With the upcoming entry into force of the Solvency II reform, the European regulator aims to enable insurers to increase their contribution to financing the European economy.

As stated by the European Commission as the first objective: “[Solvency II Delegated Regulation will]1. help insurers provide more long‑term financing to the real economy, supporting the objectives of the savings and investments union.

This will encourage long‑term investments and increase investment capacity by making the valuation of long‑term liabilities less volatile and more predictable.

To what extent will these objectives be achieved?

Parameters in the Spotlight: Risk Margin Cost on Capital, Long Term Equity Investment and symmetric adjustment

A direct relief of capital requirement

The reduction in the cost of capital will have a direct impact on the level of the Risk Margin and mechanically free up capital, particularly for long-term liabilities. That does not tell how this capital will be allocated: more risky assets? Deleveraging of the balance sheet? …

Equity exposure boost?

Enlarging the symmetric adjustment will help dampen the pro-cyclicality of the equity shock, but it doesn’t change either the fundamental high cost of equity at 39% SCR Charge (Solvency Cost Ratio) nor the implied volatility on the balance sheet and the accounting profit and loss.

The criteria for Long-Term Equity Investments (LTEI), introduced in 2019 with a reduced shock at 22%, has not met its expectation as they are overly restrictive. Even with slightly relaxed rules, criteria remain stringent (EEA-based2, dedicated portfolio, five years holding period, etc.). Plus, same accounting considerations apply, in the end it may eventually be a useful tool for specific private equity or strategic holdings but not more.

In an ALM framework, volatile equities are a poor match for long-term fixed liabilities. The capital charge remains the highest of any major asset class. The risk/return trade-off for public equity is still mathematically challenging under Solvency II compared to spread assets.

The reforms make holding equity less painful, but they don't make it fundamentally more attractive than high-quality credit or illiquid for liability matching. The asset class will likely see a marginal increase and less “panic”-selling, but not the "great rotation" that policymakers hope for.

Securitization boost ?

The reform recalibrates the spread shocks, reducing capital charges on securitized assets especially for senior STS (Standard Transparent Simple) securitizations. It is part of a broader package to incentive bank and insurance intended to increase the attractiveness of such assets.

This is a welcome technical correction that will reopen the market for high-quality securitizations. It will become a viable option for diversification and yield pickup; it will make it easier for existing securitization investors to increase their allocations and will bring some new players off the sidelines.

However, if this adjustmentmain re-enabling a niche asset class, it won’t turn securitization into a new, dominant pillar of insurer Strategic Asset Allocation.

Game Changers – Risk-Free Curve Extrapolation, Interest rate shocks, and Volatility Adjustment

While much attention has been given to the adjustments in the Risk Margin due to its direct consequences on the balance sheet, as well as for Long-Term Equity Investments (LTEI) and securitization treatments, in the hope that these will regain interest in the eyes of insurers, the truly transformative changes lie in the more technical adjustments to risk free rate curve extrapolation methods, interest rate shocks, and the Volatility Adjustment (VA).

These changes may fundamentally reshape the strategic asset allocation (SAA) and asset-liability management (ALM) frameworks of insurers, especially those with long liabilities.

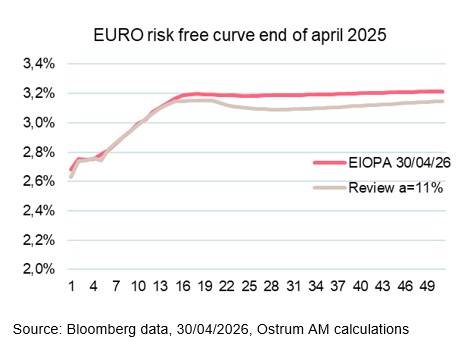

The first step: the risk-free curve

The change in extrapolation method may not look so important on a chart but it is a structural change for long dated liability hedging. The change in the Last Liquid Point (LLP) and the extrapolation method introduces new sensitivity profiles.

When the 20 years maturity swap used to concentrate the hedging swaps, the new calculation over 15y to 30y (up to 50y) changes the global sensitivity of the extrapolated curve to a broader range of maturities.

Plus, lets mention here that insurers’ ALM department cannot rely on published curves by EIOPA3 but have to code and implement the new method for testing.

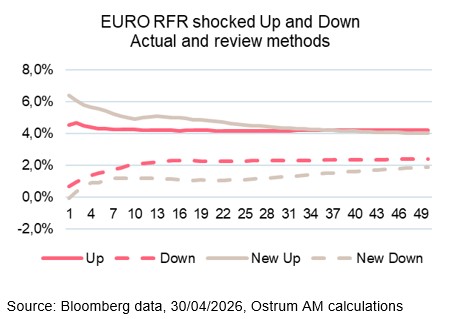

The Tectonic Shifts in Interest Rate Risk Management

The correction of the "negative rates not shocked down" anomaly is already an important point in the interest rate risk landscape. Let’s keep in mind the Solvency II reform began during the era of negative rates. Back then, insurers could maintain a negative duration gap (asset duration significantly lower than liabilities) without significant Interest Rate Solvency Capital.

But the more important moves are on the shocks: now additive plus multiplicative factors and a global increase for most part of the curve.

The negative gap duration (assets shorter than liabilities) once painless is now source of important Interest Rate Solvency Capital Requirement. The consequences will be a closer adjustment between rate portfolio and liabilities cashflows.

The VA (R)evolution

Under the Solvency II framework, the volatility adjustment mechanism is based on a currency risk-corrected spread, derived from a reference portfolio. Previously, this spread could be applied at a maximum of up to 65% of its value. The Solvency Review has now increased the application to 85% of its value.

But the most dramatic change is in personalization. While current volatility adjustment is Currency x Country specific, the review acted an insurer-specific Credit Spread Sensitivity Ratio (CSSR), ranging from 0 to 1 to better reflect each insurer’s actual risk exposure.

This CSSR is the ratio of price value of a basis point (PVBP ≈ sensitivity) of assets – bonds, loans and securitizations – and best estimate liabilities. It encourages detention of physical instruments while swaps and derivatives are not taken into account in the PVBP of assets.

Thus, it will be crucial for insurers to develop robust Asset and Liability modeling to leverage the potential benefit of their bond exposure and maximize their CSSR while controlling Spread and Interest Rate SCR.

Conclusion

The reform is moving in the right direction as it aims to loosen certain constraints and reduce some prudential biases. It will marginally encourage investment in equities and securitization. However, its impact on insurers' strategic asset allocation will likely be more technical than spectacular. Will these changes have a deep impact on insurers' allocation and provide more long-term financing to the real European economy? They certainly point in the right direction, but we can’t be careful enough evaluating the magnitude of the movement. While the reform may not trigger a massive reallocation towards the real economy through equities, it could profoundly transform Asset and Liability Management (ALM) frameworks and bonds portfolios facing long duration liabilities.

1Why is there a need to amend the Solvency II Delegated Regulation?

https://finance.ec.europa.eu/news/questions-and-answers-solvency-ii-delegated-regulation-2025-10-29_en as of 18/05/2026

2 EEA : European Economic Area