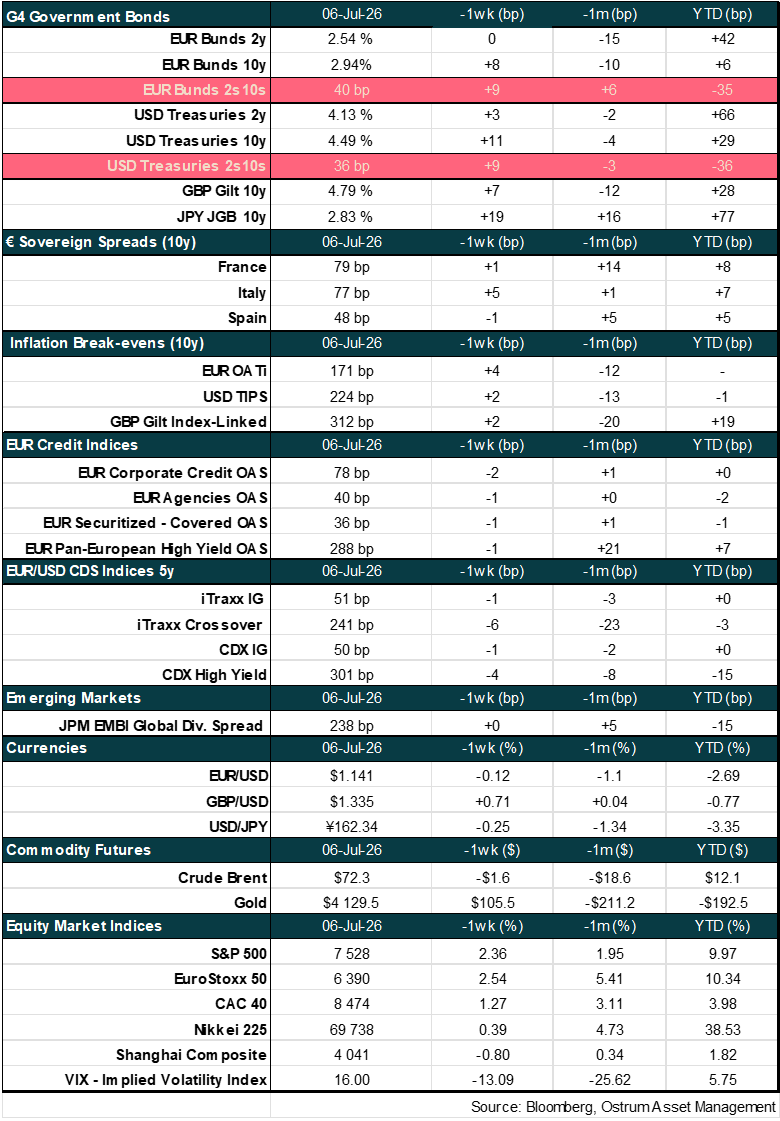

Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Listen to podcast (in French only)

(Listen to) Axel Botte’s and Aline Goupil-Raguénès’ podcast:

- Review of the week – U.S. job market remains fragile;

- Theme – Germany is embarking on an ambitious overhaul of its pension system.

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: Germany is embarking on an ambitious overhaul of its pension system.

- As in many other countries, Germany’s population ageing is set to accelerate as the baby-boom generation reaches retirement age. This demographic challenge threatens the financing of Germany’s pension system;

- The governing coalition has recently agreed to adopt an ambitious pension reform by the end of the year. The reform is based on the 33 recommendations presented by the expert commission on 23 June;

- All key parameters of the pension system would be adjusted: a gradual increase in the statutory retirement age, the abolition of early retirement without actuarial reductions, the reintroduction of a mechanism limiting pension increases when the number of retirees grows faster than the number of contributors, and a broadening of the contribution base for the mandatory pension scheme;

- ...but the most significant reform is the introduction of a public funded pension pillar to complement the mandatory pay-as-you-go system. Financed through a 2% increase in contribution rates, it would significantly raise pension levels from 2040 onwards;

- The adoption of these measures would help ensure the long-term sustainability of Germany’s pension system, deepen its capital markets (with an estimated €30–35 billion of additional investment per year), and foster a stronger equity-investment culture among households, which currently favour low-risk, low-return savings products. It would also support the EU’s Savings and Investments Union, helping to channel financing towards key investments in decarbonisation, technology and defence.

Germany is embarking on an ambitious overhaul of its pension system.

