Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Listen to podcast (in French only)

(Listen to)Aline Goupil-Raguénès' and Zouhoure Bousbih’s podcast:

- Review of the week – Iran-US interim deal and Kevin Warsh's first FOMC;

- Theme – ECB rate hikes in response to the pass-through of the energy shock to inflation.

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: ECB rate hikes in response to the pass-through of the energy shock to inflation

- As it had largely pre-signalled at its April meeting, the ECB raised its rates by 25 basis points, for the first time since September 2023, bringing the deposit rate to 2.25%;

- Persistently high oil prices, driven by the continuation of the conflict in the Middle East, and signs of the energy shock feeding through into services prices, have led the ECB to significantly revise its inflation outlook upwards;

- At the press conference, Christine Lagarde denied that this was an insurance or precautionary rate hike, stating that the decision was justified under all three scenarios (milder, adverse, and severe);

- The prospect of a broader pass-through of the energy shock to core inflation (expected at 2.5% in 2026 and 2027) reinforces our expectation of a further 25 basis point increase in policy rates at the September 10 meeting, in order to contain inflation expectations;

- The framework agreement signed between the United States and Iran over the weekend does not alter our baseline scenario. Even assuming a full reopening of the Strait of Hormuz (which is not guaranteed), oil prices would remain above pre-conflict levels, creating a risk of second-round effects that the ECB will need to contain.

ECB rate hikes in response to the pass-through of the energy shock to inflation

As it had largely pre-signalled at its April meeting, the ECB raised its rates by 25 basis points for the first time since September 2023, bringing the deposit rate to 2.25%. Persistently high oil prices, driven by the continuation of the conflict in the Middle East, along with signs that the energy shock is feeding through into services prices, have led it to significantly revise its inflation outlook upwards. Growth prospects, however, have only been marginally revised downwards. The ECB has also updated the adverse and severe scenarios published in March and introduced a third, more favorable scenario. While the central bank reiterated that it remains data-dependent for its upcoming decisions, providing no forward guidance on the future path of rates, Christine Lagarde left the door open to further monetary tightening in order to firmly anchor inflation expectations.

Persistently high oil prices and the pass-through of the energy shock to inflation

Following the April 30 meeting, Christine Lagarde stated that a rate hike had been thoroughly discussed. The ECB ultimately opted for a pause, preferring to wait for more information—both on geopolitical developments and incoming data—to assess the magnitude and speed of the energy shock’s transmission to the economy. The ECB also wanted to incorporate updated staff projections for growth, inflation, and alternative scenarios.

This has now been done. The prolonged conflict has resulted in persistently higher oil prices than initially expected. May inflation data also showed that rising energy prices are feeding through to other components. Inflation reached 3.2% in May, its highest level since October 2023, largely reflecting the 10.9% increase in energy prices—the direct impact of the energy shock.

These figures also reveal the pass-through of this shock to other prices. This indirect impact is visible in the rise in non-energy goods prices, up 0.9% year-on-year (compared with 0.8% in April and 0.5% in March), and even more so in services prices, which increased by 3.5% (vs. 3% in April). Core inflation (excluding food and energy) thus accelerated to 2.5%, from 2.2%.

The moderation in food prices (2% after 2.4%) is unlikely to persist given the rise in fertiliser prices following the blockage of the Strait of Hormuz, through which nearly 30% of global urea trade and 20% of global ammonia and sulphate trade transit.

These preliminary figures provide limited detail on the various components of inflation. As highlighted by Christine Lagarde during the press conference, second-round effects, namely the impact of higher inflation on wages, are not yet visible at this stage. It is still too early to assess them, given the slow pace of wage negotiations.

