Quarterly publication / July 2026

Analyses and data as of 07/02/2026.

Marketing communication for professional investors in accordance with MIFID II.

MARKETS OVERVIEW

THE WARSH ERA BEGINS

Kevin Warsh's arrival at the helm of the Fed marks a turning point in the conduct of U.S. monetary policy, especially as the Iran war may finally find a resolution. Several task forces have been launched to reform the institution.

Oil is trading around $75 per barrel despite declining inventories. The handover between Powell and Warsh comes at a pivotal moment with rising inflation accentuated by the oil shock and the first signs of improvement from the labor market.

In the eurozone, the ECB is raising rates in response to rising inflation expectations and core inflation accelerating toward 2.5%. Another hike will bring the deposit rate to 2.50% in September. Activity declined in the eurozone in Q2 and should experience a slow recovery thereafter. In China, exports remain the main driver of activity, but inflation is gradually recovering.

On financial markets, AI is dominating headlines, with prominent IPOs from SpaceX, to be followed by Anthropic and OpenAI. Profit-taking is generating increased volatility, particularly on the Nasdaq, Kospi, and Nikkei. Nevertheless, the outlook for earnings remains positive, especially in the United States.

In bond markets, fluctuations in oil prices have explained the bulk of yield changes since the onset of the war. Kevin Warsh's assessment of inflation risks will be crucial for bond markets.

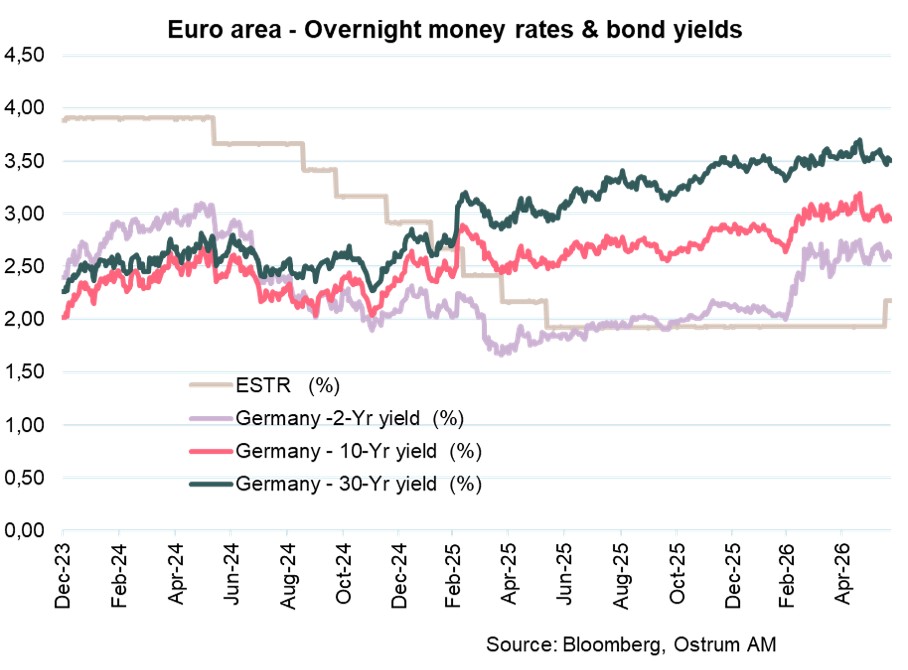

The ECB's policy, meanwhile, is more transparent, which should help the Bund stabilize around 3%. Sovereign and corporate debt spreads remain surprisingly inert and tight considering the volatility in interest rates. A slight widening of spreads is anticipated. High-yield debt is defying gravity, though default rates remain low. Regarding currencies, the yen, trading above 160 against the dollar, could prompt intervention from the Bank of Japan. The euro continues to trade within a narrow range between $1.14 and $1.18 since the start of the Iranian crisis.

