Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Listen to podcast (in French only)

(Listen to) Axel Botte’s and Zouhoure Bousbih’s podcast:

- Review of the week – U.S. employment rebounds;

- Theme – Emerging Markets external sovereign debt: from resilience to volatility?

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week:Emerging Markets External Sovereign Debt: From Resilience to Volatility?

- Emerging market external sovereign debt has demonstrated notable resilience, with a significantly more muted market reaction than during previous major shocks, despite a deteriorating geopolitical backdrop.

- However, this apparent resilience masks substantial performance dispersion, largely driven by the divergence between net commodity exporters and importers.

- Africa and Latin America have benefited from the energy shock, while Asia and the Middle East remain weighed down by higher energy import costs and persistent geopolitical risk premia.

- As the shock persists, macro-financial risks are intensifying (inflation, external imbalances, pressure on sovereign ratings), once again making country-level selectivity a key driver for the asset class.

- The broad and diversified nature of the asset class allows investors to capture opportunities arising from the reconfiguration of trade and energy flows linked to geopolitical tensions.

Emerging Markets External Sovereign Debt: From resilience to volatility?

Emerging markets external sovereign debt has demonstrated notable resilience despite the energy shock triggered by the conflict in the Middle East. Structural improvements in emerging economies’ fundamentals, supported by the implementation of robust reforms, have enabled the asset class to better withstand the volatility spike compared with previous crises. The broad diversity of the investment universe—dominated by net commodity exporters and producers that have benefited from higher prices—has also provided support to the asset class. However, as the conflict persists, the shock is increasingly extending beyond inflationary pressures, weighing more broadly on emerging credit profiles through weaker demand and deteriorating fiscal balances. Country-level differentiation is once again becoming a key structural driver for the asset class.

