Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Listen to podcast (in French only)

(Listen to) Axel Botte’s and Zouhoure Bousbih’s podcast:

- Review of the week – Is US Tech a risk-free asset?;

- Theme – The Great Macroeconomic Pivot: China is going to export inflation.

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: The Great Macroeconomic Pivot: China is going to export inflation

- The energy shock stemming from the conflict in the Middle East has rapidly increased cost pressures for China’s chemicals, plastics and logistics sectors, with these pressures feeding through to factory-gate prices.

- This signal is already visible in the data, as shown by PMI surveys and the return of producer prices to positive territory in March for the first time in more than three years, a precursor to rising selling prices.

- Chinese exporters are beginning to pass these costs on, and several categories of goods are already showing higher export prices.

- The shift in the direction of Chinese economic policy—the end of the “price war” (anti-involution policy), the gradual reduction of certain export subsidies, and the renewed focus on social protection—means China can no longer absorb raw-material price volatility.

- The return of “imported” inflation via Chinese manufactured goods increases uncertainty over monetary policy paths in so-called advanced economies.

From Hormuz to Shenzhen’s factories: an input-cost inflation shock

Despite its strategic oil reserves (1.4 mb/d) and its shift towards renewable energy, China remains vulnerable to the consequences of a blockage of the Strait of Hormuz.

A significant share of refined and petrochemical products (naphtha, liquefied petroleum gas) transits through the Strait of Hormuz. China is one of the world’s largest importers of liquefied petroleum gas, used as a substitute for naphtha when it is cheaper.

The sharp rise in natural gas and crude oil prices is materially increasing cost pressures across China’s chemicals, plastics and domestic logistics sectors.

