Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum’s views on the economy, strategy and markets.

The CIO Letter

Central banks willing to cut

The communication from Central Banks helped to realign market expectations towards a scenario of rate cuts more in line with growth and the risk of persistent inflation. Price inertia remains the main obstacle to a faster pace of easing. Monetary relief should take a more concrete form with a likely reduction in the Fed's quantitative tightening soon. US growth is in line with potential. In the euro area, surveys show an improvement despite the protracted recession in Germany. The absence of fiscal stimulus is holding back growth in Germany. China will once again aim for growth of 5% in 2024, betting on an ambitious new industrial policy.

As inflation surprised upwards, long-term rates returned to around 4.30% on the T-note and 2.50% at their highest on the Bund. These levels have revived the interest of investors so that 10-Yr yields hover about 4.05% and 2.25% respectively. The swap spread remains at its lowest around 35 bp, a sign of a low risk aversion. We observe a generalized narrowing in sovereign spreads. Italy is trading at 135 bps, its tightest level since Russia invaded Ukraine.

The market environment remains very favorable for risky assets. Volatility is remarkably low in stocks, credit or currencies. Equity markets are showing gains of 5 to 10% in 2024. However, earnings are slipping. At the same time, the tightening of credit spreads is fading somewhat but the absence of issuance premiums still indicates excess demand for the asset class. As a result, the high yield market is outperforming thanks to the low default rate in Europe.

Economic Views

Three themes for the markets

-

Monetary policy

Market rate expectations now seem better aligned with the policy stance of central banks. However, the Fed is expected to provide monetary relief by downsizing quantitative tightening in the near future. The ECB remains attentive to the evolution of wages which still seems inconsistent with a lasting return to price stability. China is pursuing a monetary easing policy while the BoJ could end its negative rate policy in March or April.

-

Inflation

Inflation is resisting monetary tightening. In the United States, inflation decelerated somewhat to 3.1% in January. Core inflation has stabilized at 3.9% since October, due to high shelter costs. The PCE deflator is however close to the target at 2.4%. In the euro area, inflation has slowed to 2.6% according to the February flash estimate. Core inflation remains above 3%. Conversely, in China, inflation remains very low. The fall in food prices continues.

-

Growth

The global manufacturing sector is showing signs of recovery at the start of the year. The US economy is close to its potential in Q1. The euro area is finally emerging from a prolonged period of stagnation. Surveys describe an improvement since the beginning of autumn. In China, activity is stabilizing, thanks to the service sector and a rebound in exports helped by a weak yuan. Japan and the United Kingdom are growing modestly.

Key macroeconomic signposts : United States

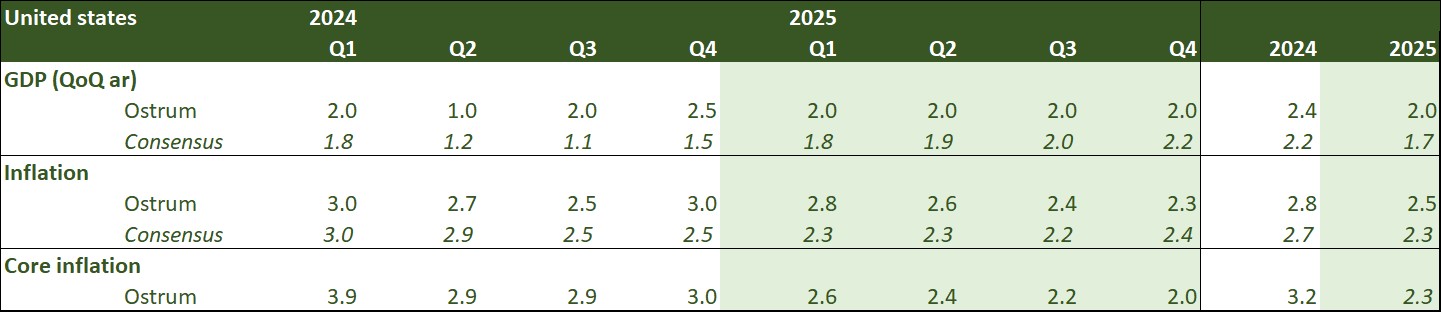

- US growth remained strong at the end of the year with 3.2% growth in the 4th quarter. Consumption and public spending support demand. Investment (equipment, R&D) is up slightly. GDP expansion in the 1st quarter should be around 2%. At the end of February, the Atlanta Fed GDP growth nowcast estimate was 2.1% in 1Q 2024.

