Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum AM's views on the economy, strategy and markets.

Outlook at 06/24/2026.

The CIO Letter

The Warsh era begins

Kevin Warsh's arrival at the helm of the Fed marks a turning point in the conduct of U.S. monetary policy, especially as the Iran war may finally find a resolution. Several task forces have been launched to reform the institution. Oil is trading around $75 per barrel despite declining inventories. The handover between Powell and Warsh comes at a pivotal moment with rising inflation accentuated by the oil shock and the first signs of improvement from the labor market. In the eurozone, the ECB is raising rates in response to rising inflation expectations and core inflation accelerating toward 2.5%. Another hike will bring the deposit rate to 2.50% in September. Activity declined in the eurozone in Q2 and should experience a slow recovery thereafter. In China, exports remain the main driver of activity but inflation is gradually recovering.

On financial markets, AI is dominating headlines, with prominent IPOs from SpaceX, to be followed by Anthropic and OpenAI. Profit-taking is generating increased volatility, particularly on the Nasdaq, Kospi, and Nikkei. Nevertheless, the outlook for earnings remains positive, especially in the United States. In bond markets, fluctuations in oil prices have explained the bulk of yield changes since the onset of the war. Kevin Warsh's assessment of inflation risks will be crucial for bond markets. The ECB's policy, meanwhile, is more transparent, which should help the Bund stabilize around 3%. Sovereign and corporate debt spreads remain surprisingly inert and tight considering the volatility in interest rates. A slight widening of spreads is anticipated. High-yield debt is defying gravity, though default rates remain low. Regarding currencies, the yen, trading above 160 against the dollar, could prompt intervention from the Bank of Japan. The euro continues to trade within a narrow range between $1.14 and $1.18 since the start of the Iranian crisis.

Economic Views

THREE THEMES FOR THE MARKETS

-

Growth

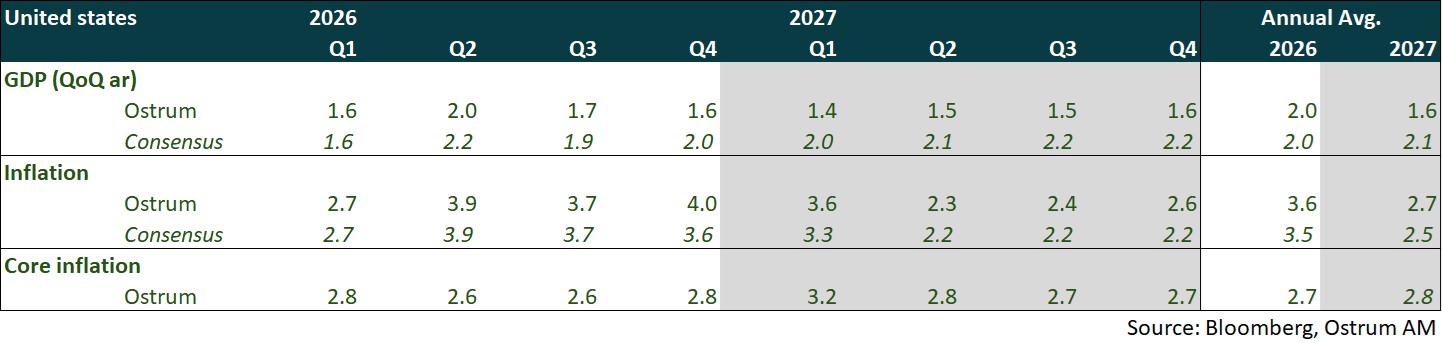

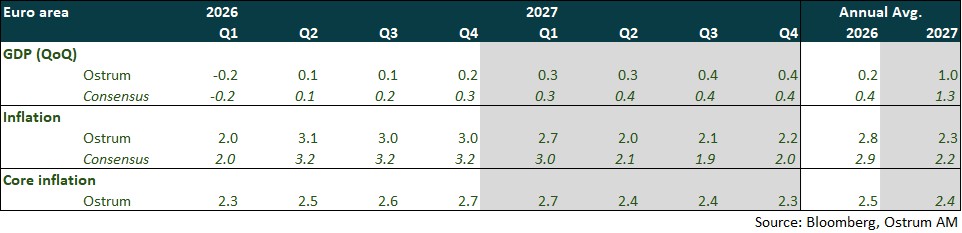

Growth trajectories are diverging. The United States recorded moderate growth in Q1 (+1.6% annualized), supported by domestic demand but showing signs of deceleration. In the Eurozone, GDP contracted by 0.2% quarter-on-quarter in Q1, largely driven by a sharp downward revision in Irish GDP (-12,1% QoQ). Excluding Ireland, growth in the region stood at +0.2% QoQ. French GDP declined by 0.1% QoQ, reflecting weaker domestic demand weighed down by the energy shock. China continues to exhibit robust momentum (+1.3% QoQ, or +5.0% YoY), driven by strong export performance, particularly in high-tech sectors such as artificial intelligence.

