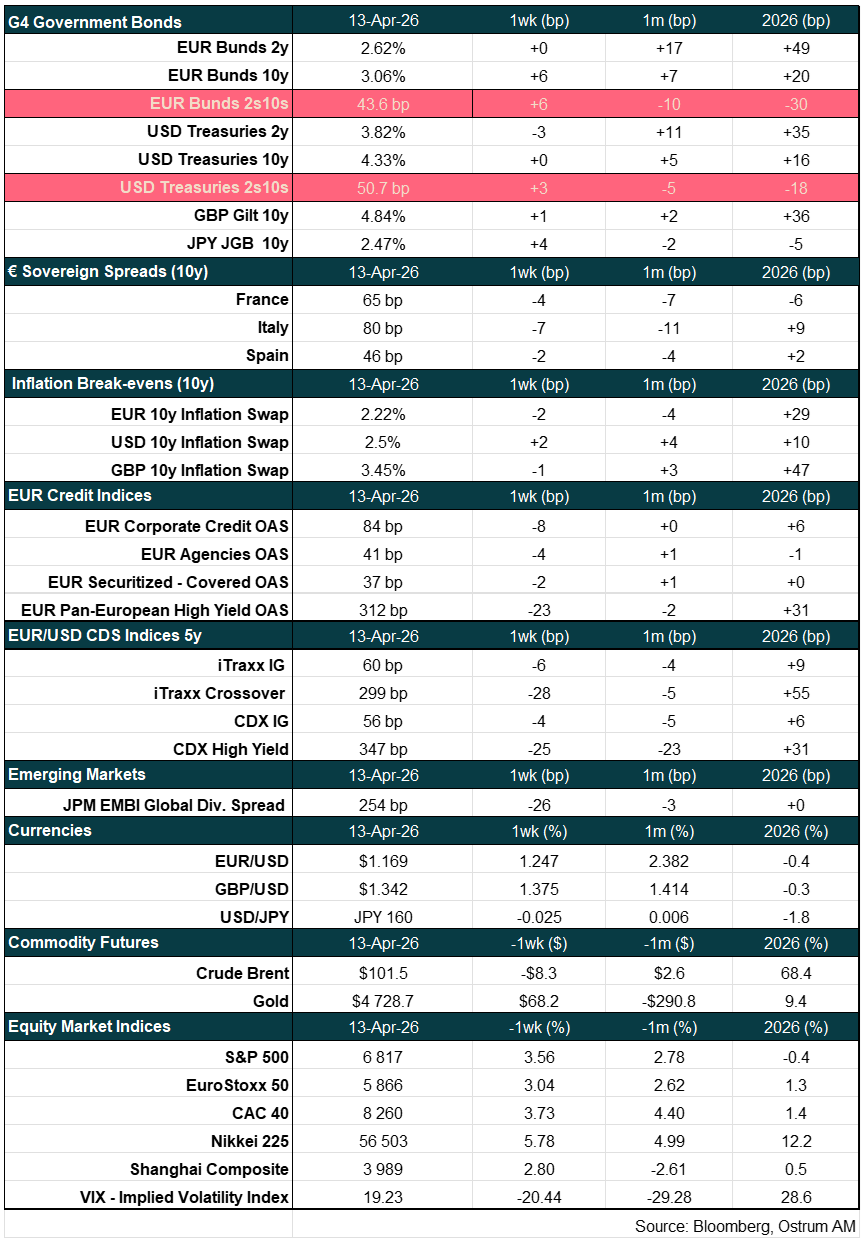

Read our market review and find out all about our theme of the week in MyStratWeekly and its podcast with our experts Axel Botte, Aline Goupil-Raguénès and Zouhoure Bousbih.

Summary

Listen to podcast (in French only)

(Listen to) Axel Botte’s podcast:

- Review of the week – Markets up despite US-Iran tensions, US growth and inflation;

- Theme – Eurozone stocks show resilience.