- The federal deficit remains under discussion but is expected to be around $1,600 billion in 2024. There is still a risk of a government shutdown in late March. The Republicans killed the budget bill in the Senate arguing that it did not provide sufficient funds for securing the Mexican border. Immigration will be the main issue of the November Presidential election.

- The risks of financial crisis appear contained. Household balance sheets remain healthy. Be careful, however, with the poorly regulated non-banking sector. The NYCB episode is a ripple from the Signature Bank event and not a harbinger of a banking crisis.

- The unemployment rate remains below its equilibrium level (4-4.5%). The Fed would probably “like” to see unemployment rise towards 4.5% to ease wage pressures. The increase in the active population is, however, a boon for the economy.

- Disinflation continues but is bumpy. Underlying inflation should hover about 3% at the end of 2024. Housing and energy are two key items for inflation, but the Fed will focus on the PCE deflator which has a lower weight on housing. The Fed will also facilitate the refinancing of the Treasury.

Key macroeconomic signposts : Euro area

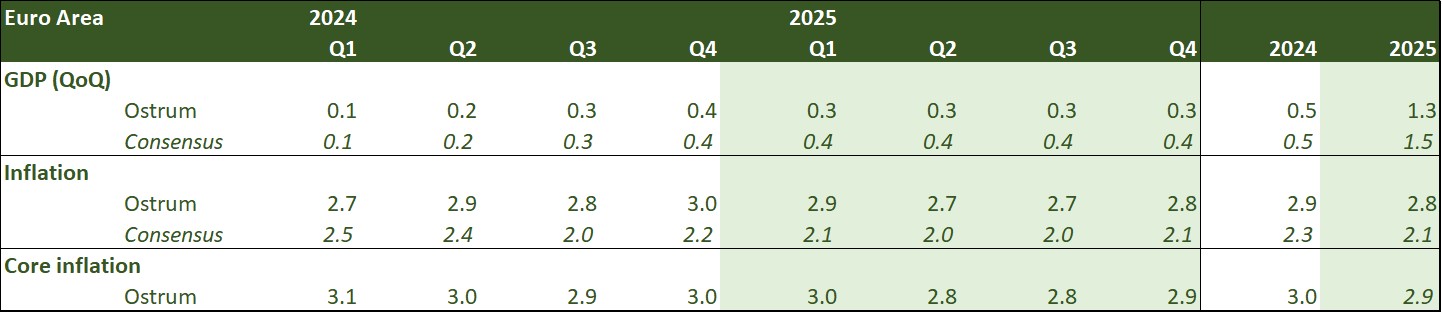

- After sluggish growth in 2023, a timid recovery should begin in the Euro zone in the first half of 2024 and strengthen in the second.

- This is perceptible through the improvement of surveys carried out among business leaders. This is linked to peripheral countries, Spain and Italy in particular, which are benefiting from an increase in their order books.

- France, on the other hand, has not found a source of impetus and Germany remains penalized by the consequences of the energy shock and its strong past dependence on Russian energy as well as by the disappointing growth of China which is weighing on its exports.

- Households will benefit from an increase in their real income given the fact that wages are expected to continue to grow at a sustained pace in a context of more moderate inflation. Combined with the maintenance of a robust labor market, this will support consumption.

- Internal demand should also benefit from a monetary policy that will become less restrictive and exports from a strengthening of world trade.

