Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Listen to podcast (in French only)

(Listen to) Zouhoure Bousbih’s podcast:

- Review of the week – Echoes of 2022;

- Theme – Another Energy Shock, Like 2022?

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: Is AI the systemic risk of the 2020s?

- Artificial intelligence is fundamentally reshaping the global economy and business models, with hyperscalers (Meta, Alphabet, Microsoft and others) leading massive infrastructure investments.

- According to the BIS, AI has contributed 0.4 percentage points to annual U.S. GDP growth over the past three years, with investments now accounting for 5% of GDP—a larger share than during the dot-com boom.

- Tech giants are increasingly reliant on debt ($200B+ in private credit) and sophisticated financial arrangements (e.g., conduit financing) to fund AI expansion, creating potential systemic risks.

- Credit rating agencies point to accounting gaps used by hyperscalers to hide off-balance sheet liabilities.

- Authorities must monitor rising debt levels, enforce capital requirements, and reassess oversight of private credit markets to prevent AI-driven systemic vulnerabilities.

AI is the major driver of U.S. growth

AI investment spending may have accounted for nearly half of U.S. growth in 2025.

The artificial intelligence boom is redefining the financial and technological landscape, reshaping the priorities of capital markets and commanding unprecedented levels of investment. AI has the potential to revolutionize industries ranging from software to hardware, and even disrupt traditional business models.

According to a BIS study, the AI investment boom has become a major driver of US economic growth, contributing an average of 0.4 percentage points to GDP growth over the past three years. By mid-2025, expenditures on IT manufacturing facilities and data centers reached 1% of GDP, with total IT investment rising to 5% of GDP. This level exceeds even the dot-com boom peak of 2000. AI infrastructure becoming a critical component of modern capital formation.

Major technology firms including Meta, Alphabet, Amazon, Microsoft, Nvidia, and Oracle —often referred to as hyperscalers—.are at the forefront of this transformation. Their collective commitment to AI is reflected in investment plans totaling $600 billion in 2026 and more than $3 trillion in data and power infrastructure through 2030 funded by private shareholders and creditors. A recent Bloomberg Intelligence report found that only 35% of global cloud computing infrastructure is optimized for AI workloads. That suggests increasing capex is justified if hyperscalers want to be able to turn a profit.Despite the optimism and the impressive profitability of these firms, the true payoff of such monumental investments remains uncertain, echoing the lessons of past technological revolutions where not all major players reaped the anticipated gains. As the AI sector continues to expand, its influence on both the equity and credit markets grows, raising questions about the long-term implications for market structure, investor behavior, and economic resilience.

From financial flexibility to complexity and debt constraints

As operating cash-flows lag spending plans, Big Tech must borrow heavily in public and private markets.

Hyperscalers have embraced the AI boom from a position of financial strength. Low leverage and immense free cash-flows have made hyperscalers high-quality stocks. A critical transformation in how AI companies fund their operations is underway. Traditionally, leading IT sector firms financed investments internally through operating cash flows while maintaining minimal debt levels. However, the unprecedented scale of current and anticipated AI investments has forced these companies to seek external funding sources. Free cash flows now lag behind capital expenditures in absolute terms, necessitating a strategic pivot to debt financing. This shift represents a fundamental change in the financial structure of technology companies and signals the massive capital requirements of AI infrastructure development.

The explosive growth of private credit as a financing mechanism for AI investments. According to the BIS paper, outstanding private credit loans to AI-related sectors have surged from near zero to over $200 billion in a remarkably short timeframe. Projections suggest this could reach $300-600 billion by 2030, indicating the continued importance of alternative financing channels. The share of private credit loans to AI companies has jumped from less than 1% to almost 8% of total outstanding loan volumes.

Creative accounting, SPVs and conduit: a blast from the past?