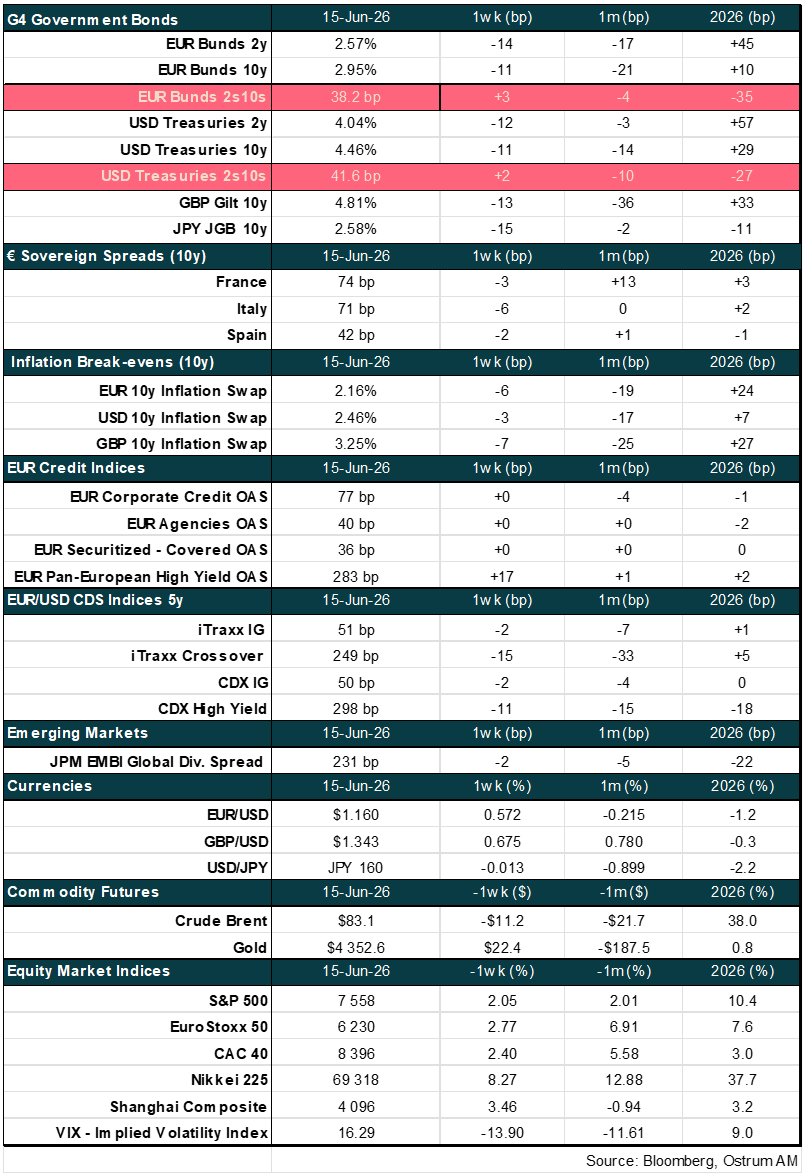

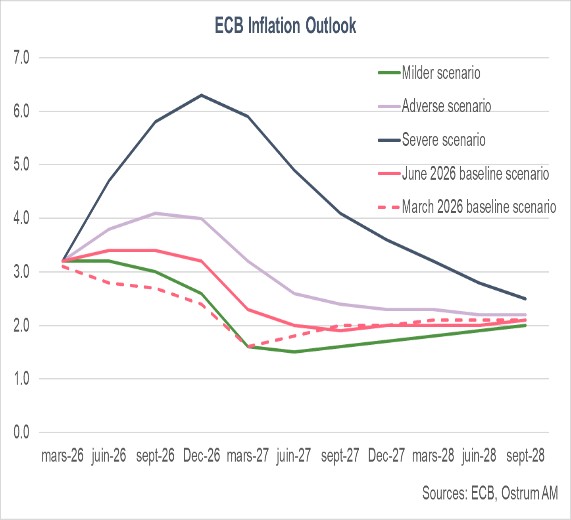

Significant upward revision of inflation outlook

Higher oil prices and signs of the pass-through of the energy shock to inflation have led the ECB to significantly revise upwards its inflation outlook for 2026 and 2027 compared with its March projections.

In the baseline scenario, Brent crude is assumed at $112 per barrel on average in Q2 2026—25% higher than in the March assumptions and 75% higher than in December. On an annual average basis, oil prices are projected at $96.9 per barrel in 2026, $82.2 in 2027, and $77.1 in 2028. Gas prices, however, have been revised down compared with March, to €45.6/MWh in 2026, €37.5 in 2027, and €27.9 in 2028.