-

Inflation

Iran and AI are contributing to rising inflationary pressures. In the United States, inflation accelerated to 4.2% in May, reaching a three‑year high, driven by higher energy costs. Core inflation also edged up to 2.9% from 2.8% in April. The transmission of the energy shock has been more pronounced in the euro area. Headline inflation rose to 3.2% in May, while core inflation increased to 2.6% from 2.2% previously. This trend reflects stronger services inflation, which reached 3.5% year‑on‑year, up from 3.2% in April. By contrast, inflation in China remained stable at 1.2% in May, supported primarily by contributions from transportation and communication components.

-

Monetary policy

Central banks are facing the inflation vs. growth dilemma. At the first meeting chaired by Kevin Warsh at the Fed, the decision to maintain the status quo was unanimous, despite inflation being well above target. Forward guidance was also removed. The ECB raised its key interest rates by 25 bps due to the spillover of the energy shock to other prices, particularly services. It left the door open to another rate hike. The PBOC is not under pressure and is maintaining an accommodative bias to support domestic demand.

ECONOMY: UNITED STATES

Growth is mediocre outside of AI, which is growing at 25% annually; a slowdown seems inevitable.

- Demand: Consumption is constrained by falling real wages and employment stagnation. The trade balance is improving temporarily with petroleum product exports but the deficit should widen again in the second half. Housing investment continues to contract due to a shortage of goods and rising prices. Productive investment will remain essentially driven by AI (data centers, software and R&D).

- Labor Market: The situation is uncertain. Revisions indicate an improvement in April-May. The unemployment rate caps at 4.3% given low participation (declining immigration, 55+ age group). However, the number of bankruptcies suggests significant revisions to employment figures.

- Fiscal Policy: The reimbursement of illegal tariffs (~0.5 pp of GDP) would constitute a stimulus benefiting businesses. The budgetary situation remains precarious and prevents debt extension.

- Inflation: Upside risks are accentuated by the war in Iran. Housing, however, contributes to containing inflation. Inflation will remain above target.

ECONOMY: EURO AREA

The energy shock stemming from the conflict in the Middle East is expected to weigh on euro area growth in the second and third quarters, before a gradual recovery in activity supported by easing inflation.

- Irish GDP volatility: Euro area growth is distorted by the volatility of Irish GDP, driven by multinationals (-12.1% in Q1). Excluding Ireland, euro area GDP would have grown by 0.2%. A partial rebound in Irish GDP in Q2 and Q3 is expected to partly offset the ongoing slowdown in euro area.

- Domestic Demand: Business surveys point to a sharp downturn in activity in April and May, along with a plunge in consumer confidence, driven by expectations of a strong rise in prices and elevated uncertainty. Household consumption is expected to be hit in Q2 and Q3 by losses in purchasing power, while investment will be constrained by more cautious behaviour from both firms and households.

- External Demand: External trade is expected to make only a limited contribution to growth in a context of slowing global demand. Europe also continues to face increasing competition from China and remains constrained by weak competitiveness.

- Fiscal Policy: Aside from Germany, which is significantly increasing its infrastructure and defence spending, fiscal space remains limited for most countries. Support measures implemented so far are very modest compared with 2022.

- Inflation: Inflation is expected at 2,8 % on average in 2026, driven by the energy shock and its gradual pass-through to other sectors of the economy. It should moderate in 2027, in line with energy prices.

ECONOMY: CHINA

Despite the Middle East conflict, China confirms the resilience of its economy. China is undergoing a structural shift: it will export inflation.

- Activity: Q1 GDP growth reached 1.3% q/q, i.e. 5% y/y, driven by exports (close to 15% y/y in Q1). The resilience in May activity, as reflected in PMI surveys, contrasts with a sharp slowdown in hard data, particularly investment (-1.6% y/y).

- The decline in public spending—especially infrastructure—likely explains this and should reverse in the coming months. Stabilizing US-China relations should support investment.

- Exports: External trade remains very dynamic, supported by exports of technology goods, AI equipment, and renewables. The easing of US non-tariff barriers should further support Chinese foreign trade.

- Consumption: The NBS has released a new retail sales series combining goods and services, which has risen by 2.8% year-on-year since the beginning of the year. Retail sales of services increased by 5.8% year-on-year, while goods rose by 1.2% year-on-year over the same period. Service consumption is expected to strengthen, supported by developments in digital services AI.

- Inflation: Cost pressures remain elevated despite a slight moderation in input prices. This has fed through to producer prices (+2.8% y/y in April) and export prices (+5% y/y), which have reached their highest level since April 2023.