Central to the AI expansion is a complex and increasingly intricate web of financing structures designed to support the sector’s capital-intensive growth. Tech giants are not only issuing record-breaking corporate bonds—such as Meta’s $30 billion financing for its Louisiana data center—but are also leveraging sophisticated arrangements like conduit financing and circular capital flows to optimize their balance sheets and manage risk exposure. Conduit financing, for instance, involves special purpose vehicles borrowing funds, constructing infrastructure, and subsequently leasing assets back to the originating company, effectively keeping debt off the parent’s books while maintaining significant lease obligations. Moody’s considers that this gap in US accounting rules allows Big Tech companies to conceal tens of billions of dollars of potential liabilities for their AI data centers. According to a financial Times article, the rules mean AI companies may not have to account either for the cost of renewing a data center lease or for the cost of not renewing it. In some cases, companies are taking relatively short-term leases (4 years in the case of Meta’s Hyperion data center in Louisiana) while at the same time guaranteeing to pay compensation if they do not renew (up to $28 billion in this case). Under US GAAP, the lease renewal must be “reasonably certain” (>70% probability) before it is accounted for. The cost of the residual value guarantee must be accounted for if the non-renewal is “probable”, meaning more than 50 % likely. Potential liabilities hence go down this accounting black hole. In the footnotes of Meta’s most recent annual report, one can read: “As of December 31 2025, RVG payments are not probable and therefore, no liability has been recorded”.

Moreover, circular financing structures obscure the location and magnitude of risk. For example, Nvidia invests in entities like CoreWeave, which then purchase Nvidia hardware, lease capacity to other tech firms, and generate revenues that recycle back into the system. These capital flows are dizzying in their complexity, involving private loans from insurance companies, securitizations with varied risk tranches, and multi-billion-dollar commitments from private-credit firms, much of which is ultimately held by mutual funds and ETFs. While these mechanisms are technically compliant and legal, they challenge traditional notions of transparency and risk distribution. It could make it more difficult for regulators to pinpoint where exposure resides and how it might evolve as the sector’s obligations mount over decades.

The systemic risk has shifted to hyperscalers and private credit

AI is now the main source of systemic risk.

At present, financial stability risks appear moderate currently, there are several areas of concern for policymakers and market participants. The increasing leverage of traditionally low-debt AI firms could amplify future shocks and affect financial intermediaries if expected returns fail to materialize.

The concentration of risk—whether on corporate balance sheets, within passive investment vehicles, or through off-balance-sheet structures—raises the specter of instability should AI monetization fall short of expectations. If the lofty valuations assigned to leading AI firms are not supported by future returns, the consequences could be severe.

Meanwhile, the surge in bond issuance—potentially adding $120 billion in net supply from hyperscalers this year alone—is largely being absorbed by passive funds, whose indiscriminate buying could amplify volatility if market conditions deteriorate. The proliferation of debt, both seen and hidden, exposes investors to risks that may only become apparent in a downturn, especially given the sector’s reliance on long-term forecasts and untested conduit structures.

The disconnect between debt pricing and equity valuations—loan spreads for AI firms remain similar to non-AI companies despite sky-high equity valuations, suggesting potential mispricing of risks.

Regulators must monitor the concentration of leverage, enforce robust equity capital requirements, and reconsider the relaxed oversight of private credit markets that currently prevails. Without vigilance and proactive analysis, the AI boom could turn into a systemic vulnerability, with repercussions that could extend far beyond the technology sector itself.

Conclusion

The AI boom has begun to transform the economy as investments have already had a significant impact on US growth. However, Big Tech borrowing needs have exploded as operating cash flows no longer cover investment spending. Corporate bond issuance from US Tech companies is increasing sharply in the US and around the world. Financing arrangements and accounting have become more creative. If things turn sour, creative accounting and illiquid financing vehicles could make AI the systemic risk of the second half of the 2020s.

