Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Listen to podcast (in French only)

(Listen to) Axel Botte’s and Aline Goupil-Raguénès’ podcast:

- Review of the week – Tech keeps pulling stock markets higher;

- Theme – The ECB leaves the door wide open for a rate hike in June.

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: The ECB leaves the door wide open for a rate hike in June

- The energy shock linked to the conflict in the Middle East has resulted in a deterioration of activity indices through business surveys and a plunge in household confidence;

- Short and medium-term inflation prospects have at the same time significantly increased, heralding even higher inflation. It stood at 3% in April;

- In this context, the ECB was particularly explicit during the April 30 meeting, indicating that a possible increase in key interest rates had been widely debated, before unanimously deciding to leave them unchanged;

- This leaves the door wide open for a rate hike in June to contain medium and long-term inflation expectations. The ECB fears that the recent memory of inflation might generate larger second-round effects, making inflation persistently high;

- It does not want to act too soon, as in 2011, or too late, as in 2022. This reinforces our anticipation of two ECB rate hikes, of 25 basis points each, the first in June, the second in September.

Intensification of downside risks to growth

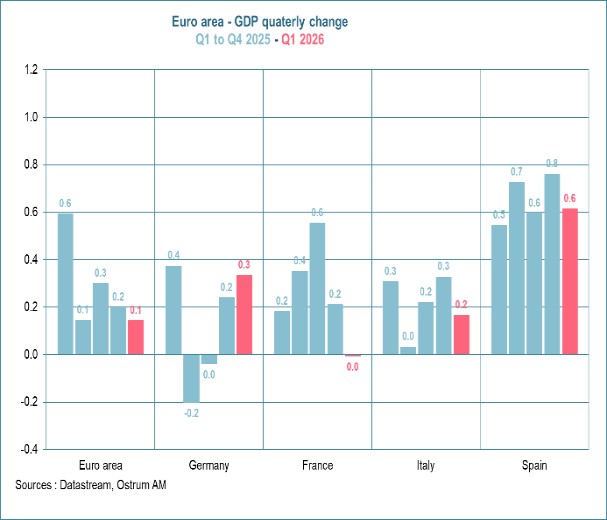

Disappointing growth in Q1

Growth moderated to 0.1% in Q1, while the conflict only began on February 28.

Even before the consequences of the conflict in the Middle East were fully felt, euro area growth proved disappointing in the first quarter. It was only 0.1%. A breakdown by component is not yet available. Among the major countries, Germany stands out with an improvement in its growth (0.3% after 0.2%). The statistical office indicates an increase in consumption (household and public) and exports. Growth moderated in Italy (0.2% after 0.3%), with the positive contribution of foreign trade being offset by the negative contribution of domestic demand (including inventories). It slowed in Spain (0.6% after 0.8%) while remaining robust. Growth, on the other hand, was sluggish in France. Only inventories contributed positively to growth, which helped offset the negative impact of foreign trade. In contrast, the contribution of domestic demand was zero, or even slightly negative, with a decline in household consumption and investment.

Deterioration of business surveys

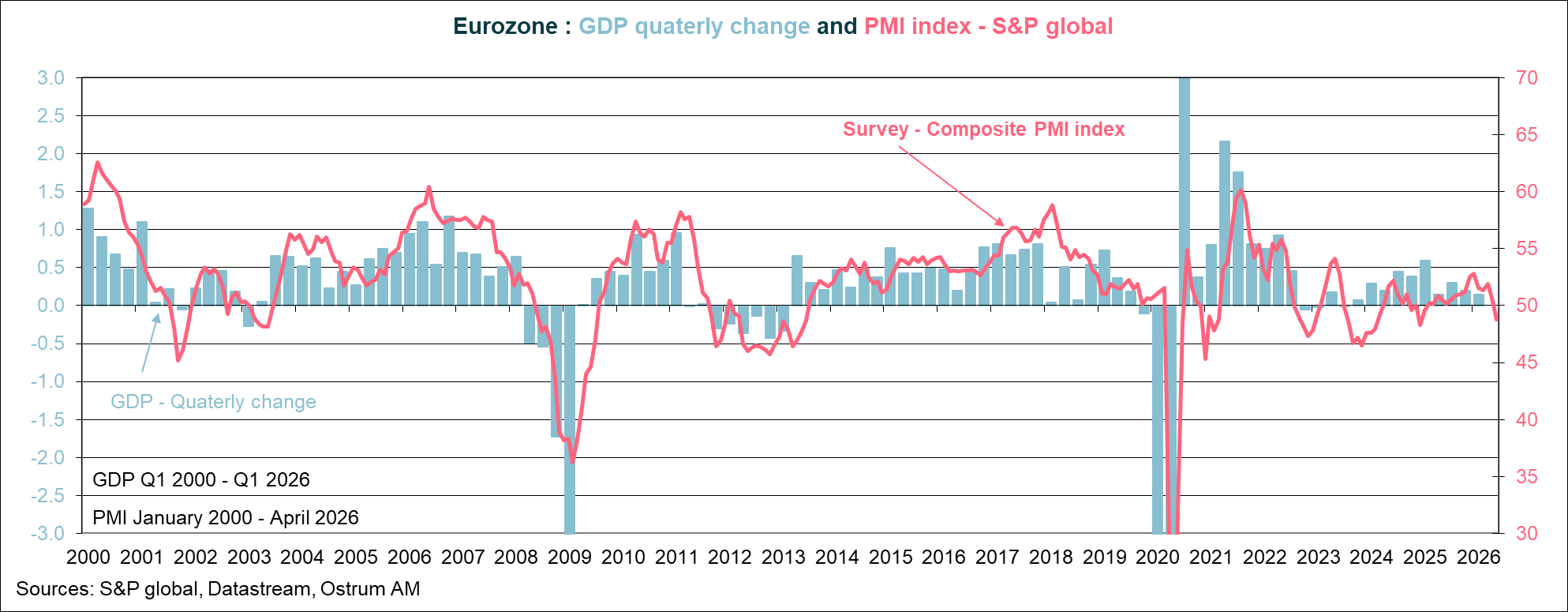

Downturn in activity according to the S&P Global survey...