Germany, like many other countries, is experiencing a steady ageing of its population. This trend is set to accelerate over the coming years as the baby-boom generation reaches retirement age. This demographic challenge threatens the financing of Germany’s pension system, which is based primarily on a pay-as-you-go scheme. An ever-smaller workforce must finance a growing number of retirees. Without reform, higher contribution rates and lower pension benefits would be required to maintain the system’s financial viability. A government-appointed expert commission has recently delivered its conclusions and proposed 33 measures aimed at ensuring the long-term sustainability of Germany’s pension system. The members of the ruling coalition have agreed to implement these ambitious reforms by the end of the year.

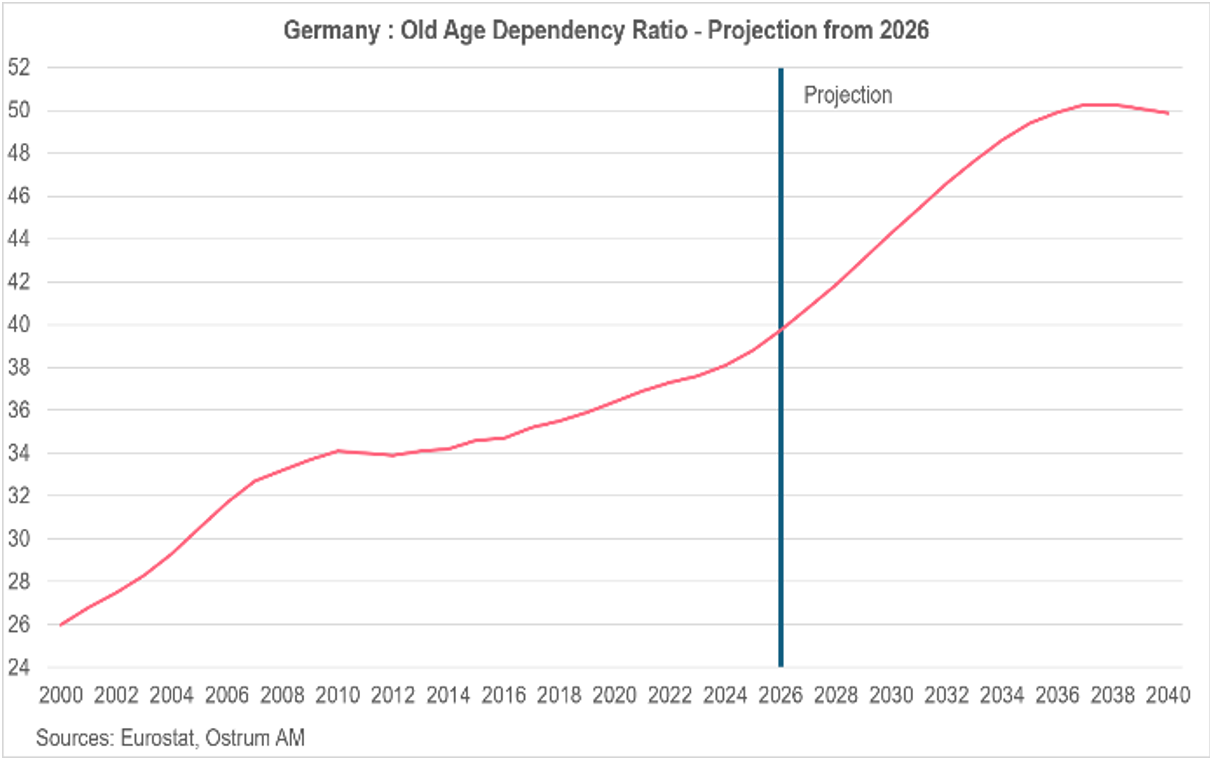

Germany faces a demographic challenge.

Germany, like many other countries, is facing the ongoing ageing of its population. This trend is the result of two key factors. First, life expectancy at birth has risen steadily, reflecting major advances in healthcare and medicine. It has increased from 67 years in 1950 to 82 years in 2025. At the same time, the fertility rate has declined markedly, falling from 2.12 children per woman in 1930 to 1.72 in 1950 and 1.32 in 2025, its lowest level since 1997. This is well below the population replacement rate of 2.1.

As a result, Germany is now one of the world's few “super-aged” societies, with more than 20% of its population aged 65 or over. According to the United Nations, it ranks sixth globally, behind Japan, Italy, Portugal, Greece and Finland. Population ageing is set to accelerate further over the coming years as the baby-boom generation reaches retirement age, a process that will continue until the mid-2030s.

