Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Summary

Listen to podcast (in French only)

(Listen to) Axel Botte’s podcast:

- Review of the week – Monetary status quo amidst oil volatility;

- Theme – BoE: to hike or not to hike?

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: BoE: to hike or not to hike?

- The BoE faces a paradox where rate cuts since August 2024 (150 bps) have failed to revive growth while fueling inflation, now at 3.3% against a 2% target.

- The Monetary Policy Committee struggles to reach consensus, with only 2 unanimous decisions since December 2022. Members oscillate between maintaining the status quo and preemptive hikes in the face of inflationary risks.

- Unlike a simple external oil shock, the UK suffers from persistent domestic inflation, with services at 4.5% and wages still at 4%, in the context of an economy operating close to potential.

- BoE simulations forecast tightening of 50-75 bps in moderate scenarios, but up to 100-200 bps if the Iranian energy crisis persists and generates second-round wage effects.

- Despite cautious rhetoric from officials, markets anticipate two consecutive hikes in June-August and a third in November, reflecting the perceived urgency to contain inflationary pressures.

Why can’t the MPC reach consensus?

The BoE is a strange animal.

The Bank of England’s policy objective is to maintain price stability defined as a 2% (CPI) inflation target over the medium term. Whilst most central banks have similar inflation mandates, split decisions by the Monetary Policy Committee (MPC) are much more frequent than at other monetary institutions. The BoE has a unique decision-making process where consensus is seldom reached and the Governor can fall into the minority camp (as happened under Mervyn King’s leadership).

The MPC includes 9 policymakers. Unanimity regarding the appropriate level of policy rates has been the exception rather than the norm. Since December 2022, the MPC has indeed delivered a unanimous decision on just two occasions. Prior to the March 2026 MPC, in the early days of the Iran war, there had not been a unanimous decision for eight straight meetings. In February 2026, a three-way split – with a member calling for a hike and four in favor of a 25-basis point rate cut - led to a second round of votes ending with a 5-4 majority for a status quo on policy rates at 3.75%.

Transparency regarding the views and votes of individual BoE policymakers can be helpful… but only up to a point. Efficient monetary transmission requires a clear message from authorities. The lack of a solid consensus decision can inadvertently send the wrong signals on the policy bias and undermine forward guidance on interest rates, if any. In turn, uncertainty about the BoE’s rulebook may enhance the volatility in short-term interest rate markets.

Recent comments suggest range of views persists

Urgent to ‘wait and see’.

Looking at recent comments from Bank of England policymakers, officials lean towards maintaining a restrictive stance while being cautious about immediate rate hikes. Governor Andrew Bailey emphasized a "no rush to judgments" approach, stating it's too early to form strong opinions given uncertainties, particularly regarding the second-round effects of inflation from the war and the broader economic conditions. Governor Bailey also touched upon the potential stress in the opaque world of private credit, which the Iran war could be compounding.

Chief Economist Huw Pill acknowledged that current policy is likely restrictive but did not rule out the possibility of further rate increases if necessary. This sentiment was echoed by MPC member Megan Greene, who, while recognizing downside risks to demand, stressed that upside risks to inflation are paramount and warned against waiting too long to address potential second-round effects, as it might become "too late."

Conversely, MPC member Alan Taylor suggested a "high bar for voting for hikes," indicating that a deterioration in the inflation outlook would be needed to justify further increases, and he views holding rates steady as already restrictive. Taylor also invoked historical lessons, cautioning against ignoring supply shocks and international arbitrage, while also warning against overreacting to such events. Catherine Mann highlighted the need to observe market developments, firm pricing strategies, wage demands, and economic activity before making decisions. Deputy Governor Sarah Breeden noted that the conflict in the Middle East increases the risk of multiple market shocks, potentially leading to a "rocky ride."

BoE speak hints a prolonged status quo

Speech analysis depicts mildly hawkish stance.