KEY INDICATORS

3 MONTH OUTLOOK ON BOND MARKETS

Source: Ostrum AM, 02/07/2026

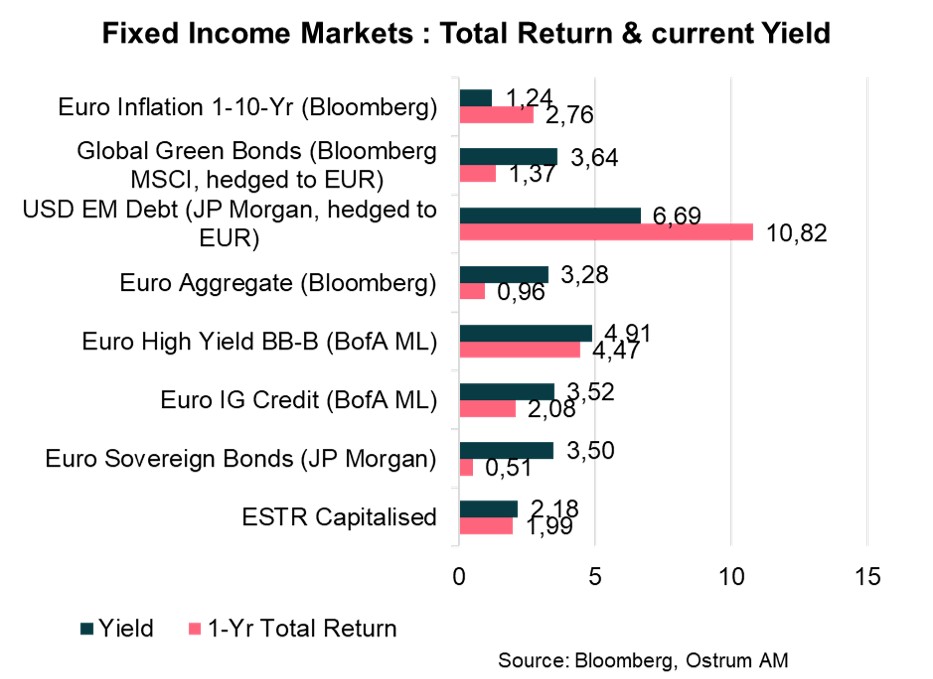

FIXED INCOME RETURNS & PERFORMANCES

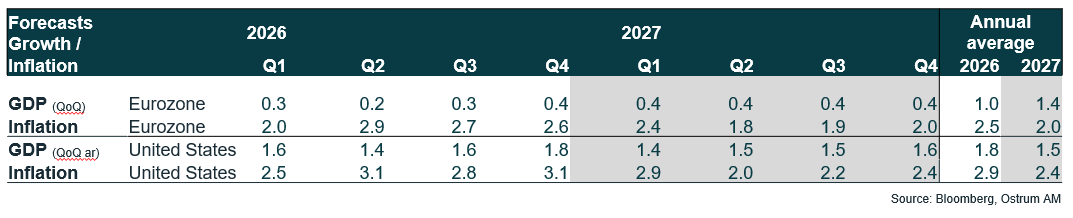

GROWTH & INFLATION

GROWTH

- Growth trajectories are diverging.

- The United States recorded moderate growth in Q1 (+1.6% annualized), supported by domestic demand but showing signs of deceleration.

- In the Eurozone, GDP contracted by 0.2% quarter-on-quarter in Q1, largely driven by a sharp downward revision in Irish GDP (-12,1% QoQ). Excluding Ireland, growth in the region stood at +0.2% QoQ. French GDP declined by 0.1% QoQ, reflecting weaker domestic demand weighed down by the energy shock.

- China continues to exhibit robust momentum (+1.3% QoQ, or +5.0% YoY), driven by strong export performance, particularly in high-tech sectors such as artificial intelligence.

INFLATION

- Iran and AI are contributing to rising inflationary pressures.

- In the United States, inflation accelerated to 4.2% in May, reaching a three‑year high, driven by higher energy costs. Core inflation also edged up to 2.9% from 2.8% in April.

- The transmission of the energy shock has been more pronounced in the euro area. Headline inflation rose to 3.2% in May, while core inflation increased to 2.6% from 2.2% previously. This trend reflects stronger services inflation, which reached 3.5% year‑on‑year, up from 3.2% in April.

By contrast, inflation in China remained stable at 1.2% in May, supported primarily by contributions from transportation and communication components.

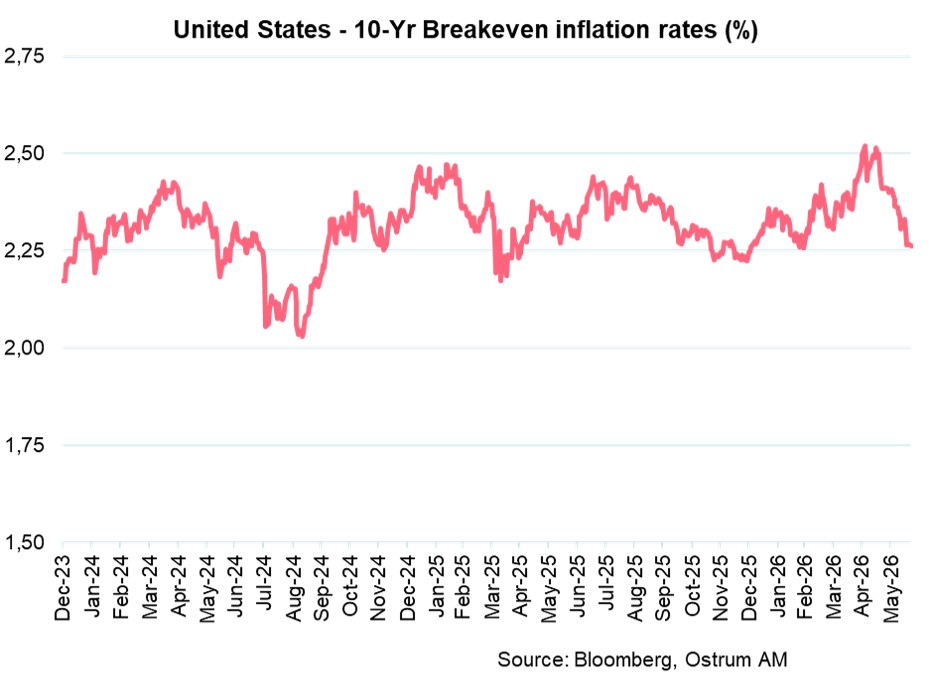

Eurozone inflation: Long-term inflation expectations have increased due to the oil shock. The premium is beginning to diminish.

