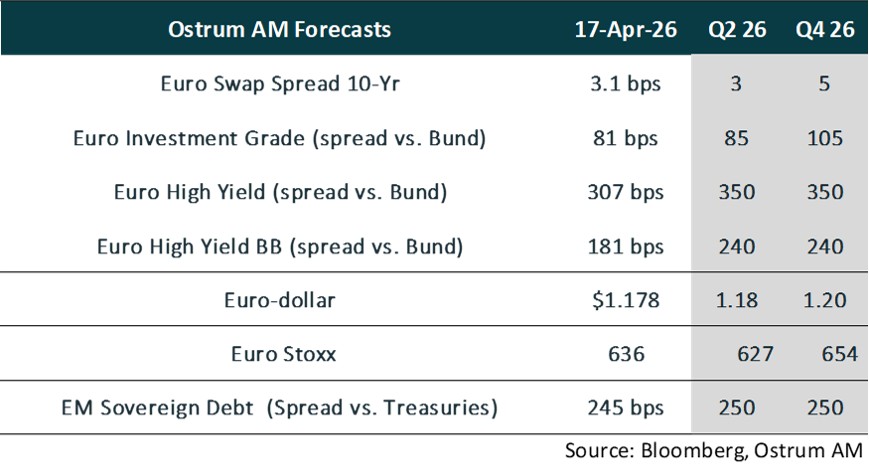

Investment-grade credit spreads have demonstrated resilience amidst the Iranian crisis and significant issuance volumes. We still expect a gradual normalization of spreads toward higher levels.

- Broad market decline: The ICE BofA ML Euro Corporate Index fell 0.95% in Q1 2026, reflecting challenging conditions across European corporate credit markets with universal negative returns across all sectors.

- Sector performance hierarchy: Energy (-0.72%) emerged as the most resilient sector, while Real Estate (-1.49%) suffered the worst decline, with Financial (-0.89%) slightly outperforming Industrial (-1.01%) sectors overall.

- Financial sector subordination impact: Within financials, Banking (-0.84%) significantly outperformed Insurance (-1.16%), while credit quality mattered with Senior Banking (-0.81%) leading and Junior Subordinated securities (-1.18%) posting the worst performance.

- Industrial sector broad weakness: Industrial subsectors showed wide dispersion, with defensive sectors like Transportation (-0.82%) and Services (-0.83%) holding up better than cyclical areas like Technology & Electronics (-1.38%) and Leisure (-1.29%).

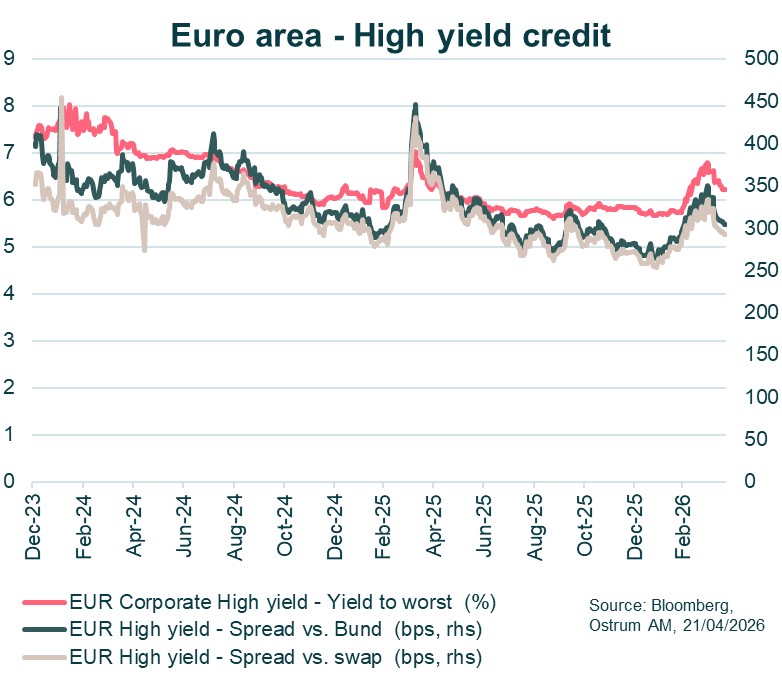

EURO HIGH YIELD CREDIT

Valuations in the high yield segment are expected to normalize over the course of the year. However, the default rate remains contained and below average.

Industrial sector weakness

- Broad market decline: The Pan-European High Yield index fell -1.50% in Q1 2026, reflecting significant stress in the European leveraged credit markets with widespread negative returns across all sectors and rating categories.

