Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Listen to podcast (in French only)

(Listen to) Axel Botte’s and Zouhoure Bousbih’s podcast:

- Review of the week – The ongoing Iranian crisis;

- Theme – Hormuz Crisis: The Spectre of a Covid‑19‑Type Shock Looms Over Global Supply Chains.

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: Hormuz Crisis: The Spectre of a Covid‑19‑Type Shock Looms Over Global Supply Chains

- The Hormuz crisis is transforming a localized energy shock into a global value‑chain disruption by simultaneously tightening energy supply, maritime logistics, and critical industrial inputs.

- Asia stands on the front line given its structural reliance on imported LNG, its central role in global production networks, and its high exposure to maritime transport disruptions.

- The semiconductor industry represents the systemic weak link, owing to its acute sensitivity to energy outages and to shortages of non‑substitutable critical inputs such as helium, making it particularly vulnerable to supply‑side disruptions.

- The risk is that of Covid‑19‑like inflationary pressures—targeted in nature but potentially more persistent.

Hormuz: Asia’s Energy Achilles’ Heel

For decades, Asian economies have built their growth model on the stability of global oil and natural gas markets. The current shift in the energy regime is challenging this equilibrium and exposing the region’s structural vulnerabilities.

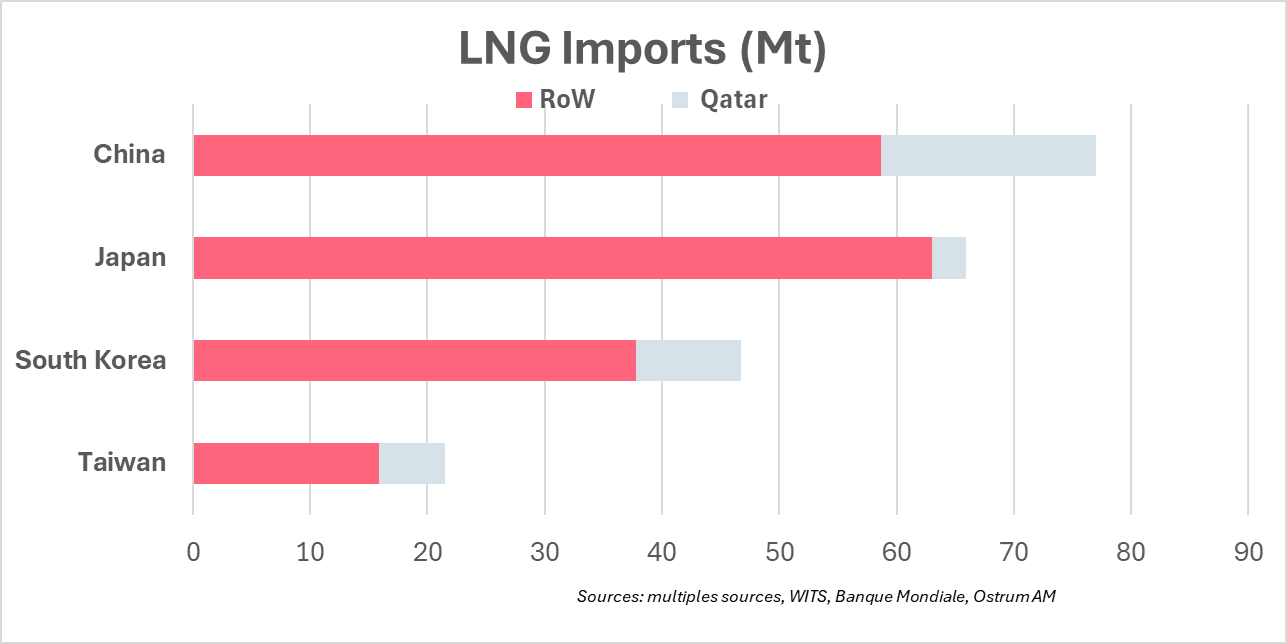

Asia has developed a structural dependence on fossil fuels transiting through the Strait of Hormuz. Almost 90% of liquefied natural gas (LNG) and around 85% of crude oil passing through the Strait of Hormuz are destined for the region.