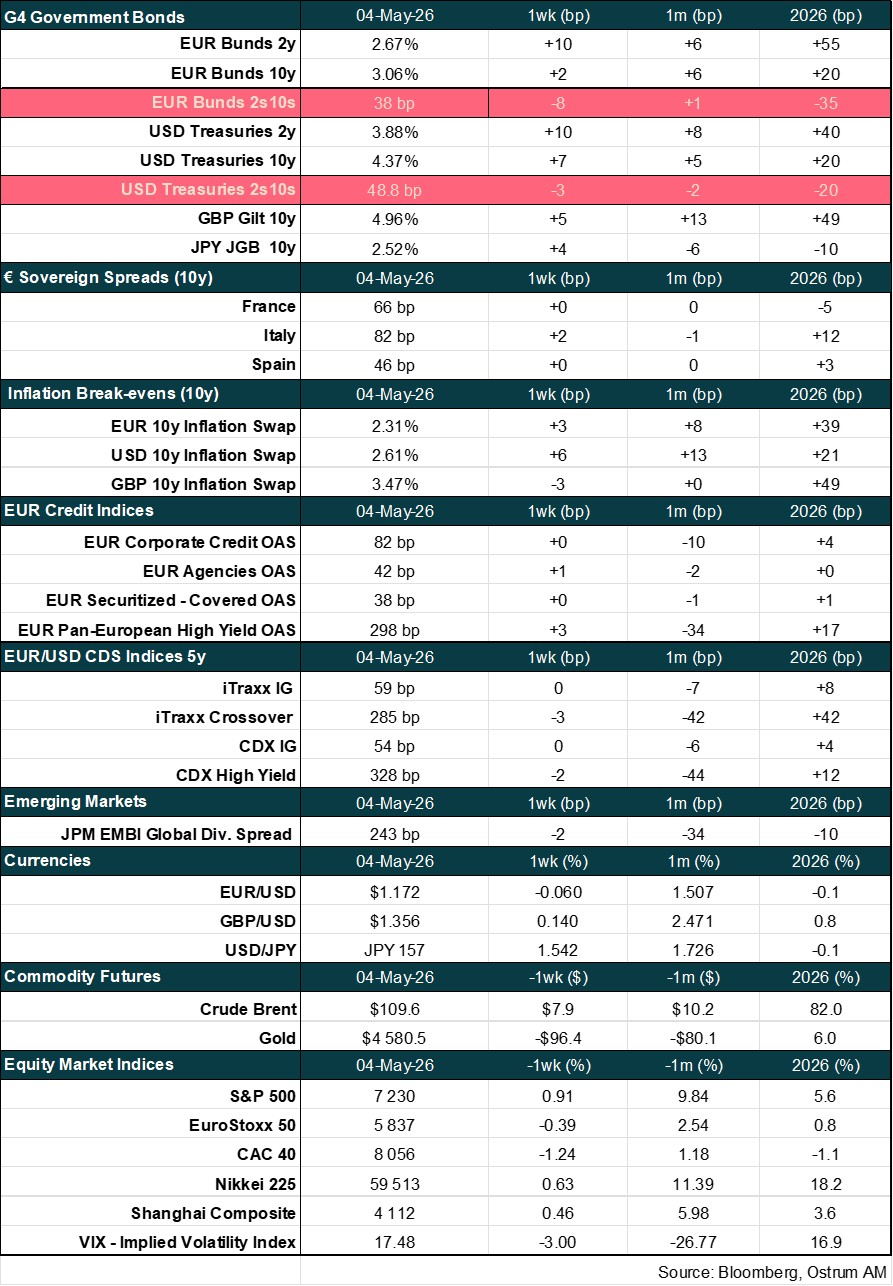

The comments of BoE policymakers can be scored using natural language models. Bloomberg has developed a daily BoEspeak Index. The index is underpinned by an NLP algorithm trained on news headlines, covering thousands of speaking engagements by BoE officials since 2009.

