Gold: A Post-Dollar World

Political tensions in Latin America, the Middle East, and the Arctic continue to fuel a fragile global environment, reinforcing gold’s status as a safe-haven asset. However, the appeal of the precious metal goes beyond mere risk protection. It reflects a broader transition in monetary power. The US dollar established itself as the world’s reserve currency by displacing the pound sterling—a process that took nearly forty years and relied on a strategic accumulation of gold.

Before the First World War, the United Kingdom was the world’s financial center, and British government bonds were considered the safest asset globally. Sterling was then the dominant reserve currency. The United States had accumulated substantial holdings of British sovereign debt, fully integrated into the prevailing financial system. Between 1914 and 1917, the United States became an industrial power and began to reduce its exposure to British debt amid concerns over the financing of the war effort, converting large volumes of these assets into gold and US Treasuries. From 1919 onward, the United States emerged as the world’s main creditor, and the dollar established itself as the new international monetary benchmark.

China appears to be embarking on a comparable transition. It has been gradually reducing its holdings of US Treasuries, from $1.3 trillion in November 2013 to just over $600 bn in November 2025. At the same time, the People’s Bank of China has significantly increased its gold reserves, which have reached a record level and now represent close to 11% of total reserves—still below the 15% threshold often cited as a benchmark.

More recently, Chinese regulators have instructed financial institutions to further limit their exposure to US Treasury securities, a clear signal of the authorities’ intention to strengthen the resilience of its banking system and reduce its dependence on the dollar. Beijing is preparing for a world in which the global monetary equilibrium may be fundamentally reshaped.

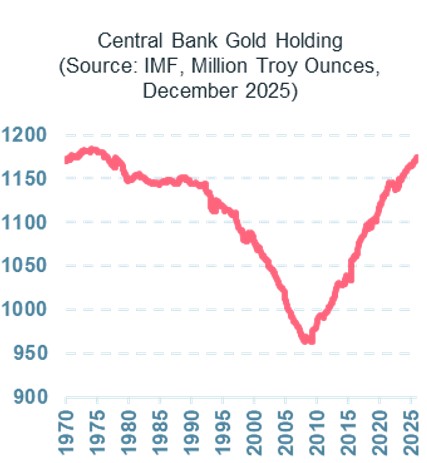

In Search of Independence

While the rise in gold prices has been particularly striking since 2025, the share—and therefore the role—of gold in the foreign exchange reserves of emerging market central banks has been following a remarkable upward trend for some time now (see chart below).

This trajectory in gold holdings is marked by a major inflection point in 2008–2009, driven by multiple factors that were amplified during the global financial crisis: the Federal Reserve’s rate cuts aimed at supporting the economy, the depreciation of emerging market currencies, episodes of domestic confidence crises, as well as heightened geopolitical tensions and, in some cases, sanctions imposed on sovereign states. These developments have significantly reshaped the strategies of emerging market central banks, with the objective of enhancing resilience and achieving a greater degree of independence from the US dollar.

The second term of Donald Trump and the shocks triggered by his policy decisions have only reinforced this trend. Beyond the increased share of gold in their reserves, emerging market central banks are now also benefiting from a significant price effect.

This has become one of the key pillars underpinning the resilience of emerging market currencies and providing central banks with greater autonomy in the conduct of their monetary policies.

Gold is a powerful diversification asset than helps manage risk

Gold can be analyzed at two distinct levels for an investor:

1) a purely speculative asset aimed at maximizing profits,

2) a strategic diversification component to optimize the Sharpe ratio.

In the first case, the entry point is paramount. Today, projecting gold’s price on its historical drivers – supply and demand, real rates, the US dollar, inflationary pressures, monetary policy, risk appetite, political uncertainty – the fair value would seem closer to $4,000 per ounce than $5,500.

Gold appears overvalued and the risk of a pullback is high. That does not mean the potential is zero: if cyclical drivers warrant short‑term caution, more structural drivers such as geopolitical fragmentation and rising public debt prompt greater diversification of official reserves away from government bonds. This paradigm shift could support gold’s price above its historical fair value for the long term.

In the second case, gold is used to manage risk and timing is less critical. Efficient frontier studies show that a positive exposure to gold can optimize the risk–return pair of a diversified portfolio, especially if gold is paired with the US dollar. The target is about 7% for a conservative risk profile (volatility below 5%).

Investing in gold and the US dollar within a portfolio provides protection against macroeconomic and/or systemic shocks and dampens volatility.

It can also offer a credible alternative to equities when the environment remains favorable for risky assets but valuations are near cycle-end levels, as it is the case today.

Ostrum’s Multi-Asset Quant strategies are currently invested in gold via “gold producers” ETFs.