Axel Botte

Chart of the week

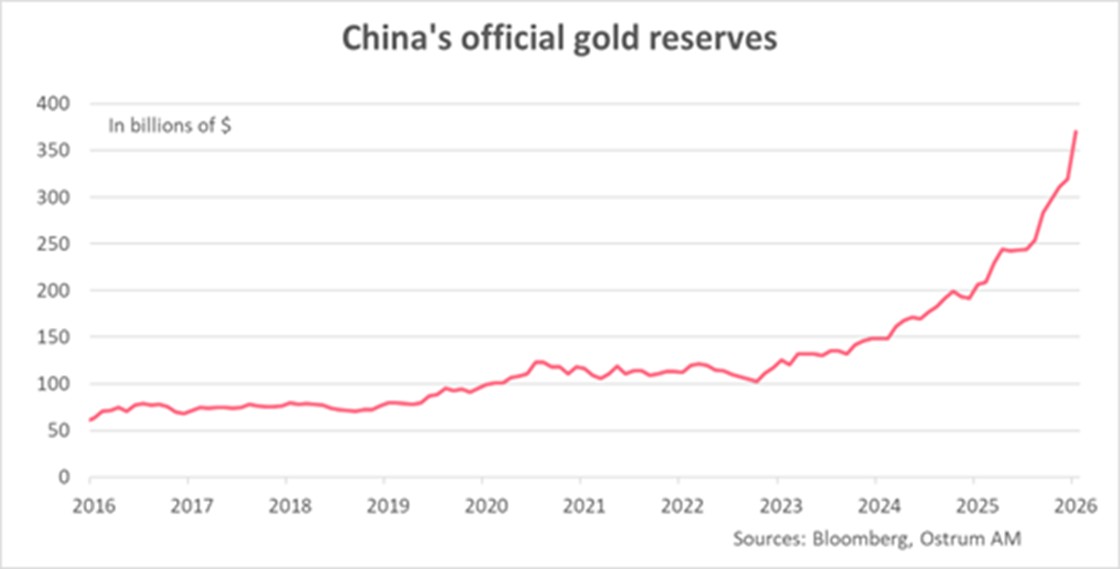

China’s gold reserves rose by more than 15% year-on-year in January to a record high of USD 369.6 billion, marking the eighth consecutive increase.

Since October 2022 and the freezing of Russian assets, China’s gold reserves have increased by USD 266 billion, or 260%.

Gold now accounts for 11% of China’s official reserves, close to the standard 15% level for central banks.

Strong Chinese demand is supporting the rally in the yellow metal.

Figure of the week

108

108 minutes. The duration of Donald Trumps’s State of the Union address, the longest on record.

Market review:

- Fed: Monetary policy powerless against the AI shock?

- Rates: T-note breaks below 4%, Bund follows suit under 2.70%.

- Equities: Indices hold firm, but rotational activity intensifies.

- Private Credit: Two fresh default and asset impairment events in the UK and US.

The AI Dilemma and Private Credit Turmoil

Risk-free rates are plummeting (4% on the T-note) in response to adverse developments in the private credit market (KKR, MFS) despite emerging inflationary signals. The risk of military intervention in Iran maintains upward pressure on crude oil. Credit spreads are widening moderately.

Treasuries and Bunds have once again emerged as the primary safe-haven assets amid financial stress, related to private credit. The easing in long-term JGB yields is also contributing to the bond rally. Equity markets remain stable despite heightened volatility at the single-stock level. Below the surface, volatility remains elevated. Interest rate volatility, conversely, remains subdued, with sovereign and credit spreads holding steady

From a cyclical perspective, February regional Fed surveys indicate a modest downward inflection in US growth momentum. Real estate data confirm the price recovery observed since autumn, reflecting the shortage of available housing inventory. Existing home sales remain at historic lows of approximately 4 million transactions annually. Furthermore, intense debate rages within the Fed regarding the central bank's capacity to mitigate potential unemployment increases driven by AI adoption. Capital-labour substitution will elevate the equilibrium unemployment rate while simultaneously boosting potential growth and the "neutral" rate. Demand stimulation through rate cuts would likely prove ineffective in curbing unemployment increases, leaving the Fed powerless against labour market deterioration. Concurrently, employment difficulties facing recent graduates would result in human capital erosion, below-expectation wages, and further deterioration in student loan defaults. In the eurozone, surveys present mixed signals without undermining the recovery narrative. French and Spanish inflation readings came in slightly above expectations ahead of the eurozone flash estimate.

In financial markets, sovereign yields are declining. The T-note has breached the 4% threshold while Bunds trade below 2.70%. AI development implications are exerting considerable pressure on software company valuations and their creditors. Risk aversion logically benefits government bonds. Additionally, the JGB curve steepening is attracting foreign flows. Declining Japanese yields (2.14% on the 10-year) are transmitting across major bond markets. Inflation nonetheless surprised to the upside in Australia, Japan, Europe, and even the United States, with producer prices at +2.9% year-on-year. Near-term inflation expectations are also incorporating crude oil increases linked to the Iranian situation (Brent at $72 per barrel on Friday). Eurozone sovereign spreads are widening marginally, benefiting alongside Bunds from risk aversion. French OATs (57bp at 10 years) have outperformed Italian BTPs (60bp) in recent weeks. Credit is widening (+3bp) moderately in reaction to current stress in private and structured credit funds. The iTraxx crossover, frequently employed as a hedge, is approaching 260bp. Equity markets are experiencing turbulence, though overall volatility remains near 20%, well below crisis levels. Utilities and financials are outperforming healthcare and technology in Europe. The S&P 500 posted weekly gains while displaying intraday fragility. The impressive outperformance of the Kospi (+48% in 2026) and Nikkei (+17%) continues.