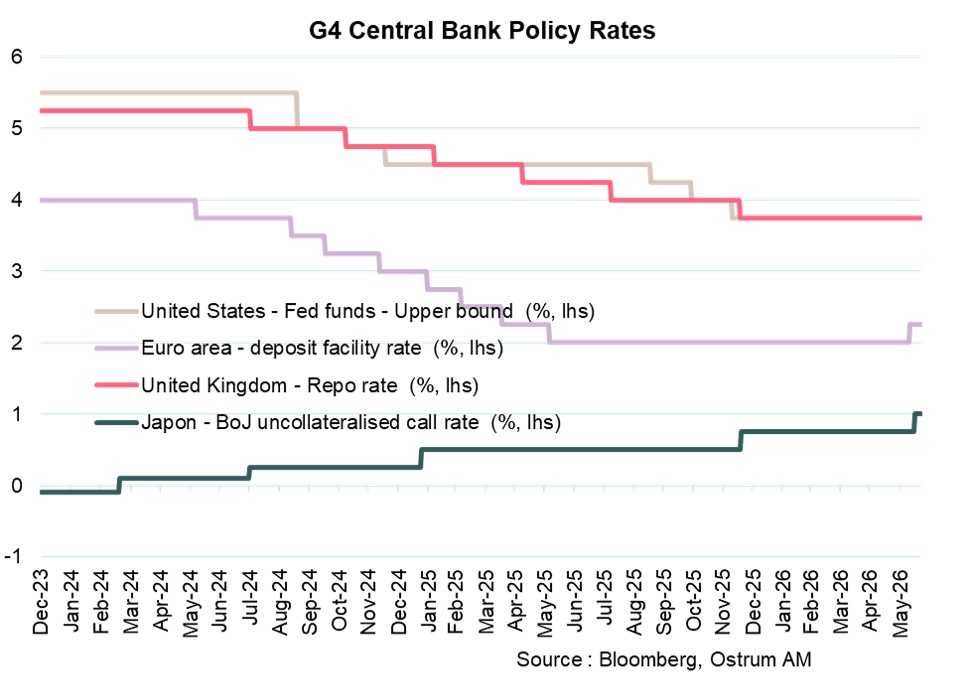

CENTRAL BANKS RATES

MONETARY POLICIES

KEVIN WARSH LEAVES HIS MARK FROM HIS VERY FIRST MEETING AT THE HELM OF THE FED

At his first meeting as Chair of the Fed, held on June 16–17, Kevin Warsh has already altered the central bank’s communication. Forward guidance on the future path of interest rates has been removed, reducing the Fed’s statement to just nine lines.

The decision to leave rates unchanged, within the 3.50%–3.75% range, was unanimous. Economic activity is still viewed as solid, while inflation remains elevated. The statement states that the Fed will deliver price stability (one of its core objectives).

Another change is that Kevin Warsh did not present his own outlook in the SEP (Summary of Economic Projections) and, at the same time, downplayed those provided by FOMC members. Nine members expect at least one rate hike by year-end, eight foresee a status quo, and one is in favor of a rate cut. These divergent views reflect limited conviction within the FOMC.

Kevin Warsh also announced five task forces aimed at overhauling the Fed, with most conclusions expected by year-end. They cover: communication, balance sheet policy, data usage, productivity and employment, and the inflation analysis framework.

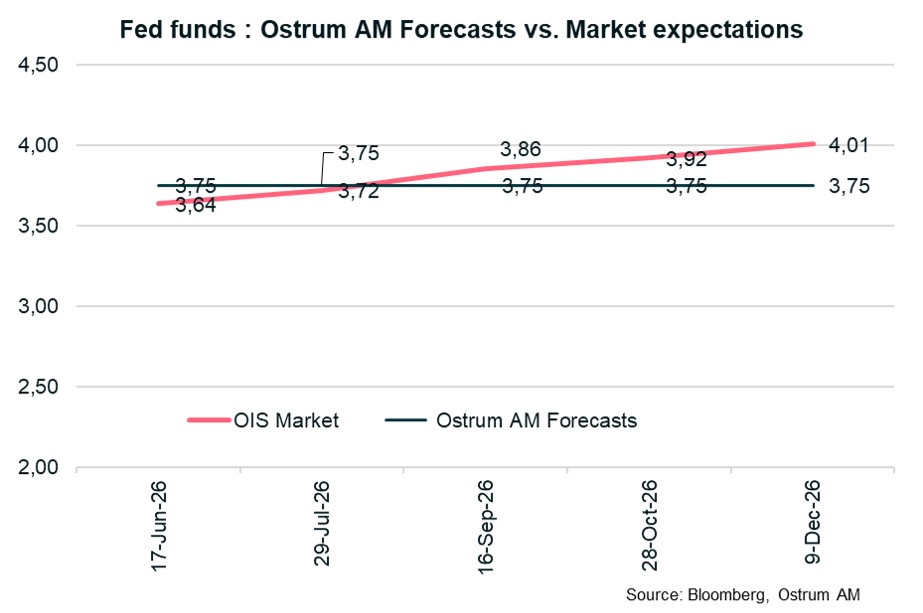

With Kevin Warsh at its helm, the Fed is operating under the influence of the White House. Although our forecast is for a status quo on the Fed funds rate through the end of the year, the next rate move is more likely to be a cut.

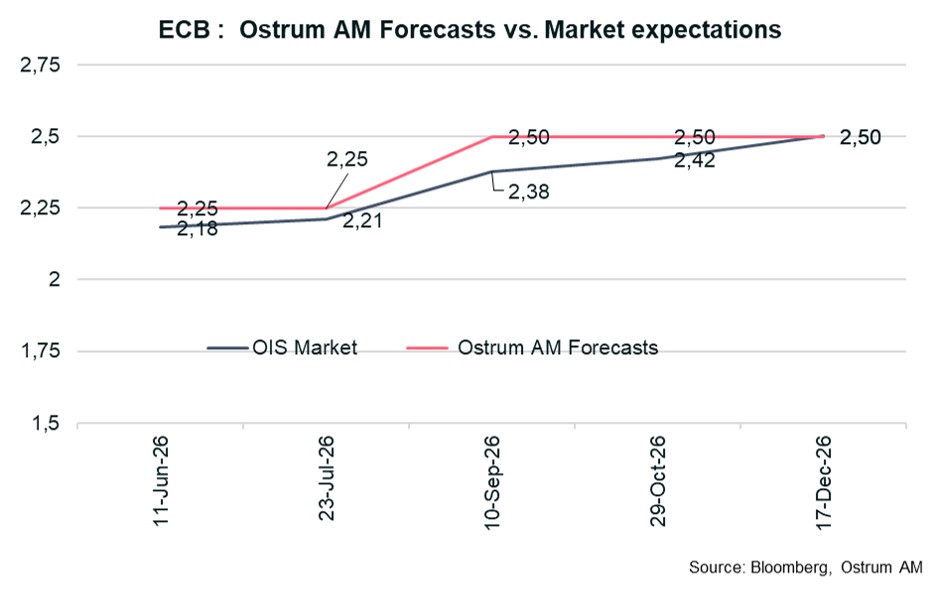

HEADING TOWARD A SECOND ECB RATE HIKE IN SEPTEMBER.

