Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum AM's views on the economy, strategy and markets.

Outlook at 04/17/2026.

The CIO letter

Markets ignore the war

The closure of the Strait of Hormuz should concern investors given the crucial importance of this passage for oil and gas trade. Conversely, the announcement of negotiations between Iran and the United States, though fruitless at this stage, immediately triggered an equity rebound. War-related losses have been erased. The oil shock has had limited impact on activity according to initial surveys, so the economic recovery is not in question in Europe. In the United States, the weakening of household consumption since autumn is a point of concern, but AI investment is preventing a sharp slowdown. China, highly exposed to the Gulf, seems to be accommodating higher oil prices thanks to its energy mix and export capacity. Downward revisions to growth and inflation are ultimately modest.

In this context, the ECB appears determined to raise rates twice, validating ex-post the rise in market expectations. This is a free option for the ECB, which is concerned about guaranteeing the stability of inflation expectations. The Fed will maintain monetary status quo while remaining attentive to labor market developments. The handover between Jerome Powell and Kevin Warsh suggests that rate adjustments will not occur before the end of the year. In the markets, the initial shock did not trigger a drift in long-term inflation expectations, so long-term rates have remained moderate. Our year-end projections of 4.30% on the T-note and 2.80% on the Bund have not changed. Market resilience is impressive. Sovereign and credit spreads have already erased the Iranian crisis, and the valuation problem will arise again, including on high yield. The default rate remains low, although it is worth monitoring the impact of the U.S. private credit market. On equities, earnings revisions are modest, and even upward in the United States thanks to the energy sector. The equity rebound will continue.

Economic Views

THREE THEMES FOR THE MARKETS

-

Growth

U.S. growth weakened at the end of the year with the shutdown and a stalled labor market. Rising oil prices are weighing on household consumption, but AI investments continue to stimulate activity. According to surveys, the eurozone is experiencing a moderate recovery despite the oil shock. In China, domestic demand is showing some signs of stabilization. Investment remains under pressure due to the policy of reducing overcapacity. The blockade of the Strait of Hormuz is creating difficulties for supply chains beyond oil.

-

Inflation

In the United States, the CPI now incorporates rising energy prices (3.3% in March). Core inflation remains stable at 2.6%. In the eurozone, inflation stands at 2.6% in March. Price adjustments are expected to continue, with the HICP likely to approach 3% in Q2. Excluding volatile items, inflation has stabilized around 2.3% over the past year. In China, inflation is recovering from very low levels. The CPI stands at 1%. Producer price deflation is moderating thanks to rising metal prices and anti-involution measures.

-

Monetary policy

The Fed left monetary policy unchanged in March. The downward adjustment of rates is expected to resume at the end of the year, given the likely rise in unemployment despite the inflationary episode. The ECB will likely raise rates twice in line with market expectations to ensure the anchoring of inflation expectations. The PBOC may postpone its rate cuts to the second quarter, awaiting more data to gauge the state of the Chinese economy.

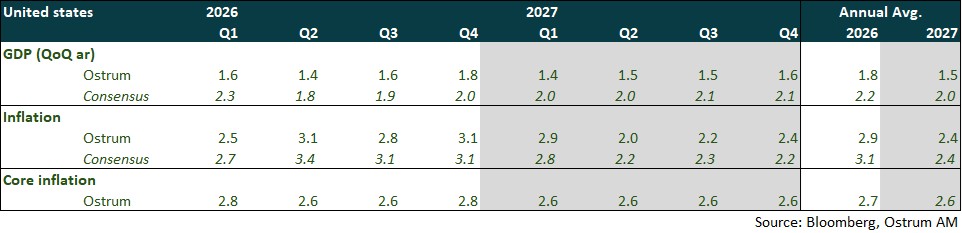

ECONOMY: UNITED STATES

In the US, the oil shock is less severe than in Asia or Europe, but household consumption is weakening. AI remains the sole source of growth while the labor market has stalled.

