Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Listen to podcast (in French only)

(Listen to) Aline Goupil-Raguénès’ and Zouhoure Bousbih’s podcast:

- Review of the week – Appointment of Kevin Warsh as Fed Chair and Eurozone S&P Global surveys;

- Theme – Indian equities: has AI put an end to the demographic dividend?

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: Indian Equities: Has AI Put an End to the Demographic Dividend?

- India’s demographic dividend (a young and abundant population) has been a key driver of growth, the expansion of outsourced services, and Indian equities;

- This model is now being challenged by AI, which threatens standardized service jobs, particularly in the IT sector;

- India faces a structural paradox: strong economic growth that fails to generate sufficient employment, resulting in a relatively weak labor market;

- The main challenge lies in employability: skills mismatches, widespread informality, and an incomplete structural transformation of the economy;

- For Indian equities, the demographic dividend remains a long-term pillar, but AI calls for a more selective approach, favoring companies capable of upgrading their business models and converting productivity gains into sustainable growth.

Indian equities: has AI brought an end to the demographic dividend?

India’s demographic dividend—i.e., the potential economic advantage stemming from a large, young, working-age population—has long been a cornerstone of the bullish case for Indian equities. The country’s youthful demographics and abundant labor supply enabled India to emerge as a global hub for outsourced services (IT, customer support, accounting, back-office operations), attracting foreign firms seeking both cost efficiency and high-quality delivery. However, artificial intelligence (AI) directly threatens these standardized service roles, which rely heavily on mid-skilled labor. The information technology sector, at the core of India’s growth model, is particularly exposed. Yet it is also the sector that has most effectively monetized the demographic dividend—driving formal job creation, supporting the rise of the middle class, and underpinning India’s economic growth. At the same time, AI highlights a deeper structural paradox in the Indian economy: strong growth that fails to generate sufficient high-quality employment. It raises a critical question for India’s economic outlook: can the country create enough higher-skilled, better-paid jobs for its demographic dividend to remain a durable asset?

An imperfect demographic dividend

The paradox of the Indian economy: strong growth that fails to generate sufficient employment.

With around 63% of its population in the working-age bracket (15–59) and a median age of just 29, India has one of the largest and youngest labor forces in the world. However, a young population alone is not sufficient: a demographic dividend only materializes if this workforce is productively employed.

Despite robust and sustained growth of around 7%, India has struggled to generate enough jobs (circa 3% YoY), reflecting a growth model primarily driven by capital-intensive sectors rather than labor-intensive industries. As a result, millions of young people remain unemployed.

The Indian labor market exhibits two key structural features.