In this model, positive readings indicate a hawkish-leaning MPC and negative readings a more dovish MPC. It is fair to say that shifts in BoE speak are much more frequent and abrupt than actual changes in policy rates (other monetary tools including asset purchases have been used for an extended period after the Great Financial Crisis and through Covid). The BoEspeak index Now stands in moderately hawkish territory. Historically, rate increases have been associated with a BoEspeak index above 2.

An external shock coumpounding a domestic inflation problem

The inconvenient truth: domestic pressures have persisted through the downturn.

With the ongoing Iran crisis, the Bank of England must deal with an external shock at a time when domestic price pressures have not abated. It’s tempting for Andrew Bailey to frame the debate in terms of an external oil shock, but the reality is that the UK’s inflation problem is home grown. The UK economy is operating near potential. The UK’s output gap was positive at 0.2% in 2025 according to OECD estimates. There is thus little space for monetary stimulus amid above-target inflation.

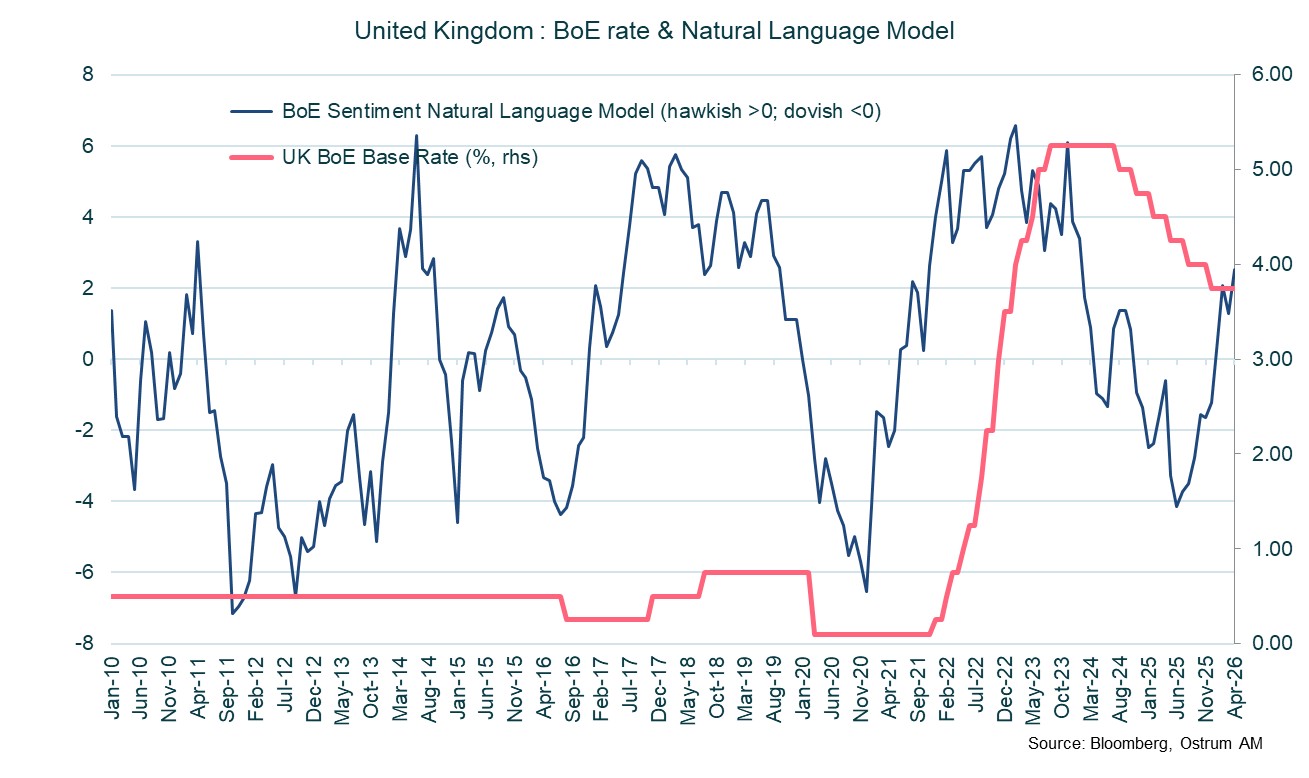

Furthermore, monetary policy is ill-equipped to deal with supply-side issues. The job market has softened, but the UK jobless rate may have already peaked at 5.2%. The participation rate of people aged 16 and over is elevated at 64% and labor force growth has slowed since Brexit. Constrained labor supply is an inflationary factor, even more so that output-per-hour has been stagnant since 2020.