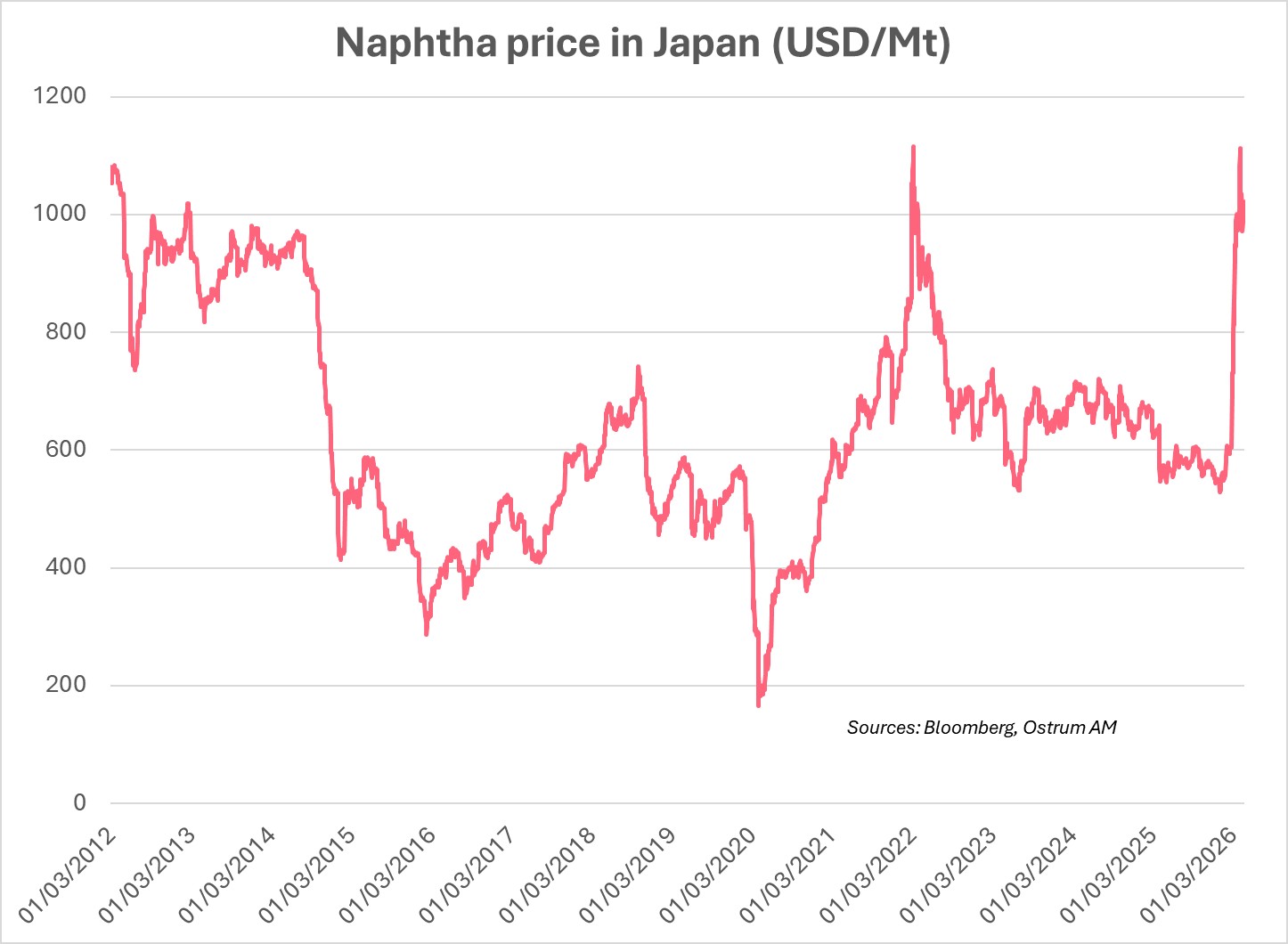

Higher crude prices therefore translate into higher costs for oil-based inputs—first and foremost naphtha, whose prices have risen sharply, as in Japan (up more than 60% since the start of the conflict) to $1,019/mt. China imports naphtha indexed to this Japanese benchmark price.

Around 60–70% of global plastics are indirectly derived from naphtha, with a higher share in Europe and Asia, notably in China.

Military tensions are also disrupting supplies of metals needed for transition-related industries (batteries, electric vehicles). In parallel, higher gas prices are significantly increasing costs in the most energy-intensive segments of the chemicals industry: ammonia, methanol, soda ash, fertilisers and basic chemicals.

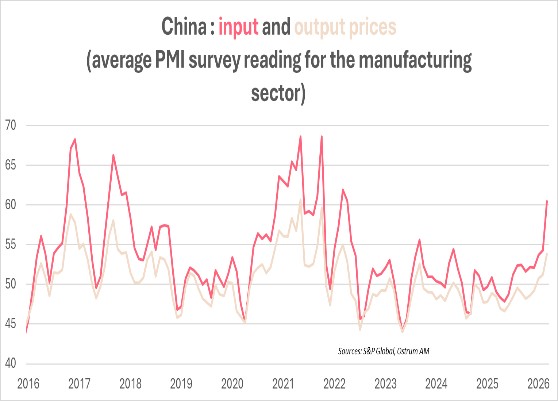

Cost pressures evidenced in the PMI surveys and in the producer price index…

Cost pressures are contributing to the pronounced rebound in input prices reported in the March PMI surveys for the manufacturing sector …

Although electricity generation still relies predominantly on coal (61%), China’s economy remains highly dependent on fuel for road transport, handling and distribution. The sharp increase in crude oil prices has, in turn, driven fuel prices higher, raising delivery costs, while more expensive gas is increasing operating costs for warehouses and logistics hubs (heating, backup generators, etc.). The heightened uncertainty surrounding the conflict also lifts insurance premium and freight rates, wich feed directly into import prices.