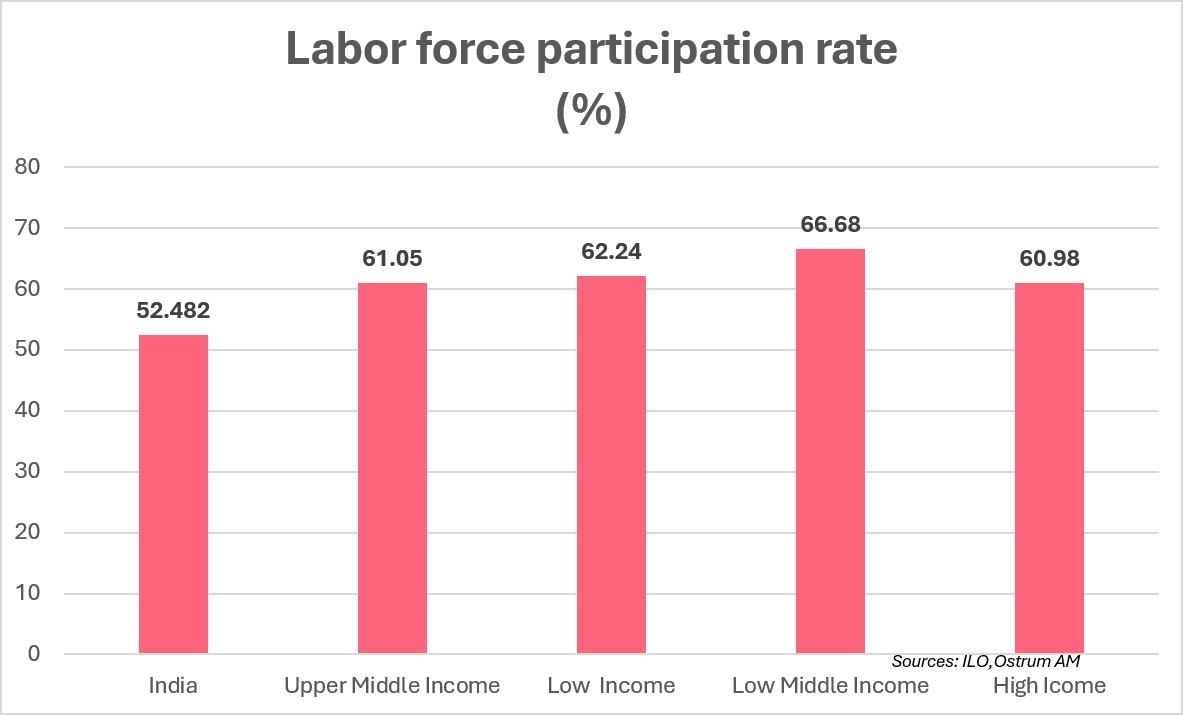

India has a labor force participation rate of around 50%, significantly below that of comparable countries.

First, labor force participation remains low, at around 50%, well below that of comparable lower-middle-income countries—India’s peer group—even at similar levels of educational attainment. Youth participation is also below global trends, pointing to an underutilized demographic dividend.

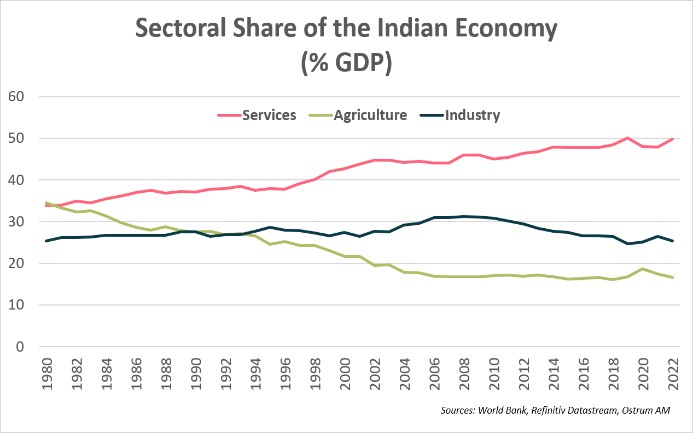

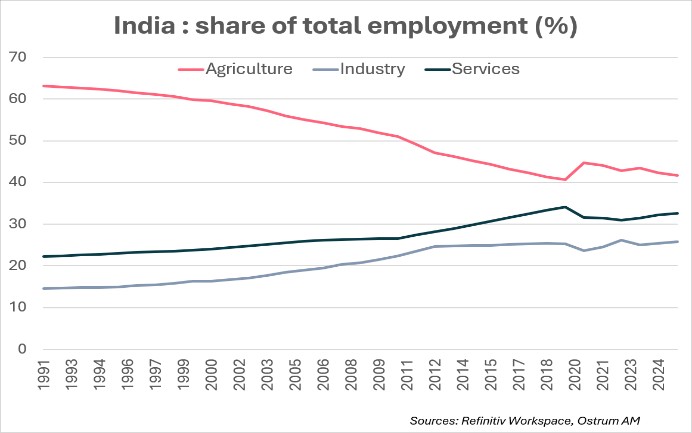

Second, India’s challenge is not merely the size of its workforce, but its employability. This is closely tied to the country’s incomplete structural transformation. Unlike the typical development path followed by emerging economies—transitioning from agriculture to industry and then to services—India has leapfrogged directly into services.