Remarkable resilience compared with previous major shocks…

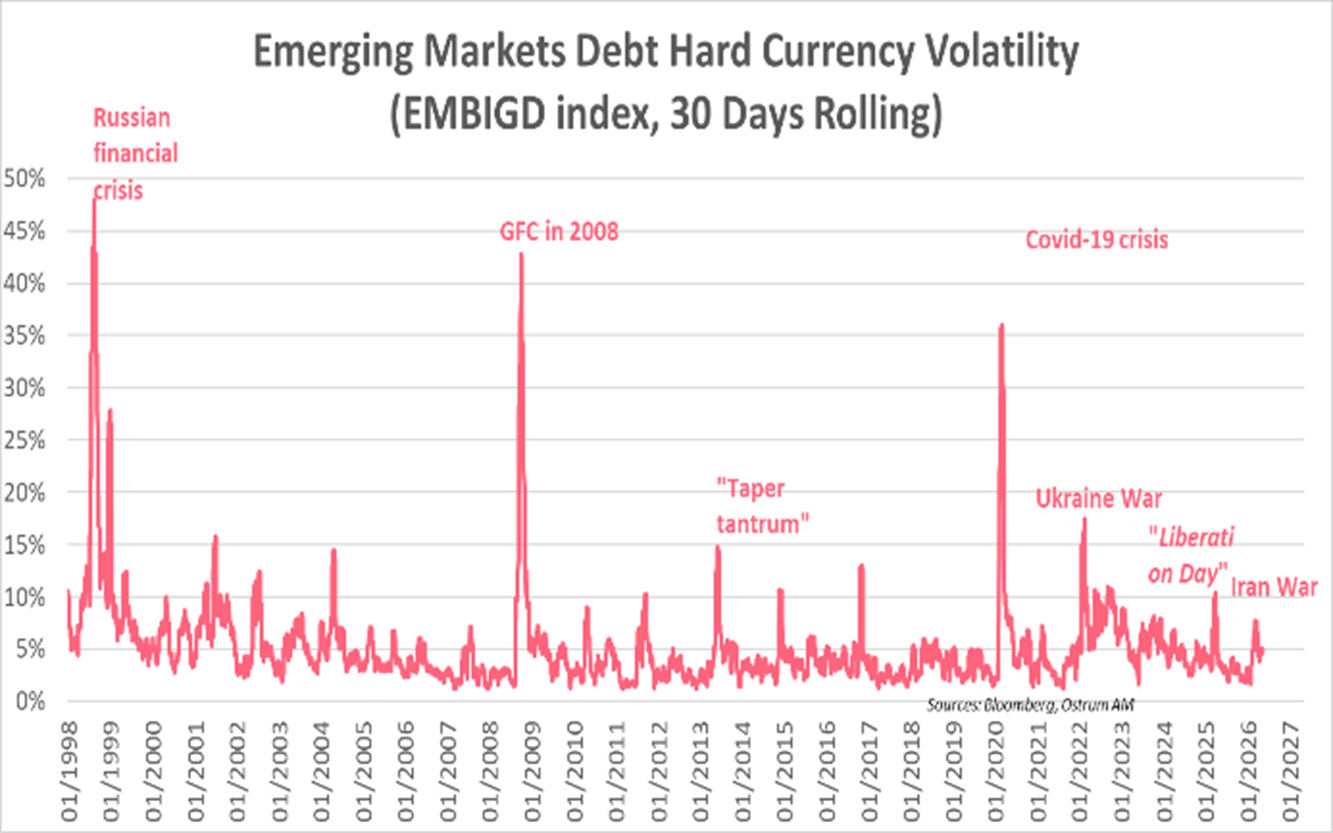

The conflict in the Middle East has triggered a significantly more contained volatility response in emerging markets external sovereign market debt (JPM EMBIGD index) compared with previous major shocks.

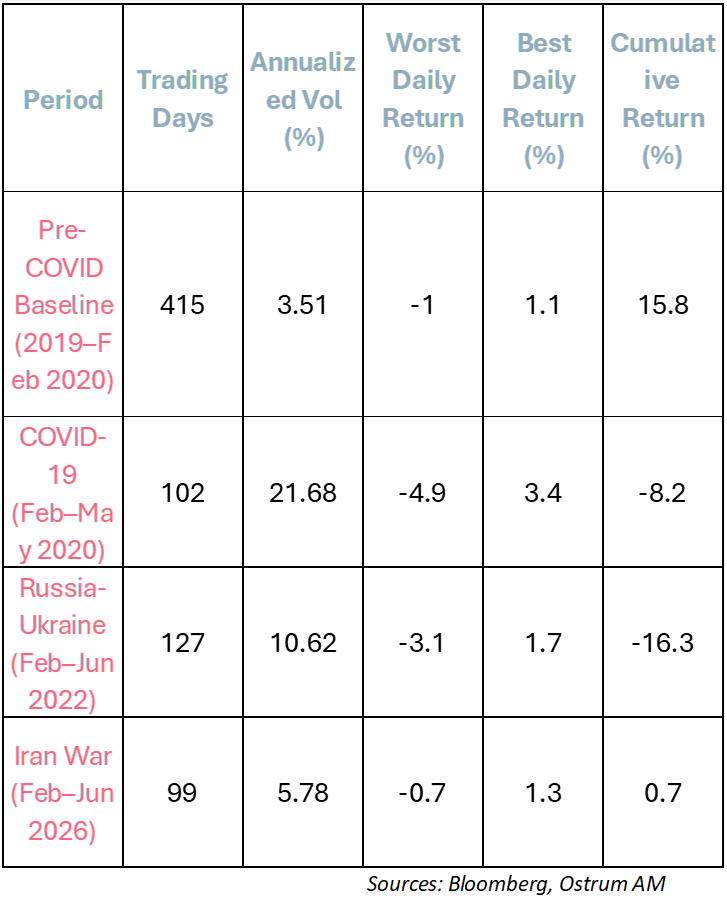

The table opposite compares annualized volatility, extreme daily returns, and cumulative performance across different shock periods.

The COVID-19 crisis by far represents the most severe shock for emerging market external sovereign debt, with annualized volatility exceeding 21%—more than six times pre-Covid levels. The war in Ukraine ranks as the second most severe shock, with volatility above 10% and cumulative performance of -16.3%, the worst across all major shocks analyzed. This underperformance reflects a sustained widening of spreads and the interest rate shock associated with conflict-driven inflationary pressures.

By contrast, the shock linked to the Iran war (2026) appears to be the most moderate in terms of volatility (5.8%), close to the pre-Covid regime (3.51%). The worst daily performance was also significantly less pronounced (-0.7%), while cumulative performance remained broadly stable (+0.7%). EMBIGD spreads widened by only 17 basis points, pointing to a limited and orderly market reaction. Moreover, although the VIX index recorded a sharper increase than in 2022—indicating elevated volatility in U.S. equities (see chart)—the JPM EMBIGD index absorbed the shock with greater resilience.

What explains this notable resilience?