Nearly 90 % of LNG and 85 % of crude oil transiting through the Strait of Hormuz are destinated for Asia.

The main exporters in the Gulf are Qatar (the world’s second‑largest LNG exporter) and the United Arab Emirates. Several major Asian economies are therefore highly exposed to the Middle East, as illustrated in the table opposite.

Japan and South Korea are the two most exposed countries, importing respectively around 90% and 60% of their crude oil needs from the Gulf. Taiwan is also highly exposed to the Strait of Hormuz, sourcing around 60% of its crude oil imports from the region. More broadly, the Middle East accounts for around 45% of China’s crude oil imports.

LNG Shock: A Systemic Energy Shock for the Semiconductor Industry

The disruption to LNG supplies is unfolding in a region that accounts for nearly half of global demand.

China is the world’s largest LNG importer, with Qatar representing around 24% of its total gas imports. Japan ranks second globally, although Qatar accounts for only about 3% of its gas imports. Taiwan is also highly dependent on Qatari LNG, which represents around 26% of its total gas imports.

In China, Japan, South Korea, and Taiwan, LNG is a critical pillar underpinning power‑grid stability and the smooth functioning of the industrial base.

LNG is a fundamental pillar of the semiconductor industry.

In this context, the energy shock extends well beyond the energy sector itself, becoming a systemic risk for the semiconductor industry—a central link in global value chains—whose production continuity depends on an exceptionally reliable power supply.

Semiconductor manufacturing is in fact extremely sensitive to power quality: even minor power disruptions can trigger substantial industrial losses and prolonged production outages. This structural vulnerability helps explain the heightened nervousness in financial markets, as reflected in the sharp corrections seen in regional equity markets, notably in South Korea and Taiwan. These economies concentrate a large share of global semiconductor production while facing a growing dependence on imported LNG.

Semiconductors: A Critical Dependence on Helium

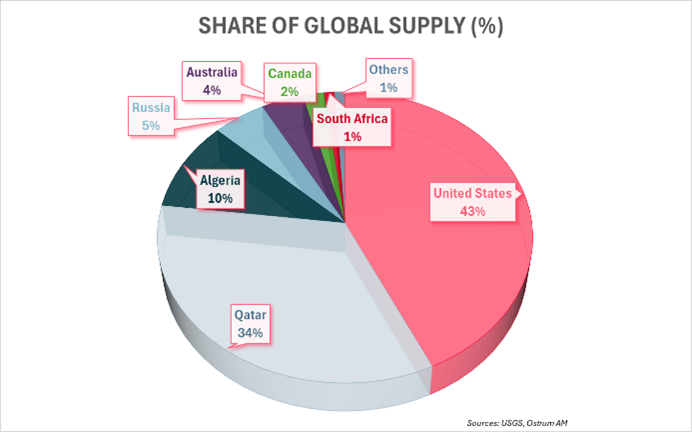

Helium is a critical input for industrial continuity in the semiconductor sector, on a par with electricity. It is an indispensable gas in advanced manufacturing processes, notably for the ultra‑stable cooling of lithography equipment. The semiconductor industry accounts for nearly 30% of global helium demand.

The semiconductor industry a ccounts for around 30 % of global helium demand.

Helium is a by‑product of natural gas extraction, implying a structurally rigid supply and a high geographical concentration of production, as illustrated in the chart opposite.

Helium supply is essentially concentrated in two countries: the United States (43%) and Qatar (34%).

Helium supply is concentrated in two countries: the United States (43 %) and Qatar (34 %)

LNG processing facilities play a key role in helium recovery. The declaration of force majeure by QatarEnergy has disrupted LNG supplies, which will mechanically translate into tighter helium availability, thereby increasing supply‑side pressures on the semiconductor industry.

