Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum AM's views on the economy, strategy and markets.

Outlook at 05/15/2026.

The CIO letter

Tech stocks as the way out

The war in Iran maintains a climate of uncertainty to which financial markets are adapting all the more easily given that the earnings season has proven very solid in the United States. The oil market, however, remains problematic. The use of commercial and strategic stocks has so far managed to balance the market, but OPEC production has declined by 7 million barrels per day since the onset of hostilities. While a gradual return to normal remains the most likely scenario, a new sharp rise in oil prices cannot be ruled out if the crisis is prolonged. In other words, beware of non-linearities. Growth, despite internal imbalances, has maintained 2% at an annualized rate in the first quarter thanks to AI. The European recovery, however, is being slowed by the oil shock.

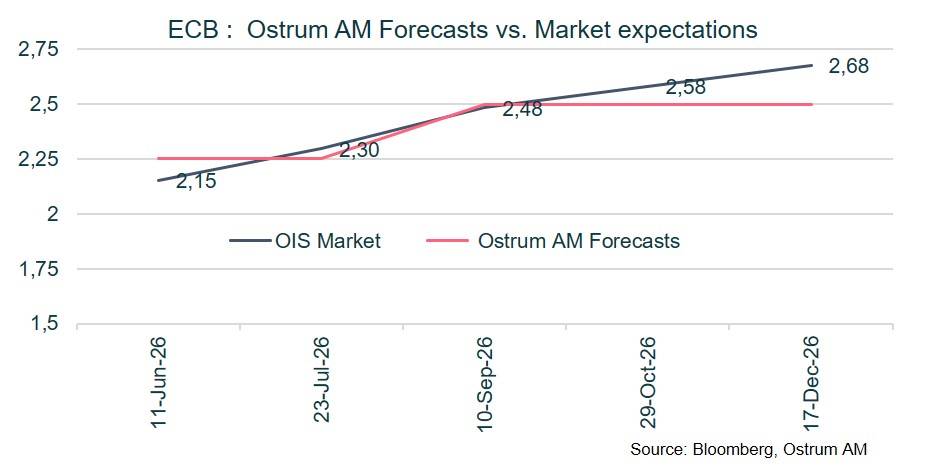

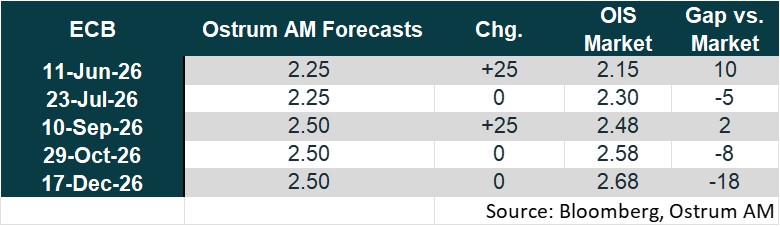

In this context, central banks will be cautious. Kevin Warsh will chair his first FOMC in June. He will need to build consensus to steer monetary policy toward new rate cuts at the end of the year. The ECB will proceed with two rate hikes, in June and September, according to our scenario, to respond to rising inflation expectations.