Structural improvements in fundamentals, supported by the implementation of robust reforms, have enabled the asset class to better withstand volatility spikes compared with previous exogenous shocks. The breadth and diversification of the investment universe also constitute a key strength. Some 70 countries are represented in the JPM EMBIGD index, with the dominance of net commodity exporters and producers that have benefited from higher prices, thereby improving their credit profiles. Finally, market participants’ perception of the shock’s duration has also played a role: expectations of a relatively short-lived episode have contributed to containing volatility across the asset class.

…But masking significant dispersion

Emerging markets external sovereign debt started 2026 on a strong footing, driven by the same themes as in 2025: favorable macroeconomic conditions and robust country fundamentals. A weaker US dollar and spread compression were the main contributors to EMBIGD index performance during the first two months of the year.

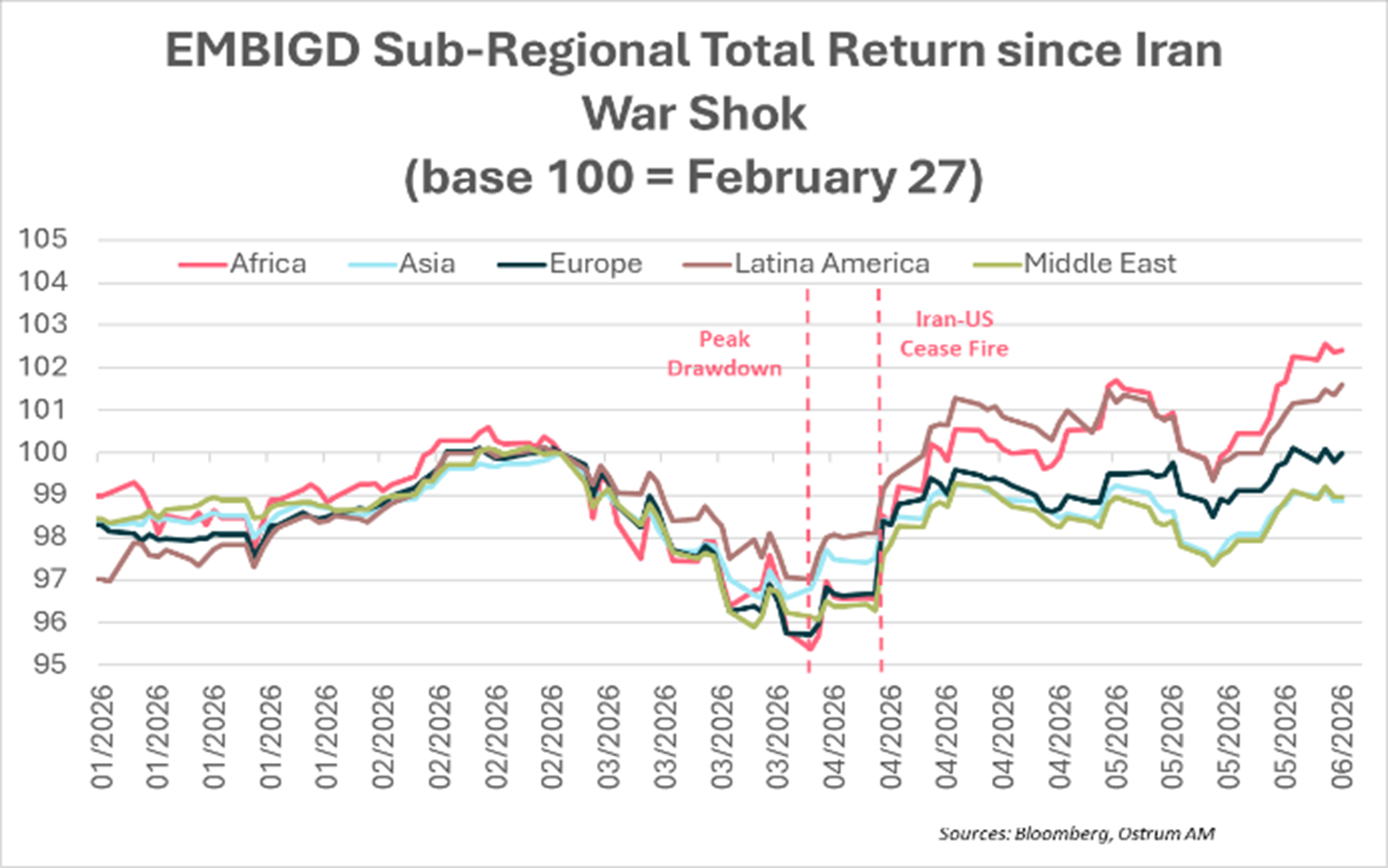

These initial gains reversed in March, as the war in Iran triggered the largest regional divergence within the JPM EMBIGD index since the Ukraine conflict, as illustrated in the chart of regional sub-index performance.