Logistical Disruption and Supply‑Chain Fragmentation

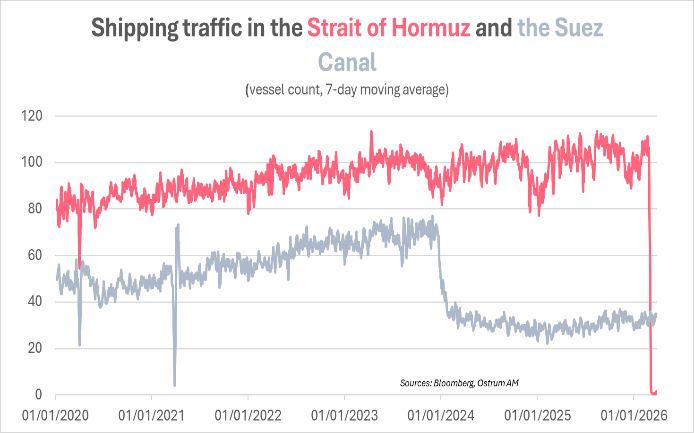

The closure of the Strait of Hormuz is triggering an abrupt and costly reconfiguration of global shipping routes, exacerbating the logistical disruptions already observed in the Red Sea in 2024.

The collapse in traffic, the rise in security risks, and the surge in insurance costs have forced major shipping lines to reroute flows around the Cape of Good Hope, significantly lengthening transit times and reducing effective global maritime transport capacity.

The collapse in traffic through the Strait of Hormuz is exacerbating tensions across production chains, exerting upward pressure on prices…

This logistical dislocation represents a structural shock for the semiconductor sector, which relies on just‑in‑time deliveries of heavy equipment and highly sensitive chemical inputs. Current geopolitical tensions are therefore intensifying strains along production chains, extending delivery lead times and exerting upward pressure on global semiconductor prices.

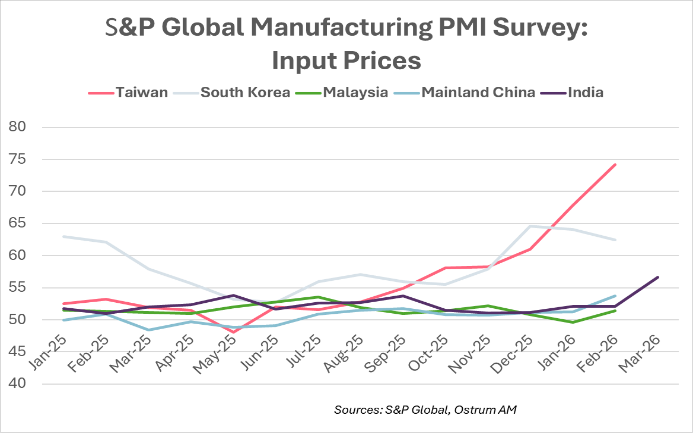

The semiconductor supply chain is already under strain

S&P Global PMI surveys for the manufacturing sector already point to rising input prices linked to the Middle East conflict, notably in India, as illustrated in the chart opposite.

… For a supply chain already under strain

Data for March are not yet available for other countries. However, price pressures are already trending higher in China, Malaysia, and particularly in Taiwan.

This development partly reflects the rapid surge in semiconductor demand driven by artificial intelligence, which has led not only to tight supply conditions for high‑end chips but also to shortages of components used in consumer and industrial electronics.

The tightening of helium supply is likely to exacerbate these pressures further.

