Illustration with Ostrum AM’s Climate and Social Impact Bond strategy

Impact finance is gaining momentum. It is also now more structured, benefiting from French and European frameworks, standards and definitions. Although there may still be a lack of uniformity across asset managers, the trend is in place for greater transparency.

Investors are signalling they want more alignment between goals, assets and savings, aspiring to invest for a positive impact on the environment. That said, these goals cannot be achieved at any price. We cannot transition to a lower carbon economy by creating insecurities. We must transition in an inclusive manner. Based on thinking about consequences, the principle of a “Just Transition” emerged, fair and equitable.

Ostrum Asset Management’s (Ostrum AM) Climate and Social Impact Bond strategy is an investment solution that seeks to finance a “Just Transition”. The objective is to transition to a low-carbon economy, by being respectful of the environment and its biodiversity, while being socially and regionally inclusive.

Ostrum AM has a defined impact investment policy, inspired by different initiatives in France and in Europe. The approach relies on the three recognised principles that define impact investing: intentionality, additionality and measurability. The selection process relies on demanding in-house ESG policies, in-depth proprietary credit research and a dedicated team of sustainable bonds analysts. Ostrum AM’s experts have developed proprietary methodology to select issuers with a recognized track record for social and territorial considerations and instruments that finance projects that will make a viable contribution to a “Just Transition”. Ostrum AM’s Climate and Social Impact Bond strategy respects SFDR Article 9 guidelines with ambitious targets to finance the “Just Transition".

Introduction

Both Sustainable Finance and Impact Finance have developed rapidly over the past few years. Momentum has come from investors’ shifting decision making to take into consideration how the public and private sector stand up in terms of achieving the United Nations 17 Sustainable Development Goals (SDGs). This ambition was raised further with goals set under the 2015 Paris Agreement, which highlighted the need to limit the rise in temperature to 1.5°C above preindustrial levels. The COP28 symposium (December 2023), is a new occasion to assess the progress made towards achieving these goals. This meet-up provides a “global stocktake”, and an opportunity to identify the gaps.

Institutional investors have also been a big driver of growth in sustainable and impact finance by adding more social aspects and targets to their Corporate Social Responsibility (CSR) policies.

Ostrum AM, one of Europe’s leading asset managers for institutional investors, is committed to supporting its clients in their sustainable investments and their impact goals.

1. Definition of impact finance

With environmental issues and social concerns more prevalent, impact investing provides a means of channelling money to viable projects that are backed by sustainable economic growth plans. Various marketplace workgroups collaborated on a framework to clearly define impact investing.

In September 2021, the Paris Sustainable Finance Institute (previously Finance for Tomorrow) workgroup proposed the following definition: “impact finance is an investment or financing strategy that aims to accelerate the just and sustainable transformation of the real economy, by providing evidence of its beneficial effects”1. The definition is based on the three founding principles of impact finance, recognised by the market, and grounded in the France Invest and French SIF framework: intentionality, additionality and measurability.

This three-fold definition sets a basis for asset managers to define their impact assets, for which they must provide clear and transparent communication.

2. Ostrum AM’s Global Sustainable Transition Bonds strategy: how is it an impact investment?

Ostrum AM’s Climate and Social Impact Bond strategy invests in sustainable bonds: green bonds, social bonds, sustainability bonds and sustainability-linked bonds issued by public and private sector issuers. The strategy adheres to Ostrum AM’s demanding ESG policies (sector policies, exclusion policies and controversy management policies). The investment team selects instruments based on in-depth credit research analysis, relying on a dedicated team of sustainable bonds analysts and proprietary methodology and scoring (Sustainable Bonds Score, Just Transition Indicator). The objective is to select instruments that are financing projects that will make a viable contribution to a just transition.