- Demand: Household consumption is suffering from the oil shock and wage deceleration (3.5% in March). The trade balance is widening, continuing the trend from late 2025, driven particularly by corporate investment in AI. Housing investment will contract further in 2026 due to a shortage of available properties and high prices. Public spending is rebounding mechanically after the Q4 shutdown. Military expenditures will recover in Q2.

- Labor Market: The labor market is sluggish. The stable unemployment rate in Q1 primarily reflects weak participation. Job openings are below the number of unemployed (labor supply surplus). Job placement for graduates is extremely difficult.

- Fiscal Policy: Tax refunds have begun, but the oil shock will erase two-thirds of the purchasing power increase. A $200 billion budget supplement is being requested from Congress, risking an increase in the federal deficit to 7% of GDP.

- Inflation: Disinflation is confronting a significant oil shock for consumers. Core inflation remains close to 3% (PCE). However, housing remains a source of disinflation.

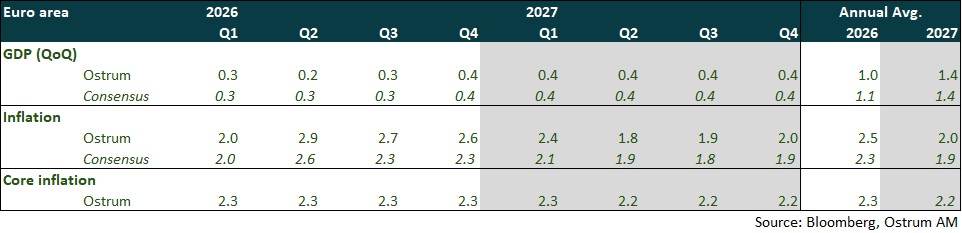

ECONOMY: EURO AREA

The conflict in the Middle East is making forecasts more uncertain and dependent on its duration. As Europe is a net importer of oil and gas, rising energy prices will translate into more moderate growth and higher inflation in 2026.

- Domestic Demand: the first effects of the energy shock are beginning to be observed through the decline in household confidence and new orders placed with businesses. This will partially offset the impact of the implementation of German plans, the rise in military spending in Europe, as well as the disbursements from NextGenerationEU. Growth has been slightly revised downwards for 2027 due to the ECB's anticipated interest rate hikes in 2026.

- External Demand: Foreign trade is expected to make only a small contribution to growth. Tariff uncertainty should persist, and Germany will continue to face increased competition from China.

- Fiscal Policy: Germany, after years of fiscal prudence, will significantly increase its spending on infrastructure and defense. In France, the budget deficit will remain the highest in the Eurozone in 2026 (the government's target is 5%). The approach of the 2027 presidential election will make compromises even more difficult to achieve in the autumn of 2026. Measures to limit the impact of rising energy prices are being taken by some countries (Italy, Spain, Portugal, etc.). The longer energy prices remain high, the greater the risk of a fiscal slippage.

- Inflation: The acceleration of inflation to 2.6% in March is linked to energy prices. It is expected to continue accelerating in the second quarter with the spillover to other sectors of the economy before moderating, in line with energy prices. The impact on underlying inflation should be limited. The ECB states it is agile and vigilant and will ensure inflation expectations are well contained in the medium term.

ECONOMY: CHINA

The end of deflation in China leads us to accentuate the inflation profile for Q2 and Q3.

- Global Scenario 2026-2027: At this stage, we are not revising our growth forecasts as China has adopted a pragmatic approach to counter risks linked to the Middle East conflict. Its coal-dominated energy mix (61%), substantial oil reserves (1.4 million barrels), trade surplus, and domestically oriented sectors provide cushioning effects. Having revised our inflation forecasts upward, we are accentuating the profile for Q2 and Q3 to 1.2% and 1.3% respectively.

- Inflation: The sharp rebound in input costs reflected in March PMI surveys, driving selling prices higher, has prompted us to revise our Q2 and Q3 forecasts upward. Encouraging signals from the anti-involution policy should also support producer prices. China is on the path to exiting deflation but must strengthen support for domestic demand to make it sustainable.

- Exports: China benefits from a diversified energy mix and robust supply chains, as well as low dependence on foreign inputs. Its exports should remain resilient, as during the 2020 pandemic.