As it had largely signaled at its April meeting, the ECB raised its rates by 25 bps on June 11, for the first time since September 2023, bringing the deposit rate to 2.25%. Persistently high oil prices, driven by the ongoing conflict in the Middle East, along with signs that the energy shock is feeding through to services prices, have led the ECB to significantly revise its inflation outlook upward. The prospect of a stronger pass-through of the energy shock to core inflation (expected at 2.5% in 2026 and 2027) reinforces our view that the ECB will deliver another 25 bps rate hike at the September 10 meeting, in order to anchor inflation expectations. During the press conference, Christine Lagarde dismissed the notion that this was an insurance or pre-emptive rate hike, stating that the decision was justified under all three scenarios (milder, adverse and severe). The framework agreement signed between the United States and Iran does not alter our scenario. Even assuming a full reopening of the Strait of Hormuz (which is not guaranteed), oil prices would remain above pre-conflict levels, posing a risk of second-round effects that the ECB will need to contain.

INTEREST RATES INDICATORS

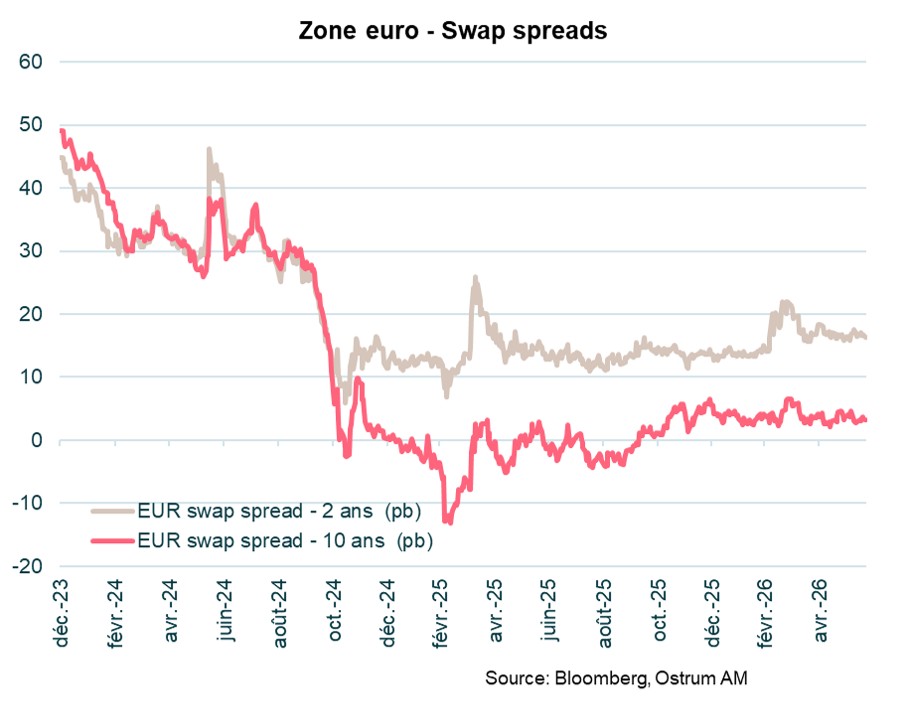

EURO SOVEREIGN BONDS

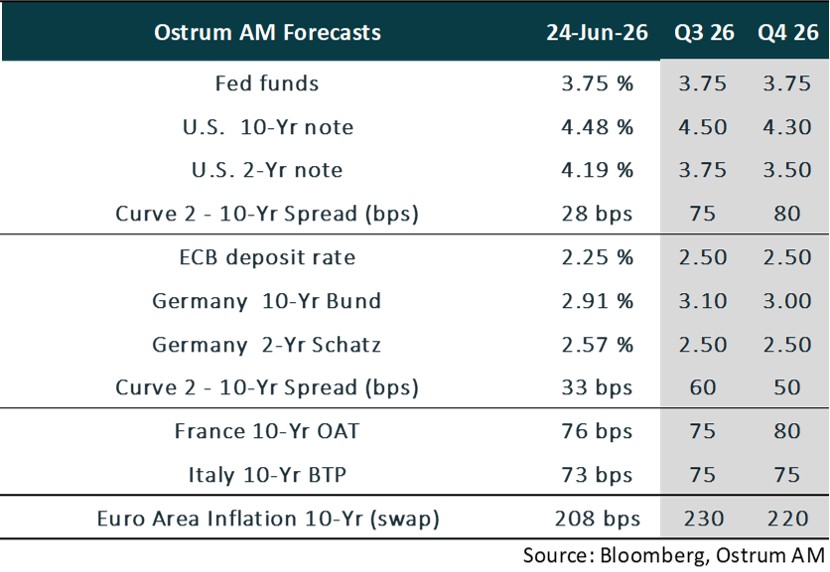

- U.S. Rates: Kevin Warsh has assumed his duties as head of the Fed and chaired his first FOMC in June with the ambition to reform the institution. Monetary status quo should be maintained until the end of the year.

