Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum’s views on the economy, strategy and markets.

The CIO Letter

2024: In Fed we trust!

The growth gap between the United States and Europe is expected to persist in 2024. The US economy will nevertheless be subject to political uncertainty with the presidential elections next autumn, but the good financial health of households and businesses will enable growth of around 2%. Disinflation and the recent easing in financial conditions also reduce the risk of recession. In the euro area, the economy is slowly emerging from a phase of stagnation, paradoxically without a negative impact on employment. The pickup in household consumption will generate a modest recovery limited to 0.5%. In China, the government’s economic priority is once again industrial production after the disappointing rebound in consumption. Structural brakes on growth are causing a long-lasting slowdown.

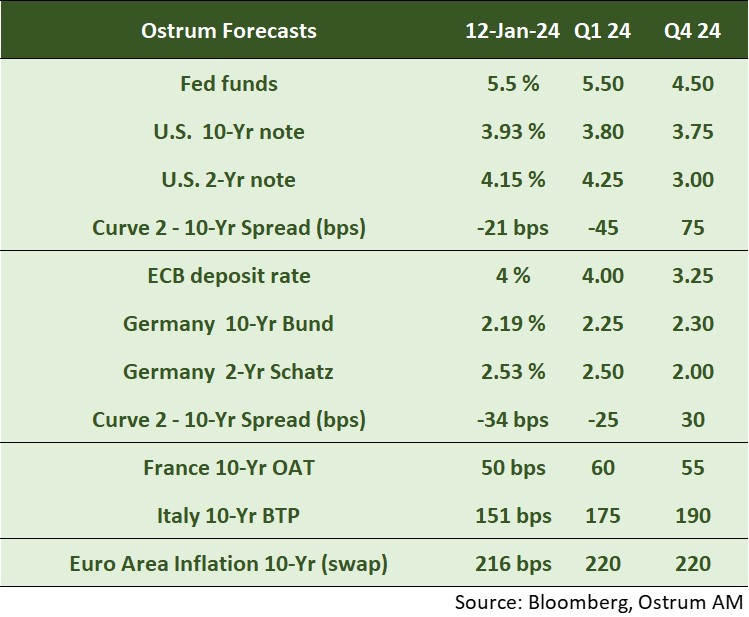

Amid disinflation, the Fed will cut rates 4 times in 2024. The ECB will follow with 3 rate reductions of 25 bp. Cutting rates whilst conducting quantitative tightening will be difficult to achieve. If financial difficulties arise, the Fed will quickly abandon QT. The pressure would then be intense on the ECB to do the same. As for Japan, the exit from negative rates remains hypothetical.

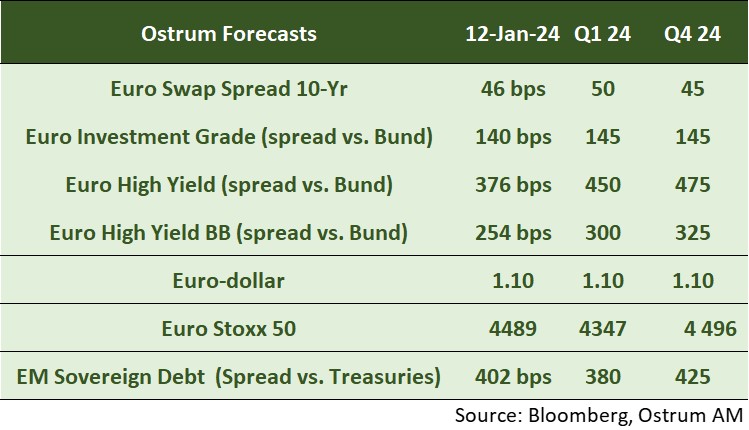

US bond yields are expected to remain capped by the Fed's dovish rhetoric. In the Eurozone, the issuance calendar constitutes an upward risk for sovereign spreads after the sharp tightening in the fall. Credit appears best positioned for 2024 given low spread volatility. High yield valuations have richened, which is already reducing potential performance in 2024 despite the low level of defaults. European stocks lack a catalyst capable of reviving international flows. The slow decline in margins will nevertheless be offset by the increase in multiples.

Economic Views

Three themes for the markets

-

Monetary policy

The Fed will likely cut rates several times in 2024 in line with the latest FOMC projections. Central bankers nevertheless disagree with the trajectory of Fed rates penciled in by market participants. In the euro area, the ECB must deal with the dovish environment created by the Fed and market pressure. The inertia of inflation projected for the first quarter nevertheless calls for caution. The BoE is in a similar situation despite progress on the inflation front.