- Consumption: An initial strengthening of domestic demand has emerged through signals of stabilization in the real estate sector. Official rhetoric continues to emphasize rebalancing growth toward consumption. The yuan's appreciation against the dollar should strengthen.

- Investment: The objective of technological self-sufficiency implies accelerated investment in AI domains where China aims to become the global leader. The anti-involution policy should rapidly improve private enterprise margins.

Monetary Policy

Fed and ECB cautious given uncertainty surrounding energy shock

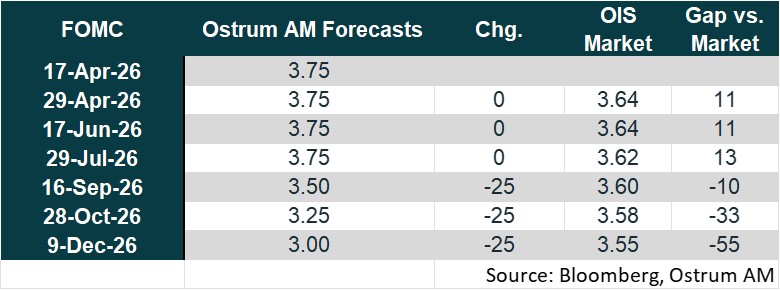

- FED EASING POSTPONED

The Fed left its rates unchanged for the second consecutive time on March 18. Growth forecasts were slightly revised upward to 2.4% from 2.3% for 2026 (Q4/Q4), as were inflation projections (2.7% versus 2.4%). The unemployment rate is expected to remain at 4.4% (unchanged). FOMC members continue to anticipate, on average, one rate cut this year and another in 2027. The Fed Minutes revealed a committee divided on how to respond to sustained high energy prices. Most members believe a rate cut would be necessary to support the labor market, while several lean toward raising rates to counter higher inflation. We believe the Fed should prioritize the continued deterioration of the labor market and cut rates three times this year, starting in September.

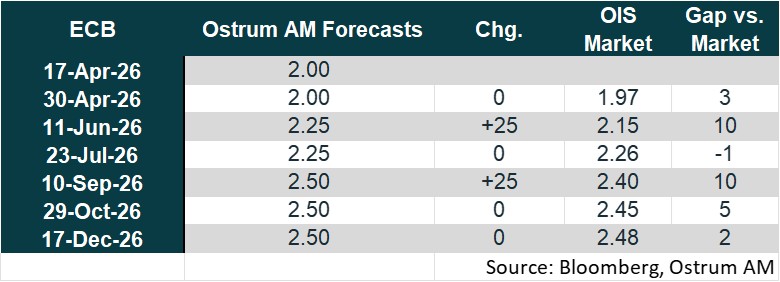

- A VIGILANT ECB

At the March 19 meeting, the ECB left its rates unchanged and proved highly reactive by incorporating data up to March 11 in its forecasts, thus integrating part of the energy price increases linked to the Middle East conflict. Inflation was thus significantly revised upward for 2026 (2.6% versus 1.9% anticipated in December) before returning to 2% in 2027 and 2.1% in 2028. Growth was revised downward for 2026 and 2027 (0.9% and 1.3%). The ECB also published two alternative scenarios due to high uncertainty. On March 25, Christine Lagarde stated that if the energy shock resulted in a significant but not overly persistent overshooting of the inflation target, a monetary policy adjustment could be justified, especially since not reacting could pose a communication risk. The memory of inflation is moreover recent, unlike in 2022, which could generate more significant second-round effects. For these reasons, we believe the ECB should raise its rates by 25 basis points in June and September to demonstrate its unconditional determination to bring inflation back toward the 2% target in the medium term.