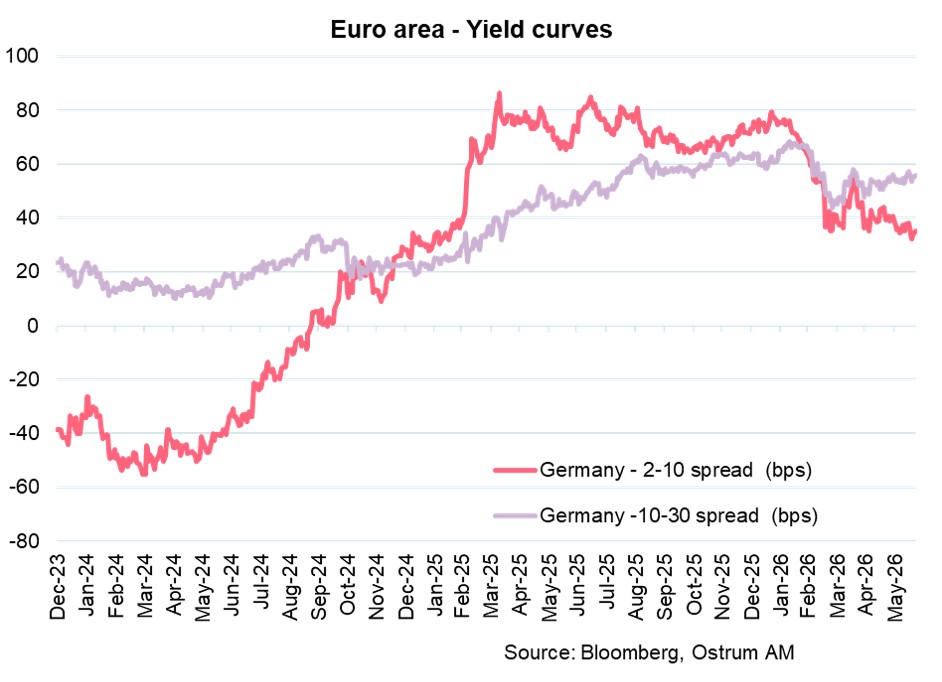

- European Rates: The ECB should raise rates once more to weigh on inflation expectations. The 10-year Bund will oscillate around 3.10% before declining toward 3.0% at year-end.

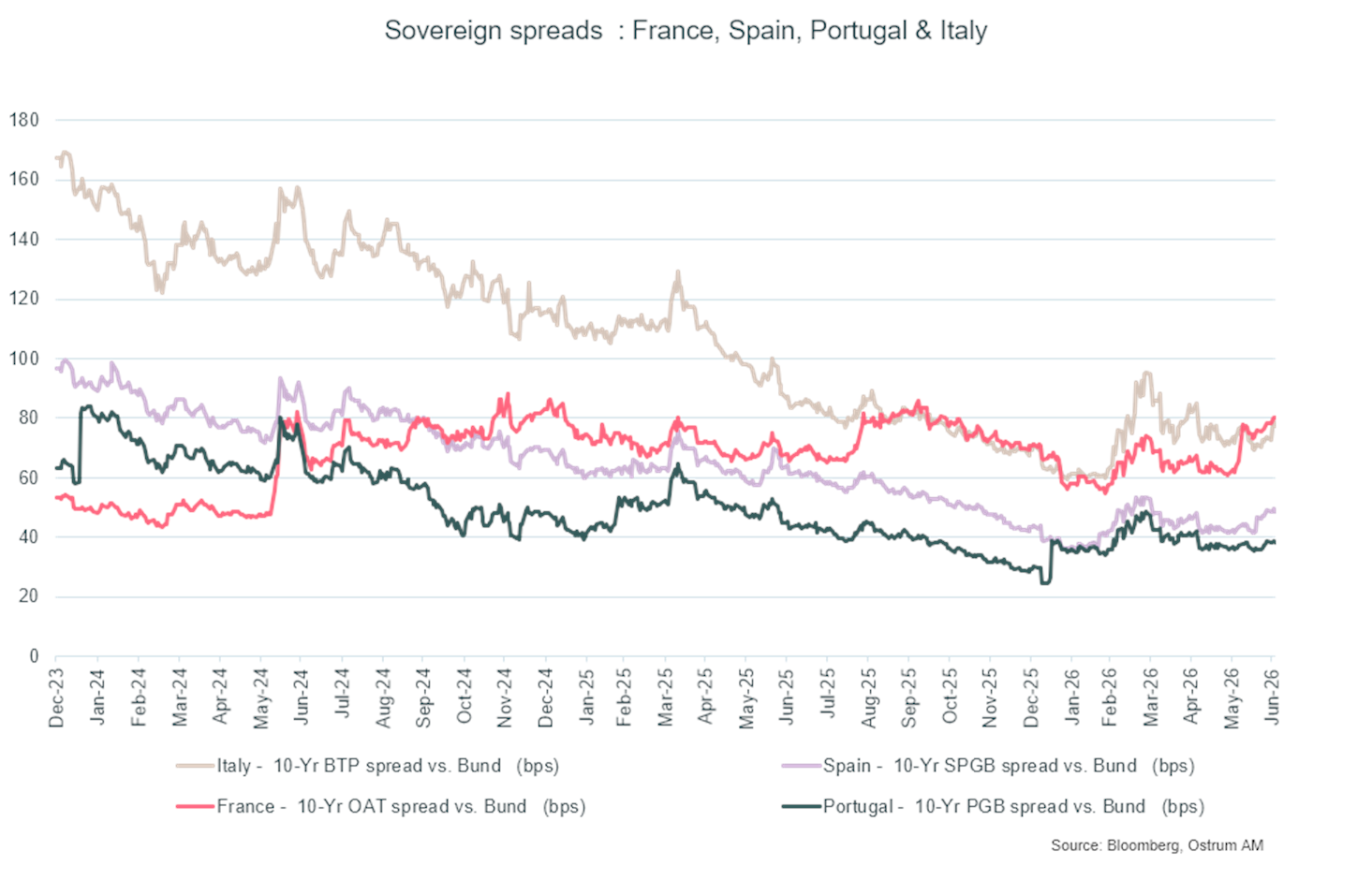

- Sovereign Spreads: Sovereign spreads have almost completely erased the Iranian crisis. Political considerations in France should weigh on the OAT at year-end. Italy's spread should remain around 75 basis points or higher.