Axel Botte

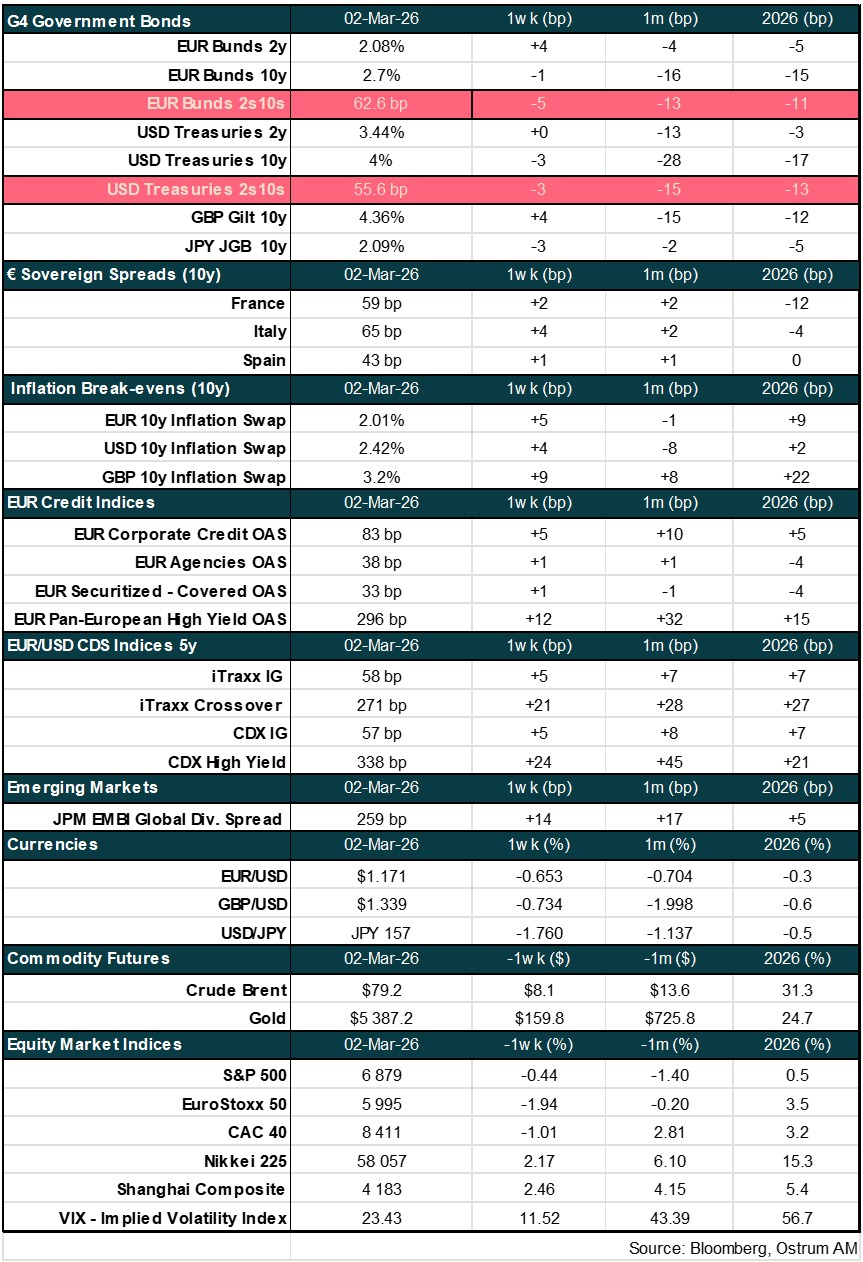

Main market indicators