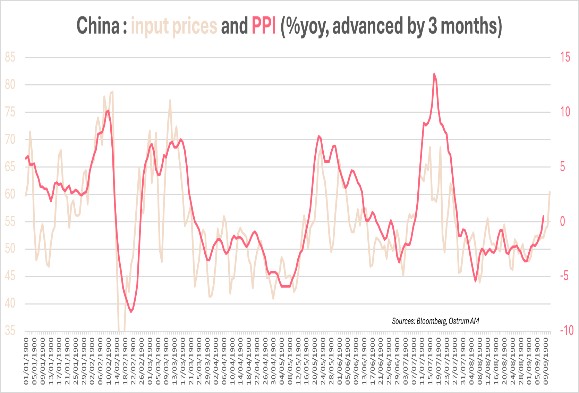

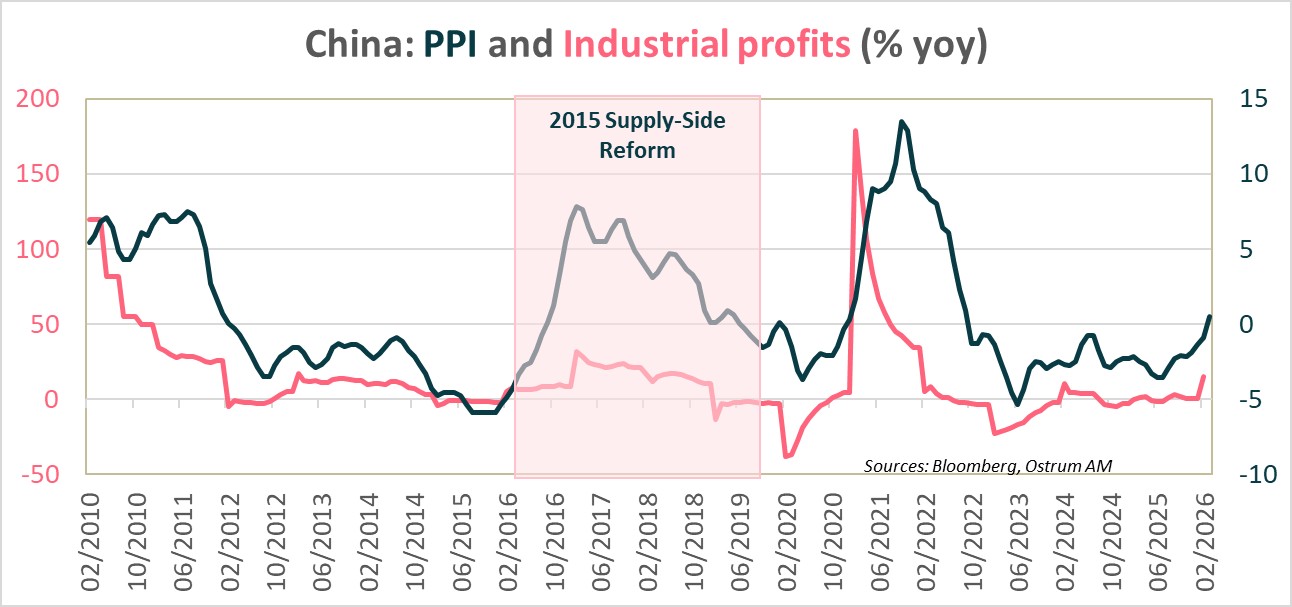

This domestic logistics channel is contributing to the rebound in “prices paid” reported in the March PMI surveys for the manufacturing sector, before being transmitted to the producer price index (factory-gate prices). These higher input and transport costs have already resulted in producer price inflation turning positive in March, at 0.5% y/y, for the first time in 41 months. As a result, upward pressure on selling prices is intensifying, particularly for low unit-value products (basic chemicals, plastics).

… and have already translated into a renewed increase in producer prices, for the first time in more than three years!

…Already resulting in higher export prices

Chinese exporters have begun to pass the increase in input costs through to export prices.