Market views

Asset classes

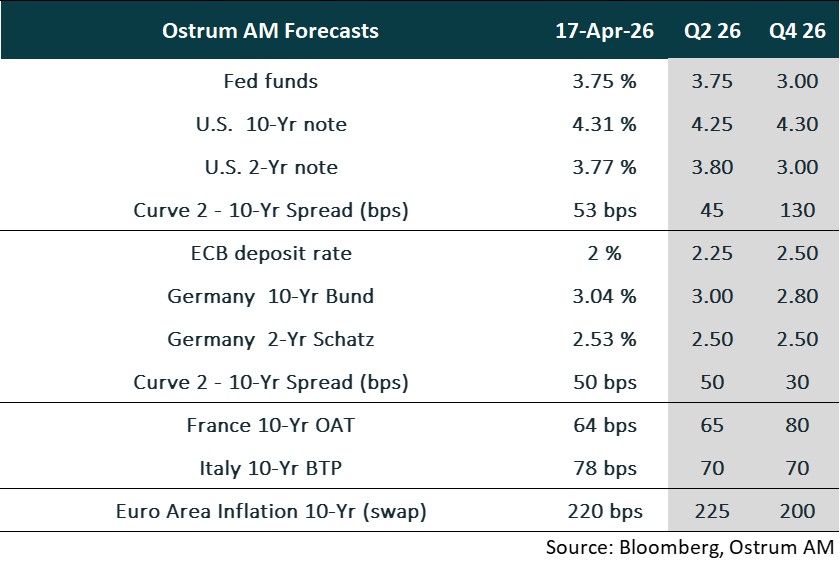

- U.S. Rates: The inflation shock complicates the Fed's task. We anticipate monetary easing to resume towards the end of the year.

- European Rates: The ECB is expected to maintain its current policy rate of 2% but stands ready to intervene should inflation expectations rise. The 10-year Bund yield is projected to fluctuate around 3% before declining towards 2.80% by year-end.

- Sovereign Spreads: Sovereign spreads are modestly higher amid the Iranian crisis. However, political risk in France is expected to weigh on OATs later in the year. Italy's spread is likely to resume tightening, reversing its recent underperformance.

- Eurozone Inflation: Long-term inflation expectations have increased due to the oil price shock. This inflation risk premium is expected to diminish in the second half of the year.

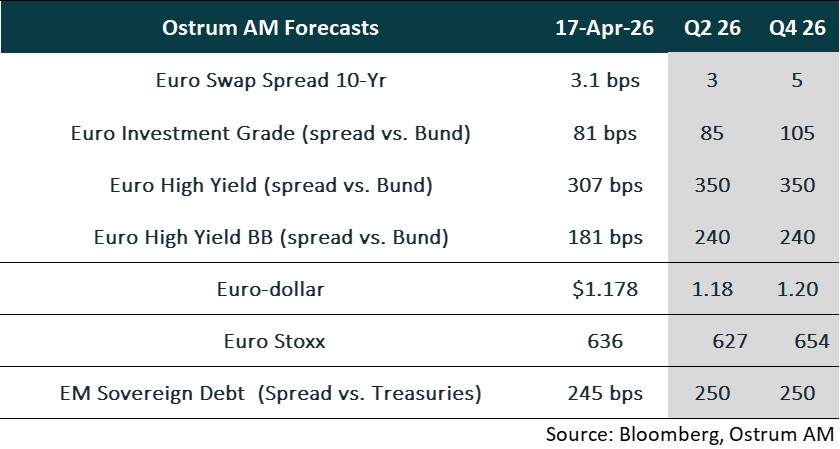

- Euro Credit: Investment-grade credit spreads have demonstrated resilience amidst the Iranian crisis and significant issuance volumes. A gradual normalization of spreads toward higher levels is still anticipated.

- Euro High yield: Valuations in the high yield segment are expected to normalize over the course of the year. However, the default rate remains contained and below average.

- Exchange Rates: The dollar has reasserted its safe-haven status during the Iranian crisis. Nevertheless, the structurally bearish trend for the greenback is expected to resume in the second half of the year.

- European Equities: Equities are being impacted by the energy crisis. Earnings revisions are likely before a rebound in profits and an increase in multiples in the latter half of the year.

- Emerging Debt: The EMBI Global Diversified (EMBIG) is showing resilience amidst the Iranian crisis. The trend of spread tightening is expected to resume