By 2035, one quarter of Germany’s population will be aged over 67, which is the statutory retirement age for individuals born in 1964 or later. As a result, the old-age dependency ratio, defined as the number of people aged 65 and over per 100 working-age individuals (aged 20 to 64), is expected to nearly double compared with its 2000 level, reaching close to 50% by 2035.

… threatening the financing of the pension system.

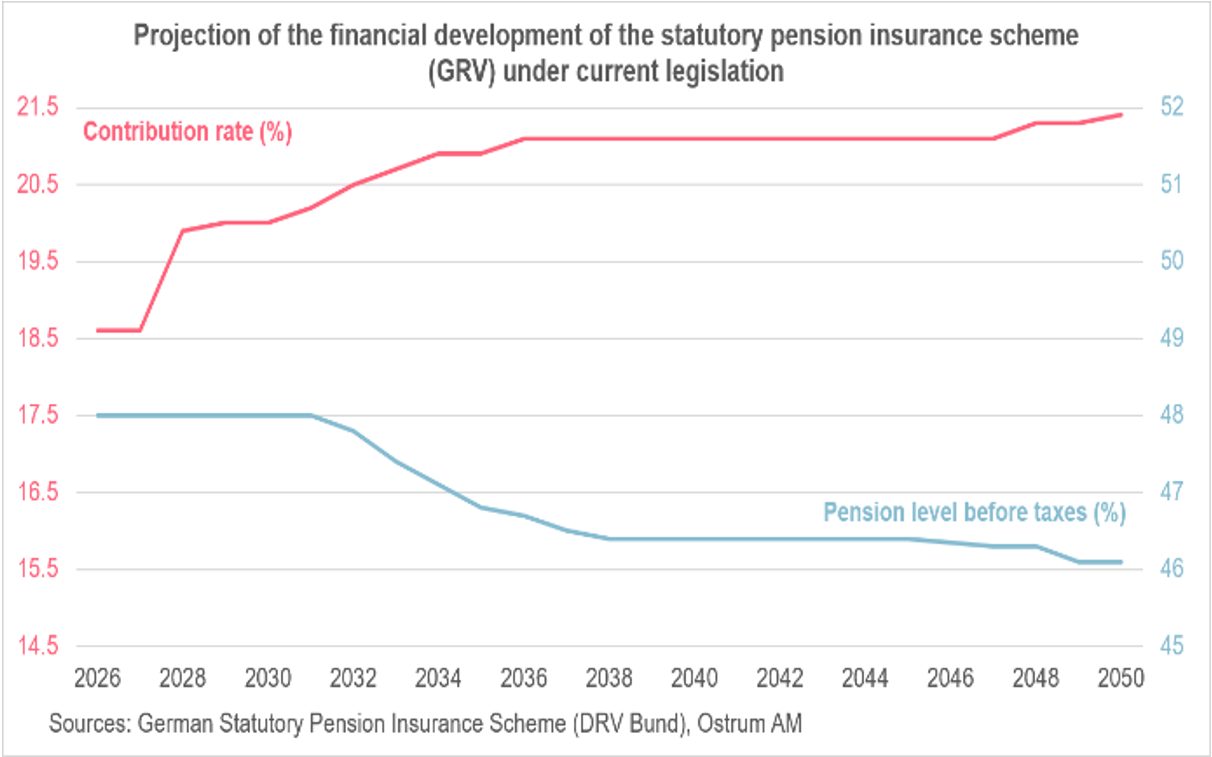

These demographic developments are threatening the financing of Germany’s pension system. The system is based primarily on a pay-as-you-go scheme, under which contributions paid by today’s workers are used to finance the pensions of current retirees. This mandatory scheme covers around 87% of the labour force. It is known as the Statutory Pension Insurance Scheme (Gesetzliche Rentenversicherung, GRV) and constitutes the first pillar of Germany’s pension system.

As outlined above, an ever-smaller workforce must support a growing number of retirees, putting increasing pressure on the pay-as-you-go system.

According to the German Pension Insurance Federation (Deutsche Rentenversicherung Bund), in the absence of reform, the contribution rate would have to rise from 18.6% of gross wages today to 20.2% in 2031, 21.1% in 2040 and 21.4% in 2050. At the same time, pension adequacy would decline, with the pension replacement rate falling from 48% today to 46.4% in 2040 and 46.1% in 2050. The replacement rate measures the median gross pension of people aged 65-74 as a share of the median gross earnings of individuals aged 50-59.