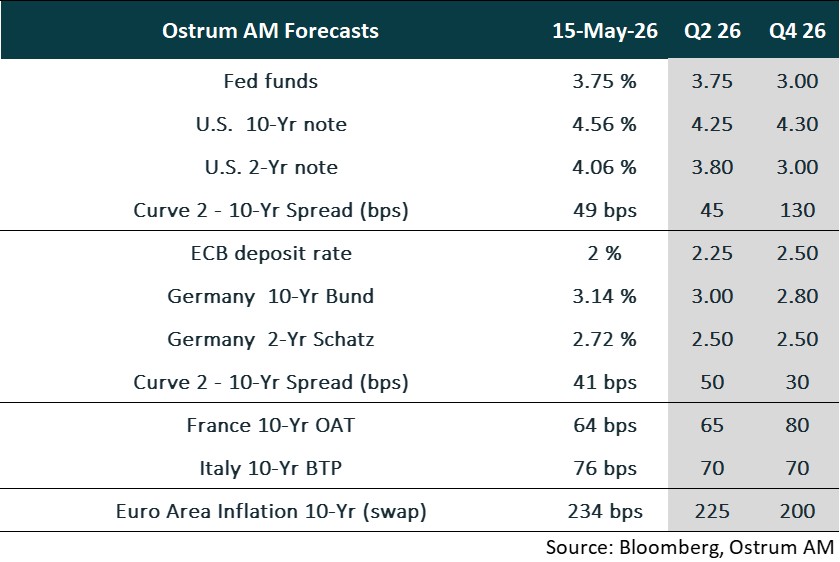

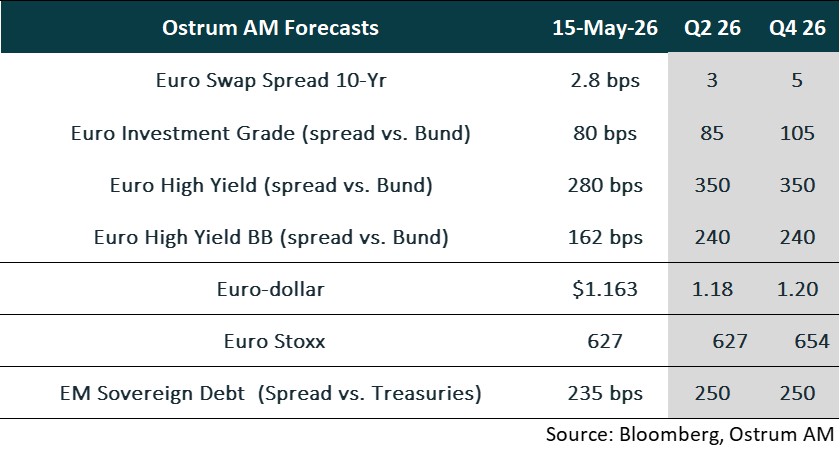

As for financial markets, the Bund is trading around 3%, with the expected decline in inflation expectations allowing a return toward 2.80% by year-end. The T-note should remain around 4.30%, despite the likely resumption of easing in the fourth quarter. Sovereign spreads have tightened significantly and are below our year-end targets, particularly for the OAT. Credit has erased the impact of the war and remains low in volatility with strong demand. After solid quarterly earnings, the equity market is once again dominated by the AI theme. U.S. and Asian indices (Korea, Japan) are logically outperforming.