The key driver behind this dispersion is the dichotomy between commodity exporters and importers.

During the initial shock phase (from February 28 to end-March), the Middle East and Europe were the most affected, with a peak drawdown of -4%, reflecting both geographical proximity and strong dependence on energy imports. Africa also recorded its worst drawdown (-4.4% on March 30), driven by idiosyncratic credit stress in high-beta countries. Latin America proved the most resilient, with a drawdown of -2.9%, supported by its geographic distance and higher commodity prices.

Asia experienced a -3.4% drawdown, reflecting its heavy reliance on energy imports from the Middle East, with countries such as the Philippines, India, and Indonesia contributing to the underperformance.

The announcement of a ceasefire on April 7–8 triggered a broad-based rebound across EMBIGD sub-indices, led by Africa and Latin America. The Middle East, however, remained in negative territory, reflecting a persistent geopolitical risk premium. Europe temporarily returned to positive territory before slipping back into negative territory in May.

During May, a new wave of sell-off hit emerging market external sovereign debt, with the Middle East (-2.7%) and Asia (-2.2%) posting the largest spread widening before a partial rebound.

Africa—supported by oil exporters such as Nigeria and Angola, along with improving credit fundamentals in Sub-Saharan Africa—recorded the strongest performance since the start of the conflict (+2.5%), extending its gains. Latin America posted the second-best performance (+1.6%), driven by Brazil and Colombia benefiting from elevated oil prices.

Since the beginning of the conflict, Africa and Latin America have outperformed Asia and the Middle East by 350 basis points, as well as the EMBIGD index, which has delivered a return of 0.6%.

The duration of the conflict will be a key determinant of the asset class’s medium-term outlook

Rising pressures from the energy shock are likely to drive a redistribution of risk within the asset class. The duration of the conflict will be critical in shaping credit profiles.

Inflationary and external pressures are intensifying. Several countries, particularly in Southeast Asia, have swiftly implemented measures to address disruptions in crude oil supply. Indonesia and India have maintained administered fuel prices, thereby amplifying fiscal constraints. The sustainability of such policies, along with the associated budgetary pressures, represents a key medium-term challenge.

The deterioration in fundamentals among net energy-importing countries is not yet fully reflected in risk premia but is increasingly visible through sovereign rating downgrades.