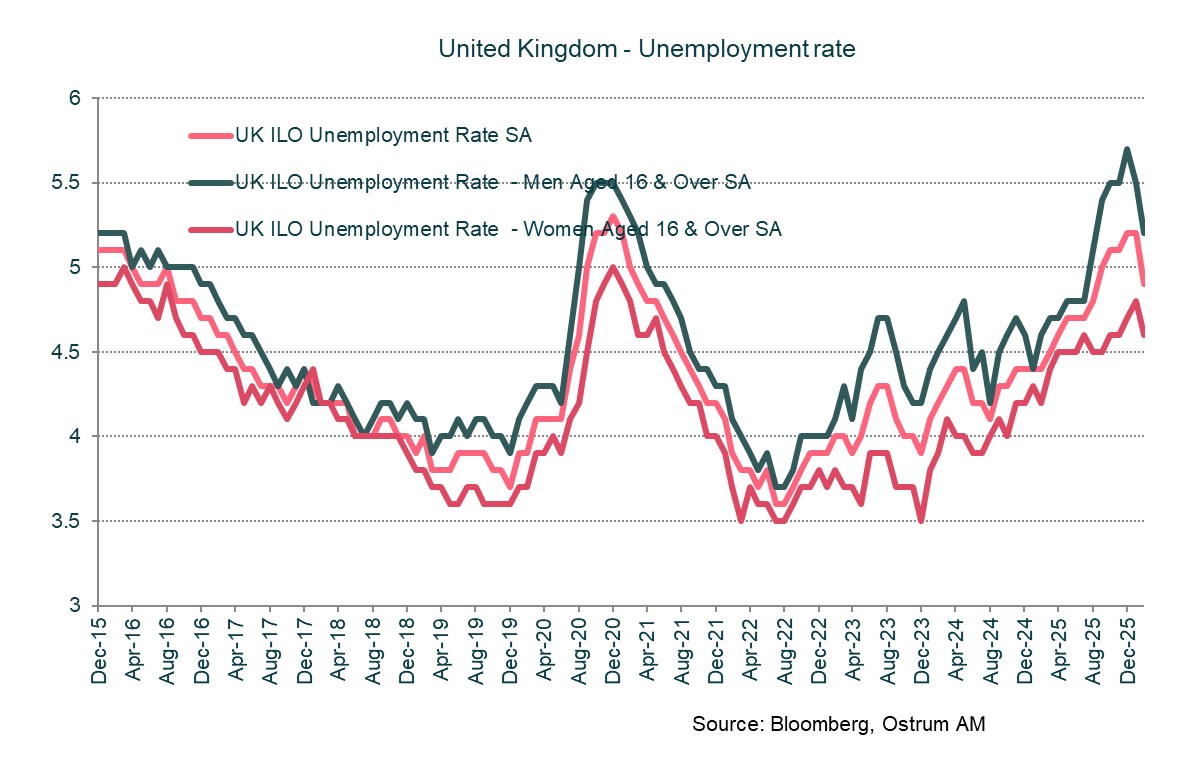

Since the BoE began lowering policy rates from 5.25% in August 2024, CPI inflation has increased from 2% to a peak at 3.8% a year later. During this period, the MPC cut interest rates by a total of 150 bps. The repo rate now stands at 3.75% whilst progress on inflation appears to have stalled more than 1% above target (3.3% in March 2026).