As illustrated in the accompanying chart, the services sector expanded rapidly from the 1990s onwards, following economic liberalization. Its share of GDP rose from 35% in 1980 to 50% in 2024, while industry remained broadly stable at around 25%. Although agriculture accounts for only 16% of GDP, it still employs roughly 40% of the workforce, highlighting significant underemployment. Labor reallocation has therefore largely bypassed manufacturing and shifted directly into services, reflecting the economy’s limited capacity to absorb productive labor

Services account for 50% of GDP but only 30% of total employment.

To fully harness its demographic potential, India needs to expand both manufacturing and labor-intensive service sectors. At the same time, declining labor intensity i.e., the falling share of labor in value added—further constrains job creation, a trend likely to be reinforced by advances in artificial intelligence and automation.

AI primarily threatens the very sectors that have driven India’s rise in services, with a risk of “hollowing out” the middle of the labor market

AI threatens the IT sector—the most effective channel for monetizing India’s demographic dividend.

India has established itself as a major global platform for services (communications services, customer support, and outsourcing). Yet these are precisely the types of roles where generative AI can significantly reduce the volume of repetitive tasks.

The Indian information technology (IT) sector is the most exposed. Its young, English-speaking, and technically skilled workforce has made it globally competitive. The sector generated around USD 283 billion in revenue in 2025 (+5.1% year-on-year), accounts for nearly 7.4% of GDP, and employs approximately 5.5 million people.

While the services sector represents close to 50% of GDP and over 30% of employment, the IT sector has been the most effective channel for translating this demographic potential into formal employment, supporting the expansion of the middle class and driving GDP growth.

The key risk is that AI-driven disruption may sever this link. Young call center employees and IT graduates could increasingly be replaced by algorithms. AI has the potential to displace segments of “middle-skill” jobs, leading to a polarization of the labor market—commonly referred to as the “hollowing out” of the middle.

This issue is particularly critical for India, as a large share of urban middle-class upward mobility has historically depended on these intermediate service-sector jobs, especially in export-oriented activities.

India’s real challenge: the gap between the quantity of young workers and the quality of skills

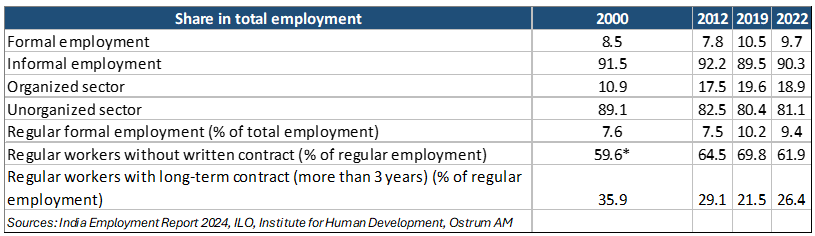

India’s challenge lies not only in the number of jobs, but also in their quality and productivity. Despite its very young population and the large influx of new graduates each year, the country’s education and training systems do not always keep pace. Skills shortages—particularly in technical and industrial areas—persist, alongside a mismatch between workforce capabilities and firms’ needs, and a high degree of heterogeneity, with a highly skilled elite coexisting with a large pool of underqualified workers. As a result, underemployment and informal employment remain elevated, as illustrated in the table below.

India suffers from a shortage of formal employment (9.4% of total employment) and a high level of informality, at around 90%.

India continues to face a shortfall in formal job creation (only 9.4% of total employment in 2022), alongside a very high level of informality (around 90% of jobs). At the same time, rising entrepreneurship—especially in rural areas—suggests that India’s demographic dividend was already only partially captured even before the AI shock. The high share of informal employment indicates that, despite their large numbers, young workers often lack the skills needed to be “employable” in modern sectors, thereby constraining industrialization, particularly the development of a competitive manufacturing base.