Podcast slides (in French only)

Download the Podcast slides (in French only)Topic of the week: European stocks show resilience amid the oil shock

- The Iran conflict initially caused significant European stock market declines, but markets quickly rebounded following ceasefire talks, indicating resilience.

- Despite an oil shock, the energy crisis in the Eurozone was less severe than anticipated due to diversified imports and French nuclear power; equity performance depends on firms passing on input costs.

- While overall earnings forecasts remain upbeat (+9% expected growth), cyclical sectors face downward revisions, with oil & gas seeing significant upgrades (+24%).

- Growth vs. Value: Rising long-term interest rates pressured growth stocks, while value stocks, sensitive to current conditions, might benefit if the crisis abates and risk premiums decrease.

- Eurozone equities attracted substantial monthly inflows into ETFs averaging €1.2 billion, and increased M&A activity, particularly in mid- and small-caps, is providing further support.

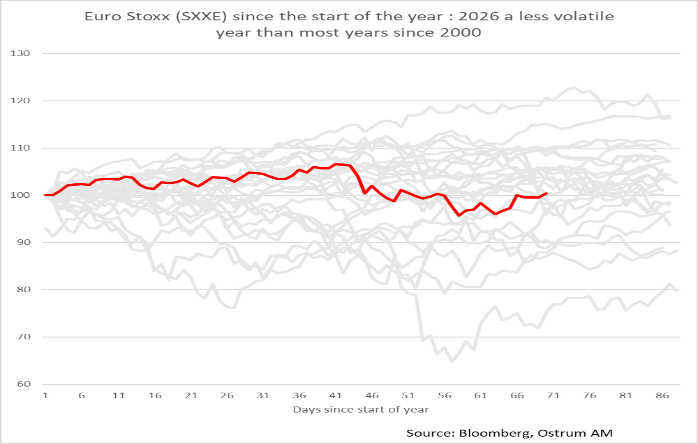

Euro area stocks decline upon start of Iran war

The war in Iran caused a 10% decline before markets found a floor.

In a challenging context, Euro area equities started the year 2026on a strong footing. The Euro Stoxx index, representing the 300 largest companies in the euro area, had a strong start of the year gaining 6.7% in January-February before the war on Iran started on February 27th. To be fair, European equity markets could have been much weaker given the geopolitical backdrop including crises in Greenland, Venezuela and now Iran. Since the start of the war in Iran, the euro area stock gauge wiped out earlier gains before the announcement of a two-week ceasefire sparked a sharp rebound that appears traceable to short covering flows.

Comparing the 2026 stock price path with the past 25 years, the euro stock market performance appeared remarkably benign even before the ceasefire. The range of year-to-date price returns is well within prior years’ extremes with a maximum drawdown of just -4.3%.

An oil shock, rather than a broad energy shock

Oil prices are under pressure, but natural gas and electricity have remained stable.

The significant shock to energy prices took a toll on equity prices, yet the market drawdown has been manageable. Likewise economic surveys available for March have shown resilience even as euro area firms have begun reporting higher input costs. Energy imports make up about two-thirds of energy use in the euro area (according to World Bank data). In 2022, the Russian invasion of Ukraine had caused unprecedented disruption in gas supply from Russia, a sharp rise in crude prices and thus skyrocketing electricity prices (most notably in Germany). This time around, the increase in gas prices has been less pronounced with highs around 50 €/MWh compared with repeated spikes above 200 €/MWh four years ago. Imports from Qatar. Coal prices, which dictates the marginal cost of electricity in parts of Germany, have also barely budged. Consequently, the oil crisis did not spill over into a full-fledged energy crisis. A recovery in nuclear electricity production in France played a role in cushioning against higher imported energy costs.