Economic Views

THREE THEMES FOR THE MARKETS

-

Growth

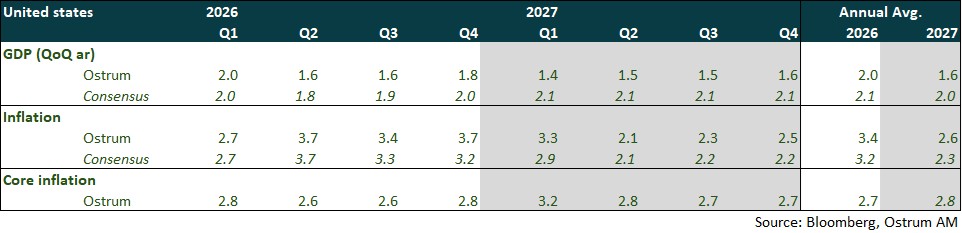

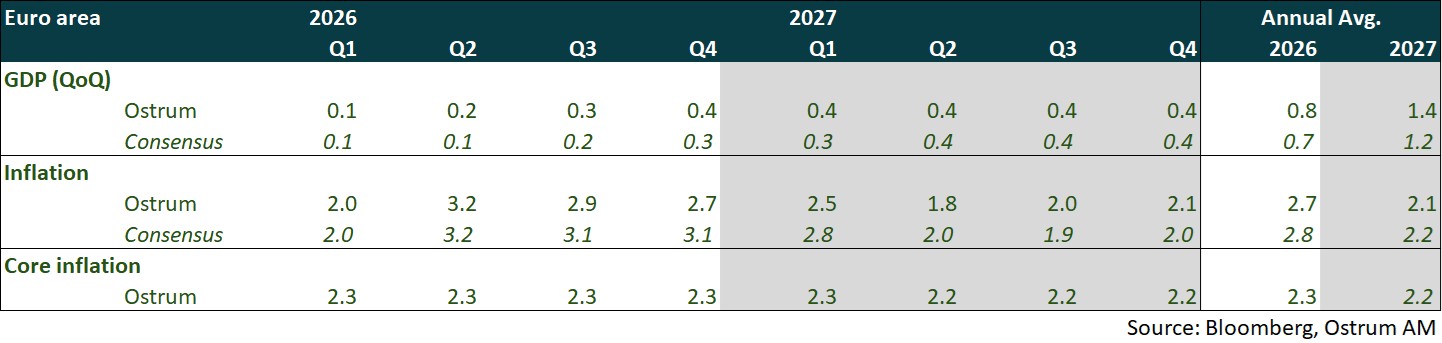

U.S. growth rebounded in Q1 (+2%). Household consumption weakened, but AI-related investments are strongly stimulating activity. According to surveys, the moderate economic recovery (+0.1% in Q1) has been confronted by the oil shock since March, particularly in the services sector. In China, growth remains driven by exports despite the international situation. Investment remains under pressure due to the policy of reducing overcapacity.

-

Inflation

In the United States, the CPI now incorporates rising energy prices (3.8% in April). Core inflation stood at 2.8%. In the eurozone, inflation reaches 3% in April. Price adjustments are expected to continue, with the HICP likely to exceed 3% in Q2. Excluding volatile items, inflation is nonetheless stabilized at 2.2%. In China, inflation is recovering from very low levels. The CPI has risen to 1.2%. Producer prices are strengthening (+2.8%), driven by overcapacity reduction measures and the impact of energy prices.

-

Monetary policy

The Fed left monetary policy unchanged in April, despite dissensions ahead of Kevin Warsh's appointment. The downward adjustment of rates is expected to resume at the end of the year given the likely rise in unemployment, despite the inflationary episode. The ECB will likely raise rates twice in line with market expectations to ensure the anchoring of inflation expectations. The PBOC may postpone its rate cuts to the second half, awaiting more data to assess the state of the Chinese economy.

ECONOMY: UNITED STATES

The oil shock is less severe for the US economy than in Asia or Europe, but consumption is weakening. The labor market is poor, but AI investments are a source of growth.

- Demand: Household consumption is suffering from the oil shock, which is weighing on real disposable income. The consumption rebound linked to tax refunds will fade. The trade balance will improve with hydrocarbon exports, but technology goods imports will remain strong. Data center investments are increasing by 25% annually, but physical constraints are accumulating (employment, components, equipment prices). Housing continues to contract, with prices set to decline further.

- Labor Market: The labor market is sluggish. The stable unemployment rate in Q1 reflects weak participation. Job openings are below the number of unemployed (labor supply surplus). Graduate job placement is extremely difficult. Unemployment duration is lengthening.

- Fiscal Policy:Tax overpayment refunds are two-thirds complete, but the oil shock is limiting purchasing power. Tariff refunds have begun ($137 billion requested, equivalent to 0.4 percentage points of GDP).

- Inflation: Disinflation is encountering the oil shock. Core inflation remains close to 3% (PCE). Housing is a source of disinflation.

ECONOMY: EURO AREA

The conflict in the Middle East makes forecasts more uncertain and dependent on its duration. As Europe is a net importer of oil and gas, the rise in energy prices will translate into more moderate growth and higher inflation in 2026.

- Domestic Demand: While Q1 growth proved weaker than expected, the energy shock is translating into a decline in business activity indices from surveys and a plunge in consumer confidence. This will partially offset the impact of the implementation of German plans, the increase in European military spending, as well as NextGenerationEU disbursements.