AI vs. the demographic dividend: substitution or complementarity?

The demographic dividend has equity value only if India invests in digital infrastructure, data, and, above all, skills.

India retains a powerful demographic foundation, with more than 65% of its population under the age of 35 and a demographic window that could extend until 2055, according to the United Nations Population Fund. This relative advantage remains rare globally, particularly in contrast to the ageing populations of China, Europe, and Japan.

Moreover, India’s labor market continues to expand in absolute terms. According to International Labour Organization data, India’s labor force reached 617 million people in 2025, representing a significant pool of consumption, housing demand, financial deepening, and growth potential for domestically oriented listed sectors

AI has the potential to enhance human capital productivity rather than fully replace it. According to the International Monetary Fund, AI could boost productivity and generate growth gains, with a potential increase in global GDP of up to 0.8 percentage points per year. India’s IT sector is expected to generate more than USD 300 billion in revenue for the first time this year, according to a Reuters article (“India IT industry surpasses $300 billion amid AI‑driven challenges, openings”), and should remain a net job creator, with 135,000 net jobs added over the referenced fiscal year.

In other words, AI may reduce specific tasks but not necessarily overall labor demand: it reshapes job content, accelerates specialization, and can enhance the competitiveness of Indian firms—provided they successfully move up the value chain.

The World Bank’s Digital Progress and Trends 2025 report emphasizes the “4Cs” of AI adoption (connectivity, compute, context, competency), implying that the demographic dividend will translate into equity value only if India invests in digital infrastructure, data, and, critically, skills.

India also benefits from structural advantages in AI adoption, including a young, English-speaking, and technically skilled workforce. According to NASSCOM, more than 2 million professionals have already received AI training, highlighting ongoing adaptation. As a result, part of the demographic dividend could shift from standardized services toward broader sectors such as healthcare, finance, logistics, data centers, and consumption.

Conclusion

Artificial intelligence has not brought an end to India’s demographic dividend, but it has fundamentally reshaped the conditions for its success. The advantage of a large and young population can no longer be viewed as a simple reservoir of abundant, low-cost labor, particularly in outsourced services. AI is automating part of these tasks and weakening the mid-skilled jobs that underpinned India’s rise in the global economy. However, it also opens a new cycle in which youth, English proficiency, STEM capabilities, and the ability to reskill become key competitive advantages. For Indian equities, the demographic dividend remains a long-term pillar but no longer justifies broad-based optimism. A more selective approach is required, favoring companies capable of translating AI into productivity gains, moving up the value chain, and delivering sustained domestic growth.