.png)

Stability in equity performance will depend on the ability of firms to pass on increased input costs. As it stands, the outlook for earnings remains quite upbeat. The Bloomberg consensus estimate for 12-month forward EPS for the Euro Stoxx index stands at 41.94 in index point terms, implying a 15.7% growth from current the trailing EPS. Consensus earnings expectations may look somewhat stretched and may not fully factor in the impact of the Iran war. Our earnings forecast point to a more moderate 9% growth this year.

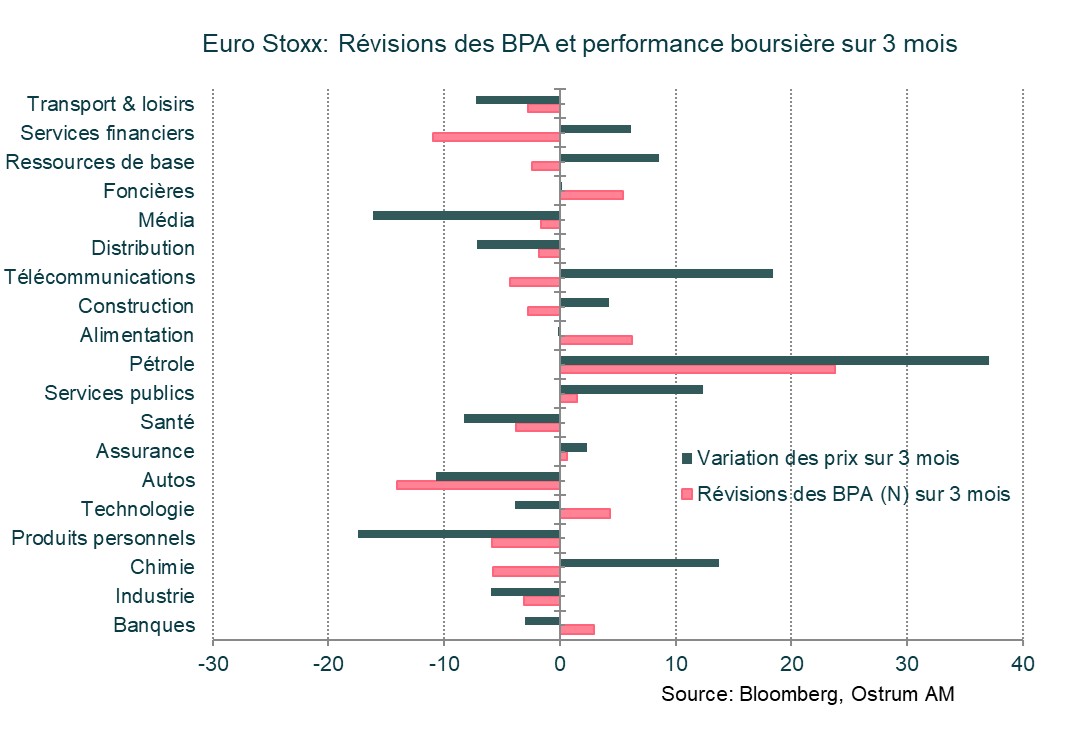

Modest EPS revisions ahead of the earnings season.

Over the past 3 months and heading into the earnings season, there have been some downward revisions to earnings forecasts. Cyclical sectors have been hit hardest. Earnings for auto companies have been revised down by around 15%, with chemicals, industrials and consumer products seeing 3 to 6% cuts in EPS estimates. Conversely, the oil and gas sector enjoy sharp upgrades in profit expectations (+24%). Food companies, banks and technology firms also record more modest upgrades to their EPS outlook. As can be seen in the chart opposite, the 3-month stock performance is not always aligned with the recent adjustments to the EPS forecasts.

Domestic revenue exposure, seen in sectors like financials and utilities, is also a boon in the troubled international environment. Indeed, European companies with high sales exposure to continental Europe have declined far less since the war started than stocks with a higher proportion of international revenue.