- On the other hand, fiscal policy will not support growth. After being suspended since 2020, the budgetary rules were reinstated at the start of the year and a reform was adopted.

- Inflation will no longer benefit from the strong negative contribution of energy prices, governments will stop measures aimed at containing the rise in energy bills and wages should continue to increase at a sustained pace. In a context of falling productivity, company margins will have an essential role to play in partly absorbing wage costs.

Key macroeconomic signposts : China

- The first meeting of the C.P.C., under the leadership of Premier Li Qiang, set the growth target for 2024 at 5% as in 2023.

- The Chinese authorities should therefore accelerate the country’s economic transformation towards better growth. The "3 new industries" electric vehicles, batteries and solar energy, which contributed 8% of GDP last year, must quickly replace the real estate sector that contributed to ¼ of China’s growth.

- For 2024, we expect growth of about 5%, above consensus expectations, as we believe the policy mix should support activity. The negative contribution of the real estate sector is also expected to be more limited than in 2023.

- The real estate sector is showing signs of stabilization. The authorities should continue to reduce financial pressures on the sector.

- Monetary policy took an accommodative turn at the beginning of the year, reflecting the surprise 50 bps fall in the reserve requirement rate to 10% and a 25 bps drop in the 5-year prime rate to support the real estate sector. We expect a further reduction in the reserve requirement rate in the second half of the year to boost growth in the middle of the US election.

- Fiscal policy should manage local government debt risk in coordination with monetary policy. On the other hand, the focus will be on social protection spending by targeting low-income households in rural areas to allow families to settle in cities. Orderly urbanization should support consumption.

- Inflation (0.7% in February) probably hit a low point, not a short-term problem. The 2024 inflation target was maintained at 3% to anchor inflation expectations; however, 3% is more of a ceiling than a target.

Monetary Policy

Towards a rate cut by the summer from the Fed and the ECB

- The Fed is not far from being confident enough to cut rates

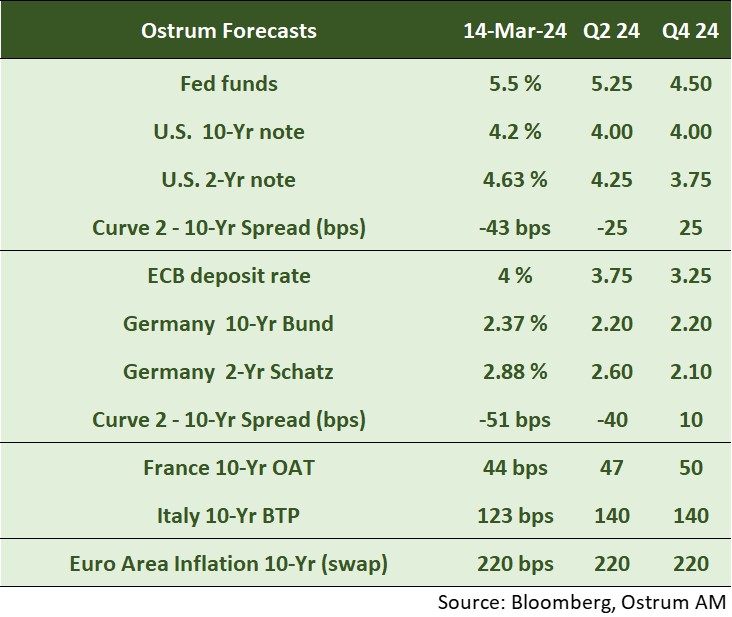

During his semiannual speech to Congress, Jerome Powell reiterated the remarks made at the end of the January 31 meeting. The Fed must become even more confident of the sustainable convergence of inflation towards the 2% target to make its monetary policy less restrictive. During the press conference, he indicated that the Fed was not far from having reached this level of confidence. This is consistent with our scenario of a first rate cut in May which should be followed by 3 others over the rest of the year. The Fed should probably announce at the March 20 meeting the terms of a reduction in the pace of contraction of its balance sheet (QT) to pave the way for rate cuts. - The ECB awaits wages and company margins for the 1st quarter