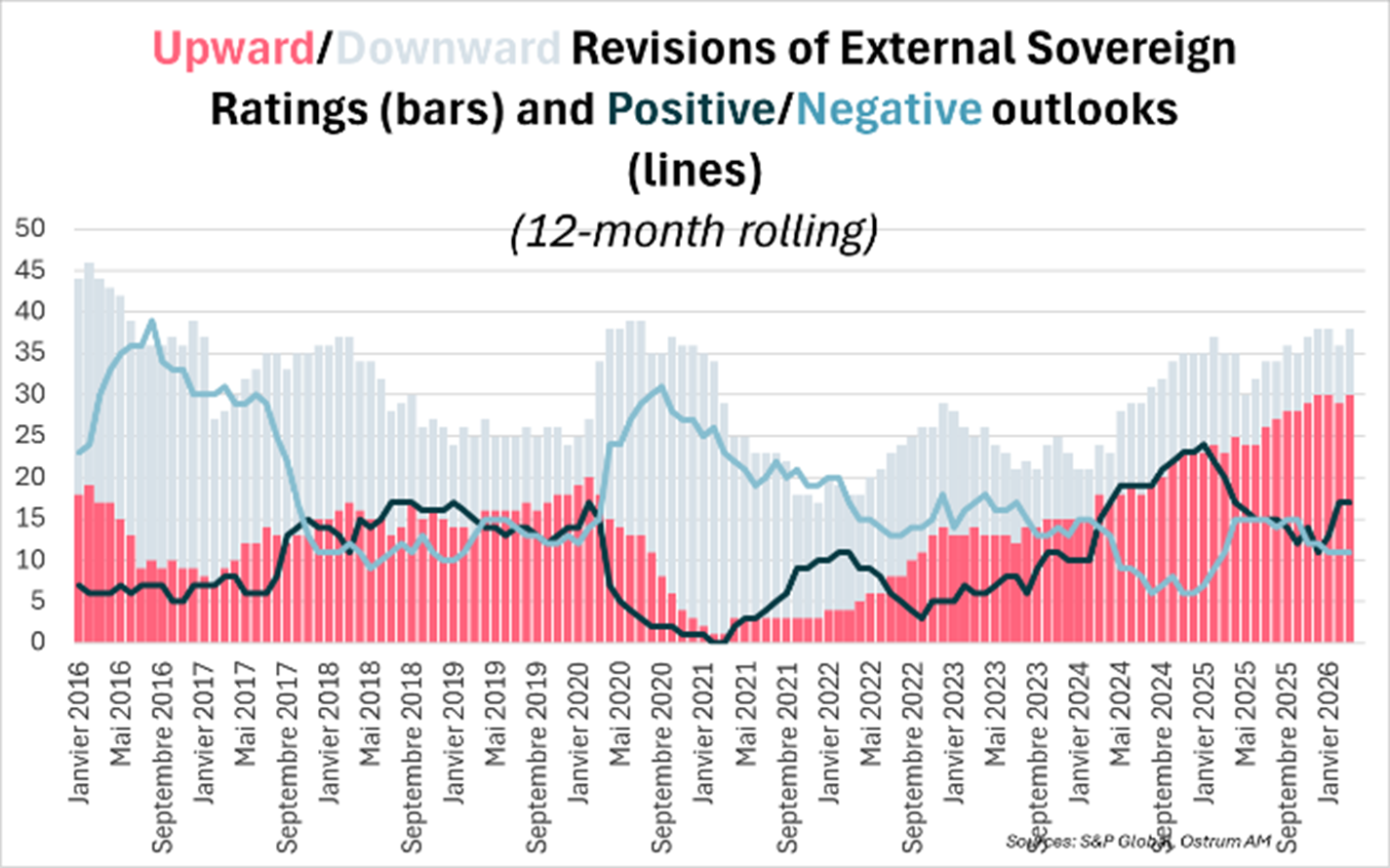

Indeed, in April, S&P carried out 4 upward revisions against 15 downward revisions of external sovereign ratings, reversing the positive trend that had been underway since 2023, as illustrated in the chart opposite. Oil-producing and exporting countries are not immune. Mexico, for instance, saw its external sovereign rating downgraded by Moody’s to Baa3—just one notch above high yield—raising the risk of a “fallen angel.” The country is also facing multiple headwinds, including restrictive U.S. migration and trade policies.

The improvement in outlook (17) has also stalled since February, reflecting significant uncertainty about the impact of the energy shock on macroeconomic prospects.

