Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Summary

Listen to podcast (in French only)

(Listen to) Axel Botte’s podcast:

- Review of the week – Yields ease with falling crude, US growth, European economic outlook;

- Theme – The Warsh Fed: the reform agenda.

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: The Warsh Fed: the reform agenda

- Kevin Warsh's arrival at the Fed marks the end of the transparency era initiated by Ben Bernanke. He advocates a return to discretion and policy flexibility, inspired by Alan Greenspan, while firmly opposing forward guidance.

- Believing the Fed’s economic forecasts are unreliable, Warsh refused to submit his own projections for the June 2026 dot plot. This move significantly reduces the informational value of the chart and frees policymakers from past rhetorical commitments.

- Warsh argues that the AI investment boom will generate immense disinflationary productivity gains, believing that the Fed should not hinder this technological expansion cycle with excessive monetary tightening.

- To guide monetary policy, the new Chair favors alternative, less volatile metrics, such as the Dallas Fed's trimmed-mean inflation indicator or real-time private sector datasets (such as Truflation).

- Faced with colossal public debt and $8.5 trillion in maturing securities in H2 2026, discussions could emerge to update the landmark 1951 Accord, aiming to coordinate balance sheet policies and quickly ease the federal government's interest burden.

The Warsh Fed: the Reform Agenda

Kevin Warsh will bring change to the Federal Reserve. The new Chair has already undertaken some changes in terms of communication, whilst refusing to contribute forecasts for rates, growth and inflation. Task forces have been put in place to reform the Fed’s operational framework. In this piece, we discuss the possible outcome from these working groups.

Background and Appointment Context

Warsh comes in with strong opinions on the Fed’s modus operandi

Kevin Warsh's appointment as Federal Reserve Chair in May 2026, succeeding Jerome Powell under President Trump's administration could bring about major changes in the modus operandi of the US central bank. Since the end of Alan Greenspan’s Chairmanship, the Vice President has always been appointed as the Fed’s next Chair (Greenspan to Bernanke to Yellen to Powell). Warsh, a former Fed governor under President Bush is a highly politicized figure. His appointment may signal a fundamental shift away from the transparent communication approach introduced by Ben Bernanke that has characterized Federal Reserve operations since the 2008 financial crisis.

The transition occurs amid challenging economic conditions, particularly with the Iran war creating an energy price shock.

At his first press conference, Kevin Warsh announced a task force in each of five areas: First, Fed communications; second, the Fed’s balance sheet policy; third, the use and reliance on existing data sources; fourth, productivity and jobs in an era of transformation; and last, the Fed’s inflation frameworks. We dig into data use and communication.

Monetary Policy Communication

Communication is often as important as changing policy rates for central bank. Kevin Warsh's communication tactics will likely emphasize discretion over transparency, allowing maximum flexibility about future decisions on interest rates. In a way, Warsh’s communication may mimic Greenspan’s hard-to-interpret messages along the lines of his famous answer in a Senate committee hearing in 1987: “If I seem unduly clear to you, you must have misunderstood what I said”.

• Forward Guidance

Kevin Warsh's press conference provided clear indication of his reform intentions, including explicit opposition to forward guidance. Forward guidance emerged as a critical monetary policy tool during the zero-rate era following the 2008 financial crisis. Forward guidance on interest rates was meant to influence longer-term borrowing costs by providing explicit signals about future policy intentions. Such communication arguably helped to anchor expectations and stabilize markets during uncertainty periods.

Kevin Warsh fundamentally opposes this framework. During his Senate confirmation, he had stated unequivocally: "Unlike many of my colleagues past and present, I don't believe in forward guidance. I don't believe that I should be previewing for you what a future decision might be." His opposition stems from beliefs that such guidance constrains policy flexibility and creates unrealistic market expectations, potentially solving fewer problems than it creates.

Somewhat ironically, the concerns about the easing bias language in the May FOMC communiqué expressed by Christopher Waller, Lisa Cook, Beth Hammack, Lorie Logan, and Neel Kashkari bring support for Warsh's approach. The June communiqué was indeed much lighter and removed the forward guidance language.