-

Inflation

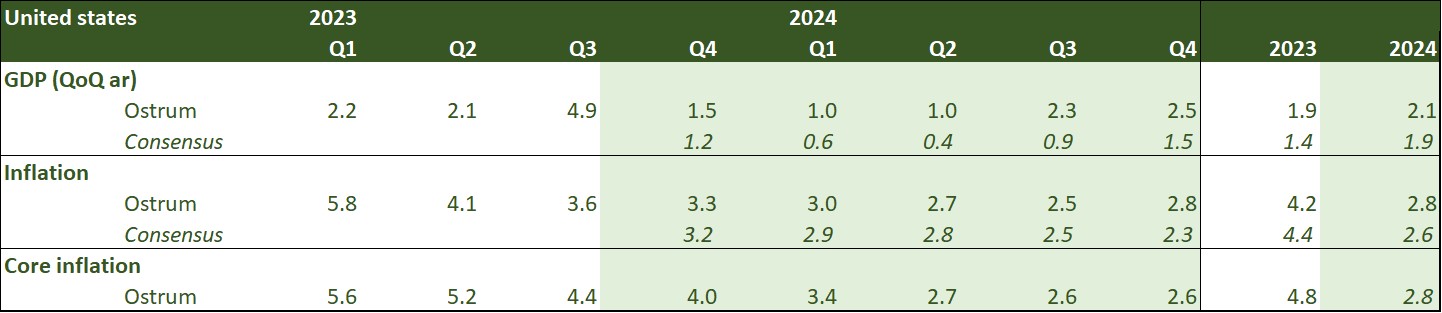

US inflation rose to 3.4% in December. Goods’ inflation has declined, but the prices of services, notably housing, remain too high for a sustainable return of inflation to 2%. In the euro area, inflation rebounded mechanically to 2.9% in December. The fall in energy prices is moderating. Public transfers to limit the cost of living will be reduced gradually. Core inflation remains elevated at 3.4%. In China, industrial overcapacity and falling food prices are maintaining disinflationary pressures.

-

Growth

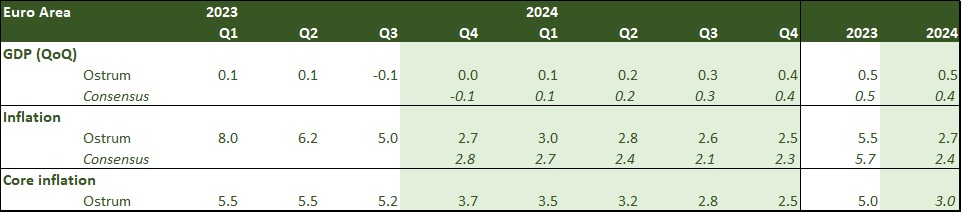

US growth will slow towards potential in Q4, after a solid Q3 (+4.9%). Fiscal policy is expected to be less supportive next year but a soft landing remains our central scenario. Stagnation continues in the euro area after the contraction of 0.1% in Q3. Tighter financial conditions and the lack of fiscal stimulus are weighing on European domestic demand. In China, the government is prioritizing industrial production to the detriment of domestic demand for 2024.

Key macroeconomic signposts : United States

- The US economy is expected to slow down until Q2 2024. On the other hand, recession is not part of our central scenario. Consumption in the 4th quarter will remain solid though slower than in the 3rd quarter. Inventories will dent growth by almost 1 pp. The external balance is stable. Investment spending should improve.

- The federal deficit will be reduced next year with higher household taxation in Q2 in particular. The rise in the markets generates taxable capital gains. However, there is no proactive reduction of the deficit. The increase in household taxes should temporarily weigh on consumption.

- The risks of financial crisis appear contained. Household balance sheets remain healthy. Be careful, however, with the poorly regulated non-bank sector.

- The unemployment rate is expected to rise gradually as job creation moderates. The Fed would probably “like” to see unemployment rise towards 4.5% to alleviate domestic price pressures. The increase in the labor force is, however, supportive.

- Disinflation continues. Underlying inflation should decrease towards 2.6% at the end of 2024. Housing costs remain key for monetary policy. Potential inflation shocks for 2024 are a more restrictive OPEC policy (stronger reduction in quotas in Q1), climate effect on food prices.

Key macroeconomic signposts : Euro area

- Growth is sluggish in the Eurozone. Internal demand is affected by the increasingly significant impact of the ECB's strong monetary tightening and the continued high inflation while foreign trade is suffering from weak global demand.

- The surveys carried out among business leaders do not show any improvement and do not allow us to rule out a slight contraction in GDP in Q4 (after -0.1% in Q3) and thus a technical recession in the 2nd half of 2023.