- Strong Duration-Driven Rally: European sovereign bonds delivered robust Q2 performance (+1.88% Euro Area average), with longer-duration bonds significantly outperforming as yields fell sharply following the Iran crisis resolution and ECB repricing.

- Periphery Outperformance vs. Core: Peripheral sovereigns substantially outpaced Bunds, with Greece (+2.84%), Italy (+2.48%), and Portugal (+1.97%) leading gains as credit spreads compressed dramatically amid reduced energy import concerns.

- Duration Sweet Spot in 7-10 Year Bucket: The 7-10 year maturity segment delivered optimal risk-adjusted returns across most issuers (+2.38% Euro Area average), benefiting from the steepest part of the yield curve rally while avoiding some of the convexity drag affecting ultra-long bonds.

- German Underperformance Signals Normalization: Bunds (+1.41%) lagged, reflecting reduced safe-haven demand and suggesting investors are rotating toward higher-yielding alternatives as geopolitical risk premiums normalize.

EMERGING BONDS

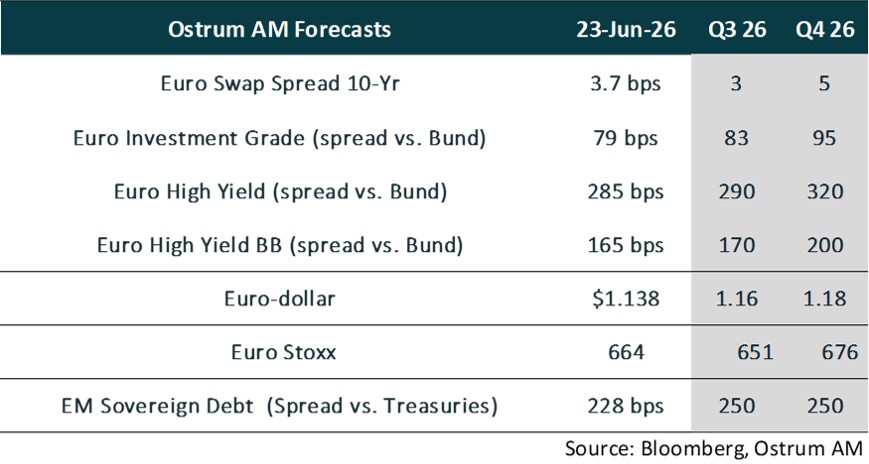

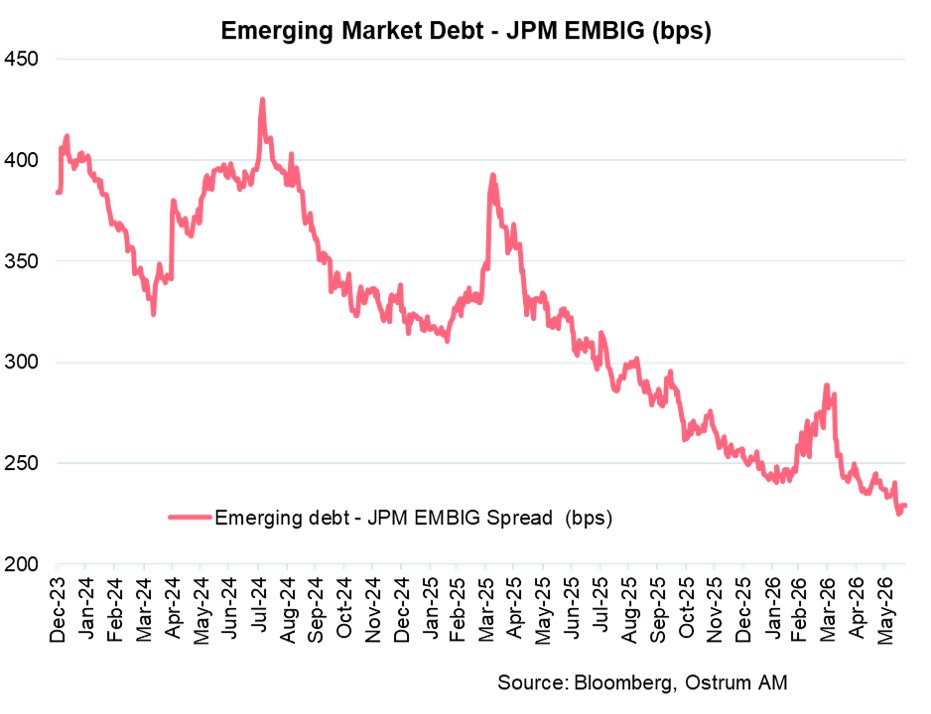

The EMBI Global Diversified (EMBIG) is withstanding the Iranian crisis. Spreads will remain tight around 250 basis points.

Outstanding EM Debt Rally

- Outstanding EM Debt Rally: EMBIG delivered exceptional Q2 returns (+4.63%), significantly outperforming developed market bonds as emerging market spreads tightened 18 basis points amid improved risk sentiment following the Iran crisis resolution and falling US Treasury yields.

- Duration-Driven Performance: Longer-duration EM bonds dominated, with 10+ year paper (+6.06%) and 7-10 year bonds (+5.50%) leading gains, reflecting investors' appetite for duration exposure.

- High Yield vs. Investment Grade Divergence: EM high yield (+6.74%) substantially outperformed high grade (+2.48%), with spread compression of 20 basis points each, indicating strong risk-on sentiment as investors embraced credit beta over quality in the improving global environment.