The rise in the unemployment rate failed to slow wage gains significantly (still about 4%, the high end of the pre-Covid range), which keeps feeding excess inflation in the service sector. The sticky service component of inflation remains elevated at 4.5% in March.

April MPC and the path forward for rates

Energy price scenarios point to moderate to significant tightening… but the situation will remain quite fluid.

The Bank of England must strike a balance between weak demand and upside risks to inflation. At its April 30 meeting, the MPC voted 8-1 to keep rates unchanged at 3.75%. The dissenting voter, Chief economist Huw Pill, argued in favor of a preemptive 25-basis point hike to curb inflation developments. Bailey described the status quo as an “active” hold.

The MPC said that second-round effects are most likely to materialize in pricing for goods rather than in people asking for higher wages. Most wage settlements for 2026 have indeed been concluded before the Iran war began. This nevertheless suggests that wage growth could accelerate in 2027 if inflation fails to slow in the second half of this year. In the latest BoE survey and agents’ work, firms are likely to raise prices to mitigate input costs, subject to demand conditions. That said, household inflation expectations have risen, and have turned more sensitive to energy prices.

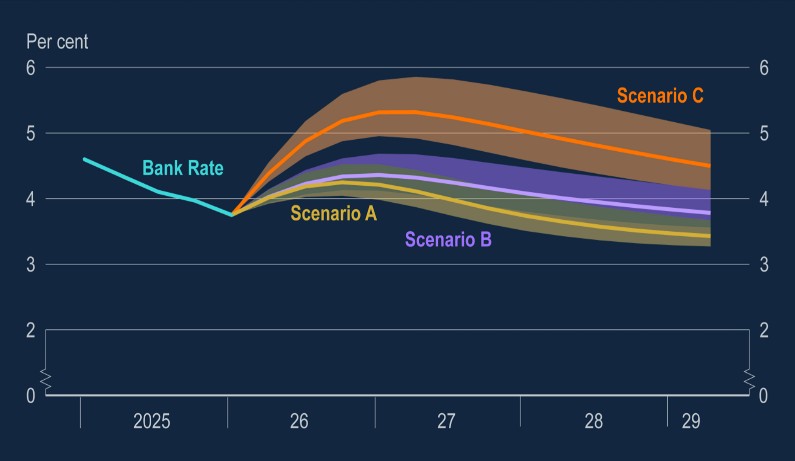

The BoE has studied three illustrative scenarios (chart below sourced from BoE) with different assumptions regarding oil and gas prices. In all three scenarios A, B and C, inflation rises but the optimal policy response is different. In A and B, oil and gas prices grind lower from current levels to pre-war levels (A) or stay higher (B) until 2029. In scenarios A and B, the simulated policy response is a moderate tightening of 50 bps to 75 bps at most in 2026. In the most severe scenario C of a prolonged spike in energy prices leading to a wage response and 5.6% inflation in Q2 2027, all policy rules used in simulations, which are different specifications of Taylor-type rules, point to significant monetary tightening of 100-200 bps in the next year. Persistence of the shock is key to the policy rate path.

Taylor-type rules link policy rates to (expected or contemporaneous) inflation and output deviations from target or potential activity. They provide simple guidance for policy rates but ignore a lot of variables that may affect actual policy decisions including the exchange rate, geopolitical risks, broader financial conditions and so on. There are some other specifics. Unlike other countries, the UK is characterized by a high proportion of fixed-rate mortgages, but generally for short periods (2, 3, or 5 years). Since the 2008 financial crisis and particularly after low-interest rate policies, the share of fixed rates has increased considerably. Variable rates, including base rate tracker mortgages and standard variable rates, represent a minority, but still significant, share of the market. The mortgages initiated in 2020-21 face resets at significantly higher rates (even assuming immediate rate cuts). The status quo on rates thus raises the mortgage interest charges for many households.