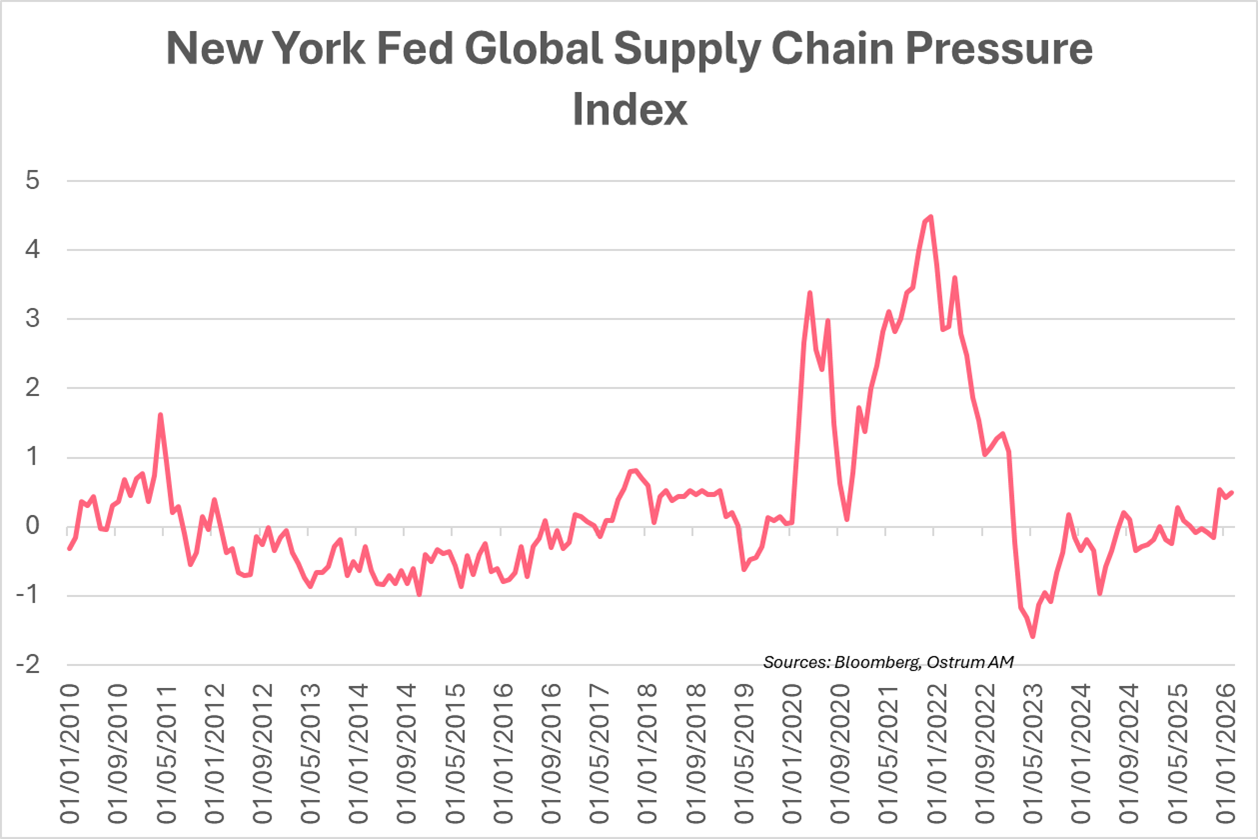

Meanwhile, the New York Fed’s Global Supply Chain Pressure Index rose in February—likely reflecting the impact of higher tariffs on input costs and occurring ahead of the outbreak of the conflict—signaling the early emergence of renewed strains across global value chains.

Conclusion

Beyond an energy shock, the Hormuz crisis is reviving the risk of distortions across global value chains, comparable in its transmission mechanisms to the Covid‑19 episode.

By concentrating stress on oil and, most notably, LNG flows to Asia, the shock propagates to the very core of global production networks—where critical manufacturing capacity and key technology value chains are located, foremost among them the semiconductor industry, which is already under strain.

The issue is no longer merely the level of prices, but the duration of the disruptions and the extent to which they feed through into industrial cost structures. The major difference relative to the Covid‑19 episode is that the current supply shock is not universal, but geographically and sectorally concentrated. Yet this very concentration may make it potentially more severe and longer‑lasting for certain critical segments of global value chains.