- External Demand: External trade is expected to make only a minor contribution to growth. Germany is expected to continue facing increased competition from China and tariff uncertainty will persist. The United States is pressuring the EU to ratify the July 2025 trade agreement, threatening to raise tariffs on European cars to 25%.

- Fiscal Policy: A very expansionary fiscal policy in Germany with the implementation of the infrastructure plan and the rise in military spending. Several countries have adopted measures to limit the impact of the energy shock on households and businesses. These are limited in scope, but more significant in Spain.

- Inflation: Inflation’s acceleration to 3% in April is linked to energy prices. It is expected to continue accelerating in Q2 as it spreads to other sectors of the economy, before moderating, in line with that of energy prices. The impact on core inflation is expected to be limited.

ECONOMY: CHINA

Despite the Middle East conflict, China continues to demonstrate the resilience of its economy, underpinned by strong exports, a recovery in domestic demand, and a structural shift in its inflation regime.

- Growth: GDP expanded by 1.3% quarter-on-quarter in Q1, equivalent to 5% year-on-year, largely driven by exports, which rose by nearly 15% year-on-year over the period. Economic momentum remained resilient in April, supported by external demand and a recovery in services activity. The sharp rebound in industrial profits in Q1 (+15.5% year-on-year) highlights strong momentum in AI-related sectors, electronic equipment, batteries, and industrial robotics, which should translate into sustained growth in non‑residential investment. The real estate sector remains a drag on activity, although early signs of stabilization are emerging.

- Exports: External trade remains particularly buoyant, driven by exports of technology-intensive goods, AI-related equipment, and renewable energy products. The gradual withdrawal of export subsidies is expected to push up prices for low and very low value‑added goods, marking a change in China’s export pricing strategy.

- Consumption: Services activity is accelerating, signalling a strengthening of domestic demand. This trend is corroborated by RatingDog PMI surveys, which point to a broad-based improvement in services momentum.

- Inflation: China has officially exited deflation. Producer prices accelerated to 2.8% year‑on‑year in April, reflecting higher input costs linked to the disruption of the Strait of Hormuz. Consumer inflation rose to 1.2% year‑on‑year in April, driven by higher transportation costs. The shift in China’s economic policy framework—encompassing the rebalancing of the trade surplus, the implementation of anti‑involution policies, and a stronger emphasis on services consumption—has reduced the country’s ability to absorb volatility in commodity prices. As a result, Chinese export prices declined by only 1.2% year‑on‑year in March (from ‑5% previously), pointing to an increasing pass‑through of higher costs into selling prices across several product categories. The conflict in the Middle East is acting as a catalyst: China is now exporting inflation.

Monetary Policy : FED

A very divided Fed before Kevin Warsh's arrival

- At the April 29 meeting, the Fed left its rates unchanged, judging activity solid, job creation still weak, and inflation high.

- The Monetary Policy Committee proved to be very divided: 4 out of 12 members expressed their dissent, which had not happened since 1992. 1 member wanted a rate cut (S. Miran, who will be replaced by K. Warsh in June), and 3 members voted against the statement associated with the decision due to the inclusion of an accommodative bias.

- During his last meeting as Fed Chairman, Jerome Powell stated that he would remain on the monetary policy committee as a governor, assuring he would maintain a "low profile" to allow K. Warsh to fully assume the role of Chairman. This constitutes a strong signal to preserve the Fed's independence.

- A consensus is emerging with rates at 3.75%, monetary policy is still relatively restrictive, as among the members most concerned about high inflation, none are expressing support for a rate hike, preferring to opt for the status quo.