- If the unemployment rate remains at historic lows (6.4% in November) in the Eurozone, the unemployment rate is starting to increase in certain countries. Faced with the drop in their orders, business leaders are becoming more cautious when it comes to hiring.

- Wages are expected to slow more slowly than inflation, which will partially offset the impact of weaker labor market dynamics. Negotiated wages still increased by 4.7% in Q3 over one year compared to 4.4% in Q2.

- Business investment should nevertheless continue to benefit from NextGeneration EU funds and the need to invest in renewable energy.

- A slow recovery should begin in 2024 and more particularly in the 2nd half of the year due to a less significant impact of the monetary tightening carried out by the ECB, an increase in real incomes and a strengthening of world trade.

- Inflation will slow but still remain high. It will no longer benefit from the strong negative contribution of energy, governments will stop measures aimed at containing the rise in energy prices and wages should moderate only slowly.of energy, governments will stop measures aimed at containing the rise in energy prices and wages should moderate only slowly.

Key macroeconomic signposts : China

- Will the Year of the Dragon be the year of China’s come back?

- International investors remain cautious about Chinese equity markets due to policy volatility.

- Yet, contrary to the techno crack in 2021, the Chinese authorities have shown themselves sensitive to their fears: removal of the head of video game advertising, acceleration of debt restructuring programs of developers and other companies. China wants to avoid contagion effects and significant outflows of capital, which could threaten its financial stability.

- The rhetoric has also changed on the economic side.

- The PBoC has indicated that it wants to further ease its monetary policy. In this perspective, Chinese interest rates have fallen, like the 10-year interest rate, which has reached a low since March 2020, below 2.5%.

- The Minister of Finance suggested a strengthening of fiscal policy favoring transfers to Chinese households to support consumption. This will require coordination of economic policies to enable China’s structural economic transition.

- Investment in industry at the expense of real estate remains robust, supporting Chinese growth.

- The real estate sector should stabilize, with social real estate absorbing the excess capacity of the sector.

- Disinflationary pressures are expected to abate, given the strengthening of measures to support activity.

- In conclusion, we have not changed our forecasts, which already included more proactive economic policies for 2024..

Monetary Policy

Divergence between the Fed and the ECB

- The Fed begins to talk about rate cuts

On December 13, the Fed left its rates unchanged for the third consecutive time. The highlight was the central bank’s significant change in tone following the stronger-than-expected slowdown in inflation. Median inflation expectations of FOMC members were revised down in 2023 and to a lesser extent in 2024 and 2025 (to 2.8%, 2.4% and 2.1% respectively). The FOMC members anticipate on average 3 rate cuts in 2024 while in September they expected a new increase in late 2023 (which did not take place) and 2 rate cuts in 2024. Jerome Powell went further in the press conference noting that discussions had focused on when it would be appropriate to lower rates. We now expect 4 rate cuts from the Fed funds in 2024, the first one probably taking place in the second quarter. - The ECB doesn’t let its guard down

The ECB left its rates unchanged for the second consecutive time in December. It revised down its inflation expectations in 2023 and 2024 (to 5.4% and 2.7% respectively) and to a lesser extent those for core inflation (5% and 2.7%). Core inflation in 2025 was revised up to 2.3%. Growth prospects were also revised down (0.6% in 2023 and 0.8% in 2024). Christine Lagarde was very clear: the work is not yet finished and this is not the time for the ECB to let its guard down. The central bank will closely monitor data on wages and unit profits during the first half of 2024. Rate cuts were not discussed. The ECB has announced changes to the PEPP. While the reinvestments of the tombs were to continue until the end of 2024 at least, the Central Bank decided to reinvest only half in the 2nd half (at the rate of 7.5 billion euros on average per month) and to put an end to 2024. We anticipate 3 rate cuts from the ECB in 2024, the first probably taking place in the 2nd quarter, after the Fed.

Market views

Asset classes

- US rates: the Fed will begin an easing cycle in 2024. Interest rates should slide towards 3.75% at the end of 2024 despite possible tensions due to the debt refinancing of the Treasury.

- European rates: the Bund should normalize somewhat in the first quarter, with the ECB reluctant to act as quickly as expected by the markets.

- Sovereign spreads: a later reduction than expected of the PEPP and the prospect of lower rates eases the pressure linked to degraded public finances.

- Euro area inflation: breakeven inflation rates seem to be anchored at levels slightly higher than the Central Banks' targets.

- Euro credit: credit spreads should remain stable. High yield should be marked by a decompression trend.

- Foreign exchange: the euro should remain around $1.10 due to weak growth in the euro zone.

- Equities: falling margins will be offset by higher multiples.

- Emerging debt: spreads benefit from monetary relief from the Fed.

Ostrum Perspectives January 2024

Download Ostrum Perspectives January 2024