Zouhoure Bousbih

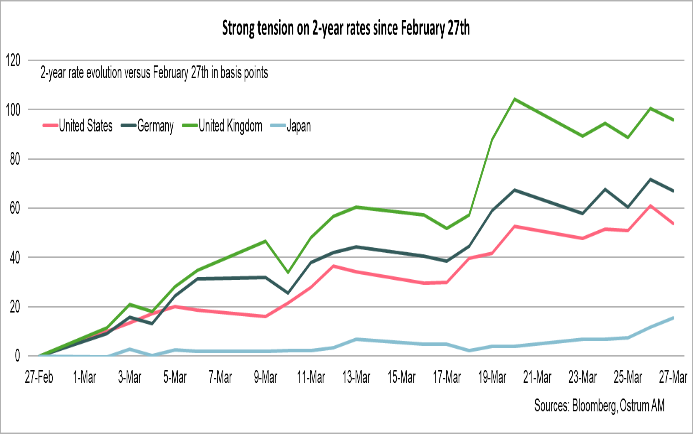

Chart of the week

The geopolitical shock in the Middle East is now being transmitted to interest‑rate markets—not through an immediate recessionary scenario, but via the risk of a resurgence of imported inflation. This is prompting investors to reprice central bank policy rates higher and for longer, resulting in pronounced volatility at the two‑year maturity.

The United Kingdom has recorded the sharpest increase, with its two‑year yield rising by nearly 100 basis points, reflecting its high degree of energy vulnerability. Short‑term rates have increased by more than 65 basis points in Germany and around 55 basis points in the United States. Japan’s two‑year yield has also been pulled higher in the wake of other G4 markets, reaching its highest level since 1996, underlining the country’s strong exposure to crude oil imports from the Gulf region.

If uncertainty surrounding energy supply and logistical chains persists, pressure is likely to remain concentrated on the short end of sovereign yield curves, reinforcing volatility across global bond markets.

Figure of the week

112

Maritime traffic via the Cape of Good Hope has surged by 112% year‑on‑year since the outbreak of the Middle East conflict.