- Structural shift: The Middle East conflict is acting as a catalyst for China. Domestic reforms combined with geopolitical constraints mean China can no longer neutralize commodity price volatility. China is set to export inflation.

Monetary Policy : FED

Kevin Warsh leaves his mark from his very first meeting at the helm of the Fed

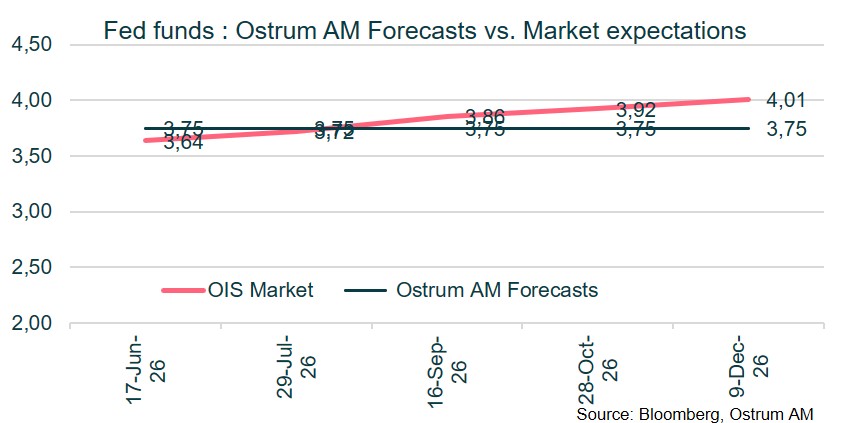

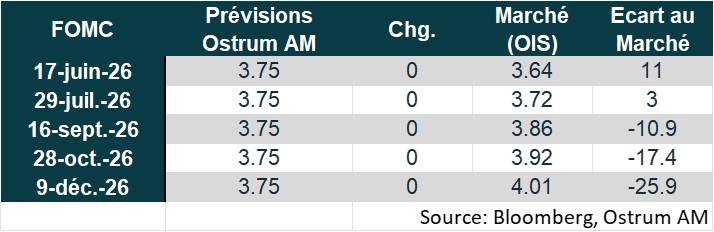

- At his first meeting as Chair of the Fed, held on June 16–17, Kevin Warsh has already altered the central bank’s communication. Forward guidance on the future path of interest rates has been removed, reducing the Fed’s statement to just nine lines.

- The decision to leave rates unchanged, within the 3.50%–3.75% range, was unanimous. Economic activity is still viewed as solid, while inflation remains elevated. The statement states that the Fed will deliver price stability (one of its core objectives).

- Another change is that Kevin Warsh did not present his own outlook in the SEP (Summary of Economic Projections) and, at the same time, downplayed those provided by FOMC members. Nine members expect at least one rate hike by year-end, eight foresee a status quo, and one is in favor of a rate cut. These divergent views reflect limited conviction within the FOMC.

- Kevin Warsh also announced five task forces aimed at overhauling the Fed, with most conclusions expected by year-end. They cover: communication, balance sheet policy, data usage, productivity and employment, and the inflation analysis framework.

- With Kevin Warsh at its helm, the Fed is operating under the influence of the White House. Although our forecast is for a status quo on the Fed funds rate through the end of the year, the next rate move is more likely to be a cut.

Monetary Policy : ECB

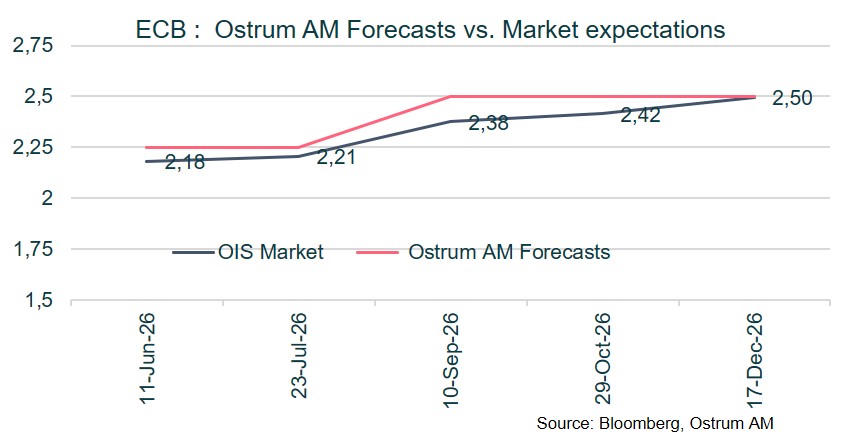

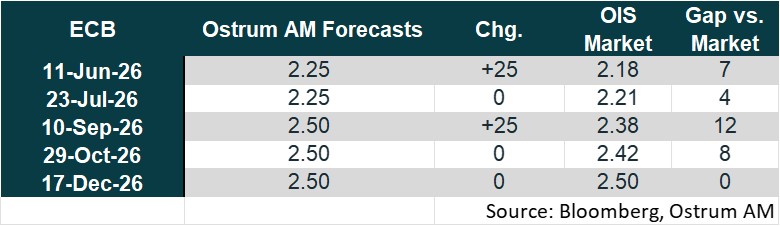

Heading toward a second ECB rate hike in September.