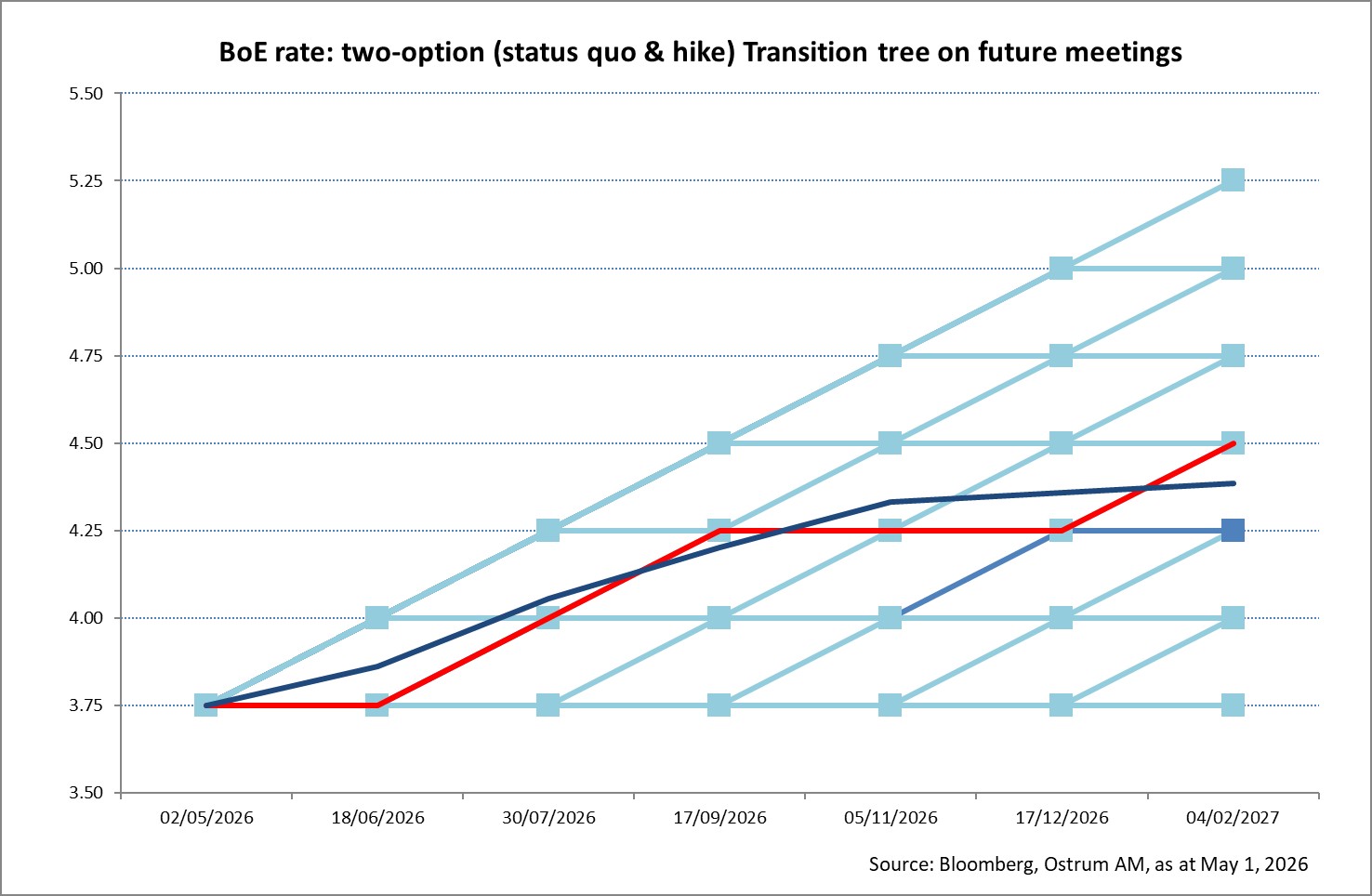

In light of the above, the BoE is considering rate increases, albeit reluctantly. Assuming there are only two policy options, namely status quo or a 25-basis point hike at each meeting, one can infer from overnight index swaps a market-consistent transition tree for policy rates.