Zouhoure Bousbih

Chart of the week

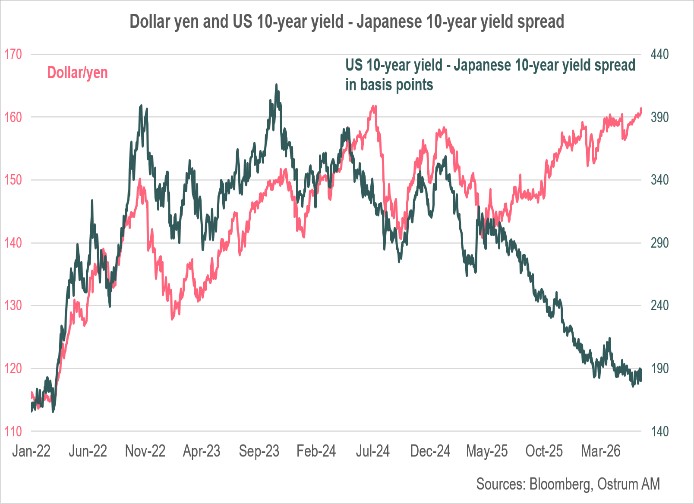

The yen closed last week at 161.3 against the dollar, approaching its lowest levels in 40 years. The Japanese currency did not benefit from the BoJ’s 25 bp rate hike, which brought the policy rate to 1%, its highest level since 1995. Monetary policy remains accommodative, however, as the BoJ is normalizing only very gradually to ensure that the economy has definitively exited the long period of deflation that began in the late 1990s. The interest rate differential between the United States and Japan remains wide, encouraging investors to favor the dollar over the yen. At the same time, the dollar appreciated against all currencies on the back of rising expectations of rate hikes by the Fed. The finance minister stated that Japan was ready to take bold measures to support the currency, suggesting that intervention could be imminent if the yen approaches the 161.95 level reached in December 1986.

Figure of the week

114

This is the word count of K. Warsh’s first statement as Fed Governor. It represents an average reduction of 60% compared to previous statements, signaling a shift in communication style.