• The Dot Plot Controversy

The quarterly "dot plot" exercise, introduced by former Fed Chair Ben Bernanke in 2012, requires 19 FOMC members to submit anonymous interest rate projections for one, two, and three years ahead, plus longer-term neutral rate assessments. This practice has become a market-moving event, with Wall Street analysts scrutinizing every quarterly release for policy trajectory signals.

Kevin Warsh is skeptical about the Fed's ability to accurately predict economic conditions. Its credibility is not enhanced by providing poor forecasts. This is the reason why Kevin Warsh refused to submit his forecasts so that the June 2026 dot plot only has 18 contributions. With the Chair’s outlook missing, its informational content of the dot plot has fallen considerably.

In any case, the dot plot creates perverse incentives, making officials "prisoners of their own words" and leading to policy errors when they struggle to reconcile changing conditions with previously stated expectations. Former Fed officials report that many FOMC members have grown to "despise" the exercise, finding it constraining and potentially misleading. Former Fed official Daniel Tarullo, for instance, was very critical of the summary of economic projections. Inflation forecasts were systematically made in line with the 2% target two years out, in what resembled a reverse engineering exercise rather than actual forecasting. Instead of reviewing forecasts penciled in by policymakers, it would be perhaps more interesting to unveil the Fed staff’s forecasts that are presented to the FOMC participants.

Of course, removing a policy tool like the ‘dot plot’ designed to anchor rate expectations could initially spark volatility in bond markets, but the inertia created by the Fed rate guidance during the ‘not-so-transitory’ inflation spurt led to belated policy tightening and elevated interest rate volatility.

• Forecasts risk being over-interpreted

Furthermore, unintended precision may increase volatility by encouraging markets to over-interpret decimal-point projection changes. Anonymous forecasts also mean that markets may put too much weight on projections by non-voting members. As a matter of fact, former Chairman Jerome Powell repeatedly argued during post-meeting press conferences that the median Fed rate projection is not to be confused with the committee’s decision.

The concept of Price Stability, and the Inflation Measures

Price stability needs not referring to a numerical target

Price stability is an elusive concept. Under Chairmen Alan Greenspan and Paul Volcker, it was never a precise number of a clearly defined inflation gauge, like the current 2% PCE deflator target. For both these Fed Presidents, price stability is achieved when expectations of price changes have no discernible impact on activity. As for reference measures, Greenspan subsequently used the GNP deflator, then the CPI before judging that the PCE was a superior measure, especially its core component (excluding volatile items like energy and food). In other words, there was never a definitive single inflation reference. Later, Ben Bernanke opted for headline PCE in early 2012 (arguably because significant favorable base effects were expected in the remainder of that year at a time when the Fed had no intention to tighten policy as the U.S. economy was still healing from the Great Financial Crisis). Jerome Powell tried to articulate a flexible average inflation framework likely designed to avoid having to raise rates and obviously dropped it once inflation took off in the aftermath of Covid. In sum, price stability was not always synonymous with 2% inflation.