As it stands, market participants expect two consecutive hikes in July and Sepetmber and a final hike in February. BoE forecasts for growth and inflation will be updated in August and November.

Conclusion

With hindsight, monetary easing since August 2024 has failed to revive growth whilst inflation rose back above 3%. The Energy price shock from the Iran war make matters worse for the MPC which is having a hard time to agree on the balance of risks. A prolonged crisis scenario may require significant policy tightening but the rhetoric and speech analysis rather point to a prolonged status quo.

Axel Botte

Chart of the week

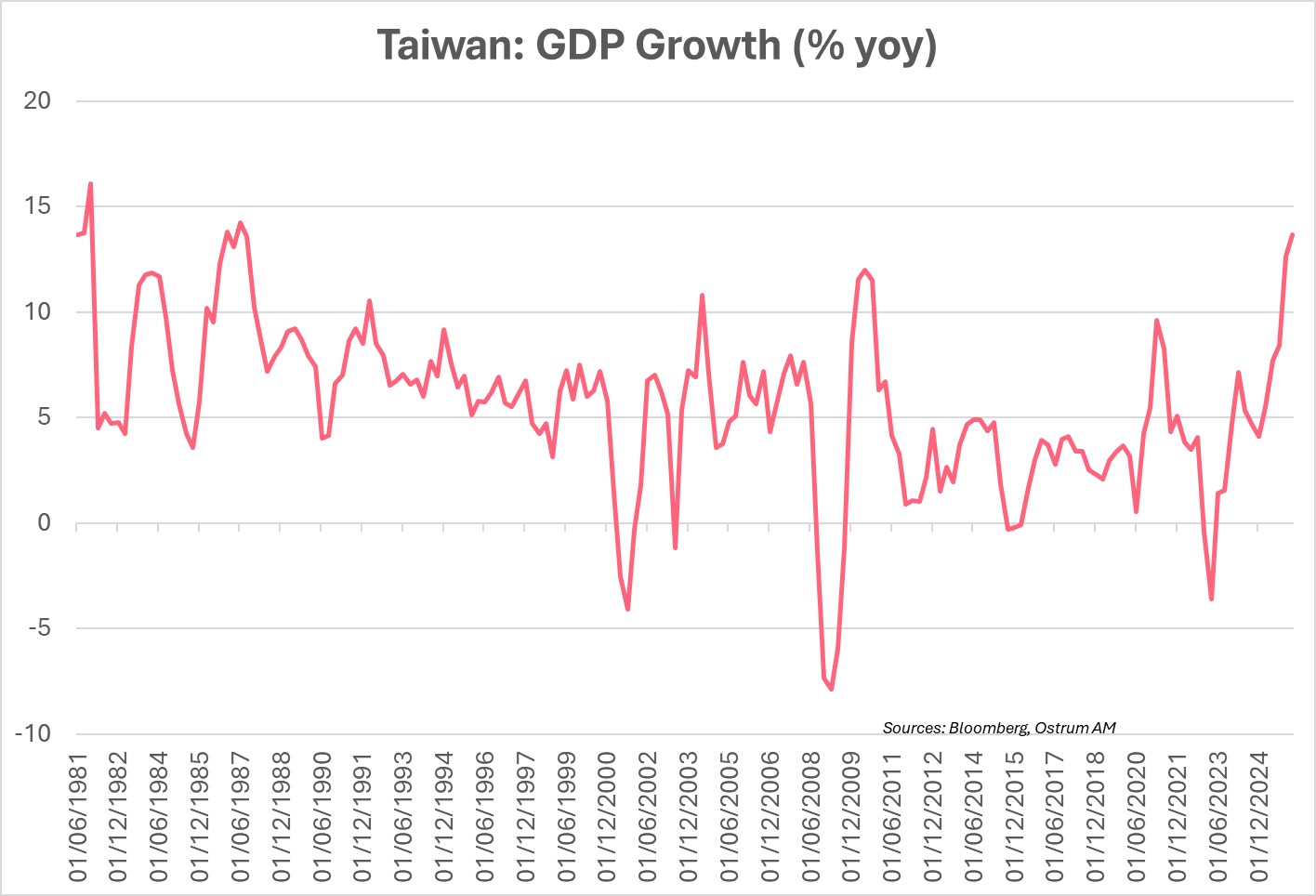

Taiwan’s economy grew in Q1 at the fastest pace since 1987.