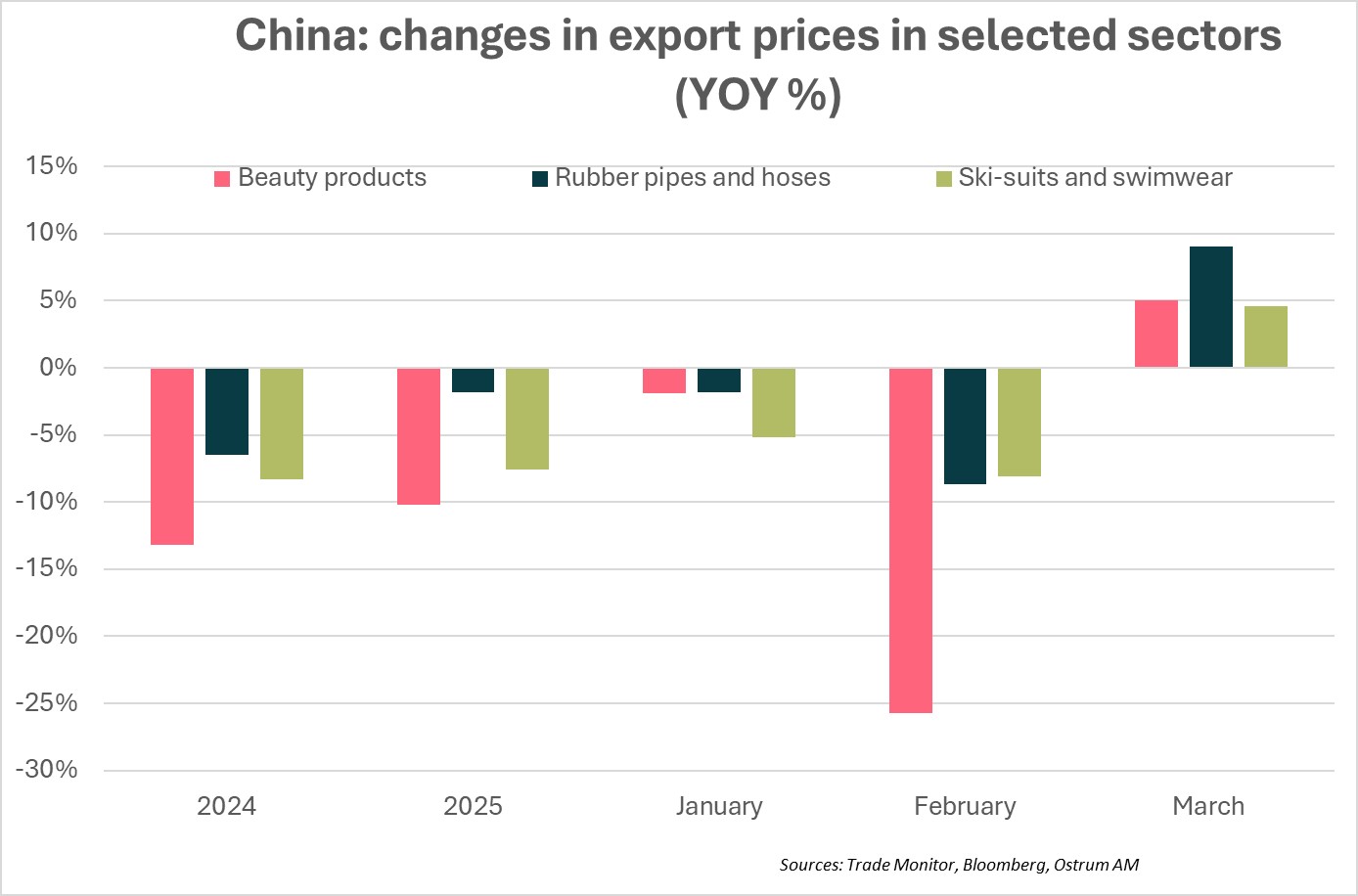

According to Trade Monitor data analyzed by Bloomberg, more than a dozen product categories recorded a marked rise in export prices in March, as illustrated in the chart below.

Export prices for more than a dozen product categories have already begun to rise.

Accordingly, export prices for beauty products (+5% y/y), rubber tubes and hoses (+9% y/y), and ski suits and swimwear (+4.6% y/y) have reversed the downward trend observed over the previous three years.

China’s export prices fell again in February to -5% y/y, extending the decline observed since May 2023. Persistently elevated crude oil prices should lend support to Chinese export prices and, in turn, contribute to higher headline inflation.