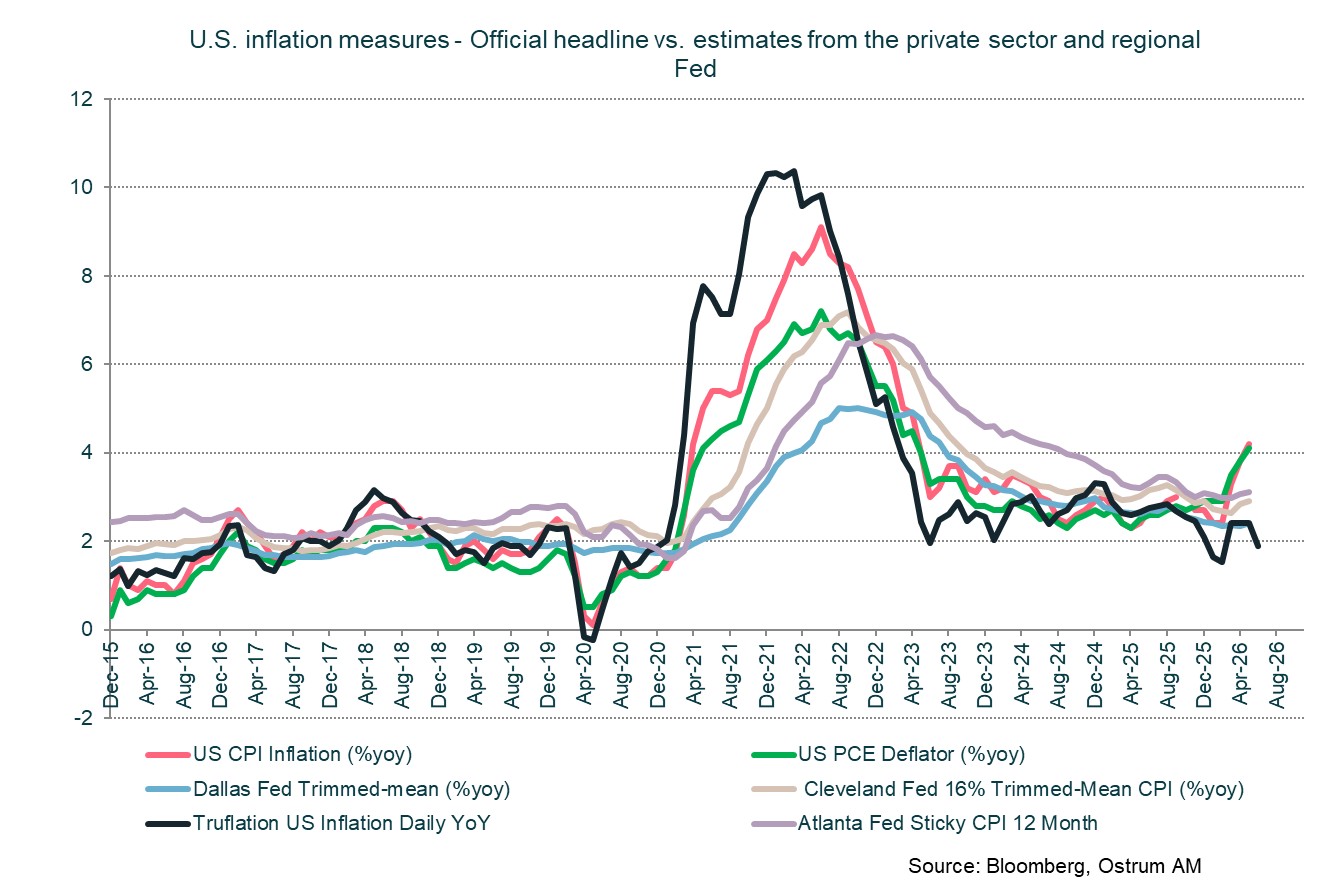

Warsh's approach to inflation communication will likely emphasize the longer-term outlook for prices. He repeatedly argued that the AI investment boom will reshape the inflation outlook as productivity gains will yield ‘massive’ disinflationary pressures. In his view, the Fed should not stand in the way of an AI-led growth cycle.

The inflation reference index is arbitrary but very important for market participants

The Fed has a dual mandate of price stability and maximum employment (the forgotten third policy objective of moderate long-term rates is no longer front and center in policy making). The ongoing Iran war significantly complicates inflation management. Energy price volatility from the conflict creates challenging conditions for monetary policy decisions, with a majority of FOMC members expressing concerns about inflationary pressures. Monetary policy is ill-equipped to deal with supply shocks. The prevailing view is that central banks should not respond to an oil price shock, although the U.S. has become a net energy exporter over the past decade thanks to the shale oil boom.