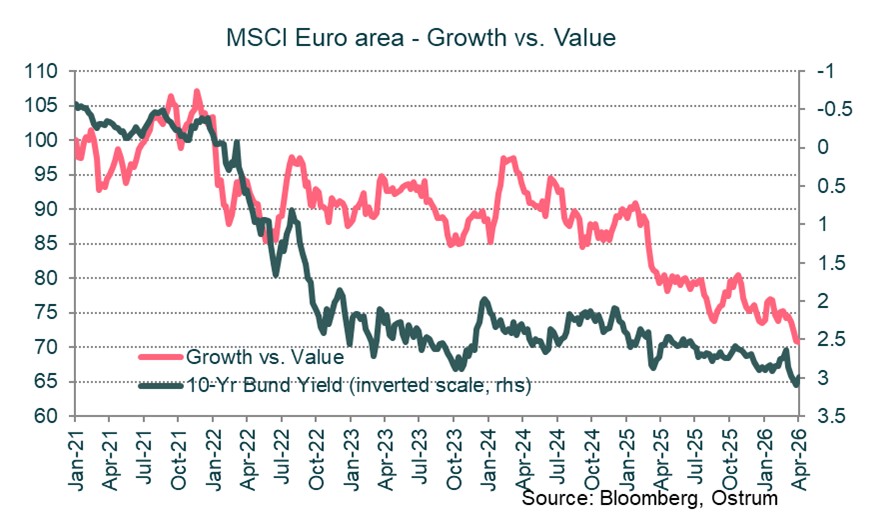

Will Growth stock underperformance come to an end?

If Bund yields stabilize near 3%, growth stocks may recover some ground.

Growth stocks trade at higher price/earnings multiples as stock prices must reflect expectations of earnings growth far out into the future. Thus, growth stocks tend to be more responsive to changes in long-term interest rates. By contrast, value stocks tend to trade at a discount and are extremely sensitive to current economic conditions and their near-term outlook for earnings. Therefore, growth stocks have a tendency to underperform when long-term interest rates are under upward pressure. The Iran crisis sparked an inflation scare pressuring 10-Yr Bund yields higher towards 3 %. If and when the crisis abates, the risk premium on long-term bonds will likely diminish which could reverse the underperformance of growth stocks vs. value.