Why China can no longer absorb these costs this time around

The anti-involution policy and the reduction of excess capacity

The anti-involution policy—aimed at reducing excess production capacity—brings the fratricidal ‘price war’ among Chinese firms to an end.

Beijing is now seeking to curb the fratricidal “price war” among Chinese firms to preserve margins and safeguard financial stability. Accordingly, since mid-2025, the Chinese authorities have rolled out the anti-involution policy to address excess production capacity.

Reduced price competition should translate into higher producer prices, which would, in turn, lift selling prices.

In parallel, industrial profits rebounded by 15.5% y/y in Mars , up from 15.2 % in the January–February period (the two-month aggregate is used to limit distortions related to the Lunar New Year), and well above the 0.6% y/y recorded for full-year 2025.

Rebalancing the trade balance

Criticised for its large trade surplus ($1.2 trillion in 2025), Beijing is acknowledging these imbalances. In early March 2026, China’s Minister of Commerce, Wang Wentao, stated that China aims to “stabilise exports while expanding imports,” notably of agricultural products, high-quality consumer goods, advanced technology and key components.

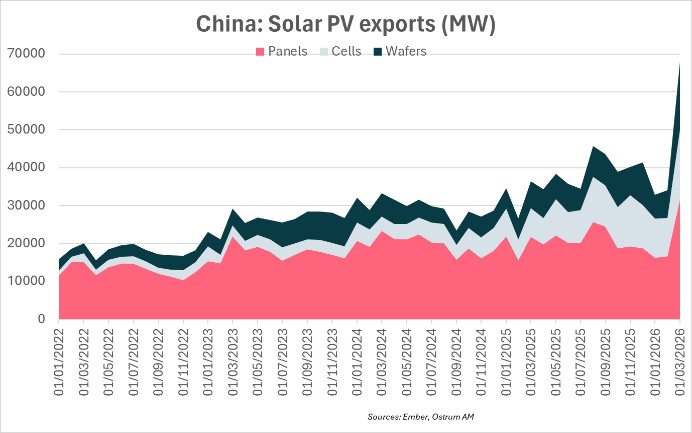

Export prices for low—and even very low—value-added goods are set to rise as subsidies are gradually phased out in sectors facing excess capacity, such as solar.

Among the measures announced, the authorities intend to reduce export subsidies for low value-added goods and to redirect financial resources towards social protection. This implies that export prices for these low—indeed very low—value-added goods will rise.

Thus, the withdrawal of the tax rebate on solar panels, effective 1 April, led to record solar exports of 69 GW in March—double the February level—as shown in the chart opposite.

This is equivalent to Spain’s entire solar capacity. The conflict in the Middle East is also boosting demand for clean technologies, notably from countries that are highly vulnerable to the energy shock.

Refocusing on social protection to strengthen services consumption

The renewed emphasis on social protection—aimed at strengthening consumption, particularly in services—reduces firms’ scope to contain costs through wage restraint.

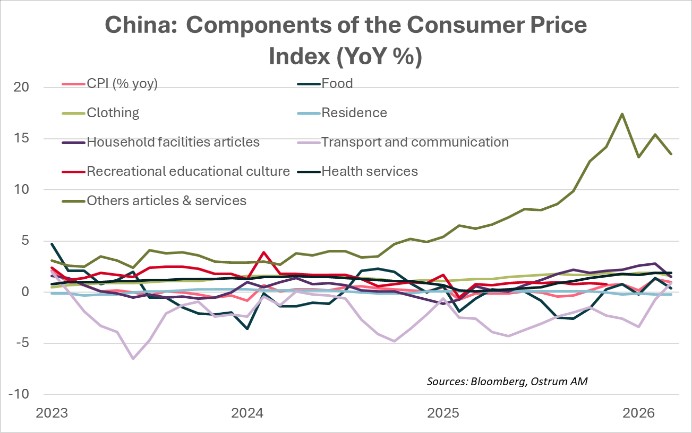

While China’s headline inflation remains subdued (1% in March), services inflation is elevated (13.5%), as shown in the chart opposite. Elevated services inflation therefore limits the room for wage compression.