- As it had largely signaled at its April meeting, the ECB raised its rates by 25 bps on June 11, for the first time since September 2023, bringing the deposit rate to 2.25%.

- Persistently high oil prices, driven by the ongoing conflict in the Middle East, along with signs that the energy shock is feeding through to services prices, have led the ECB to significantly revise its inflation outlook upward.

- The prospect of a stronger pass-through of the energy shock to core inflation (expected at 2.5% in 2026 and 2027) reinforces our view that the ECB will deliver another 25 bps rate hike at the September 10 meeting, in order to anchor inflation expectations.

- During the press conference, Christine Lagarde dismissed the notion that this was an insurance or pre-emptive rate hike, stating that the decision was justified under all three scenarios (milder, adverse and severe).

- The framework agreement signed between the United States and Iran does not alter our scenario. Even assuming a full reopening of the Strait of Hormuz (which is not guaranteed), oil prices would remain above pre-conflict levels, posing a risk of second-round effects that the ECB will need to contain.

Market views

Asset classes

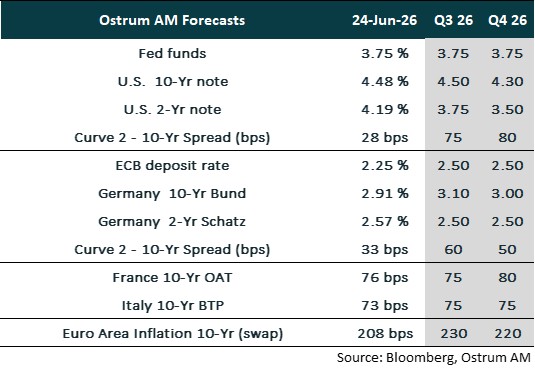

- U.S. Rates: Kevin Warsh has assumed his duties as head of the Fed and chaired his first FOMC in June with the ambition to reform the institution. Monetary status quo should be maintained until the end of the year.

- European Rates: The ECB should raise rates once more to weigh on inflation expectations. The 10-year Bund will oscillate around 3.10% before declining toward 3.0% at year-end.

- Sovereign Spreads: Sovereign spreads have almost completely erased the Iranian crisis. Political considerations in France should weigh on the OAT at year-end. Italy's spread should remain around 75 basis points or higher.

- Eurozone Inflation: Long-term inflation expectations have increased due to the oil shock. The premium is beginning to diminish.

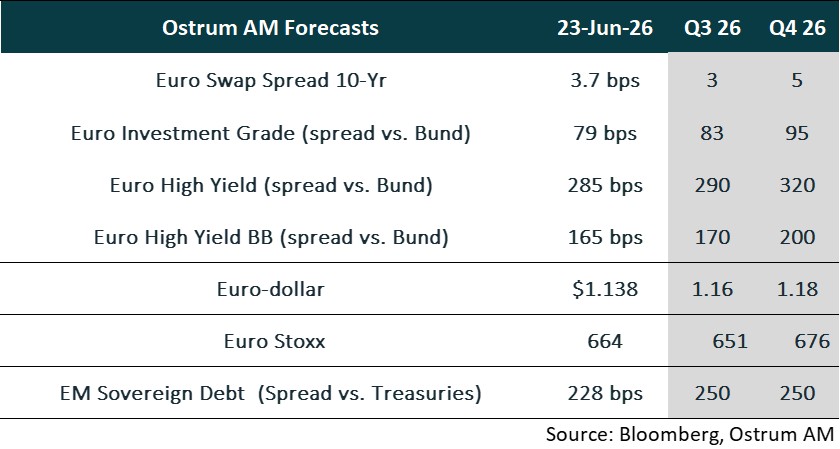

- Euro Credit: IG credit spreads have quickly erased the Iranian crisis and the primary market is well absorbed. However, valuation levels would justify widening by year-end.

- Euro High yield: High yield valuations should normalize over the course of the year. The default rate, however, remains contained and below the long-term average.

- Exchange Rates: The structurally bearish trend for the greenback should resume as the Iranian crisis dissipates.

- European Equities: Earnings should improve in the second half of the year.

- Emerging Debt: The EMBIG is withstanding the Iranian crisis. Spreads will remain tight around 250 basis points.