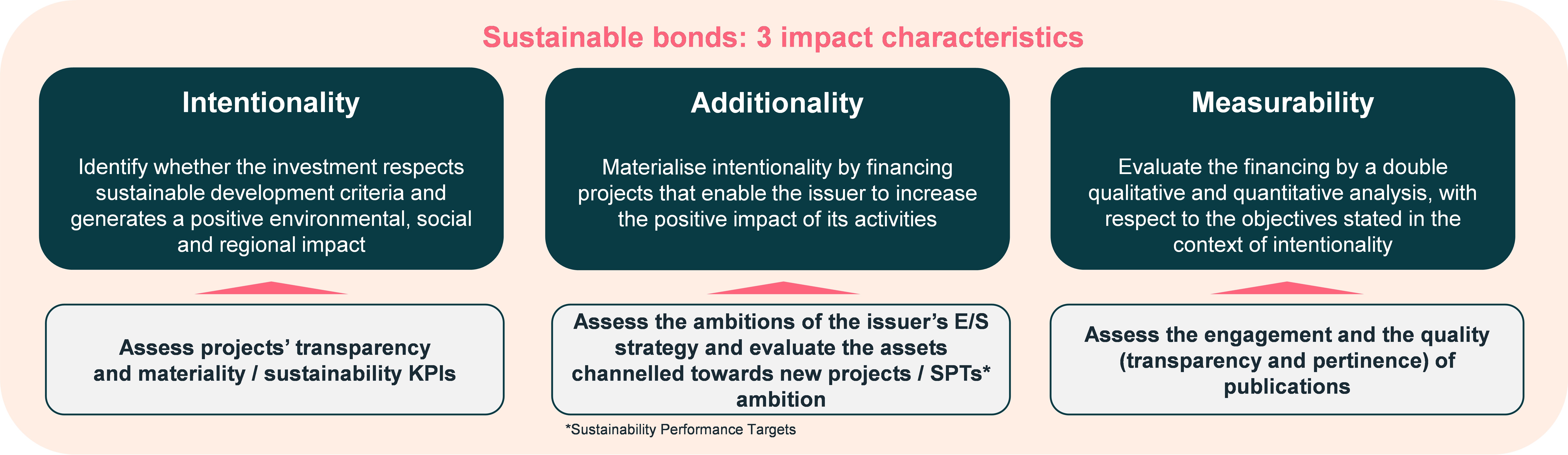

The selection process, particularly the Sustainable Bonds Score, ensures that instruments selected meet requirements for intentionality, additionality and measurability.

- Intentionality: Do the projects to be financed respect sustainable development criteria and that the projects will generate a positive environmental, social and regional impact? Ostrum AM qualifies intentionality by assessing the transparency and materiality of the projects.

- Additionality: Do the projects financed create value add? Ostrum AM assesses additionality by analysing the ambitions of the issuer’s E/S strategy and by evaluating assets channelled towards new projects or towards capex development.

- Measurability: How is the impact of the projects financed measured and reported (qualitative/quantitative outputs)? Is this measurability aligned with the objectives stated in the context of intentionality? Ostrum AM assesses measurability through engagement with issuers and analysis of reports and publications, seeking to identify impact quality (transparency and pertinence).

Ostrum AM developed proprietary sustainable bond analysis methodology, applied at issuer and project level, adapted by instrument type with a dedicated dashboard for each instrument. Indicators (see Appendix 1) are adapted to identify intentionality, additionality and measurability.

In addition, Ostrum AM takes into consideration public information sources: Second Party Opinions (documents produced by ESG data service providers indicating alignment of bonds with the ICMA Bond Principles), presentations to investors which are forums where issuers provide information on sustainable bond issues, and issuers’ websites (annual and non-financial reports), data providers and other independent third-party sources, including NGOs.

3. How to ensure intentionality?

Intentionality is assessed through an analysis of transparency, and the materiality of projects and sustainable performance indicators (E/S).