Alongside the public pay-as-you-go system, there are two complementary pension arrangements:

The second pillar of Germany’s pension system consists of occupational pensions. Employers usually contribute to their financing, and these schemes are often based on collective agreements. The third pillar is private retirement savings.

Both pillars operate on a funded basis. Contributions are invested, generate returns over time, and are subsequently paid out either as lump-sum capital or as annuities. However, they currently account for only a limited share of retirement income: the second pillar represents around 10% of total pension payments, while the third pillar contributes less than 1%.

Proposed reforms to ensure the long-term sustainability of the pension system.

Faced with the challenge that demographic ageing poses to the financing of Germany’s pension system, the government appointed an expert commission to formulate reform proposals to be implemented after 2031. The objective is to ensure adequate and reliable retirement income while avoiding an excessive and lasting burden on contributors and the federal budget.

The commission published its conclusions on 23 June and presented 33 recommendations to the governing coalition. The most important proposals are outlined below.

- Set a net replacement rate target of at least 70% after tax

The commission recommends setting a target of a net replacement rate of at least 70% of average earnings after tax. Replacement rates would be higher for lower-income individuals. This indicator would provide a clearer picture of the share of a worker’s final net income that remains available after retirement.

- Gradually increase the statutory retirement age

Current legislation provides for a gradual increase in the statutory retirement age to 67 by 2031. The commission proposes linking the retirement age to life expectancy from 2032 onwards. The additional years of life expectancy would be shared according to a 2:1 ratio between working life and retirement. In practice, each additional year of life expectancy would translate into eight extra months of work and four extra months of retirement. As a result, the statutory retirement age would rise from 67 years in 2031 to 67.5 years in 2041.

- Tighten access to early retirement

The commission recommends abolishing early retirement without actuarial reductions after 45 years of contributions. Since 2015, around 30% of new retirees have made use of this option. Evidence suggests that the scheme disproportionately benefits high-income, healthy men, while women, low-income earners and individuals with interrupted career paths benefit far less.

In addition, the minimum age for early retirement with actuarial reductions would be raised relatively quickly from 63 to 64 years.

- Reintroduce and strengthen the sustainability factor

Pension indexation currently depends on three components: gross wage growth, pension contributions, and the ratio of retirees to contributors. When the number of retirees increases faster than the number of contributors, this mechanism automatically curbs pension growth.

The sustainability factor was suspended in 2025 and is due to remain inactive until 2031. The commission recommends reactivating it from 2032 onwards and making it slightly more restrictive. Specifically, the sustainability factor would be increased from 0.25 to 0.33, leading to a stronger adjustment of pension increases in response to demographic pressures.

- Broaden the contribution base of the pay-as-you-go pension system

The commission considers the creation of a universal pension insurance scheme for all workers to be a long-term objective. It proposes extending the first pillar of the pension system, which currently covers mainly employees, to include self-employed workers who are not mandatorily insured, civil servants, members of parliament, and members of the supervisory boards of public companies.

- Expand occupational pensions

The commission also aims to significantly increase the coverage of occupational pension schemes, improve their portability, reduce costs, and boost participation among employees of small and medium-sized enterprises as well as low-income workers.

According to surveys conducted for the Federal Ministry of Labour, around 33% of individuals aged 65 and over who received a statutory pension in 2023 also benefited from an occupational pension. Among the working-age population, coverage is higher: 62% of employees aged 25 to 66 who are subject to social security contributions were covered by an occupational pension scheme in 2023. Nevertheless, coverage remains incomplete.

- Introduce a public funded pension scheme

This is the commission’s most significant proposal. It recommends introducing a funded component within the mandatory pension system, based on individual retirement savings accounts. The management of these accounts would be inspired by the Swedish model, with broadly diversified investments across global financial markets.

The funded pension scheme would be financed through an additional 2% contribution on pre-tax earnings, split equally between employees and employers. The contribution would be phased in gradually, increasing by 0.5 percentage points per year, ideally starting in 2028 and reaching 2% by 2031.

A public investment fund would be established to manage these assets, modelled for example on KENFO, Germany’s nuclear waste disposal financing fund. Individuals who do not wish to invest through the public fund would be able to choose from a limited number of certified private investment funds meeting strict regulatory criteria.