The S&P Global survey signals a downturn in euro area activity in April: the composite PMI index fell below the neutral threshold of 50, at 48.8 compared to 50.7 in March. This is its lowest level since December 2024. This contraction in activity is linked to the services sector, contrasting with a slight strengthening of activity in the manufacturing sector.

The slightly more robust activity in the manufacturing sector should be put into perspective. It reflects an increase in input purchases by business leaders in order to build up inventories in anticipation of greater shortages and higher prices. The input purchasing index is at its highest since June 2022. For the same reasons, new orders improved slightly, both global and foreign. On the other hand, delivery times lengthened significantly again, reaching levels not seen since July 2022.

...linked to the services sector, which is experiencing a sharp decline in demand.

Activity in the services sector registered a marked decline according to this survey. The index lost 2.7 points to stand at 47.6, its lowest level since February 2021, when France was alternating periods of lockdown. This resulted from a sharp contraction in new orders and, even more markedly, in new foreign orders, revealing a fall in demand addressed to businesses.

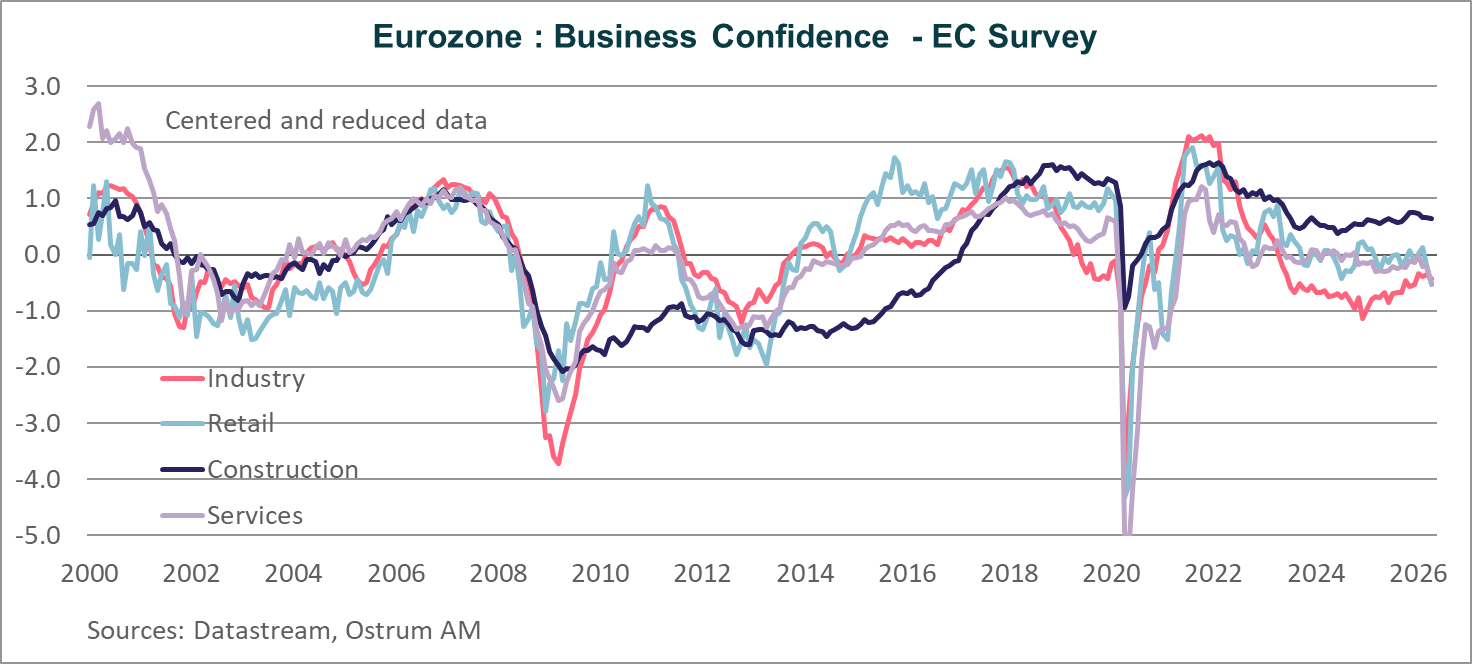

This survey was confirmed by that of the European Commission, based on national surveys. The business confidence index significantly declined in the services and retail sectors, settling below the long-term average (0 on the graph) and at lows not seen since March and April 2021. Business confidence in industry and construction, however, remained stable. While the employment component of the S&P Global survey remained unchanged in April, slightly below the 50 threshold, the EC survey revealed a sharp decline in the employment expectations index in April, following the deterioration of the activity indices. This concerned the services and retail sectors, and to a lesser extent, industry.