Q1 GDP rebounded to nearly 14% year-on-year, driven by technology exports boosted by AI-related demand as well as by rising investment and consumption (4 percentage points contribution to GDP).

The strength of the stock market also supported consumption through a wealth effect.

Figure of the week

5

5 countries have left the OPEC cartel since 2016 after the UAE’s decision to leave on May 1. Incidentally, the UAE’s oil-producing capacity will rise to 5 mbpd by 2027.

Market review:

- Fed: Monetary status quo but statement contested by 4 FOMC members;

- ECB: Lagarde gives free rein to expectations of rate hikes in June;

- Equities: Nasdaq outperforms thanks to solid quarterly earnings;

- Rates: Sharp yield curve flattening with no impact on credit spreads.

Monetary Status Quo Amidst Oil Volatility

Erratic crude price swings continue to dictate the tempo of financial markets, even as solid corporate earnings emerge for Q1. A new Iranian proposal is under review, while central banks maintain their steady course.

Fears of escalating tensions in Iran are injecting a $20-$30 risk premium into oil prices. This upward pressure on short-term rates remains significant, despite the steady hand adopted by all major central banks last week. While yield curves are flattening due to revised inflation expectations, this has had a negligible impact on credit and equities. In government debt markets, Italy's BTP saw a 4 basis point deviation over the week.

The past week was a whirlwind of economic data releases, central bank meetings, and corporate earnings reports, with a particular spotlight on major U.S. technology firms. The U.S. economy expanded at a 2% annualized pace in the first three months of the year. This growth is primarily propelled by business investment, fueled by the advancements in Artificial Intelligence. Capital expenditures are surging (+17.2% annualized), and investment in intellectual property (software, R&D) is up 13%. Conversely, housing investment and household consumption (+1.6%) have lost momentum in recent months. However, weekly ADP data suggests job creation may be poised for an uptick. In the Eurozone, inflation stood at 3% in April. Economic activity data presented a mixed picture: France registered zero growth in Q1, while Germany posted a 0.3% expansion. Spain continues to lead the Eurozone’s economic charge, buoyed by robust domestic demand.

On the central bank front, the Federal Reserve's status quo decision was marked by four dissenting votes. Beyond Steven Miran's vote for a 25 basis point cut, three FOMC members felt the accompanying statement should not signal that a rate cut would be the next move. For the European Central Bank, the duration of the current crisis looms as a significant uncertainty influencing policy. Nothing in its recent commentary appears to challenge expectations of a rate hike in June, when the institution will update its economic projections. The Bank of Japan is also anticipated to opt for a rate increase in June, having revised its core inflation forecast to 2.7%.

Financial markets saw U.S. equities extend their outperformance, driven by robust earnings growth. Following over 300 quarterly reports, annual earnings growth stands at a striking +28%, climbing to an impressive 55% within the technology sector. The Nasdaq gained 1.1%, pushing its year-to-date return to 8%. European equities traded in a mixed fashion, though the earnings season has also yielded positive results there. In fixed income markets, a similar pattern has emerged around oil prices. The surge in crude is prompting a reassessment of short-term inflation expectations, leading to yield curve flattening. The German 2-10 year yield spread narrowed by 3 basis points. Money markets tightened, with the 12-month Euribor increasing by 8 basis points over the week. Longer-dated maturities are seeing increased demand as investors seek to distance themselves from immediate oil-related risks. On the Treasury market, the 30-year T-bond is trading around 5%. Despite interest rate volatility, investment-grade credit spreads have remained stable.

Axel Botte

Main market indicators