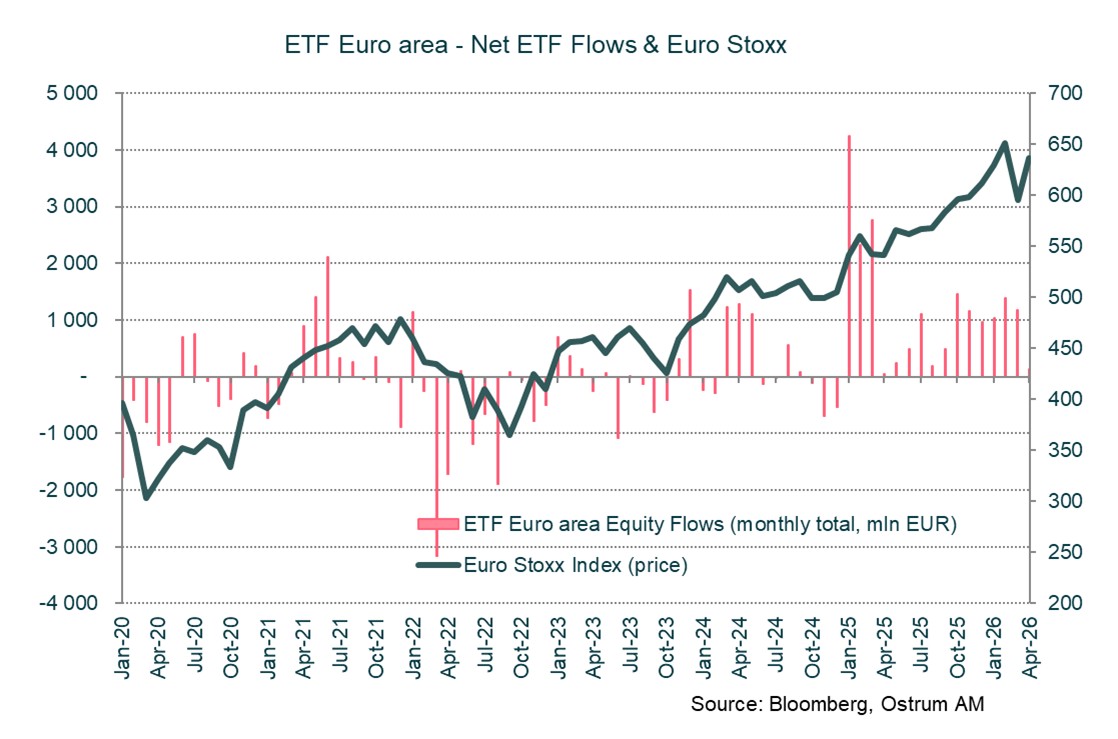

Euro area equities in high demand

Solid flows into euro equity funds.

Euro area stocks appear to be in good demand despite the energy hit to activity. We have constructed a sample of euro area equity exchange-traded funds. The flow data is available on a daily basis. The chart below shows monthly flows from January 2020 (and month-to-date flows as at April 10th, 2026). In the 6 months to March 2026, net inflows have averaged €1.2 billion a month in our sample of euro area equity ETFs with assets under management of €1.4 trillion. Net inflows are roughly equivalent to 0.1% of AuM per month. The return of Donald Trump to the White House has coincided with a sharp upturn in euro area equities inflows.

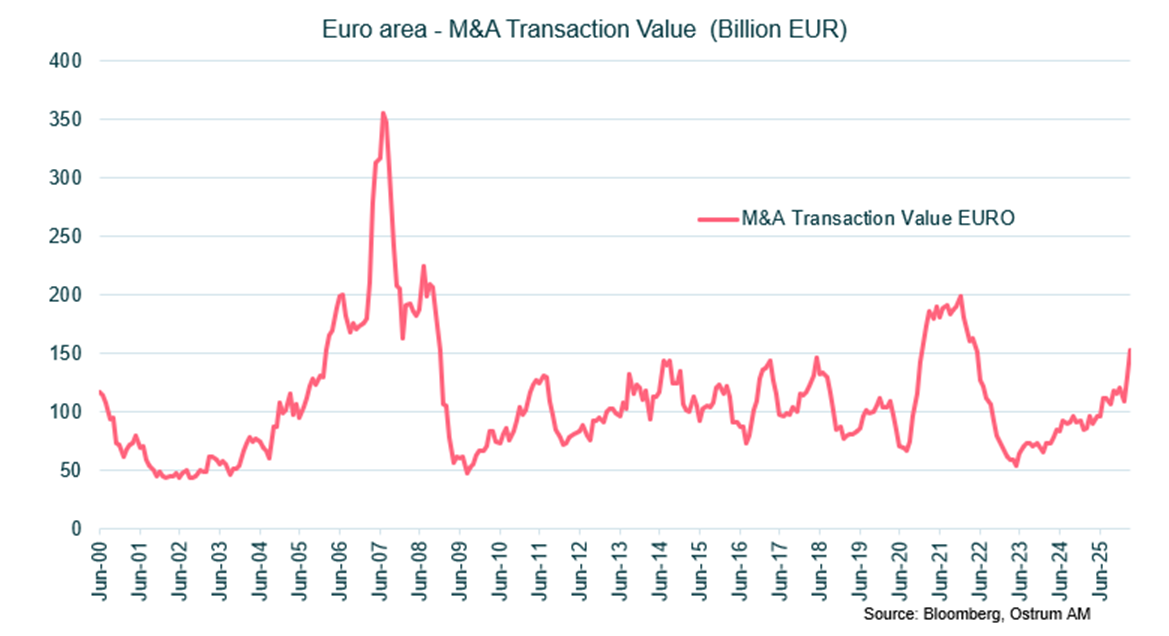

Mergers and acquisitions are accelerating, possibly explaining the strong performance of mid-cap stocks and supporting European equities. After years of limited private equity activity in small and mid-caps, M&A is now increasing in the euro area—and even more so in the U.S.