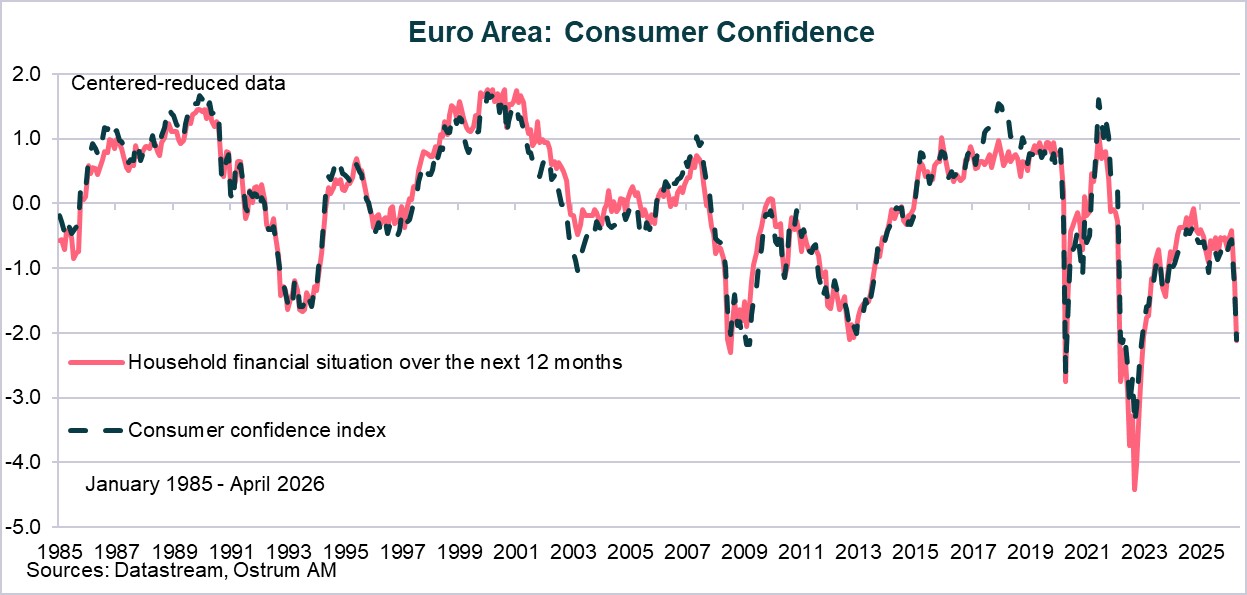

Plunge in household confidence

Household confidence plummets to lows not seen since the 2008/2009 global financial crisis and the sovereign debt crisis.

Household confidence has collapsed. The index has returned to the lowest levels seen during the 2008/2009 financial crisis and the sovereign debt crisis. They anticipate a sharp deterioration of the economic situation and their personal financial situation, as well as a rise in the unemployment rate. In this context, the "major purchases" components, both for the present and the next 12 months, have plummeted, raising concerns about a significant decline in consumption of durable goods.

Tightening of lending conditions for businesses...

Banks tighten lending conditions for businesses in Q1 and anticipate a stronger tightening in Q2 for household and business loans.

The ECB's bank lending survey revealed a tightening of credit supply conditions for businesses in the first quarter. The index is at its highest since the 3rd quarter of 2023. Perceived risks to the economic outlook and lower risk tolerance by banks are the main reasons. Banks cited geopolitical risks and concerns related to rising energy prices. Some banks reported additional tightening due to exposures to energy-intensive firms and to the Middle East. Credit supply conditions for households for real estate purchases slightly tightened, and those for consumer credit tightened more markedly. For the second quarter, banks anticipate an even greater tightening of credit conditions for businesses and households for real estate purchases. This is likely to curb the future momentum of bank loan supply and consequently weigh on investment and the consumption of durable goods.

… and decrease in loan demand

Decrease in demand for business loans to finance investment.

Demand for business loans slightly decreased in the first quarter according to this survey, due to a decline in loan demand to finance investment. This reflects a wait-and-see approach by entrepreneurs in the face of rising uncertainty. Demand for mortgage loans from households remained unchanged, while demand for consumer credit fell sharply. For the second quarter, banks anticipate a sharper decrease in loan demand from both households and businesses.

Intensification of upside risks to inflation

Acceleration of inflation to 3% in April linked to energy prices

No spillover effect at this stage, but it is likely to occur soon given the various surveys.