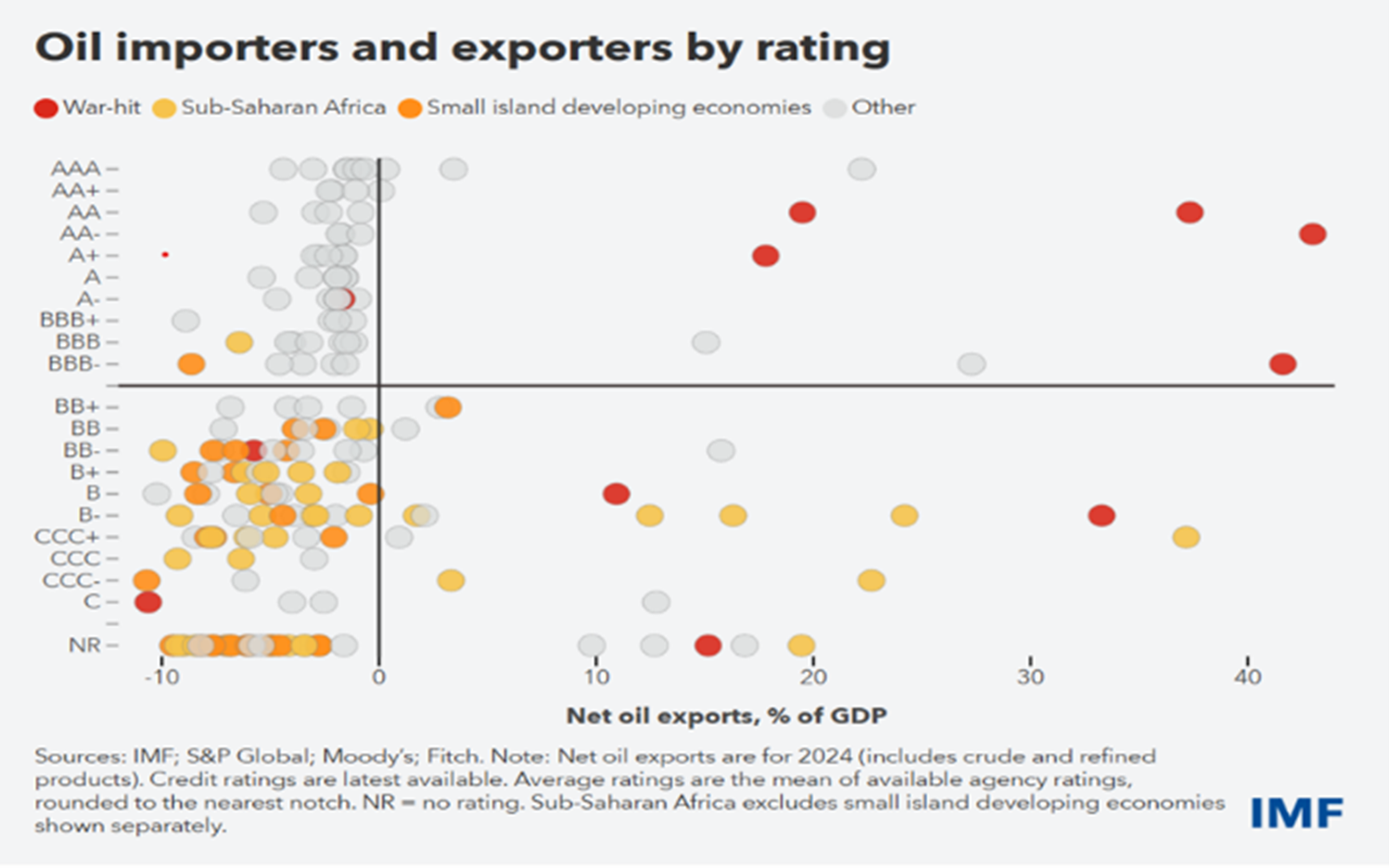

Sub-Saharan African countries, which already carry the weakest external sovereign ratings, are the most vulnerable to persistently high oil prices, as shown in the IMF chart opposite.

Egypt, a net oil importer, has seen its spread tighten back to 360 basis points—15 basis points tighter than at the onset of the Iran war. However, the country continues to face surging inflation, twin deficits (current account and fiscal), and ongoing currency depreciation. Angola and Nigeria are among the main beneficiaries of the energy shock, but remain heavily dependent on imports of refined petroleum products (notably gasoline).

Conclusion

Emerging market hard currency sovereign debt has demonstrated notable resilience in the face of the energy shock triggered by the war in Iran, with a significantly more contained market reaction than in previous crises. However, this resilience masks increasing dispersion driven by the divergence between net oil-exporting and importing countries. Mounting pressures from the energy shock—rising inflation, strains on external positions, and a gradual deterioration in sovereign ratings—could lead to a new phase of spread widening. Country selection is once again becoming critical for the asset class, whose broad and diversified universe offers opportunities to capture the reconfiguration of energy and trade flows triggered by geopolitical tensions.