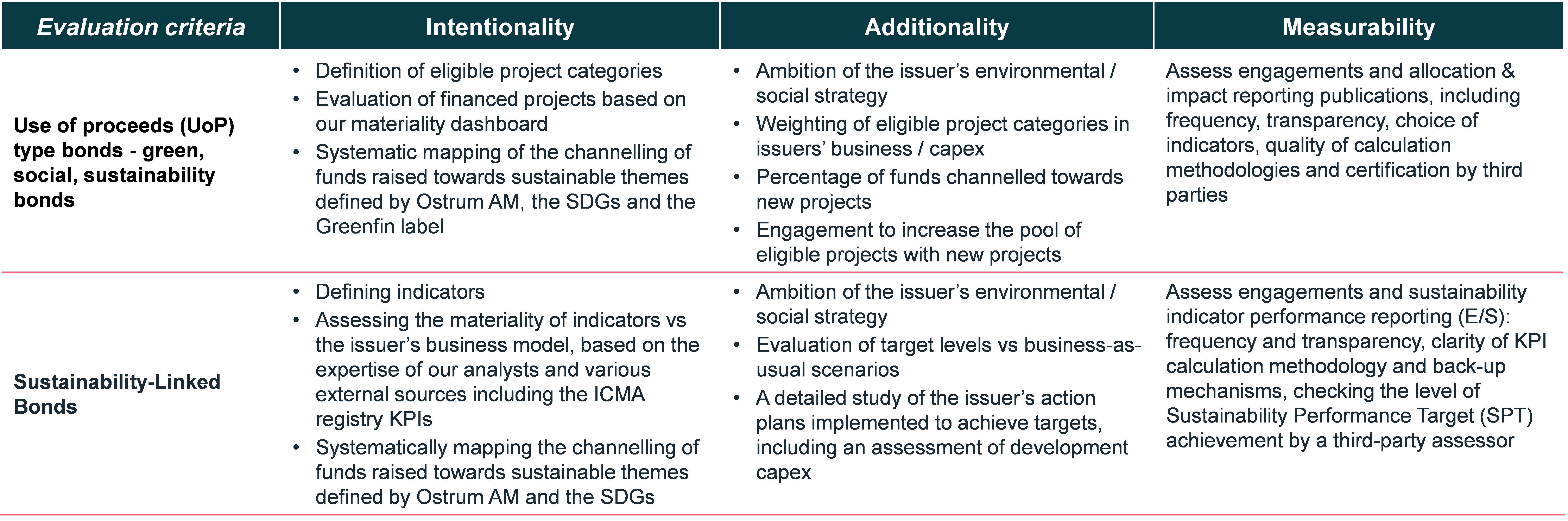

Use of proceeds (UoP) type bonds - green, social, sustainability bonds seek to channel funds raised towards environmental and/or social projects. Ostrum AM assesses intentionality through:

- The definition of eligible project categories

- The evaluation of projects financed, relying on a materiality dashboard

- Systematic mapping of the channelling of funds raised by sustainable themes (defined by Ostrum AM), SDGs and the Greenfin label

Sustainability-linked bonds are instruments issued with engagements to achieve targets relative to key environmental and/or social performance indicators. Ostrum AM assesses intentionality by:

- Defining performance indicators

- Assessing the materiality of indicators vs the issuer’s business model, based on the expertise of our analysts and various external sources including the ICMA registry KPIs

- Systematically mapping the channelling of funds raised by sustainable themes (defined by Ostrum AM) and SDGs.

4. How to ensure additionality?

Additionality is assessed by the ambition of the issuer’s E/S strategy, the channelling of funds towards new projects and sustainable performance target ambitions (E/S).

For use of proceeds (UoP) type bonds - green, social, sustainability bonds, Ostrum AM assesses the additionality of projects according to:

- The ambition of the issuer’s environmental/social strategy

- The weighting of eligible project categories in issuers’ business / capex

- The percentage of funds channelled towards new projects

- The engagement to increase the pool of eligible projects with new projects

For sustainability-linked bonds, Ostrum AM assesses the additionality of performance targets through:

- The ambition of the issuer’s environmental/social strategy

- Evaluation of target levels vs business-as-usual scenarios

- A detailed study of the issuer’s action plans implemented to achieve targets, including an assessment of development capex.