- Performance linked to credit quality: Lower-rated bonds suffered the most, with CCC-rated securities (-2.31%) declining nearly twice as much as BB-rated bonds (-1.24%), indicating investors' flight from higher-risk credits during the quarter.

- Sector performance dispersion: Energy (-0.96%) showed relative resilience as the best-performing sector, while Real Estate (-2.10%) and Leisure (-2.09%) experienced severe declines, suggesting sector-specific fundamental concerns beyond broad market weakness.

- Industrial sector weakness: Within industrials, most subsectors clustered around -1.4% to -1.6%, with Basic Industry (-1.39%) and Technology (-1.43%) showing slight outperformance compared to Capital Goods (-1.57%) and Chemicals (-1.61%), indicating broad-based cyclical concerns.

FOCUS ON SUSTAINABLE BONDS

QUARTERLY GRAPH

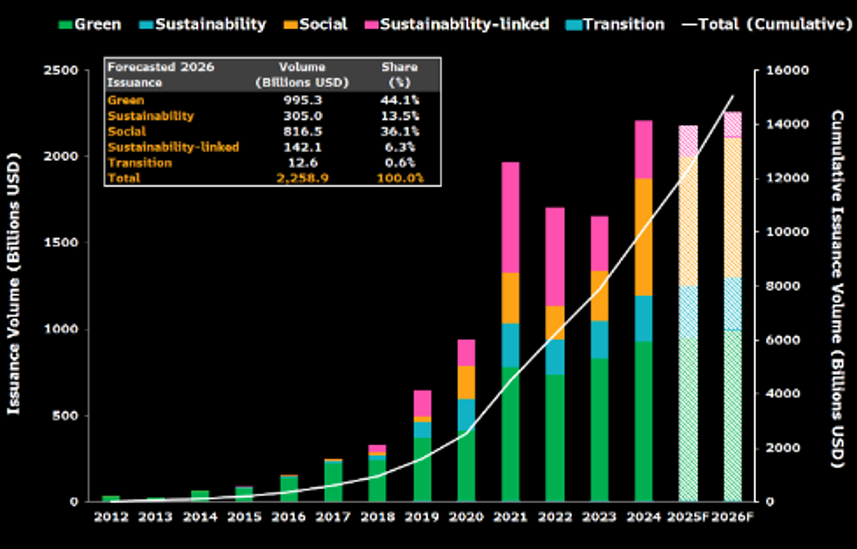

Global Sustainable Debt* Issuances

Global sustainable debt* issuances are expected to exceed $2 trillion for the third consecutive year in 2026, primarily driven by green and social bonds.

Source: Bloomberg Intelligence, October 2025.

*Sustainable debt includes bonds, loans and securitized products.

- 1% of the global population generates nearly 50% of aviation CO2 emissions. This concentration highlights a striking inequality: a small group of frequent travelers accounts for the bulk of the climate impact. According to the International Air Transport Association, about 80% of humanity has never flown. Yet air transport represents 2–3% of global CO2 emissions. The climate challenge of aviation therefore lies as much in the over- frequency of a mobile elite as in the sector’s overall volume.

- Aeroporti Di Roma issued its fourth Sustainability-Linked Bond (SLB). The company is committed to reducing its CO2e emissions (captures all greenhouse gases) both in absolute terms and on a per-passenger basis, while also increasing the share of women in leadership positions. ADR has set a target to achieve carbon neutrality by 2030 for its direct emission. However, some responsible investors remain cautious, given the company’s exposure to a highly carbon-intensive sector.

- Iberdrola, through a green bond issuance, participated in the financing of the Núñez de Balboa photovoltaic plant in Badajoz, one of the largest in Europe. With an installed capacity of 500 MW, this facility supplies clean energy to 250,000 households and notably prevents the emission of 215,000 tons of CO2 equivalent per year. It has also led to the creation of 1,200 jobs, representing approximately 70% of the workers in the region.

- Regarding concerns over the impact of Artificial Intelligence (AI) on employment, a study by the European Central Bank (ECB) reveals nuanced effects. Companies that intensively use AI are 4% more likely to hire, particularly smaller firms, to support these technologies. Those planning to invest in AI also anticipate workforce growth. Only 15% of companies employ AI to reduce labor costs. However, this specific usage is associated with a higher number of layoffs. AI therefore presents both an opportunity for job creation and a risk for certain sectors.

DASHBOARD - OSTRUM AM VIEWS

MACROECONOMIC OUTLOOK • EUROZONE AND UNITED STATES

MARKET VIEWS