The objective is twofold: to raise pension levels sustainably over the long term and to reduce the pension system’s dependence on Germany’s demographic outlook.

The reform would generate €30-35 billion of additional annual investments, channelled into a public fund inspired by the Swedish model. The Bundesbank has expressed interest in managing this fund.

Expected impact of the proposed reforms

The commission has conducted a series of simulations. According to its estimates, implementing the full package of measures would lead to higher contribution rates in the short term, reflecting the need to finance the new mandatory funded pension scheme. However, the increase would be more moderate than under a no-reform scenario.

Pension levels would stabilise over the medium term, rather than decline as projected in the absence of reform, and would then rise significantly from the 2040s onwards. The proposed measures would also help moderately relieve pressure on the federal budget from the mid-2030s onwards.

Conclusion

The governing coalition is preparing draft legislation this summer, which will serve as the basis for parliamentary debates in the autumn, with the aim of securing final approval by the end of 2026.The reform package represents a far-reaching overhaul of Germany’s pension system. It includes a gradual increase in the statutory retirement age, the abolition of early retirement without actuarial reductions, the reintroduction of a sustainability factor that limits pension growth when the number of retirees rises faster than the number of contributors, the broadening of the contribution base, and the introduction of a funded component within the mandatory pension system, managed by a public investment fund modelled on the Swedish system. According to the commission’s simulations, the full implementation of these reforms would result in a more moderate increase in contribution rates than under a no-reform scenario, while leading to a significant rise in pension benefits from the 2040s onwards. The creation of a publicly managed funded pension scheme would also help deepen Germany’s capital markets, generating an estimated €30–35 billion of additional investment per year, while fostering a stronger equity-investment culture among households. At present, household savings remain heavily concentrated in low-risk, low-return financial products. More broadly, the reform could contribute to the development of European capital markets and support the EU’s Savings and Investments Union, helping to mobilise funding for key strategic investments, notably in decarbonisation, technology and defence.