Under this baseline, inflation is expected to average 3% in 2026 (vs. 2.6% previously) and 2.3% in 2027 (vs. 2% previously), before returning to the 2% target in 2028, more precisely from autumn 2027.

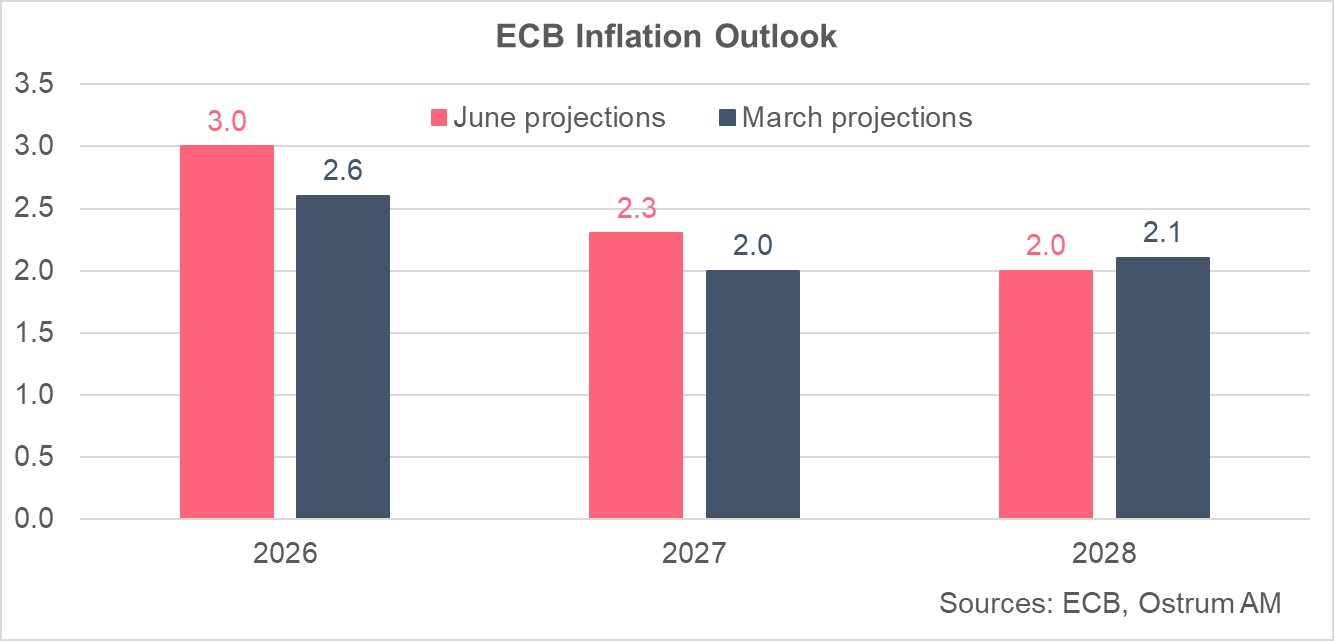

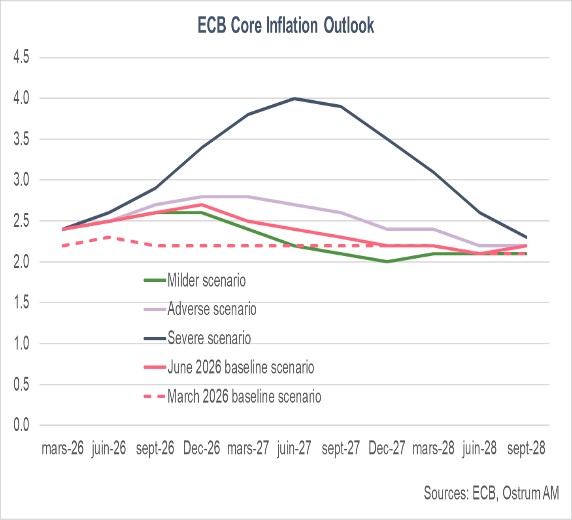

The pass-through of the energy shock to other prices is stronger than previously anticipated. Core inflation is now expected to average 2.5% in both 2026 and 2027 (vs. 2.3% and 2.2% previously) and to remain above target in 2028 (2.2%). This largely reflects stronger-than-expected direct and indirect effects relative to the March projections. Second-round effects are expected to remain contained. Compensation per employee is projected to grow by 3.2% on average over 2026–2028, down from an average of 3.9% in 2025. Wage growth moderated to 3.4% year-on-year in Q1 2026, compared with 3.6% and 