Conclusion

The energy shock associated with the conflict in the Middle East is acting as a catalyst for China, accelerating the pass-through of higher costs to factory-gate prices (producer prices) and, subsequently, to export prices. Whereas China has long “imported” commodity-price volatility and absorbed it for the benefit of the rest of the world, Beijing now has materially less room for maneuver. Efforts to curb excess capacity and the price war, the intention to rebalance a trade surplus that has become politically costly, and the renewed focus on social protection and domestic consumption all constrain Chinese firms’ ability to compress margins—or wages—on a sustained basis. In this environment, the principal risk is not merely a temporary rebound in input prices; rather, it is the prospect of a renewed wave of imported inflation transmitted through manufactured goods, which could complicate the disinflation process among China’s trading partners and heighten uncertainty regarding the future path of monetary policy.

Zouhoure Bousbih

Chart of the week

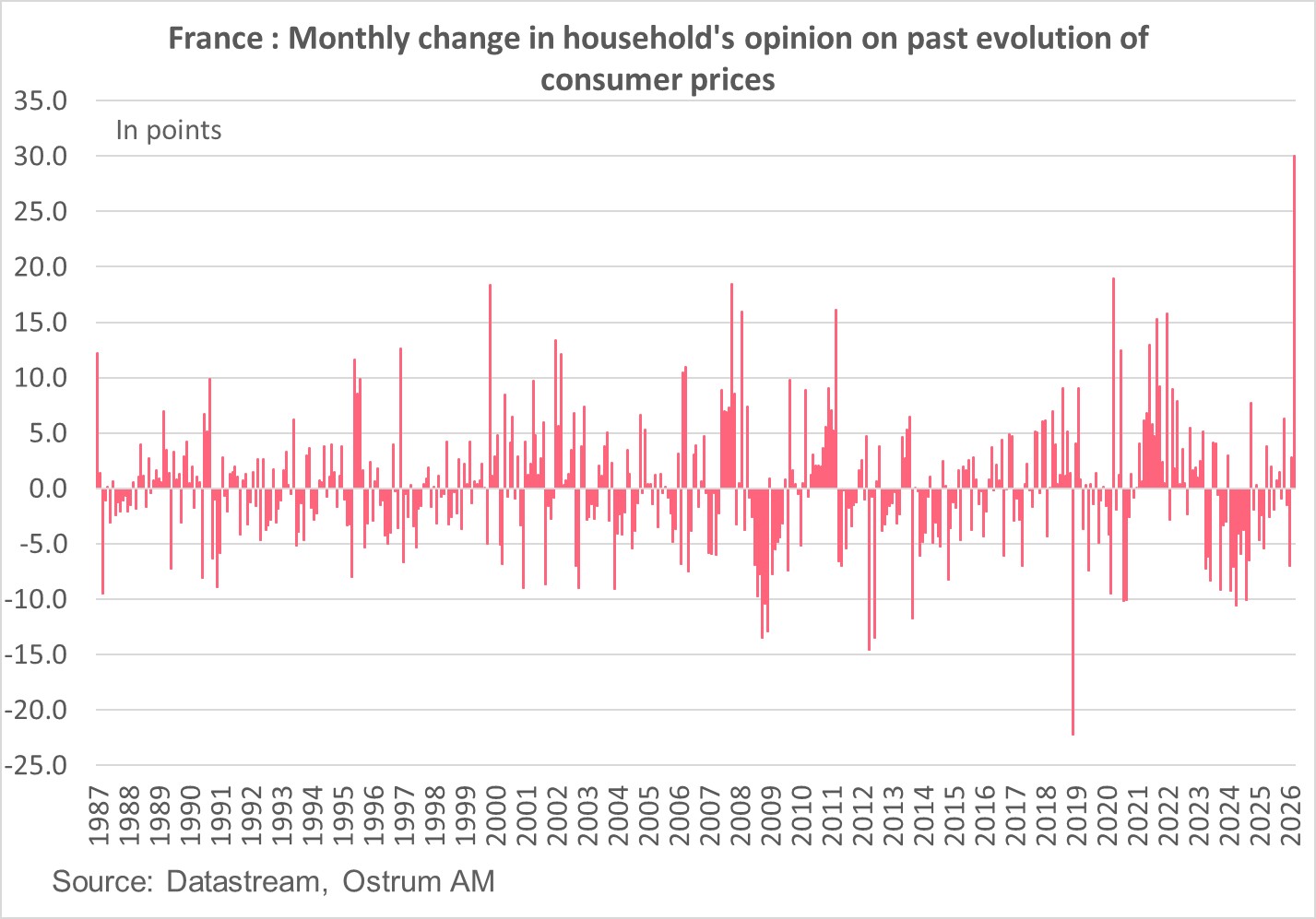

French household confidence has fallen by 5 points in April, the sharpest decline since March 2022 and the beginning of the war in Ukraine. It now stands at 84, a level significantly below its long-term average (100).

Households' opinions on their current and future financial situation have clearly deteriorated. This is due to the sharp rise in the inflation component.

Opinions on past price developments recorded their largest monthly increase since the series began in 1987: +30 points. This is a highly concerning factor for the ECB.

Figure of the week

10

That’s how many monetary policy meetings are scheduled this week, including the Fed and the ECB—likely with no change in rates.

Market review:

- Iran: Markets subject to oil price swings find an escape route in Tech;

- Growth: survey indicators mixed amid Iran crisis;

- Equities: US stocks outperform;

- Rates: the rebound in oil prices results in flattening pressure.

Is U.S. Tech the New Risk-Free Asset?

The Iranian situation appears intractable. Oil's rebound is reviving yield curve flattening detrimental to risk assets. Nevertheless, U.S. equities are holding firm.