Kevin Warsh has already suggested that he preferred the use of trimmed-mean inflation measures. The Dallas Fed trimmed-mean measure was 2.41 % in May, much lower than the 4%+ readings on both the headline CPI and PCE deflator. The Dallas Fed estimate knocks out the 31% highest-inflation items and the 26% lowest-inflation items in the PCE basket. In the Dallas Fed study, the asymmetrical trimming of the PCE index yielded better inflation forecasts two years out than spot headline and core PCE inflation. However, in the context of a sharp energy price shock, the use of an asymmetrical gauge may prove ill-guided according to the Dallas Fed.

The choice of an inflation measure has sometimes been politically motivated. In the early 1970s, Arthur Burns promoted the use of core inflation - CPI excluding energy and food - at a time when the Fed failed to recognize that a wage-price spiral was developing. The choice of the Dallas Fed trimmed-mean index as the inflation reference for the Fed would be a strong political signal. The Cleveland Fed economists calculate median and other trimmed-mean indices. In turn, the Atlanta Fed produces sticky price inflation as opposed to flexible price inflation, to gauge whether inflation is likely to divert from target.

The Fed will also look to incorporate more private sector estimates into its decision-making process. Truflation produces daily inflation indices using extensive datasets instead of monthly survey-based methods (deemed ‘old-fashioned’ by Warsh) providing alternatives to government-reported metrics. Truflation provides their own estimate and alternative price indices using methodologies in line with that of the CPI or the PCE deflator. All Truflation numbers are currently way below official data.

Bank Regulation and Treasury Market Dynamics

A smaller Fed balance sheet means that banks will need to hold more Treasuries

Michelle Bowman, the Fed governor overseeing bank supervision, has led the effort to loosen post-2008 bank regulations. Changes to the Standard Leverage Ratio, bank stress tests, and Basel III endgame implementation aim to free up bank balance sheets for increased Treasury purchases.

While reducing required reserves could increase banks' Treasury holdings willingness, these efforts cannot restore the pre-2008 regime where banks were primary Treasury market intermediaries. The Treasury market has grown fivefold since the financial crisis, requiring different intermediation approaches. Benefits of increased intermediary capacity must be weighed against losing capital requirements that have substantially improved bank safety.

After the GFC, the pendulum of bank regulation has swung too far in restrictive territory. The Warsh Fed will ease the regulatory charge.

In essence, it is possible that increased bank capital requirements to intermediate Treasury markets since the Great Financial Crisis has had unintended consequences in terms of market stability and liquidity. Hedge funds and other arbitrageurs (much less regulated than banks) indeed now play a key role as liquidity providers in cash, repo and derivative markets. These changes could fundamentally alter the Fed's financial market role and broader economic influence.

The proposed reforms raise questions about central bank independence and democratic accountability. While reducing forward guidance might increase policy flexibility, it could also make Fed decisions less understandable and evaluable for markets and the public. This represents a fundamental tension in modern central banking between flexibility and transparency.

A revisited Treasury-Fed Accord?

Warsh referred to the 1951 Treasury-Fed Accord, it is unclear how this could be updated to a new form of cooperation

The 1951 Treasury-Fed Accord may also require 21st-century updates. Practical implications remain unclear. The following is an excerpt from the Brookings Institution paper : ”Between 1942 and 1951, the Federal Reserve ceded its authority to set interest rates to the U.S. Treasury, pegging the yield on long-term Treasuries at 2.5% to help finance World War II. President Harry Truman tried to persuade the Fed to maintain that policy during the duration of the Korean War, but with inflation running above 8% year over year, the Fed resisted. The result was a March 1951 pact between the Treasury and Fed that is widely viewed as freeing the Fed to set interest rates to achieve its congressional mandate without considering the impact on the cost of Treasury borrowing. The Accord was an agreement on how The Treasury and the Fed would act in the immediately forthcoming years as the Federal Reserve transitioned to the establishment of an active, macroeconomically-oriented monetary policy… Essentially, the transitional arrangements entailed Federal Reserve agreements not to raise short-term interest rates, and to continue management of longer-term interest rates, during the initial years after the Accord”.