- Frontier Markets Outperformance: Next Generation EM (+7.39%) posted remarkable returns with 21 basis points of spread tightening, suggesting investors rotated into higher-beta frontier credits as geopolitical risk premiums normalized and commodity-linked economies benefited from stabilizing energy markets.

CREDIT INDICATORS

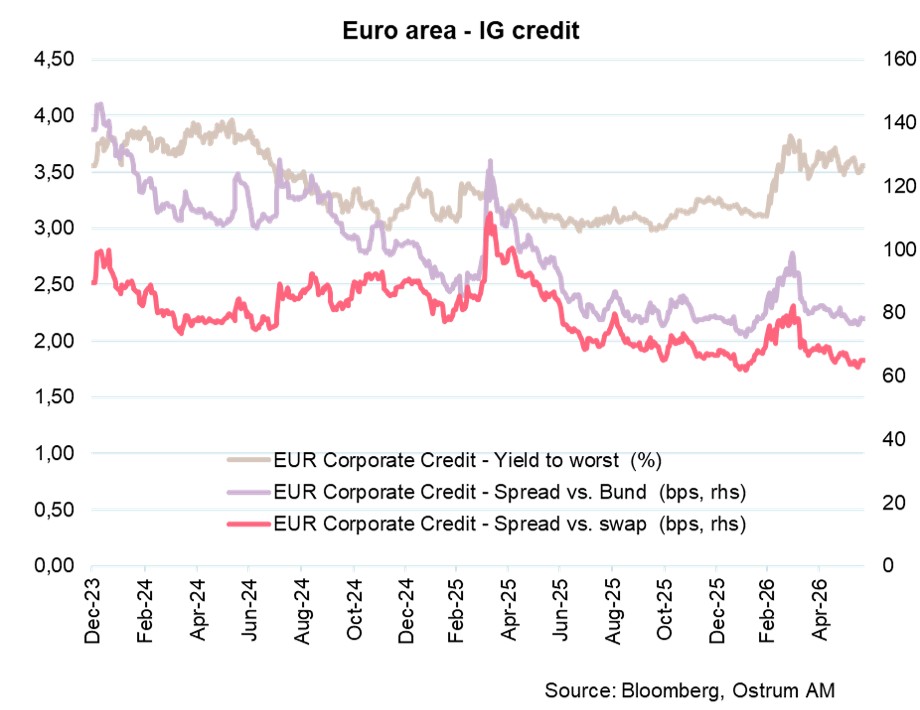

EURO INVESTMENT GRADE CREDIT

Investment-grade credit spreads have quickly erased the Iranian crisis and the primary market is well absorbed. However, valuation levels would justify widening by year-end.

- Strong Credit Rally: Euro corporate bonds delivered robust Q2 returns (+2.33%), reflecting significant spread compression and duration gains as the Iran crisis resolution drove a broad-based rally in risk assets amid falling government yields.

- Financial Outperformance Led by Subordinated Debt: Financial subordinated bonds significantly outpaced senior debt, with Junior Subordinated/Tier-1 (+3.11%) and Subordinated Insurance (+2.78%) leading gains as investors embraced credit risk and regulatory capital instruments benefited from improved bank fundamentals.

- Real Estate and Energy Sector Rotation: Real Estate (+2.99%) posted exceptional returns as lower rates boosted property valuations, while Energy (+2.29%) underperformed despite oil market volatility, suggesting investors favored interest-rate sensitive sectors over commodity plays.

- Quality vs. Beta Trade-off Auto (+2.03%) and Technology (+2.37%) showed mixed performance despite strong Q2 gains, with the sector rotation favoring defensive utilities (+2.42%) and leisure (+2.62%) as investors balanced credit quality with cyclical exposure amid economic uncertainty.