Zouhoure Bousbih

Chart of the week

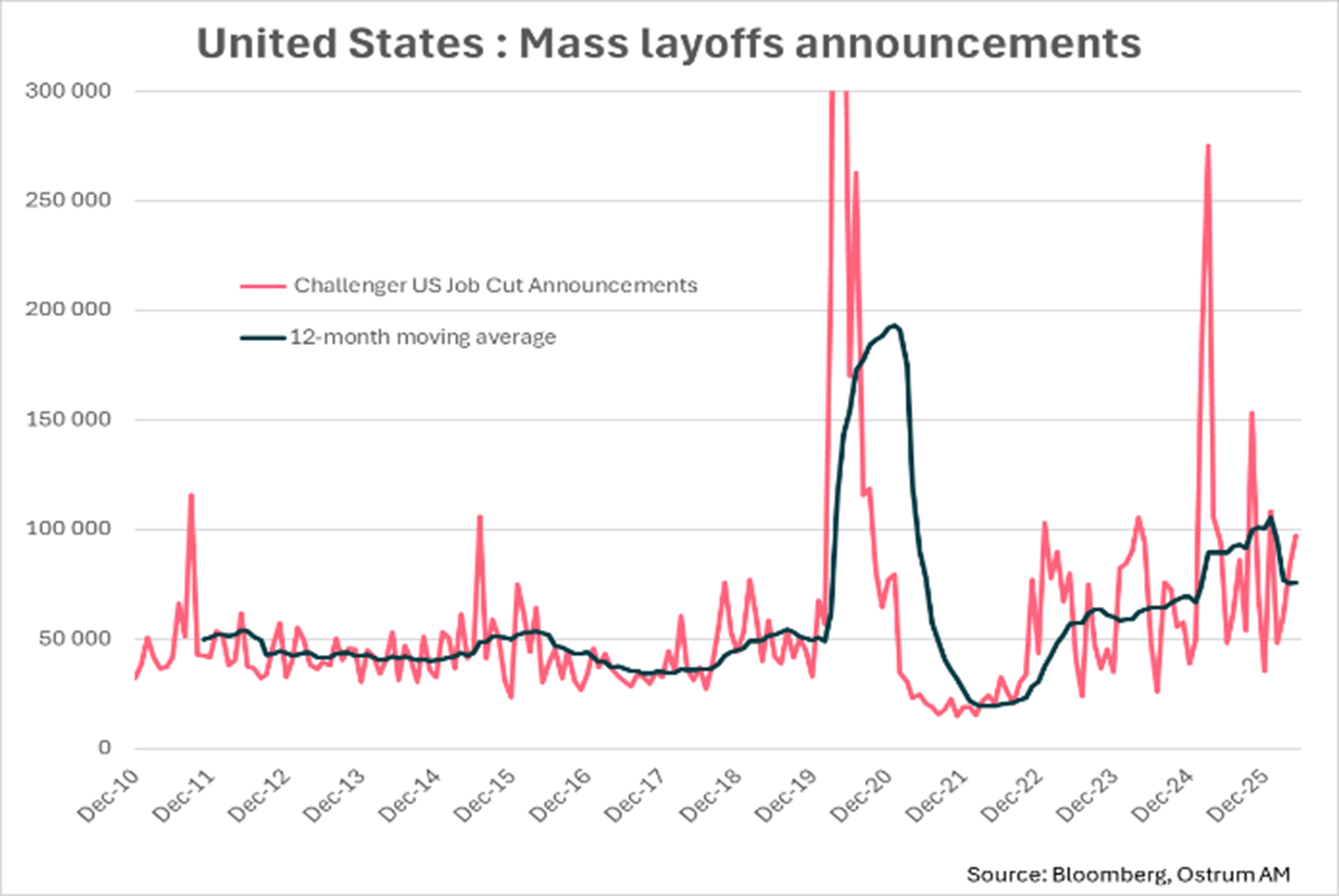

U.S. employers announced 97k job cuts in May, up 16% from April and up 3% from the 93k announced in May 2025, according to the Challenger survey. This marks the third consecutive month of rising cuts.

Since the beginning of the year, employers have announced 397k cuts, down 43% from the 696k announced during the first five months of 2025, when DOGE reductions in the federal workforce drove totals to historic highs. Beyond the AI impact (responsible for 37k of the 97k cuts), the sharp increase in layoffs appears linked to mergers and acquisitions, rising bankruptcies, and corporate restructuring as companies seek to adapt to an AI-driven economy.

Figure of the week

2,400

Foreigners sold another 2.4 trillion won ($1.6 billion) of the Korean benchmark’s shares as of midday in Seoul, taking this week’s exit to more than $10 billion