3.9% in the previous two quarters. The upward revision to core inflation is mainly driven by higher prices for non-energy industrial goods.

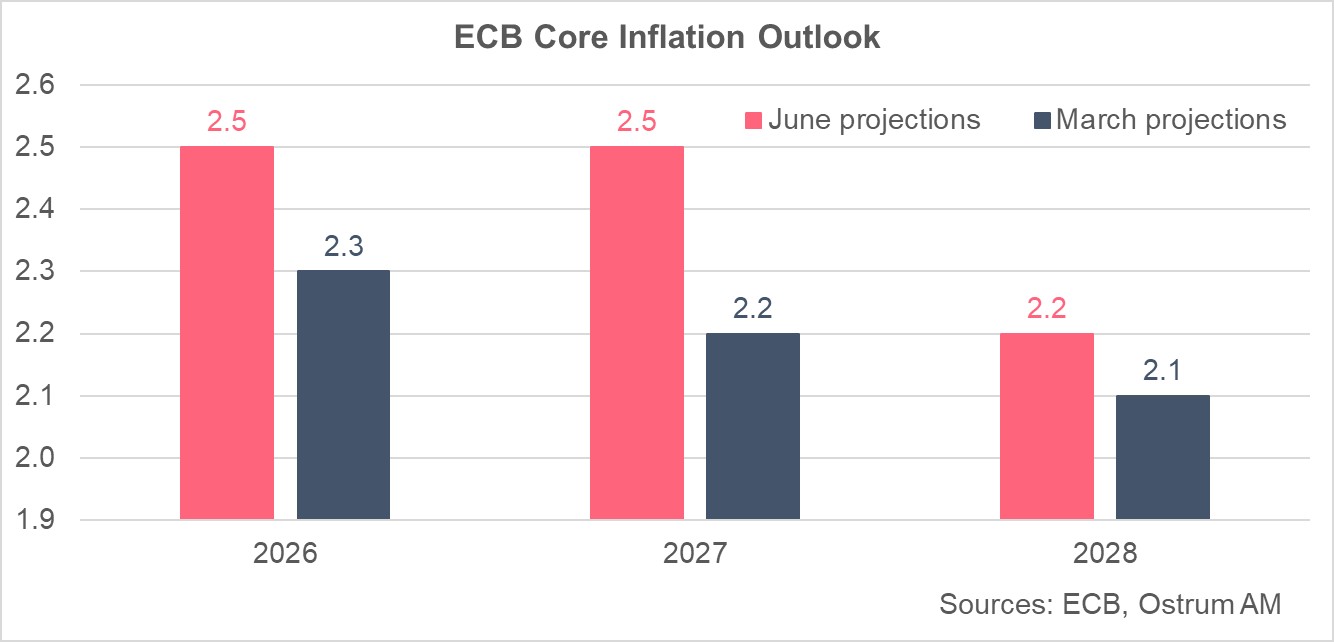

Slight downward revision of growth outlook

Growth prospects have only been marginally revised downwards: 0.8% in 2026 and 1.2% in 2027, compared with 0.9% and 1.3% in the March projections. These figures appear somewhat optimistic in light of the downward revision to Q1 GDP, now estimated at -0.2% versus +0.1% previously.

This revision, published on June 5—after the ECB staff projection cut-off date of May 27—mainly reflects a sharp downward revision in Irish GDP (-12.1% vs. -2% previously), driven by the volatility of multinational activity. By contrast, modified domestic demand, which better captures underlying domestic activity in Ireland, increased by 0.6%, exceeding expectations.