When necessary, Ostrum AM will also enter into dialogue to ensure the coherence of a sustainable bond issue with the underlying objectives of the issuer’s environmental/social strategy.

5. Measurability: allocation and impact report

Measurability is addressed via an analysis of engagements and the quality of reports published by issuers.

For use of proceeds (UoP) type bonds - green, social, sustainability bonds, Ostrum AM assesses engagements, allocation & impact reporting publications, including frequency, transparency, choice of indicators, quality of calculation methodologies and certification by third parties.

For sustainability-linked bonds, Ostrum AM assesses engagements and sustainability indicator performance reporting (E/S): frequency and transparency, clarity of KPI calculation methodology and back-up mechanisms, checking the level of Sustainability Performance Target (SPT) achievement by a third-party assessor.

The Climate and Social Impact Bond strategy annual allocation and impact report provides an overview of the environmental, social and regional impacts of investments. The report can be consulted on Ostrum AMs website: www.ostrum.com.

6. Climate and Social Impact Bond strategy: an impact investment classified SFDR Article 9

Ostrum AM’s Global Sustainable Transition Bonds strategy is classified SFDR Article 9.

According to the SFDR regulation, Article 9 strategies are “products pursuing sustainable investment objectives”. Funding must target an economic activity which contributes towards an environmental objective (measured for example through KPIs including the use of renewable energies, waste management and the impact on biodiversity) and/or an economic activity which contributes towards social objectives, including combating inequality and investing in human capital.

Investments must also respect the Do No Significant Harm principle (DNSH) based on principal adverse impact (PAI) and best governance practices considerations.

In April 2023, the European Securities and Markets Authority (ESMA) reaffirmed the SFDR transparency objective, leaving financial institutions to develop their own product classification methodologies, without endorsing a strict definition of the notion of “sustainable investment”.

This complemented the AMF project published early this year, proposing minimal environmental criteria for financial products in the Article 9 and Article 8 SFDR categories3. One of the key issues under the recommendations involves the possibility of measuring a minimum level of investments aligned with the European taxonomy. The lack of data on these criteria means that asset management companies are effectively unable to carry out this assessment conclusively at the current time.

Ostrum AM’s Climate and Social Impact Bond strategy respects the requirements imposed by its SFDR Article 9 classification.

The strategy invests in sustainable bonds that meet minimal levels required in terms of proprietary sustainable bond scores and a just transition indicator.

The strategy also respects Ostrum AM’s sector and exclusion policies (coal, tobacco, oil & gas, biodiversity, worst offenders, etc.) which complemented by additional requirements of the Greenfin and SRI Labels.

Lastly, Ostrum AM applies a dialogue and engagement policy with issuers. Defined by 8 themes (divided into 15 sub-themes), and in accordance with the United Nations Sustainable Development Goals, Ostrum AM’s policy seeks to encourage bond issuers to change their practices towards more virtuous approaches.

Conclusion

Impact finance is gaining momentum and is today more structured, benefiting from French and European frameworks of standards and definitions. Although no uniformity has yet been established among asset managers, the trend is on track towards greater transparency.

Investors are keen to give meaning to their assets and their savings and aspire to having an environmental impact. Although this should no longer be achieved at any price. The just transition principle is now at the heart of investment strategies, reaffirmed at the COP 27 in 2022 and the Paris Summit for a new global financing pact in June 2023. At the summit, 13 leaders, including Emmanuel Macron and Joe Biden, signed a tribune calling for “just ecological and socially inclusive transition”.