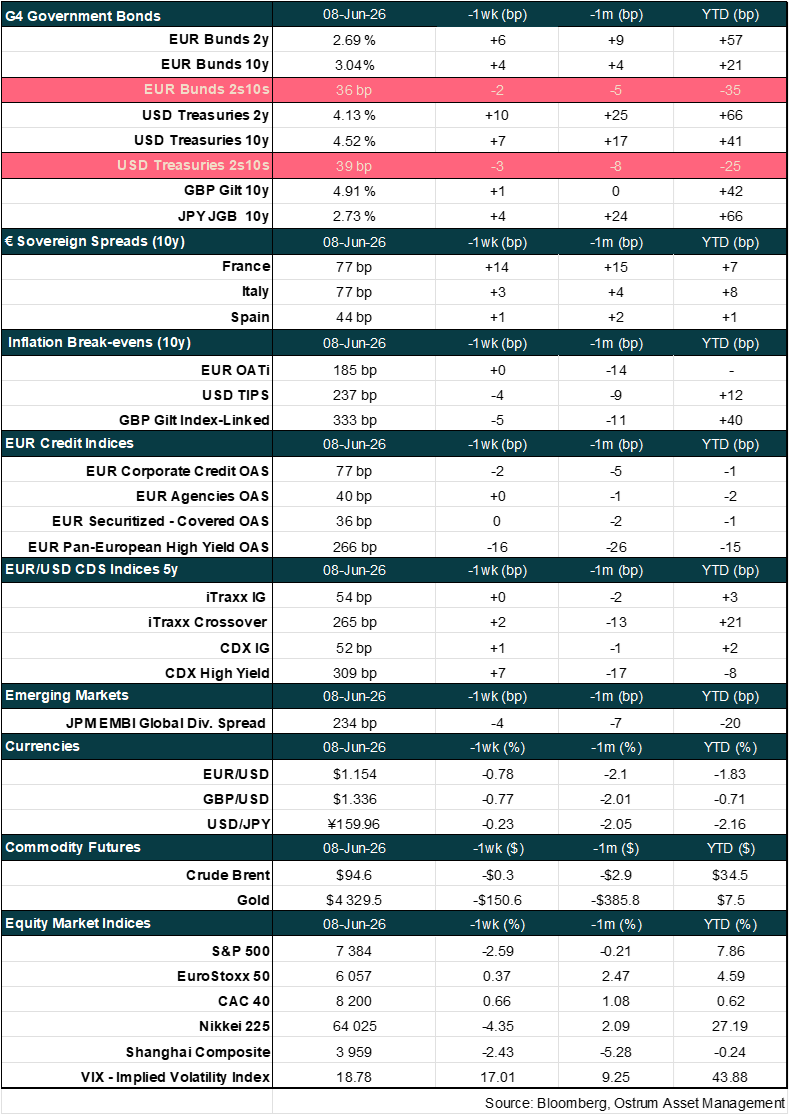

Market review:

- United States: 172k job creations in May, unemployment stable at 4.3%;

- Eurozone:Rising core inflation validates the expected ECB rate hike ;

- Rates: Bund around 3%, T-note moves back above 4.50%;

- Equities: SpaceX's upcoming IPO weighs on the AI theme.

U.S. Employment Rebounds

Markets are pricing in Fed rate rises following favourable jobs data. The T-note climbs back above 4.50% while SpaceX's upcoming IPO weighs on equity markets.

Bond markets remain subject to oil volatility and the absence of concrete progress toward resolving the Iranian crisis. Meanwhile, Kevin Warsh's arrival is prompting FOMC members to call for less accommodative U.S. monetary policy, particularly as employment figures improve. The relentless surge in AI stocks is now triggering profit-taking, notably in Asia, as portfolio managers make room ahead of SpaceX's public listing. Long-term rates are oscillating around 4.50% on the T-note and 3% on the Bund. Spreads and equity volatility remain contained.

U.S. labour market data has been improving since mid-March. The American economy created 172,000 jobs in May after 179,000 in April (post-revisions). The caveat is that most private job creation (+120,000) is concentrated in healthcare and leisure sectors. This has resulted in continued deceleration in average hourly earnings (+3.4% in May), which no longer cover annual inflation. Unemployment's stability at 4.3% of the labour force masks a significant decline in participation and employment rates, which has accelerated since autumn. This is arguably the most challenging configuration for Kevin Warsh, who will chair his first FOMC on 17 June. Growth appears to be improving but depends disproportionately on AI investments and consumption by the top income decile. In Europe, activity contracted 0.2% in Q1. The reversal in surveys is significant in April-May, with inflation accelerating (3.2% in May). The energy shock (+10.9%) is spreading to services inflation (+3.5%) and more broadly to core inflation (+2.5%).

In financial markets, Fed members calling for less accommodative policy are emboldened by rising employment. The 10-year Treasury has thus moved back above 4.50%. Put option volumes on the T-note have increased substantially in recent weeks, perhaps indicating resistance to further rises. Kevin Warsh's speech will be particularly important. Markets will test the Fed's appetite for raising rates, now pricing in a hike by year-end. This is resulting in sharp flattening of the 2-10 year spread. The Bund appears directionless around 3%. Volatility is moderating somewhat after a period marked by abrupt oil price swings. The oil price is slightly below $100. Long-term inflation breakevens have retreated modestly. Sovereign spreads are moving marginally. The French debt spread has widened 3 basis points on the week to 65 basis points. Italian BTPs trade at 75 basis points ahead of a new household-targeted inflation-linked bond launch that could lighten the issuance calendar in coming weeks. Similarly, IG credit spreads are stable at 65 basis points over swaps. Investment flows into credit funds have decelerated but remain predominantly inward. High yield spread tightening has been impressive (-23 basis points over the month). Equity markets are losing momentum late in the week on profit-taking. The AI theme must now factor in the weight of upcoming public offerings

Axel Botte

Main market indicators