Aline Goupil-Raguénès

Chart of the week

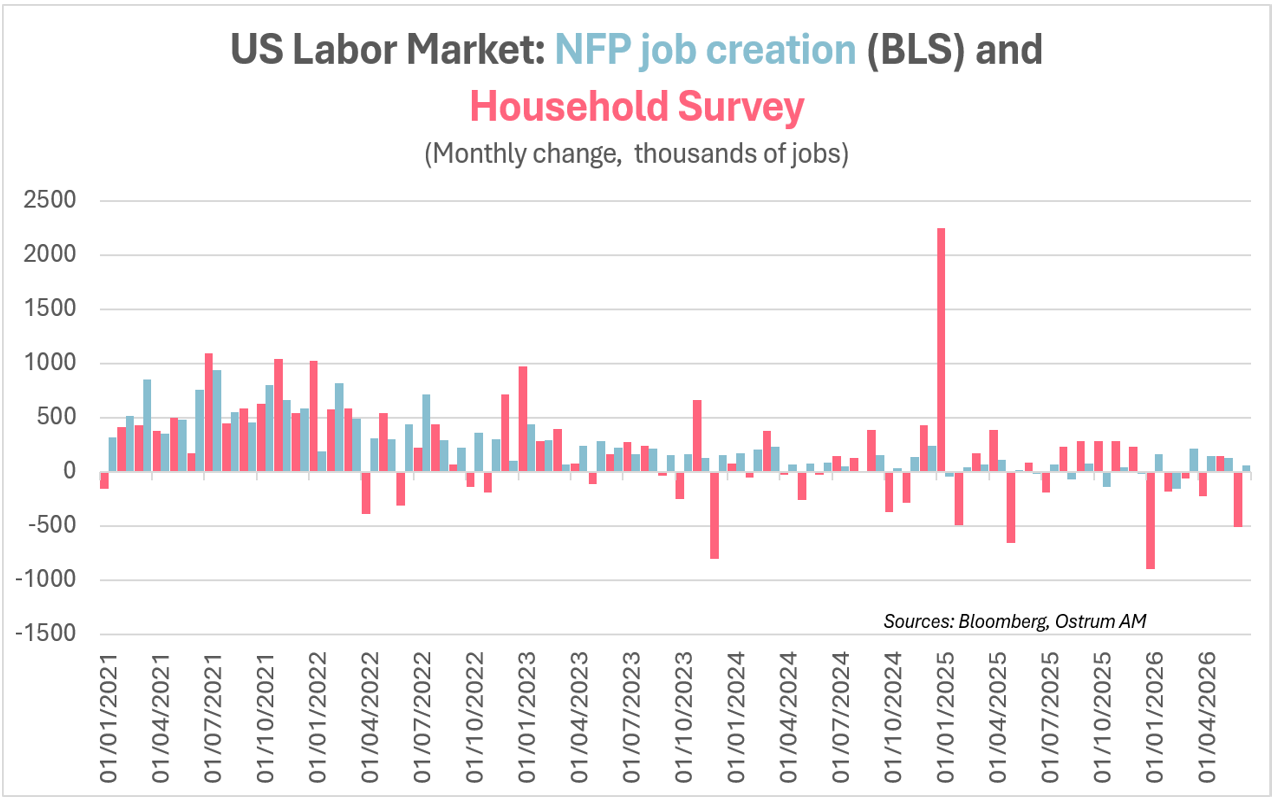

US labor market slowdown. In June, job creation totaled 57,000, according to the Bureau of Labor Statistics, following a downward revision of 74,000 jobs for the previous two months. However, the Household Survey pointed to a decline of 507,000 jobs. Annual benchmark revisions could once again reveal an overestimation of nonfarm payrolls (NFPs), similar to the findings of the Quarterly Census of Employment and Wages (QCEW), which suggested an excess of 900,000 jobs at end-2024.

The unemployment rate declined to 4.2%, largely due to a fall in the labor force participation rate to 61.5%, its lowest level in five years.

Figure of the week

250

This year, the United States marks the 250th anniversary of its Declaration of Independence from the British Empire.

Market review: U.S. Job Market Remains Fragile

- Oil : Crude prices continue their normalization process;

- United States: Job creation slowdown in june, participation rate decline;

- Bonds: Yield curve steeping, heavy presure on JGBs;

- Spreads: Portfolio lightening at half year-end.

U.S. Job Market Remains Fragile

Disappointing U.S. jobs data for June and falling crude prices are reducing expectations for monetary tightening. Meanwhile, yield curves are steepening driven by JGB movements. The dollar is partially reversing its post-FOMC rally as Japanese authorities signal potential yen intervention risks.

The week proved eventful with the ECB's Sintra symposium, major economic releases, and trading concentrated into four days due to the Independence Day holiday weekend in the United States. Oil price easing continues despite a fragile truce and lack of significant negotiating progress. Europe, however, appears resigned to the prospect that transit fees through Hormuz imposed by Iran and Oman have become inevitable.

On the economic front, U.S. employment statistics cast a chill over markets just as consensus had anticipated a spring improvement. The paltry 57,000 job creations were insignificant, particularly given revisions that wiped out nearly 100,000 positions from the previous two months. The narrow sectoral diffusion of hiring also remains incompatible with a typical growth cycle. Moreover, the unemployment rate's decline to 4.2% masks another deterioration in the participation rate (-0.3 percentage points to 61.5% in June). Labour market conditions remain highly uncertain amid accumulating AI-related layoffs and demographic shifts that are reducing the working-age population.

In the eurozone, inflation fell to 2.8% in June thanks to a 7% drop in gasoline prices and an unexpected deceleration in food costs. However, services inflation (+3.2%), which has remained above 3% since 2022, continues to cloud the return to the inflation target. Wage demands are unlikely to moderate given unemployment remains stable at historic lows (6.2%).

In financial markets, half-year-end flows likely reflected profit-taking following the bond yield rally. This resulted in curve steepening, further fuelled by continued oil price declines. With crude approaching $70, short-term inflation expectations and policy rate anticipations are under pressure, reinforcing curve steepening dynamics. The T-note trades near 4.50% while the Bund has moved back above 2.90%. The most dramatic rate movement, however, came from Japan, where the 30-year yield settled above 4%. The BoJ is threatening to change its intervention strategy given yen weakness (160 against the dollar).

Eurozone government bonds faced slight spread-widening pressure, likely reflecting quarter-end balance sheet adjustments. OATs and BTPs experienced selling pressure. Credit markets ended June on a somewhat less positive note, though without genuine distress signals. Euro IG trades at 67.5 basis points and synthetic indices remain well-supported. Equity markets showed greater volatility amid growing disagreements over semiconductor company valuations in both Asia and the United States. Nevertheless, the week proved positive for major indices.

Axel Botte

Main market indicators