One of the most unexpected characteristics of the Iranian crisis is the absence of significant reactions from traditional haven assets. Gold—too expensive and speculative—the T-note weighed down by de-dollarization themes and war costs, and the Swiss franc all appear to have lost their safe-haven status. Conversely, the U.S. technology sector, buoyed by quarterly earnings releases, has emerged as the sole source of diversification in binary markets dictated by oil price swings.

Eurozone surveys often prove contradictory. The prevailing uncertainty renders these cyclical indicators particularly sensitive to polling dates. April's manufacturing PMI rebound, for instance, contrasts with the decline in Germany's Ifo index. The absence of genuine negotiations toward resolving the Hormuz blockade invariably pushes oil prices back above $100 per barrel. Donald Trump, facing a political impasse, threatens to resume air strikes. U.S. growth nevertheless appears to be improving despite the blow to consumption. Energy goods exports are exploding in April, while corporate investment spending remains well-oriented. Private sector job creation should approach 150-200k in April, according to weekly ADP data. However, major technology companies (Microsoft, Meta) are hastily restructuring with redundancy plans designed to restore the agility needed to confront the challenges of artificial intelligence's breakneck growth. The outcome of the U.S. cycle will depend on hyperscalers' ability to maintain planned investments and subsequently monetize them. The impact of AI—supposedly disinflationary over time—represents a structural element for central banks. Incoming Fed Chair Kevin Warsh will likely see grounds for resuming easing by year-end. The ECB remains more skeptical, with anticipated inflation having risen in most surveys.

Oil's binary market dynamic is being constantly reactivated. The only escape valve is U.S. technology. Short-rate tensions have been reignited, pushing the 10-year Bund beyond 3% and the T-note toward 4.30%. Uncertainty peaks on Gilts due to the lack of consensus within the Monetary Policy Committee. Oil's $15 rebound has induced sharp yield curve flattening detrimental to risk assets. The eurozone's 2-10 year spread has tightened by 12 basis points over the week, while the 30-year Bund remained unchanged. Long-term bond convexity offers superior and inexpensive protection, reducing rate volatility's impact.