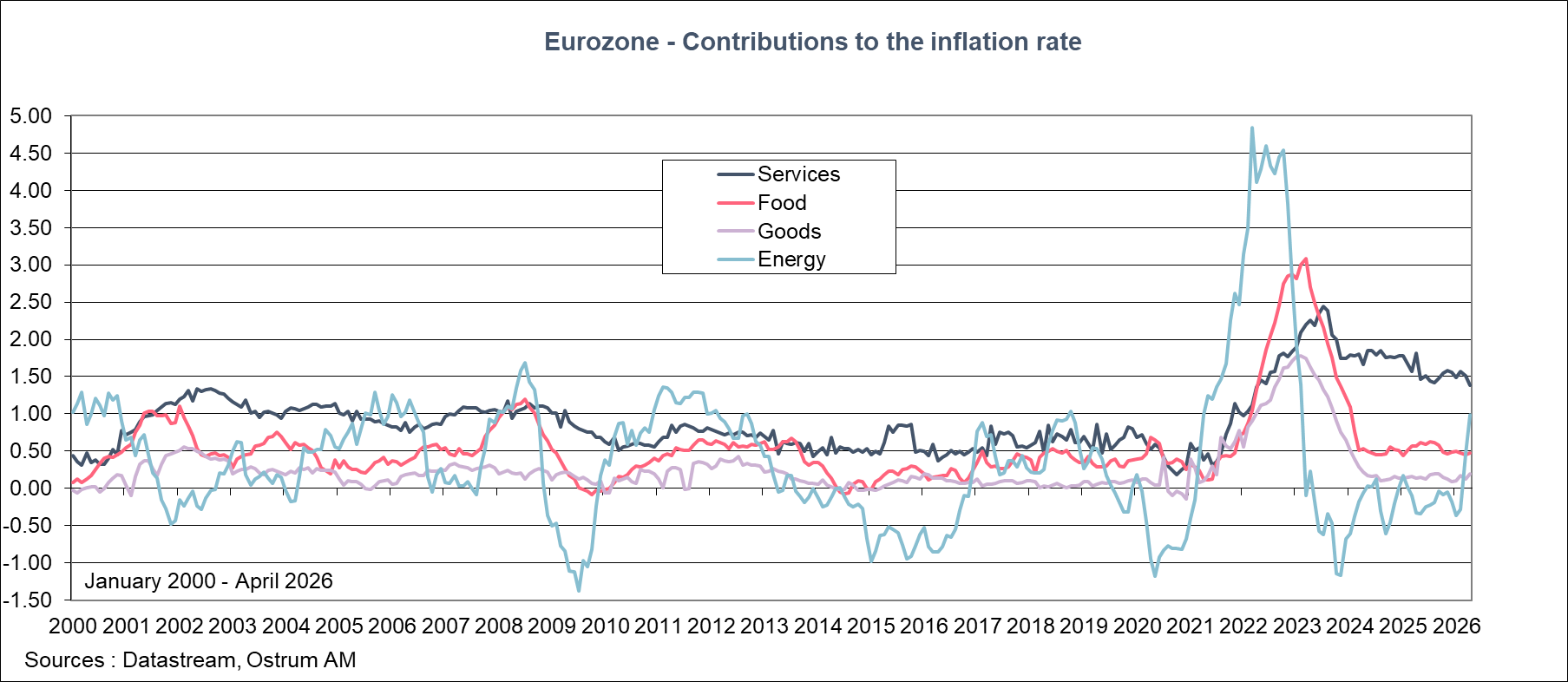

Euro area inflation accelerated again in April to 3%, after 2.6% in March and 1.9% in February. This is its highest level since October 2023. Unsurprisingly, this is linked to energy prices: +10.9% year-on-year, after 5.1% in March, whereas they had been declining for 12 months due to a negative base effect. Prices of goods excluding energy increased by 0.8% and food prices by 2.5%, in line with previous months. Services prices moderated again: 3%, compared to 3.2% in March and 3.4% in February, which resulted in core inflation of 2.2% after 2.3%. In March, the correction of the Olympic Games effect in Italy led to lower inflation in services, and in April, a seasonal effect linked to the earlier date of Easter compared to last year resulted in a less significant effect on services inflation. At this stage, there is no spillover effect from the rise in energy prices to other sectors of the economy, but this is likely to happen given the various surveys.

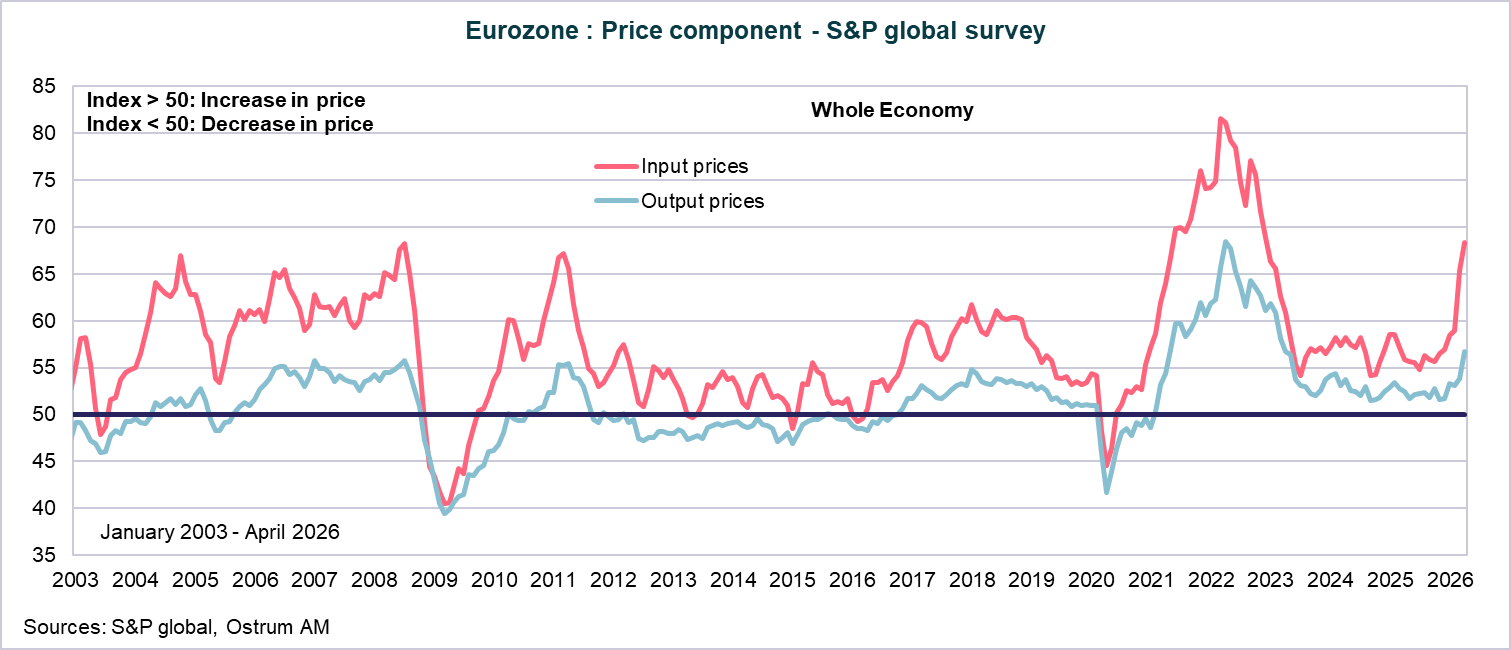

Businesses anticipate a further increase in input and selling prices

Pass-through of a portion of the sharp increase in input prices to selling prices.