Conclusion

European equities had a strong start of the year gaining more than 6% in two months before the Iran war began. The war represents a significant economic shock and sparked a 10% decline in euro area stocks, but equity markets quickly bottomed out and rebounded as soon as talks to end the war were announced. Euro area equities continue to attract flows amid modest downward revisions to earnings. Furthermore, increased M&A activity may boost demand, supporting further stock market gains.

Axel Botte

Chart of the week

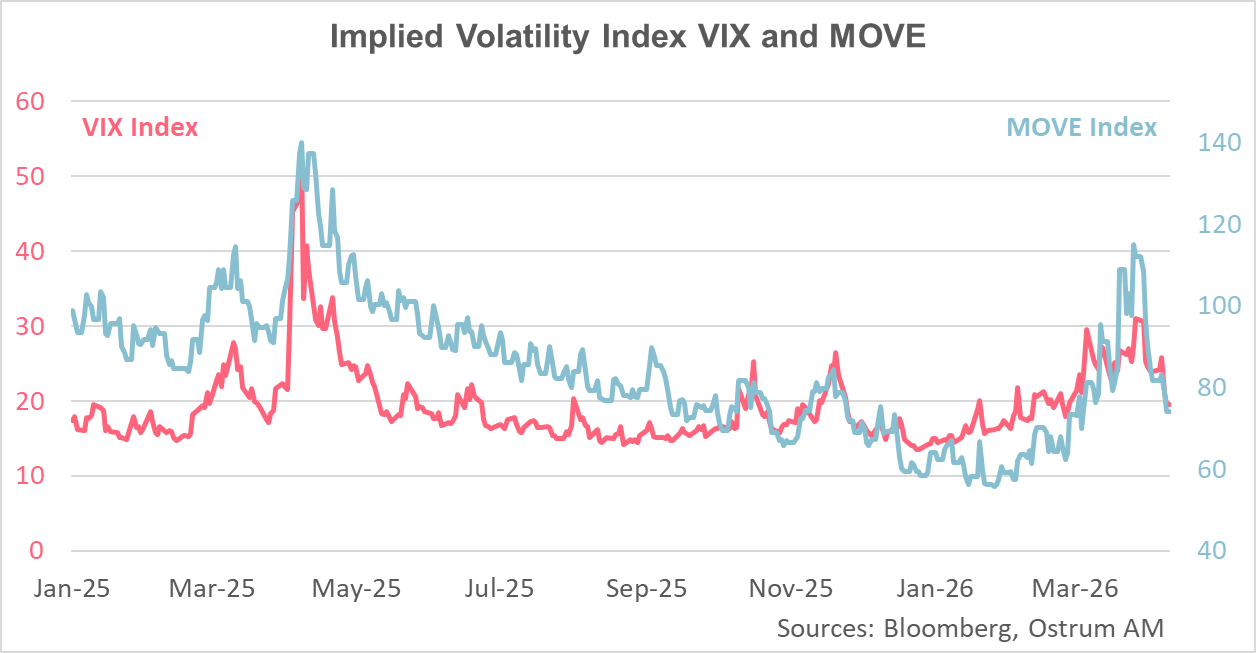

Before the Iran war that began in late February, volatility had been on the rise from the low levels seen in January. The US equity implied volatility represented by the VIX index rose from about 15% to a high at 30% at the end of March.