Eurozone sovereign spreads have widened proportionally—from 2 basis points on Irish debt to 8 basis points on Greek and Italian bonds. Credit remains stable compared to CDS indices used for hedging and therefore more reactive to international developments. The iTraxx Crossover has widened roughly 15 basis points over five sessions. Emerging market debt spread tightening (243 basis points) continues independently of U.S. rate volatility.

In equity markets, technology offers exposure orthogonal to the oil crisis. First-quarter earnings confirm anticipated strong growth, overshadowing concerns about colossal AI infrastructure investments. The S&P 500 is flat on the week while Europe has lost 2%.

Axel Botte

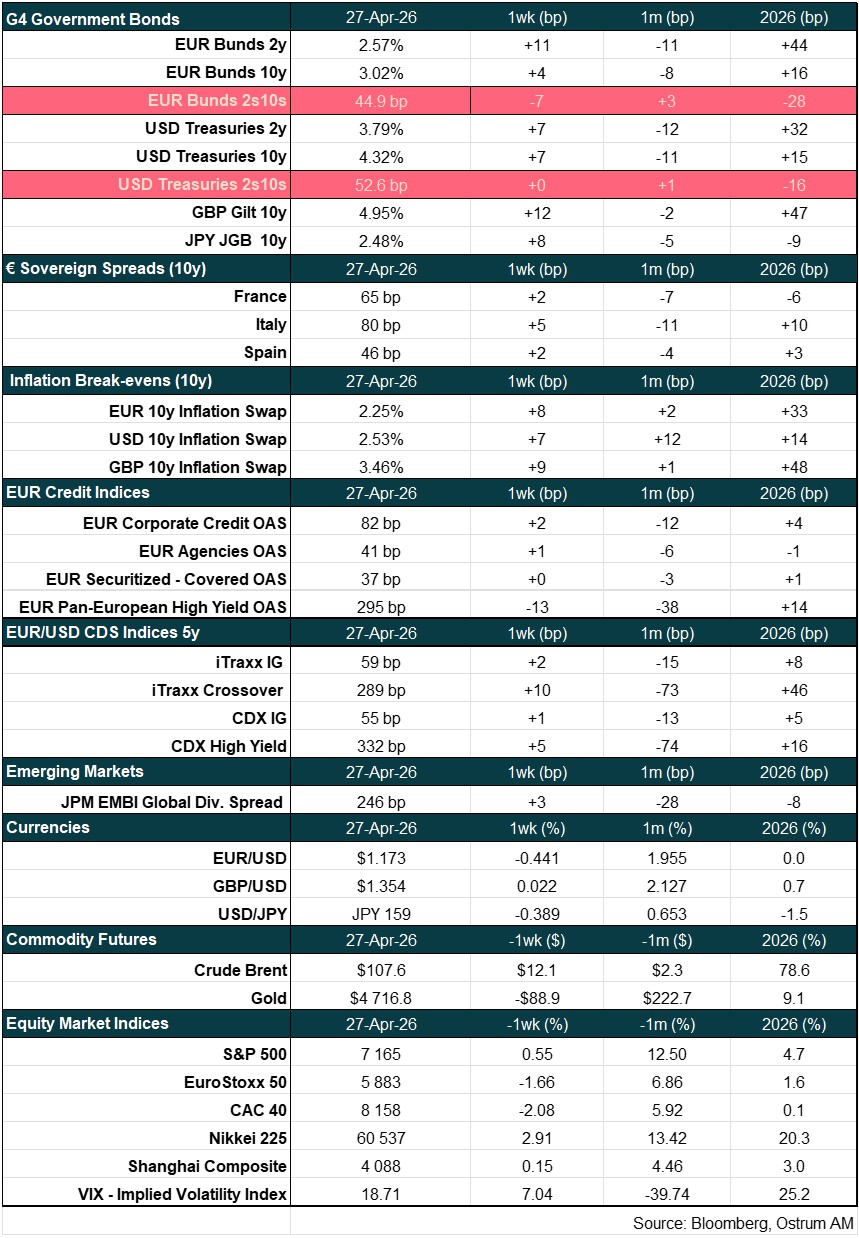

Main market indicators