Given the high uncertainty surrounding the preliminary GDP estimate, ECB staff used a smoothed profile for Irish GDP, resulting in euro area growth of 0.2% in Q1. Applying the same quarterly growth profile for Q2, Q3, and Q4 (0.2%, 0.2%, and 0.3%, respectively), but incorporating the revised Q1 figure of -0.2%, average growth in 2026 would come out at 0.4%, below the 0.8% projected by the ECB in its baseline scenario.

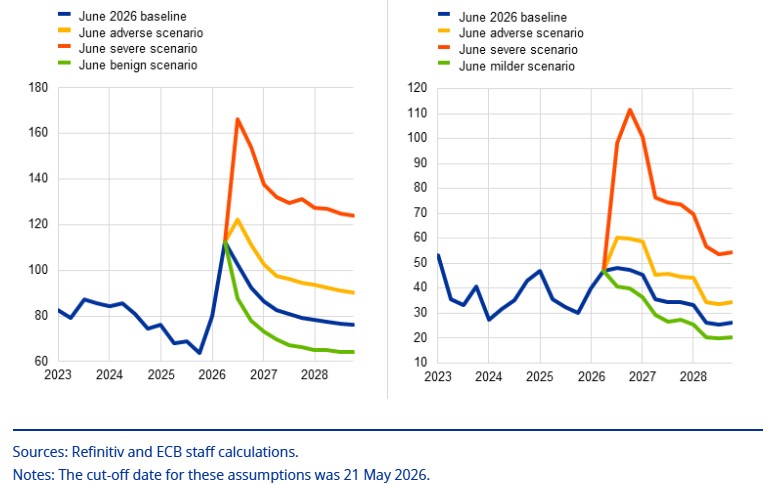

Update of alternative scenarios and publication of a milder scenario

The ECB has introduced a new scenario to capture the full range of outcomes around the baseline. The milder scenario assumes a faster decline in oil prices than currently priced in by markets, with Brent falling to $88 per barrel and gas prices dropping to €41/MWh as early as Q3 2026, remaining 15-20% below baseline levels thereafter. Oil prices would fall to $64 by Q4 2028, and gas prices to $20, reflecting expectations of a rapid resolution of the conflict and a return to pre-conflict energy price levels by end-2026.

In the adverse scenario, oil prices rise to $122 per barrel and gas prices to €60/MWh in Q3, remaining 20–30% above baseline levels over the rest of the horizon, reflecting a more prolonged conflict. Oil prices would stand at $90 and gas at $34 by Q4 2028.

In the severe scenario, oil prices increase by nearly 60% and gas prices double, reaching $166 and €98/MWh respectively in Q3 2026. The shock is persistent, with deviations from the baseline remaining elevated throughout the horizon. Oil prices would reach $124 and gas prices $55 by Q4 2028, reflecting a prolonged conflict with significant damage to oil and gas infrastructure.

ECB assumptions under the different scenarios

Oil prices (USD per barrel) and Gas prices (EUR per MWh)

The adverse and severe scenarios result in weaker growth in 2026 and 2027 compared with the baseline, alongside more persistent inflation throughout the projection horizon. The severe scenario implies a marked deterioration in the outlook due to heightened uncertainty and a sharp rise in energy prices. By contrast, in the milder scenario, growth rebounds more quickly and inflation moderates faster than in the baseline.

Conclusion

With this 25bp rate hike, decided unanimously, the ECB considers itself to be well positioned to navigate the uncertainty stemming from the conflict in the Middle East. During the press conference, Christine Lagarde dismissed the idea that this was an insurance or pre-emptive rate hike, stating that the decision was warranted under all three scenarios. She further emphasized that, had the ECB not taken this “obvious” monetary policy decision, inflation would have exceeded the medium-term target. The absence of forward guidance on the future path of monetary policy, combined with a continued data-dependent approach, signals that the ECB is in no rush to raise rates further. Instead, it is taking time to better assess potential second-round effects and the evolution of the geopolitical environment. The prospect of a stronger pass-through of the energy shock to core inflation (expected at 2.5% in both 2026 and 2027) reinforces our baseline scenario of an additional 25bp increase in key policy rates at the 10 September meeting, aimed at anchoring inflation expectations. The announcement of a framework agreement between the United States and Iran does not alter our scenario. Even assuming a full reopening of the Strait of Hormuz (which is not guaranteed), oil prices would remain above pre-conflict levels due to the damage sustained by regional energy infrastructure, the historically low level of inventories that need rebuilding, and the time required for traffic in the Strait of Hormuz to normalize.