Ostrum AM’s Climate and Social Impact Bond strategy adopts this approach and constitutes a real impact solution for financing a just transition, i.e., transition towards a low-carbon world, which respects the environment and biodiversity, while also remaining socially and regionally inclusive. The key issue, as with any sustainable investment, is the availability and access to non-financial data. Thanks to Ostrum AM’s size and broad spectrum of research and investment management resources, Ostrum AM is positioned as a major player in this domain, with 32 billion euros invested in sustainable bonds (end-September 2023).

1 https://institutdelafinancedurable.com/app/uploads/2021/09/Finance-for-Tomorrow-Definition-de-la-finance-a-impact-Septembre-2021.pdf

2 https://www.icmagroup.org/sustainable-finance/the-principles-guidelines-and-handbooks/sustainability-linked-bond-principles-slbp/

3 https://www.amf-france.org/sites/institutionnel/files/private/2023-02/AMF%20SFDR%20minimum%20standards%20FR_0.pdf/AMF%20SFDR%20minimum%20standards%20FR_0.pdf

APPENDIX 1 – criteria to evaluate intentionality, additionality and measurability

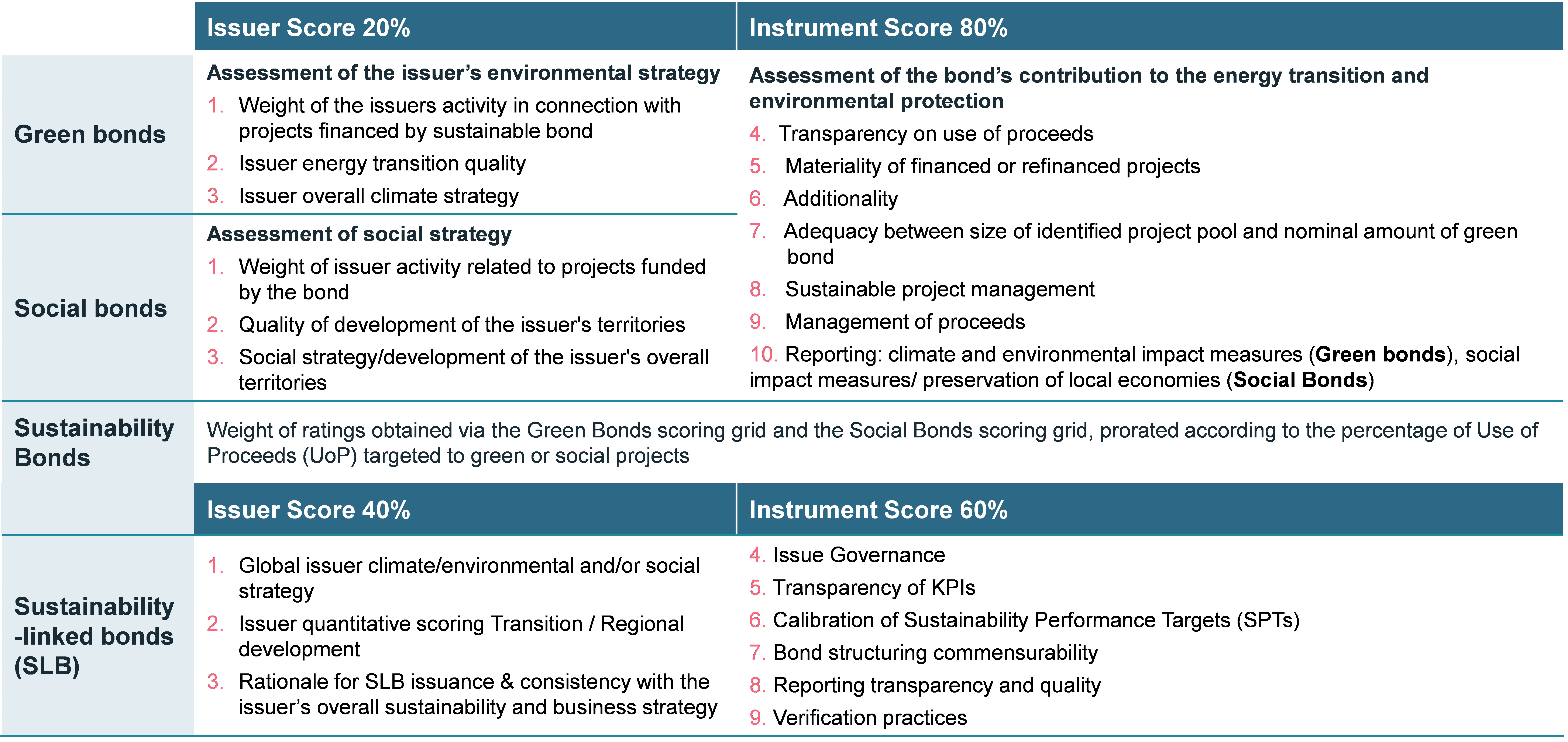

APPENDIX 2 – evaluation criteria for issuers’ Sustainable Bond Rating

Sustainable bonds definition – financing targets |

|---|

| Sustainable bonds are instruments that provide positive responses in terms of transparency and use of proceeds towards projects with environmental or social added value. There are five categories, each being by Principles and Guidelines elaborated by the ICMA (excl. Transition Bonds). However, it is a “self-labeled” market, where each investor qualifies the sustainability of its issues. It is thus crucial to be able to conduct an in-depth analysis of each issuer and issue. |

| GREEN BONDS Green Bonds are sustainable bonds that finance or re finance projects aimed at the energy and ecological transition: Renewable energy, energy efficiency, pollution prevention and control, sustainable environmental management of living natural resources and land use... Green bonds were the first sustainable bonds issued in the financial markets. Today, both private issuers and sovereign and assimilated issuers use this type of issue to finance their green projects. Green bonds dominate the market and account for about 2/3 of sustainable bonds. |