In the 4th quarter of 2025, the end of quantitative tightening helped keep coupon issuance steady, whilst rate cuts and reserve management purchases ($290 billion bill purchases from December to April) pushed short-term rates lower. Over the past year and a half, the refinancing strategy of the U.S. Treasury has been considerably tilted towards T-bill issuance. The interest charge on government debt of more than $1 trillion annually eats up 18% of federal revenue. A total of $8.5 trillion US bonds and bills will mature in the second half of 2026. Should the Fed strike a deal with the U.S. Treasury, the interest charge burden could ease rapidly.

Conclusion

Kevin Warsh is undoubtedly a politicized figure, who will profoundly reform the Fed. He will bring considerable change in the conduct of Fed policy from the communication strategy to the balance sheet policy. The interpretation of the price stability mandate will be extremely important to shape rate expectations in the context of an AI-led transformation of the U.S. economy. His communication style will likely echo that of the late Alan Greenspan, whilst the inflation approach will be expanded to include modern measures of price pressures.

Axel Botte

Chart of the week

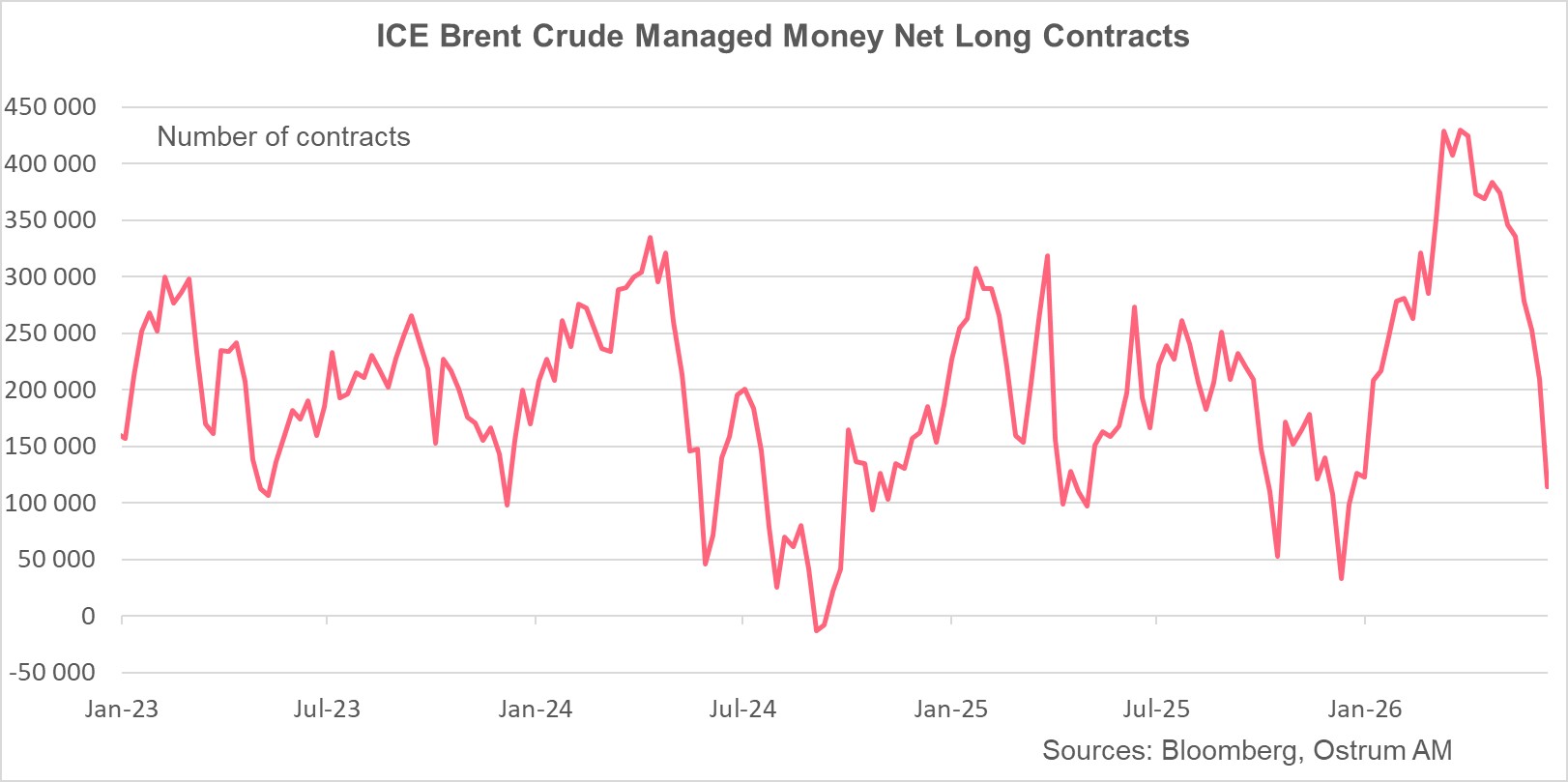

The agreement between the United States and Iran has triggered a sharp drop in oil prices, with Brent crude now trading around $75. However, inventories remain tight, which could cause the price decline to lose momentum in the coming weeks.

Speculative positions on Brent crude futures contracts were rapidly divided by four, returning to their January 2026 levels.

Figure of the week

60

$60k : Bitcoin prices dipped below the $60,000 level for the first time in two years. The cryptocurrency has lost 52% since the peak in October 2025.