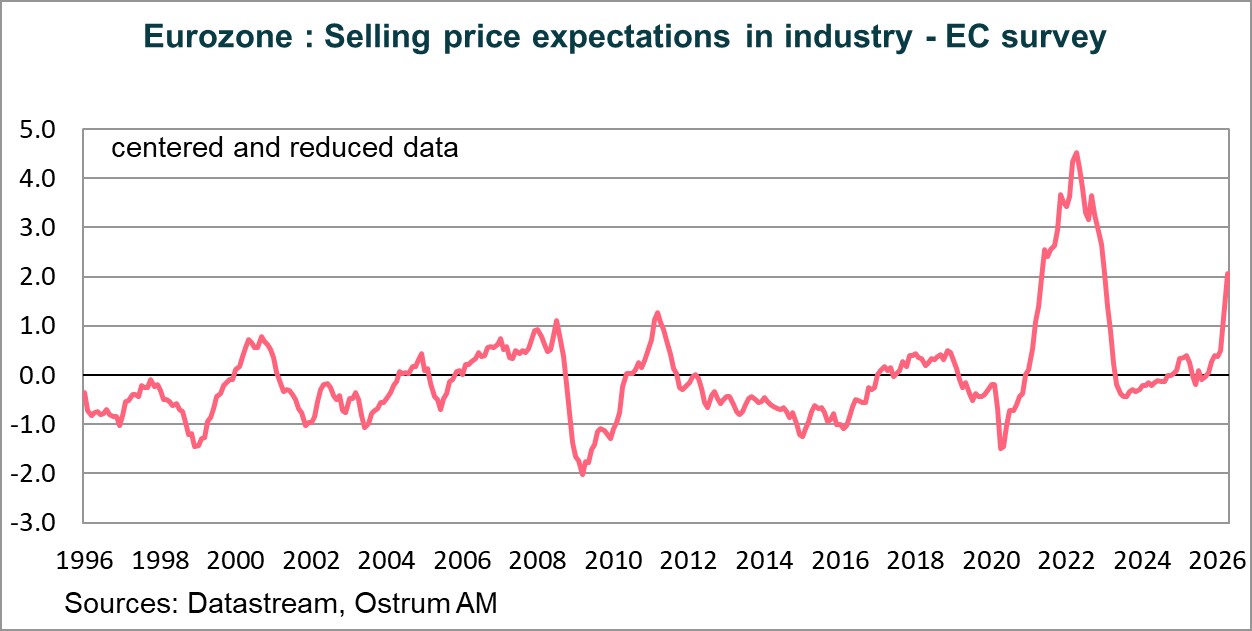

In the S&P Global survey, businesses reported a further significant increase in input prices. Unlike in March, they passed on some of these increases to their selling prices. This reflects both rising energy prices but also tensions in supply chains, as evidenced by delivery times being at their highest since July 2022. The European Commission survey, based on national surveys, confirmed the intensification of inflationary pressures. The 3-month selling price expectations increased sharply again in April, reaching a high since January 2023.