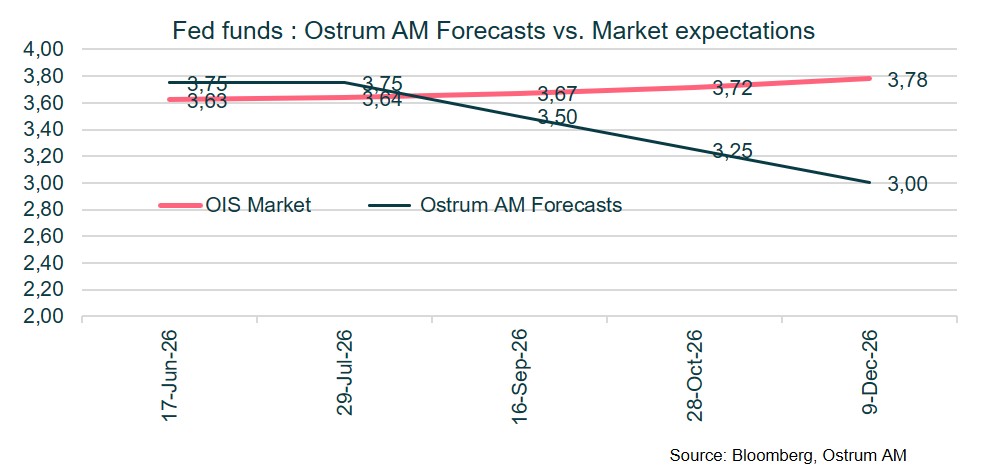

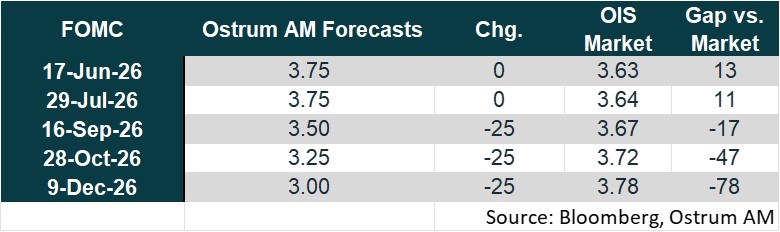

- We believe the Fed should prioritize the deterioration of the labor market and cut its rates 3 times starting in September.

Monetary Policy : ECB

The ECB has left the door wide open to a rate hike in June

- At the April 30 meeting, the ECB unanimously left its rates unchanged, judging an intensification of downside risks to growth and upside risks to inflation, linked to the consequences of the war in the Middle East.

- Christine Lagarde was particularly explicit during the Q&A session, stating that a rate hike had been debated at length and in depth, given that "we are certainly diverging from our baseline scenario."

- The ECB does not want to repeat past mistakes: acting too soon like in 2011 or too late like in 2022. It wants to give itself a little more time to have additional information. In June, it will know more about the evolution of the conflict in the Middle East and its consequences on the economy, and will also have available the updated growth and inflation forecasts from its teams, as well as alternative scenarios.

- The available data and surveys, as well as the statements from Christine Lagarde and other ECB members, reinforce our anticipation of 2 ECB rate hikes of 25 basis points each, the 1st in June and the 2nd in September, in order to well anchor long-term inflation expectations.

Market views

Asset classes

- U.S. Rates: The inflation shock complicates the Fed's task. Kevin Warsh assumes his duties as head of the Fed and will chair his first FOMC in June. Monetary easing will occur at year-end according to our forecasts.

- European Rates: The ECB should raise rates twice to weigh on inflation expectations. The 10-year Bund will oscillate around 3% before declining toward 2.80% at year-end.

- Sovereign Spreads: Sovereign spreads have almost completely erased the Iranian crisis. Political considerations in France should weigh on the OAT at year-end. Italy's spread should tighten further, reversing recent underperformance.

- Eurozone Inflation: Long-term inflation expectations have increased due to the oil shock. The premium should diminish in the second half of the year.

- Euro Credit: IG credit spreads have quickly erased the Iranian crisis and the primary market is well absorbed. However, valuation levels would justify a gradual widening.

- Euro High yield: High yield valuations should normalize over the course of the year. The default rate, however, remains contained and below the long-term average.

- Exchange Rates: The structurally bearish trend for the greenback should resume as the Iranian crisis dissipates.

- European Equities: Earnings should accelerate in the second half of the year.

- Emerging Debt: The EMBIG is withstanding the Iranian crisis. Spreads will remain tight. However, spreads have little room to tighten further.