Aline Goupil-Raguénès

Chart of the week

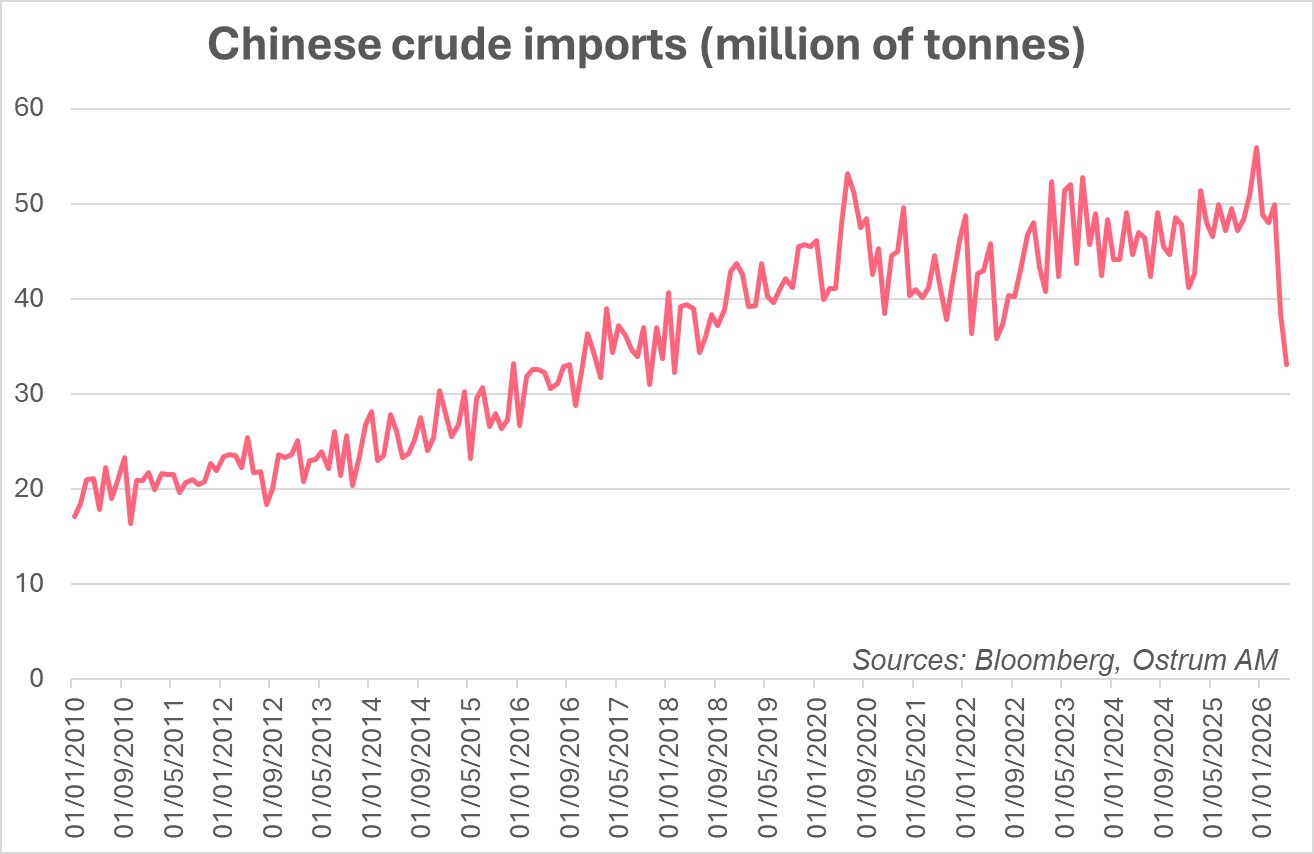

China has sharply reduced its crude oil imports to 33 million tonnes in May, equivalent to 7.8 mb/d, compared with around 11 mb/d normally. This 3 mb/d decline in imports has helped keep oil prices below $100 despite the closure of the Strait of Hormuz and has prevented a global recessionary shock. This reflects weaker domestic demand for crude, driven by the energy transition (electric vehicles, rail). Refineries are operating at reduced capacity and the petrochemical sector has cut its needs. China also built up cheap crude inventories ahead of the crisis and is now drawing on these stocks. The key point is that the Chinese economy continues to function without major disruptions.

Figure of the week

504

Governments issued a record amount of debt via syndication in the first half of the year—€504 billion—to finance the sharp increase in public spending and meet higher redemption needs. This exceeds the volumes reached in the first half of 2020, at the onset of the Covid-19 crisis.

Market review:

- U.S./Iran: Contradictory statements but optimism prevails in markets;

- ECB: 25 bps tightening as expected, inflation revised to 3% in 2026;

- Rates: T-note returns below 4.50%, Bund near 3%;

- Equities: SpaceX IPO attracts $350 billion in orders.

Space X skyrockets

SpaceX's Unprecedented IPO Disrupts Equity Markets as Contradictory Iranian Crisis Statements Drive Bond Volatility

Financial markets remain hostage to a sequence of contradictory announcements from Donald Trump, who has alternately promised strikes against Iran and then proclaimed an imminent agreement to reopen the Strait of Hormuz—for the 39th time since the conflict began. The 10-year Treasury erased its early-week rebound toward 4.57% to close nearly 10 basis points lower. The Bund returned toward 3% while SpaceX's public listing generated reallocations and volatility before a late-week recovery. The dollar sits at the upper bound of its channel since late February. The yen, meanwhile, remains close to potential BoJ intervention levels ahead of central bank meetings.