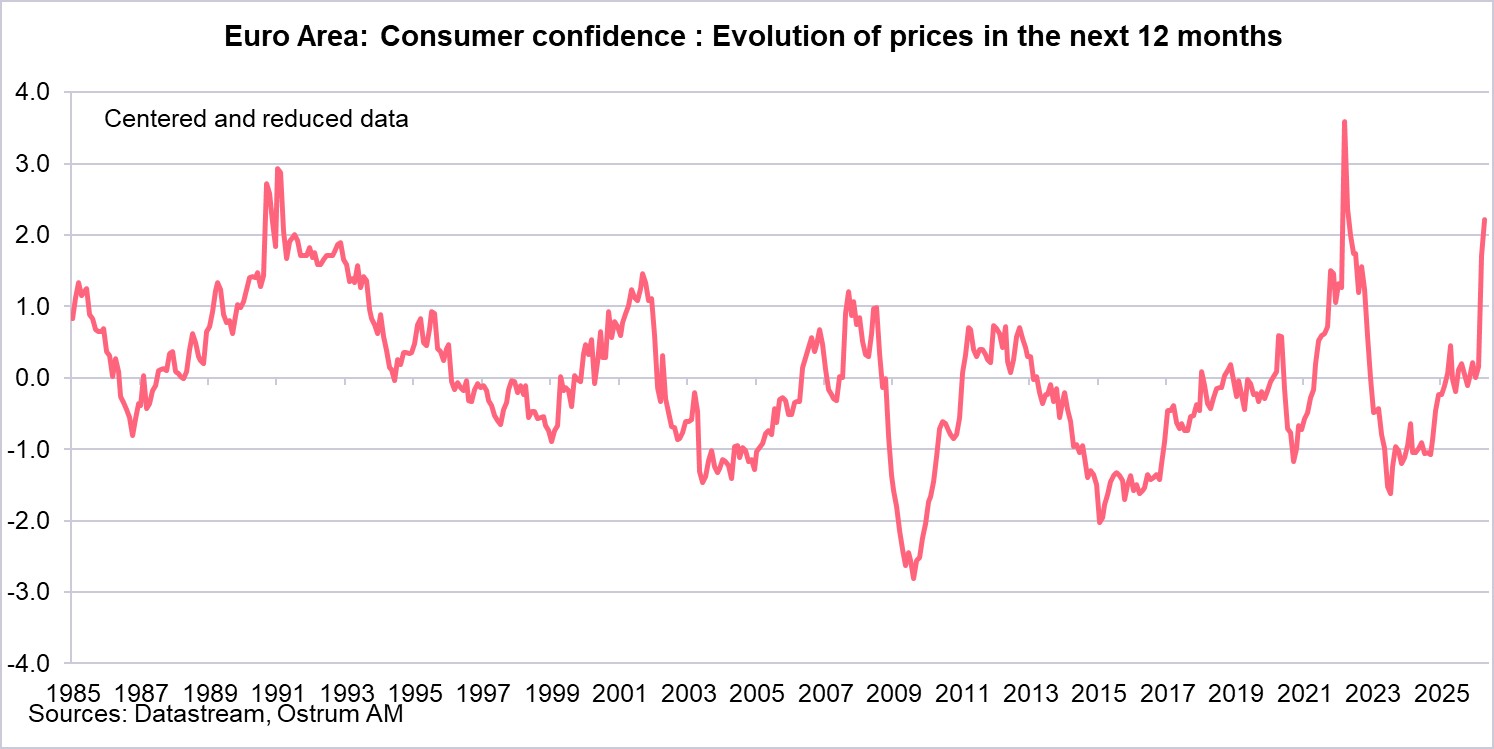

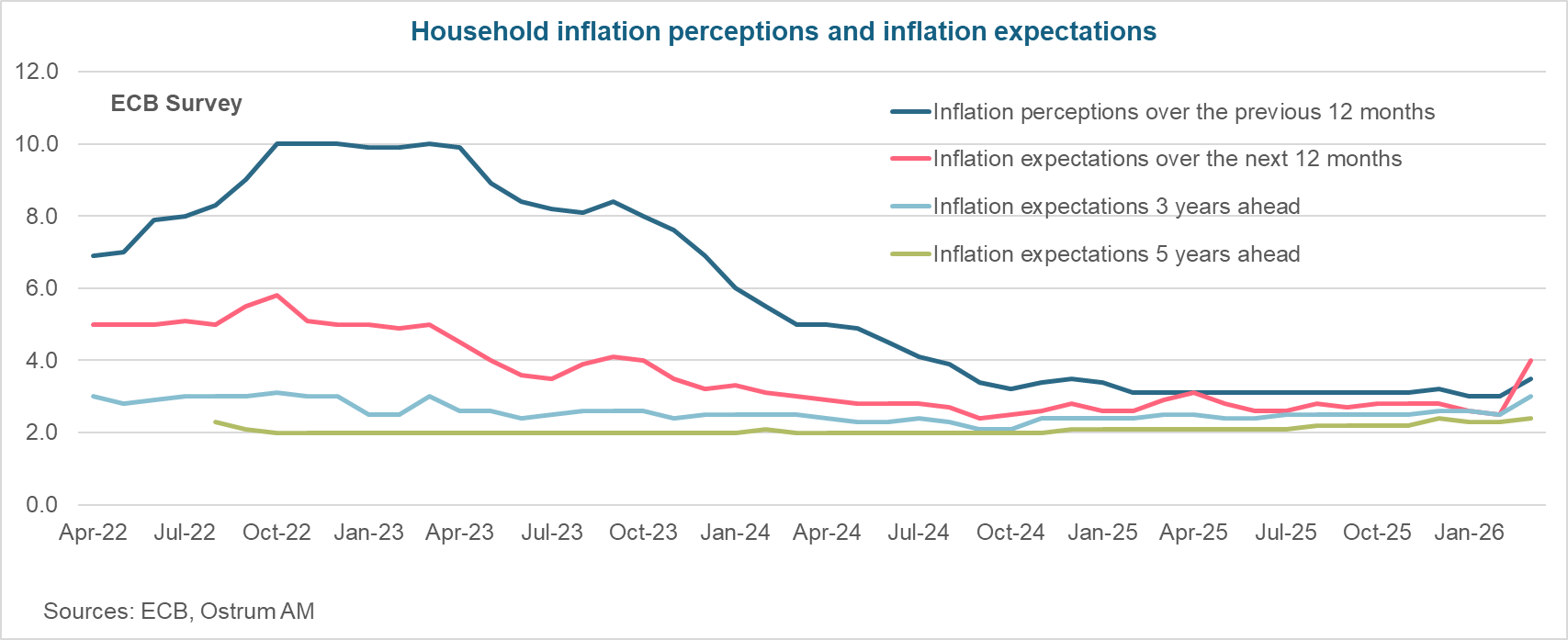

Increase in household inflation expectations for the short and medium term

The survey of households reveals a sharp increase in one-year inflation expectations. The index is well above its long-term average (0 on the graph) and reaches a high since May 2022. According to the ECB survey, 1-year and 3-year inflation expectations increased significantly in March to stand at 4% and 3.5% respectively, compared to 2.5% in February. 5-year inflation expectations remained relatively contained: 2.4% compared to 2.3% in February. Since August 2025, however, we have observed that these long-term prospects have tended to slightly deviate upwards from the ECB's 2% inflation target. This energy shock occurs at a time when household inflation perception was already high before the outbreak of the conflict in the Middle East: 3% in February, compared to 2% before the conflict in Ukraine. It stands at 3.5% in March.

Household inflation expectations for one and three years are rising, while the memory of the high inflation episode is recent.

The ECB will raise its rates in June

The ECB debated a possible rate hike at length before unanimously leaving them unchanged.

At the meeting on April 30, the ECB left its rates unchanged, indicating an intensification of upside risks to inflation and downside risks to growth. During the Q&A session, Christine Lagarde stated that "we are certainly moving away from our baseline scenario" and that participants had debated at length and in depth a possible rate hike, before unanimously deciding to opt for the status quo. The central bank wants to give itself a little more time to obtain more information on the duration of the conflict and the impact of rising energy prices on growth and inflation. In June, the ECB will also have the new forecasts from its teams and the update of alternative scenarios. The outcome of the next meeting leaves little room for doubt. Christine Lagarde was particularly explicit about the debates concerning a possible rate hike as early as April 30, while subsequently stating, "I know in which direction we are heading" before noting, in response to a question, that the two rate hikes anticipated by the markets showed that the ECB's reaction function was well understood.

The ECB will raise its rates in June to firmly anchor inflation expectations.