In bond markets, volatility also increased as higher oil prices sparked a rise in short-term inflation expectations. As result, Fed rate cuts have been priced out. However, in both equity and bond markets, the pikes in volatility has been much more muted than feared given the magnitude of the crisis in the middle east.

Figure of the week

600

Saudi Arabia’s press agency said the nation’s production capacity has been cut by around 600,000 barrels a day due to attacks on energy infrastructure.

Market review:

- Iran-US: Talks Collapse, Prolonging Uncertainty;

- US: Q4 Growth Revised Lower, Inflation Rises to 3.3% in March;

- Equities: Strong Rebound on Talks Announcement Before Difficult Week's End;

- Bonds: T-note yield Reverts Towards 4.30%, as Bund yields Drifts Higher.

Defiance Lingers

A surge in market sentiment earlier this week, sparked by announcements of talks between the US and Iran aimed at de-escalating conflict, could be in jeopardy. The initial negotiations, brokered over the weekend by Pakistan, have reportedly failed, reigniting fears of a resurgence in oil prices and a possible sell-off in equities.

Financial markets had been eager to embrace the narrative of a breakthrough accord. However, the deeply entrenched and diametrically opposed demands of both parties, particularly concerning Iran's nuclear program, proved insurmountable. While this setback may not signal a definitive end to diplomatic overtures, it is likely to prolong uncertainty and re-intensify oil market tensions. This is underscored by escalating rhetoric from Washington, with Donald Trump now reportedly threatening to blockade Iran and the Strait of Hormuz. Adding to the pressure, Saudi Arabia has quantified the impact of recent Iranian strikes on its production capacity, estimating a loss of 600k barrels per day. The restoration of output across the Gulf region is expected to be a protracted process. This environment is likely to maintain the binary behavior of markets, with oil, short-term rates, and the dollar moving in opposition to risk assets.

On the macroeconomic front, US growth figures have been revised downwards, with fourth-quarter expansion now pegged at a modest 0.5%. The weakening in private consumption towards the end of 2025 has persisted through February. The US economy continues to be driven by AI-related investments, with shipments of capital goods representing the sole bright spot so far in 2026. Real disposable income for US households has been stagnant since last spring, with the wealth effect no longer sufficient to offset moderating wage growth and a slowdown in hiring. The March CPI registered an annual inflation of 3.3%. While energy prices saw a sharp increase of 10.9%, core inflation, at 0.2% month-on-month, proved somewhat less robust than anticipated. In the euro area, March surveys indicate a degree of corporate resilience. The bloc's composite PMI stood at 50.7, buoyed by a rebound in services in Spain and, to a lesser extent, in Germany

Financial markets had priced in an optimistic scenario of a crisis resolution, only for this pricing action to soften as negotiations approached. The initial rally in equities was driven by short covering, amplified by the retreat in oil prices which, in turn, led to a decline in inflation expectations, expected monetary tightening, and, broadly, reduced credit risk premia. In US Treasury markets, positioning surveys suggest investors remain largely neutral around the 4.30% level for the T-note (closing at 4.32% on Friday). However, Bund yields have edged higher, surpassing the 3% mark. The ECB's rhetoric has hardened, now signaling rate hikes, a prospect already largely priced in by investors. Nonetheless, the robust survey data has facilitated a narrowing of sovereign spreads. Moody's has affirmed France's Aa3 rating with a negative outlook, while acknowledging a recent improvement in public finances, with the deficit revised to 5% of GDP from a projected 5.2%. French OATs traded at a spread of 67 bps over Bunds on Friday evening. Euro credit spreads are trading at 70 bps versus swaps (-8 bps), marginally wider than at the onset of the war. CDS indices have tightened, mirroring the rebound in equity indices. The S&P 500 has gained 3.6%, ahead of the start of the earnings season. US earnings are being revised upwards, with Q1 expectations hovering around +15%. European stocks posted weekly gains of 3%.

Axel Botte

Main market indicators