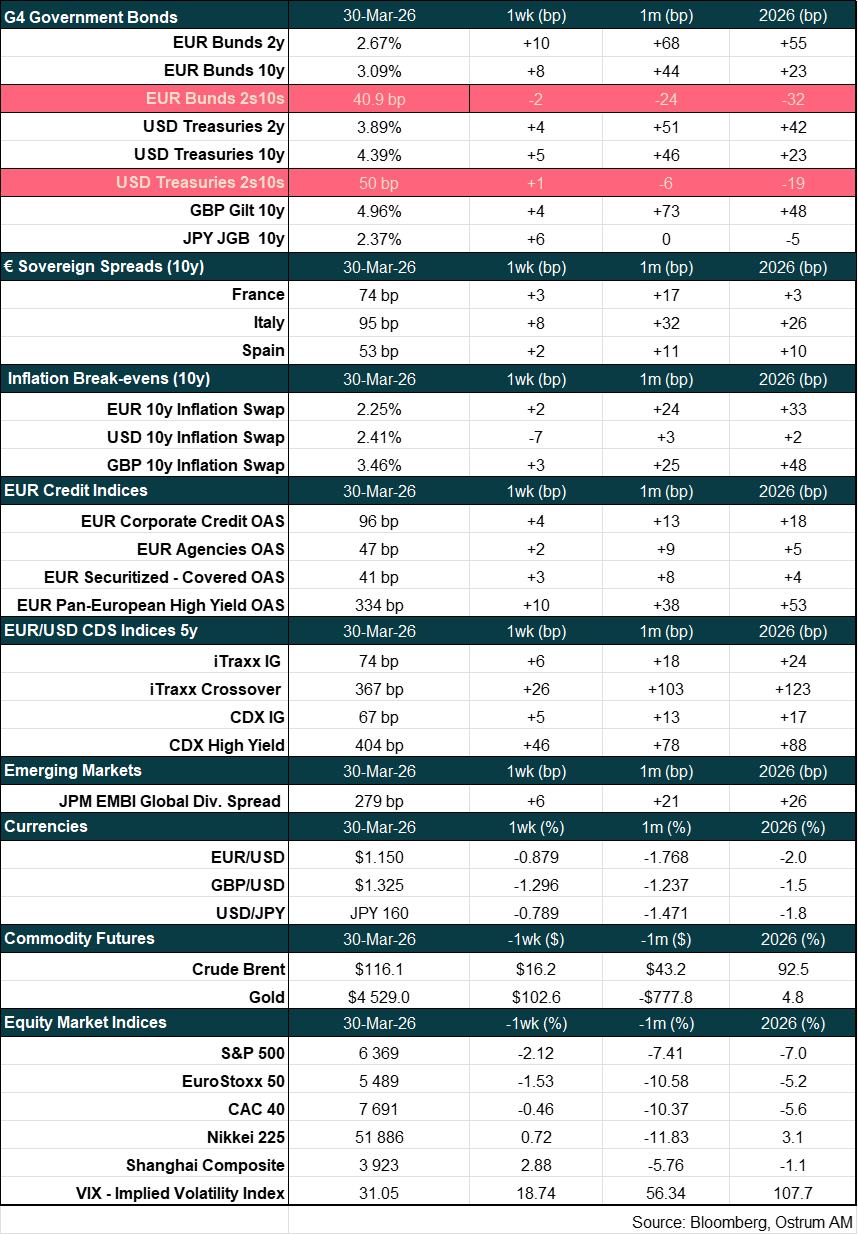

Market review:

- Iran crisis: Trump's delayed ultimatum to Iran offers no comfort to the market;

- Company surveys: lengthening delivery times and rising input prices;

- Bonds: yield curves steepening over the week;

- Equities: S&P plunges at week's end on fears of a longer conflict.

Fears of a more protracted conflict are setting in

The week proved to be very volatile, with markets reacting to contradictory information ranging from fears of an escalation of the conflict to alleged progress in discussions for a potential peace agreement. The postponement of the ultimatum set by the United States to Iran did not reassure investors.

The conflict enters its fifth week with no signs of de-escalation. Donald Trump's ultimatum to Iran, demanding a reopening of the Strait of Hormuz, failing which the country would face American strikes on power plants, has been postponed twice (on March 27th and then on April 6th). According to the United States, discussions are underway with Iran for a potential ceasefire agreement. These negotiations have been denied by Iran, and the deployment of additional American ships and troops raises concerns about an escalation of the conflict. The Brent crude oil barrel finished the week around $113.

The week was marked by the publication of the first surveys assessing the economic consequences of the Middle East war. In the Eurozone, the composite PMI index declined to 50.5 in March from 51.9 in February. Demand addressed to business leaders is moderating, and the impact of the conflict is evident through a significant lengthening of delivery times and a sharp rise in input prices. Selling prices remained virtually unchanged, with business leaders not currently passing on this increase in production costs. In Germany, the IFO index also declined due to a deterioration in expectations. In France, the business climate index remained virtually unchanged but below its long-term average. Consumer confidence indices deteriorated in France, the United Kingdom, and the United States, with the latter anticipating a decline in their purchasing power as a consequence of the sharp rise in inflation expectations. Christine Lagarde reaffirmed the ECB's vigilance regarding the risks associated with the energy shock. The central bank will not act without sufficient information on its magnitude, persistence, and propagation, but it will not remain "paralyzed by hesitation," signaling an unconditional commitment to ensuring 2% inflation in the medium term. Isabel Schnabel echoed this sentiment: the ECB should not rush in the face of high inflation but should take the time to identify the emergence of any second-round effects and long-term inflation expectation increases.

In this context, risk-off sentiment persisted. The S&P index fell by 1.9% over the week. The stability of the Eurostoxx 50 during the same period is misleading. The week was turbulent, and the index contracted by 10.3% over the month. Tensions focused on long-term rates this week, resulting in a steepening of the yield curve on both sides of the Atlantic. The German 10-year bond thus crossed the 3.12% mark in intraday trading on Friday, and the US 10-year approached 4.48%. Over a month, the flattening movement is considerable. 2-year yields increased by nearly 100 basis points (bps) in the UK, by nearly 70 bps in Germany, and by nearly 55 bps in the United States. This reflects central banks' expectations of rate hikes to curb inflation. French and Italian sovereign spreads widened by 3 bps on the week. Italy is more affected by the conflict due to its greater dependence on LNG imports. Giorgia Meloni was also weakened by the failure of the referendum on judicial system reform. Euro credit spreads widened over the week.

Aline Goupil-Raguénès

Main market indicators