Conclusion

During the last meeting, members of the Governing Council debated at length a possible rate hike before unanimously leaving them unchanged. They prefer to wait for more elements, particularly concerning the evolution of the conflict in the Middle East, new growth and inflation forecasts, and the update of alternative scenarios by their teams. The direction is clear: a rate hike in June to demonstrate the ECB's determination to bring inflation back to the 2% target. This is a communication challenge for the central bank, in order to anchor inflation expectations. Given the recent memory of the 2022 inflation, it fears that the energy shock linked to the conflict in the Middle East will generate more significant second-round effects (pass-through of price increases to wages), making inflation persistently high. All these elements reinforce our anticipation of two 25-basis-point hikes in the ECB's key interest rates, the first in June, the second in September.

Aline Goupil-Raguénès

Chart of the week

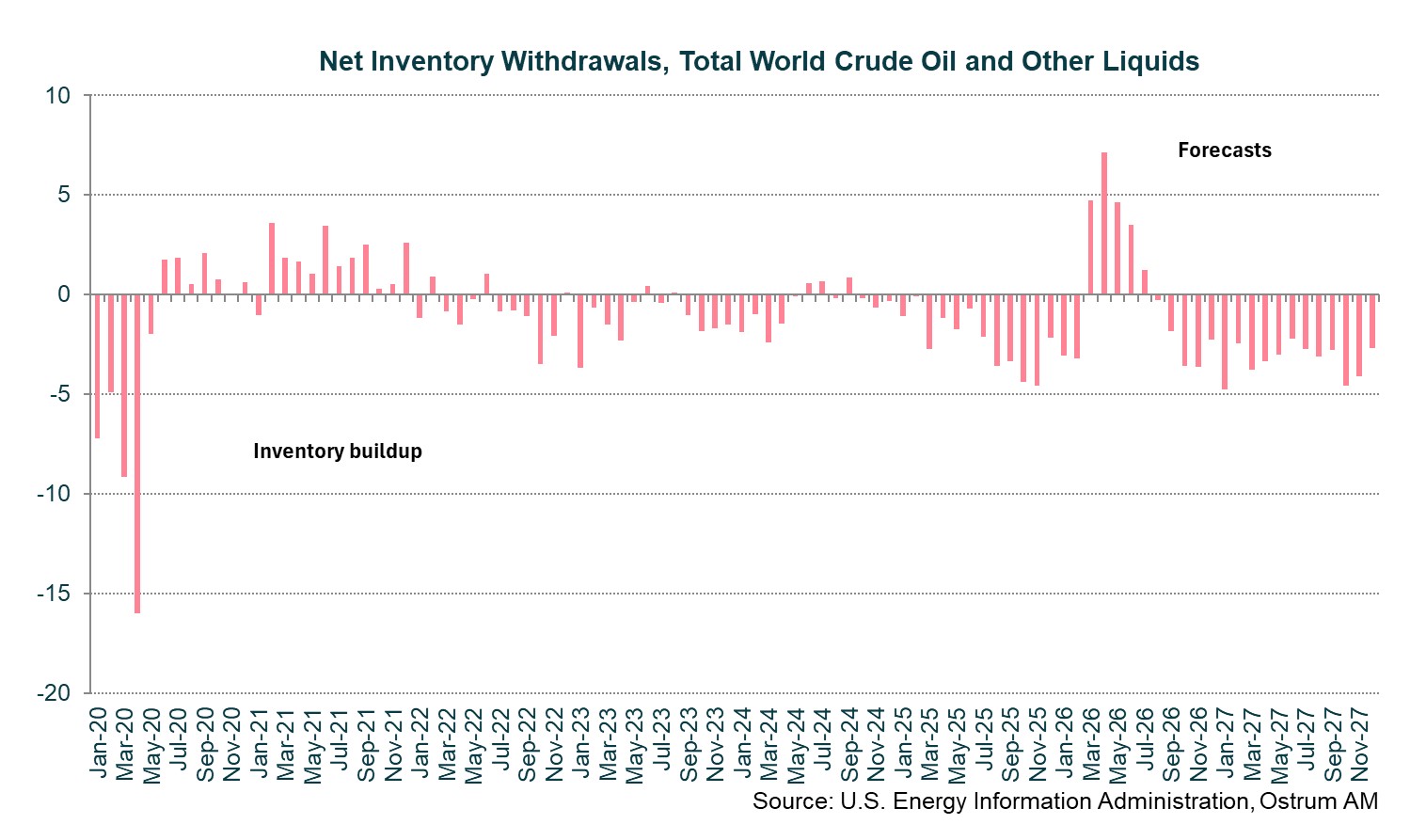

The war in Iran constitutes a significant supply shock for the global economy and access to Gulf oil. OPEC production has declined by more than 7 million barrels per day since the onset of hostilities due to a lack of available storage capacity. Consequently, the oil market is currently equilibrating by drastically reducing available inventories. The adjacent chart shows that inventory adjustment represents more than 5 million barrels per day in April, an unprecedented level. Forecasts, optimistic about the crisis outcome, indicate a return to inventory accumulation capacity after summer. In the event of a prolonged crisis, the oil price curve could become exponential, as the effect of inventory reduction on prices is non-linear.

Figure of the week

4.1

South Korea's stock market cap recently surged to a record $4.1 trillion, overtaking the UK as the world's 8th largest market.

Market review:

- Trump/Xi Summit: Toward progress on Iran and trade conflicts?

- United States: 115k job creations in April with stable unemployment, despite contradictory signals;

- Equities: Nasdaq and Asian markets continue to outperform;

- Rates: Yields ease following the decline in crude oil prices.

Tech keeps pulling stock markets higher

Oil volatility continues to dictate financial market movements. Ahead of a tension-filled weekend, with Donald Trump's visit to China this week as backdrop, crude was down $6. Rates are adjusting lower to the benefit of risk assets.