The ECB left its rates unchanged for the 4th consecutive time in March, indicating that it needed to be more confident in the disinflation process at work. Despite continued pressure on domestic prices, mainly linked to wages, the ECB has revised its inflation outlook downwards, especially for 2024, to 2.3%, compared to 2.7% forecast in December and 3.2%. % in September. The ECB is not expected to lower its rates before June in order to have the results of the spring wage negotiations and to assess the extent to which companies are absorbing part of the increase in wage costs within their margins. We anticipate 3 key rate cuts over the year. At the same time, the contraction of the balance sheet will accelerate from the 2nd half of the year, with the Central Bank reinvesting only half of the PEPP payments from July (at the rate of 7.5 billion euros on average per month) before ending it at the end of 2024.

Market views

Asset classes

- US rates: the Fed looks committed to lower rates despite inflation. The effective start of the easing cycle should bring T-note yields down to the 4% area.

- European rates: the Bund rose slightly beyond our short-term yield targets. The end-of-year target is 2.20%. The yield curve is expected to steepen.

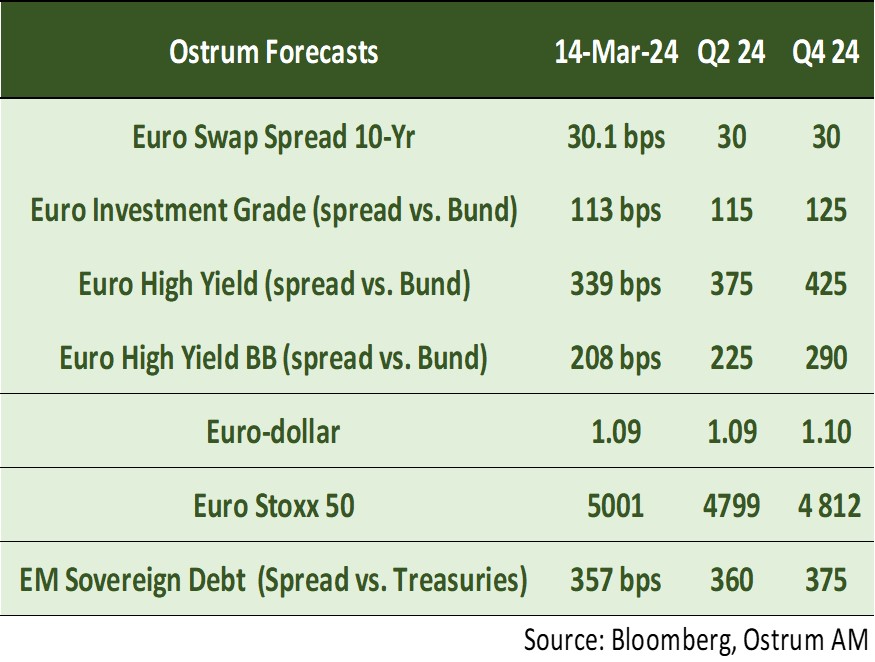

- Sovereign spreads: spreads have tightened sharply. Italy and France are trading below their equilibrium levels, but offer relative value against swap.

- Eurozone inflation: breakeven inflation rates are close to central bank targets.

- Euro credit: swap spreads keep tightening through our target levels, as the shortage of collateral has been reduced thanks to quantitative tightening. IG credit should syabilise after a strong start of year.

- Change: the euro has depreciated towards $ 1.09. The euro exchange rate is trading with a tight range under $ 1.10.

- Equities: sharp gains since the start of the year should wane somewhat as margins level out. Higher PE multiples will mitigate the downside.

- Emerging debt: emerging market spreads participated in the global rally. Consolidation around 360 bp appears overdue.

Ostrum Perspectives March 2024

Download Ostrum Perspectives March 2024