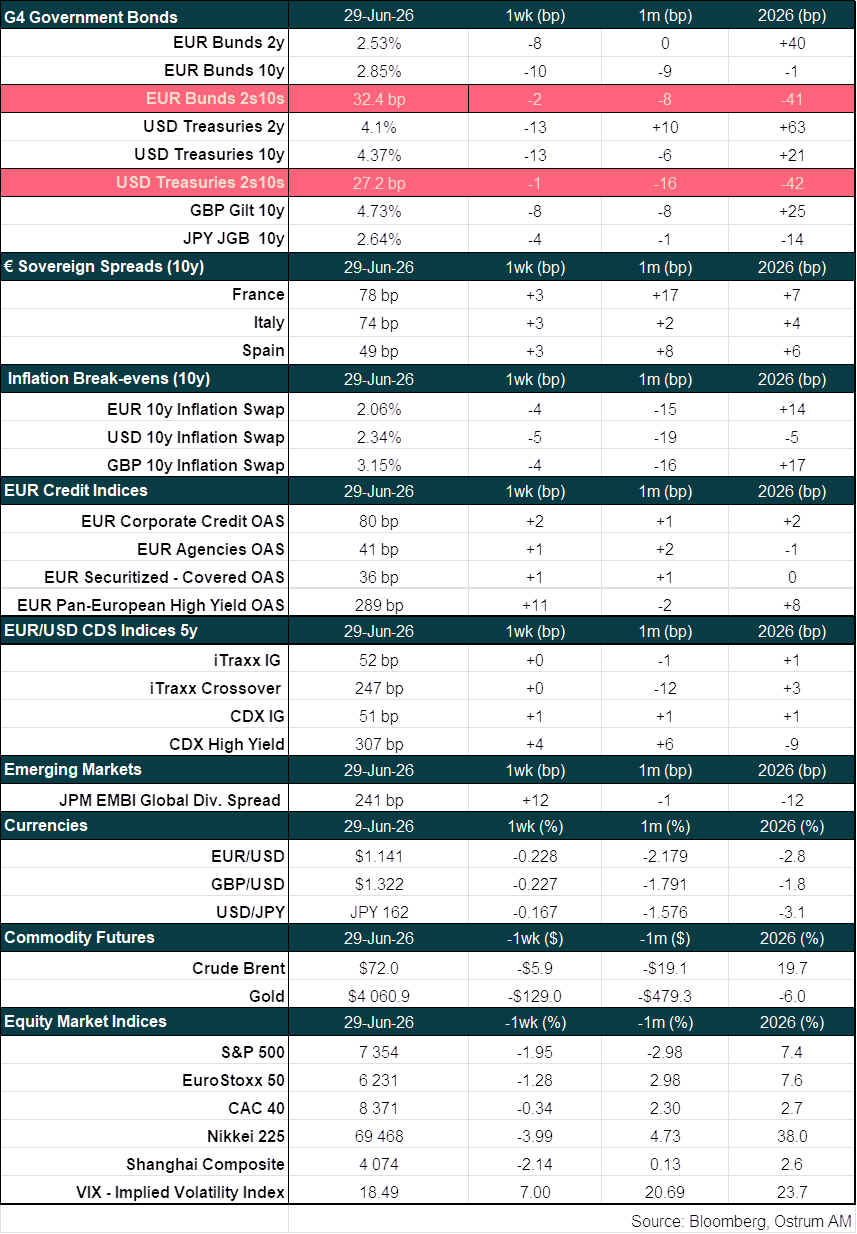

Market review: Crude’s Slide Gathers Momentum

- Oil : Brent prices closing in on pre-war price levels;

- U.S. economy : GDP growth revised up to 2.1% in Q1, despite consumer weakness;

- Bonds : Bund yields hit 3-month low at 2.85 %;

- Credit: spreads remain stable with iTraxx Crossover below 250 bps.

Crude’s Slide Gathers Momentum

The yield rally has continued to unwind in tandem with falling oil prices. Rich equity valuations are generating market volatility, but corporate credit remains largely insulated.

Financial markets have digested the hawkish undertones of the first FOMC meeting chaired by Kevin Warsh. Sovereign yields have eased, with the German Bund dipping back below 3%, particularly as the slide in crude—now almost back to pre-crisis levels—dragged down short-term inflation expectations. Equity volatility rose, driven by renewed scrutiny over the valuations of AI-exposed companies and speculation that OpenAI’s public debut may be postponed. Yield curves have partially reversed the sharp flattening that followed the recent round of central bank meetings. Conversely, credit spreads continue to absorb equity-driven volatility shocks with remarkable ease.

First-quarter US GDP growth was revised up by 0.5 percentage points to 2.1%. However, this upward revision stems primarily from a sharp drop in imports triggered by a slowdown in personal consumption, which grew at a meager 0.5% rate between January and March, weighed down by weak services spending. Consumers are increasingly relying on credit to offset insufficient real income growth. While a minor recovery has emerged over April and May—supported by tax refunds and lower gasoline prices—private consumption's overall economic contribution remains modest. The housing sector continues to contract, with new home