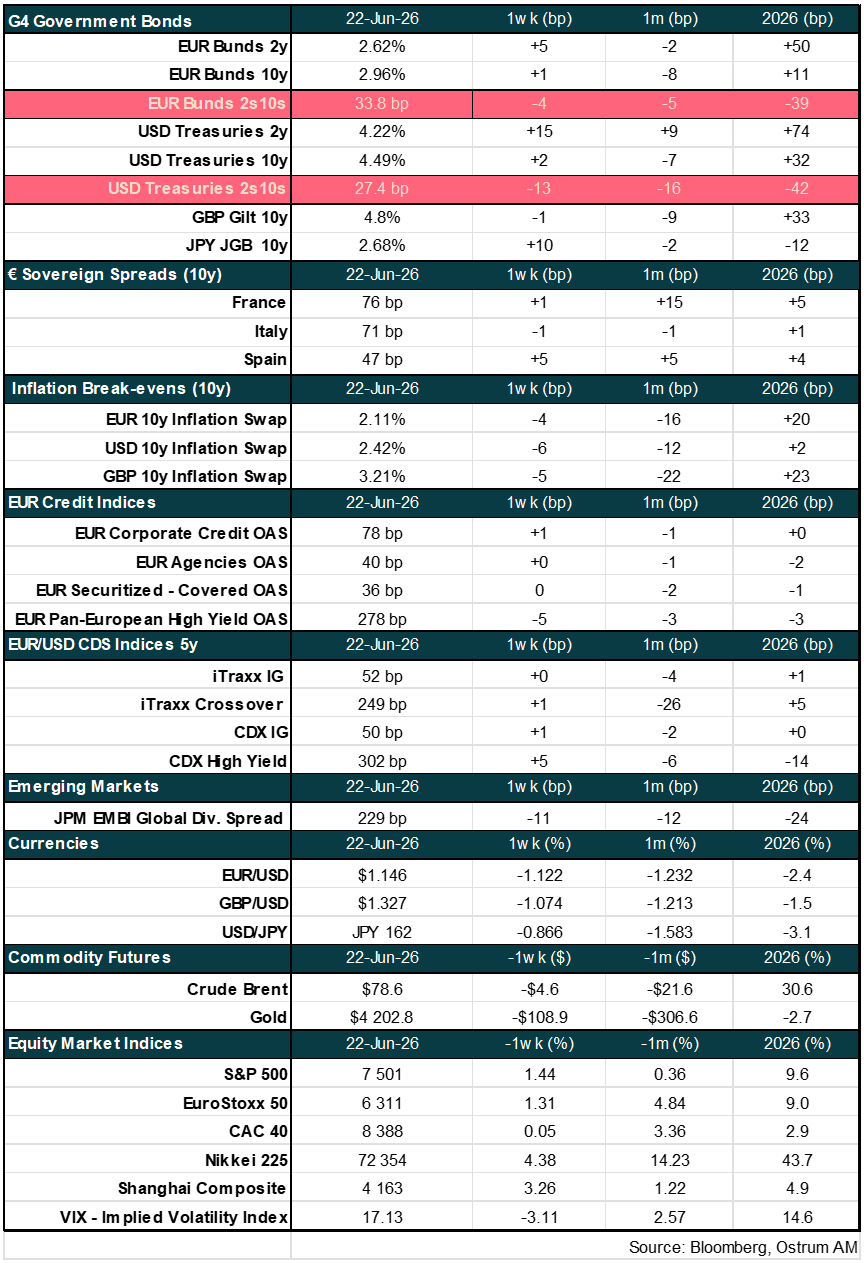

Market review: Markets caught between the Iran-U.S. protocol agreement and the Fed

- U.S./Iran: The protocol agreement leads to a decline in Brent crude prices back below $80 per barrel;

- Fed: Unanimous statu quo. Kevin Warsh scraps forward guidance and announced an overhaul of the Fed;

- Rates: Significant tensions on US short-term rates, driven by a Fed perceived as hawkish by markets;

- Equities: Markets welcome the Iran–United States agreement protocol.

Markets caught between the Iran–US protocol agreement and the Fed

Markets welcomed the prospect of a reopening of the Strait of Hormuz before becoming concerned about a Fed perceived as “hawkish” after Kevin Warsh’s first FOMC meeting.

The week began with the announcement of a framework agreement between the United States and Iran, followed by its electronic signing on Wednesday evening. This led to a decline in oil prices, with Brent briefly falling slightly below $80 per barrel, a rise in equity markets, and an easing in interest rates. However, many uncertainties remain. In a first phase, the agreement provides for a reopening of the Strait of Hormuz within 30 days. A second phase also begins upon signing, lasting 60 days and potentially renewable, focusing in particular on the challenging negotiations over Iran’s nuclear program, the unfreezing of assets held abroad, and the lifting of sanctions. A $300 billion reconstruction fund is expected to be established. By the end of the week, negotiations were delayed following Israeli strikes in Lebanon.

From Wednesday evening, the spotlight shifted to the Fed—more specifically to its new Chair, Kevin Warsh. By removing forward guidance on the future path of interest rates and emphasizing the Fed’s commitment to delivering price stability in a context of still-elevated inflation, markets perceived the Fed as more hawkish than expected. Kevin Warsh did not provide his own projections within the SEP (Summary of Economic Projections), while downplaying the forecasts submitted by individual FOMC members. Nine members expect at least one rate hike by year-end, eight foresee a pause, and one anticipates a rate cut. These highly divergent views reflect a lack of strong conviction within the FOMC. Despite PCE inflation at 3.8% in April, the decision to hold rates unchanged was unanimous. Kevin Warsh also announced the creation of five task forces aimed at overhauling the Fed. These will focus on communication, balance sheet policy, the use of and reliance on existing data sources, productivity and employment in a transformative era, and the inflation framework. Market expectations of Fed rate hikes triggered significant upward pressure on the US 2-year yield, which rose by 13bps to 4.18%, its highest level since February 2025. The US 10-year yield increased by 5bps on June 18 to 4.49%, before easing later in the week on expectations of a reopening of the Strait of Hormuz. The 30-year yield fell by 7bps over the week. In the euro area, the 2-year yield rose by 3bps to 2.65%, while the 10-year yield edged down by 1bp to 3%. The upward revision of core inflation to 2.6% in May confirmed expectations of an ECB rate hike in September. The dollar benefited from a Fed perceived as hawkish, appreciating against all currencies, notably the Brazilian real (+1.8%). The Bank of Japan’s 25bp rate hike failed to support the yen, which weakened past the 160 level, raising the prospect of intervention. Equity markets moved higher, supported by hopes of a reopening of the Strait of Hormuz and gains in technology stocks: +1.4% for the S&P and +1.7% for the Euro Stoxx 50.

Aline Goupil-Raguénès

Marchés financiers