U.S. economic news was dominated by the CPI release. Consumer prices rose 4.2% in May, with core inflation at 2.9%. Unsurprisingly, energy prices explain most of the price increases. Transportation partly reflects higher fuel costs. On a monthly basis, prices rose 0.2% excluding food and energy. Generally, goods prices are declining. Real wages are therefore down 0.7% year-on-year. Unit labor costs rose modestly by 0.5% in Q1. Conversely, commodity pressures that more heavily impact production costs are reflected in the PPI, which stands at 6.5% annually. In short, inflation is not wage-driven despite the recent inflection in job creation. Kevin Warsh will offer his reading of inflation drivers during a highly anticipated first FOMC. For its part, the ECB raised rates by 25 basis points as expected. Inflation would not return to target until 2028 (peaking at 3% in 2026) while growth suffers a 0.1 percentage point downward revision in 2026 and 2027. Core inflation will dictate the extent of tightening. At this stage, another hike in September appears certain.

In financial markets, the T-note fell back below 4.50% following announcement of an agreement "to be finalized" with Iran that would enable the Hormuz reopening. This simple announcement, which resulted in crude falling below the $90 threshold, erased the rebound following Friday's employment report on June 5. The Bund followed suit to settle at 3% with relative easing in the 2-year. Inflation expectations softened in response to falling oil prices. Sovereign spreads tightened. The OAT trades around 65 basis points over Bunds while Italian BTPs tightened to 74 basis points.

Meanwhile, credit volatility remains subdued. Euro investment-grade credit spreads are inert at roughly 65 basis points—levels that prevailed before the Iranian crisis. High yield is giving back some performance after a very strong tightening move. Spread widening reached 13 basis points over the week.

In equity markets, the main event was SpaceX's Friday IPO. The operation attracted $350 billion in orders, including $100 billion in retail demand. At opening, SpaceX traded 29% above its reservation price. The record transaction generated significant volatility in U.S. and Asian indices dominated by the AI theme as investors monetized gains ahead of the subscription. Anthropic and OpenAI are expected to follow in coming months.

Axel Botte

Main market indicators