sales lingering near the cyclical lows of 2022. Consequently, the US economy remains heavily reliant on the AI investment cycle. Tech hardware, software, and R&D continue to log double-digit growth, a dependency that explains why Donald Trump’s latest tariff salvos have spared the tech sector. Nevertheless, the trade deficit widened further to $105 billion in May, highlighting underlying structural imbalances that could trigger fragility in the months ahead. In the eurozone, the latest survey data points to a stabilization in economic activity following the agreement to reopen the Strait of Hormuz, with the retreat in crude acting as a clear tailwind.

Fixed-income pressures are relenting as crude prices slide. With Brent crude falling back below $75, two-year inflation swaps have retreated. The 10-year Treasury yield drifted toward 4.40%, as a modest steepening of the curve only partially offset the flattening impulse of the June FOMC. The Bund has also benefited from equity volatility and dialing-back of expectations for ECB tightening beyond a well-flagged second hike in September. The ECB remains highly vigilant, particularly over the risk of second-round effects in upcoming wage rounds, leaving the Bund to trade around 2.85% at the end of the week. Eurozone sovereign spreads widened marginally, lagging the rally in Bunds. Italian BTP spreads (at 74 basis points) reacted briefly to speculation of early elections next April.

Credit markets remain remarkably stable despite typical end-of-quarter positioning risks. Euro investment-grade spreads are unperturbed at roughly 65 basis points over swaps, while the iTraxx Crossover remains anchored below the 250 basis point threshold, despite the resurgence in equity volatility driven by stretched valuations in US and Asian tech names.

Axel Botte

Main market indicators