The earnings season, remarkably solid in the United States, is once again giving way to international politics. The situation at Hormuz remains troubled, with the glimmer of hope seen mid-week swept away by strikes on a U.S. vessel over the weekend as Trump prepares to meet Xi Jinping. The strait's blockade and even the war's outcome, alongside bilateral trade, will feature prominently in discussions. Financial markets performed well last week, particularly U.S. and Asian technology stocks. The dollar's decline and falling long-term rates are supporting risk assets.

Regarding the U.S. economic situation, key labour market data paint a picture of improvement since mid-March. Job creation reached 115,000 in April with unemployment steady at 4.3%. However, the three-month average for monthly job creation stands at merely 48,000, while labour force participation continues declining. Worse still, the household survey reported 226,000 job losses last month. Unemployment duration is also lengthening beyond 24 weeks. Wage deceleration reflects certain fragility and graduate employment difficulties. Job openings are decreasing, with more redundancy announcements (83,000 in April's Challenger survey). U.S. growth relies solely on AI-related investments. Hourly productivity gains remain elusive (+0.8% in Q1). Rising consumer credit (+$24 billion in April) likely reflects wage deceleration. In the eurozone, manufacturing (PMI at 52.2) benefits from inventory demand from companies concerned about the Hormuz blockade. Services (47.6 in April) are clearly downbeat. Meanwhile, inflation expectations are drifting higher according to several surveys.

Any oil price easing systematically triggers a decline in short-term inflation expectations (-19 basis points on the 2-year swap) and rates across most maturities. Brent crude ($101 on Friday) lost over $6 last week. Beyond daily headlines, the long-term risk lies in the concerning state of global oil inventories. Financial markets' binary character around oil will persist.

Regarding Treasuries, after venturing beyond 4.40%, the T-note yield retreated toward 4.35%. The Bund continues oscillating around 3% with Schatz yields hovering about 2.60%. German 30-year yield volatility remains subdued. Sovereign spreads have tightened markedly, notably the Italian BTP trading 10 basis points lower than last week. The UK Gilt (-4 basis points to 4.91%) remains the most volatile government bond, reacting this week to local elections that could lead to Prime Minister Keir Starmer's departure.

Credit markets display remarkable stability, as do swap spreads, while CDS indices declined (-7 basis points on the Crossover). Asian and U.S. equities outperform due to their technology weighting. Finally, the yen rebounded following BoJ intervention in currency markets.

Axel Botte

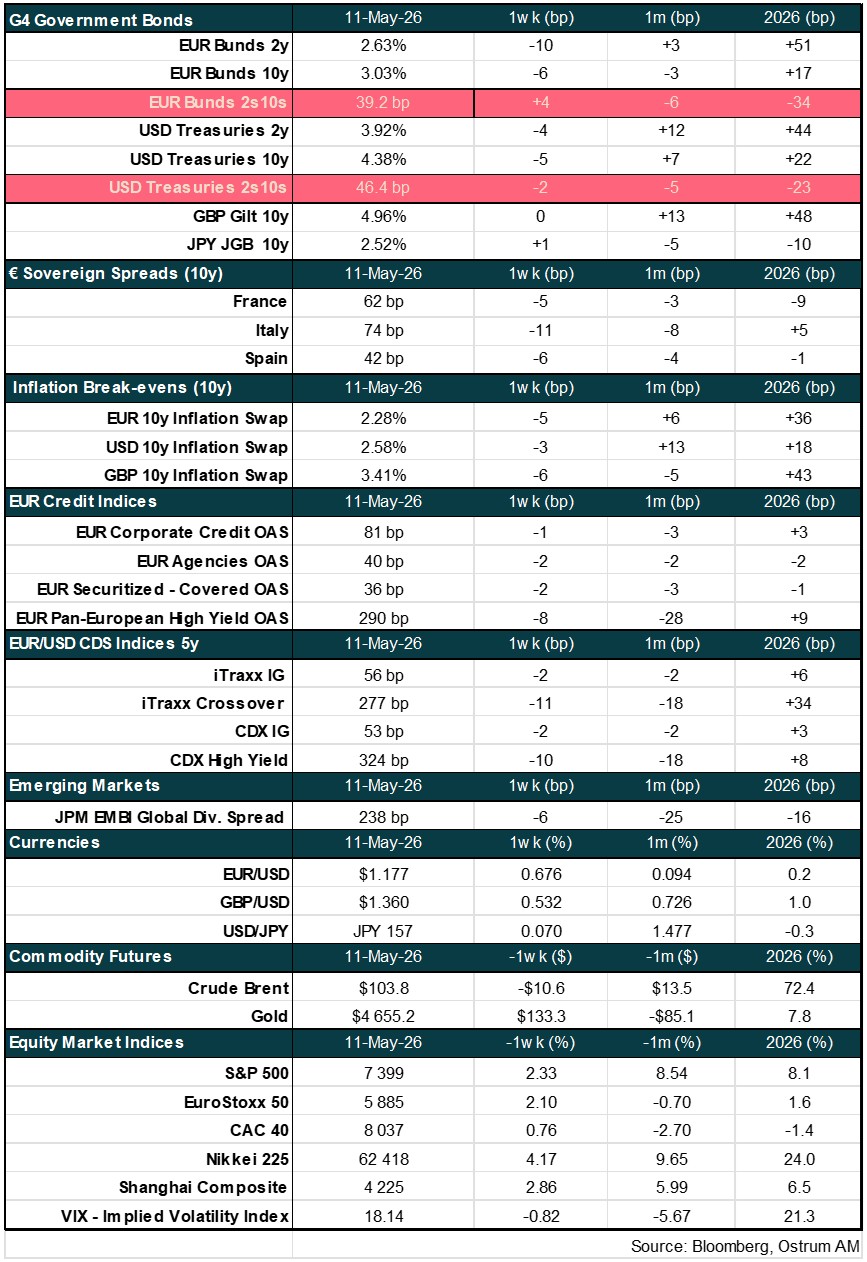

Main market indicators