| SOCIAL BONDS Social Bonds are sustainable bonds that finance or re-finance projects to solve or mitigate key social problems: basic affordable infrastructure (drinking water, sanitation, etc.), access to basic services (health, housing, education, training), job creation, food security, access to digital technology, etc. Social Bonds have grown particularly strongly in 2020 in the context of the Covid-related health crisis. Since then, they have continued to grow but at a slower pace and represent about 15% of the market. The interest of issuers is partly linked to the need for a Just Transition, which integrates social criteria into environmental projects. |

| SUSTAINABILITY BONDS Sustainability bonds are sustainable bonds that finance or re-finance a combination of both environmental and social projects. These instruments help diversify the market, an important element for both issuers and investors. Sustainability bonds allow issuers to clearly identify environmental projects that have social benefits or social projects that have positive environmental impacts. It is the issuer that chooses to classify its issue as Green Bonds, Social Bonds or Sustainability Bonds. |

| SUSTAINABILITY-LINKED BONDS Sustainability-linked bonds are sustainable bonds that finance or re-finance the general needs of a company while promoting its CSR ambitions through a commitment to specific and costed medium- and long-term sustainable development goals. The issue is accompanied by KPIs (Key Performance Indicators) to measure and monitor commitments made. Since their creation in 2020, Sustainability-Linked Bonds have continued to grow: in 2021, the number of issues has multiplied by more than ten, to nearly 100 billion dollars, or about 12% of the market. New issuers, mainly from the high yield category, have seized the opportunity to refinance through this instrument, which represents in 2022 about 4% of the market. |

| TRANSITION BONDS Transition bonds are sustainable bonds whose purpose is to bridge the gap between “already low carbon” projects, eligible for financing by Green Bonds, and those that are not. However, they do make significant progress in reducing greenhouse gas (GHG) emissions. Transition bonds are mainly aimed at the industrial sector, to finance the transition of companies to a low-carbon world. Emitters commit to measurable reductions in their greenhouse gas (GHG) emissions. The Transitions bond market does not currently have a standard definition or framework. |

Impact investment strategies: intentionality, additionality and measurability

Download Impact investment strategies