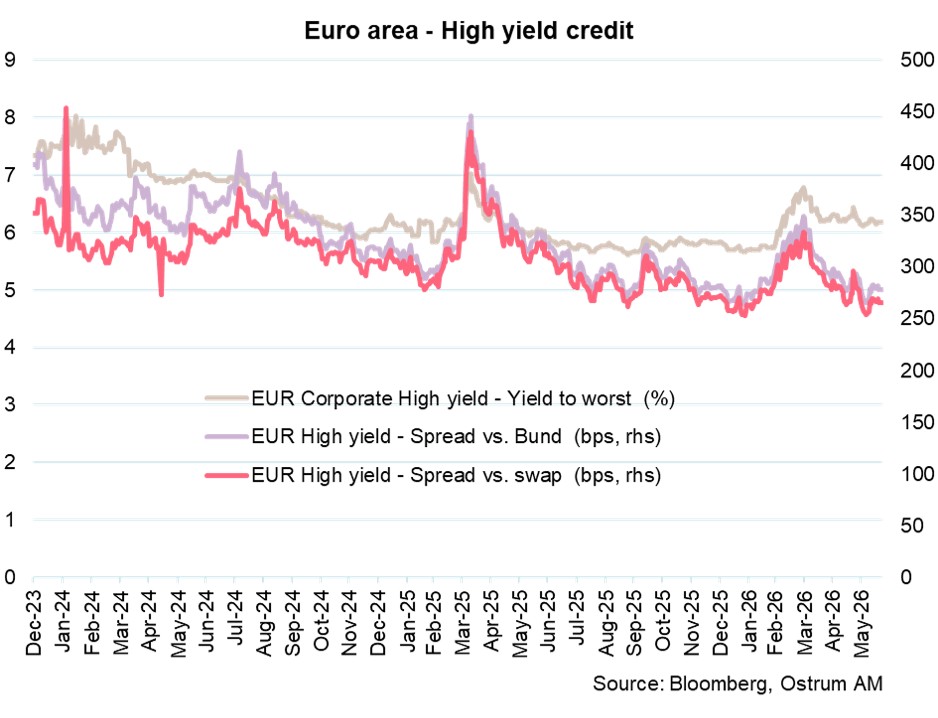

EURO HIGH YIELD CREDIT

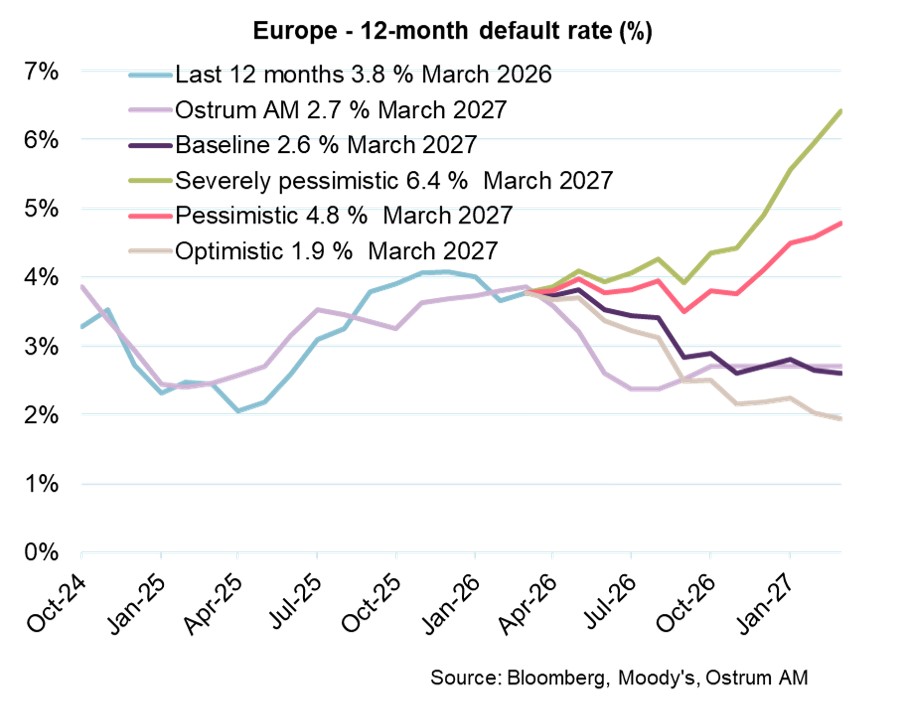

High yield valuations should normalize over the course of the year. The default rate, however, remains contained and below the long-term average.

Exceptional High Yield Rally

- Exceptional High Yield Rally: Euro high yield delivered outstanding Q2 returns (+3.69%), significantly outperforming investment grade as credit spreads compressed dramatically following the Iran crisis resolution and investors embraced higher-beta fixed income assets.

- Duration Sweet Spot in Mid-Curve: The 4-6 year maturity bucket (+4.20%) posted the strongest performance, capturing optimal duration exposure as yield curves steepened and investors favored the sweet spot between short-term rate volatility and long-duration convexity risks.

- Fallen Angels Underperform Quality: Fallen Angel bonds (+2.84%) notably lagged the broader index, suggesting investors preferred original issue high yield (+3.77%) over recently downgraded credits, reflecting quality bias in risk asset selection.

- Floating Rate Weakness: Euro floating rate high yield (+2.41%) significantly underperformed fixed-rate equivalents.

FOCUS ON SUSTAINABLE BONDS

QUARTERLY GRAPH

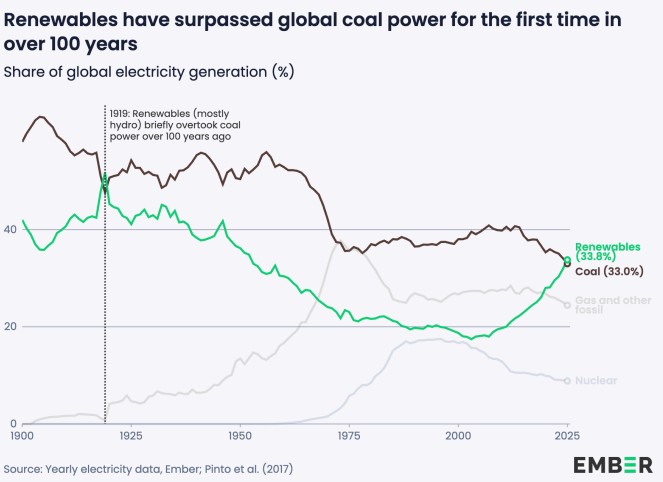

Share of global electricity generation (%)

Renewable energy has overtaken coal for the first time in over a century, accounting for 33.8% of global electricity generation in 2025, compared to 33% for coal.

Source: Ember 2026

Quarterly news selection, more information on our monthly publication MySustainableCorner https://www.ostrum.com/fr/news-insights/insights

- Renewable energies now account for one-third of global electricity generation, surpassing fossil fuels for the first time. This shift is driven by solar power, particularly in Asia. However, the diurnal nature of solar presents challenges, sometimes leading to negative prices and curtailment (voluntarily reducing the output of a power plant) during periods of abundance. To address this, the global deployment of storage batteries is massively accelerating, with an addition of 247 GWh in 2026.

- In February 2026, the City of Paris issued a new sustainable bond sized €350 M, with the aim of financing the development of clean transport (metro lines, cycle paths), the energy renovation of social housing, and adaptation to climate change through the greening of public spaces.

- L'Autorité des Marchés Financiers (French regulatory authority AMF) is launching a 2026-2028 plan to bridge the gap between men and women in investment. In 2025, only 24% of women invested in the stock market, a gap explained less by income than by a lack of confidence or a feeling of illegitimacy. The "Women and Investment" initiative will study these barriers starting in 2026 to build a dedicated financial education strategy from 2027.

- Since early 2026, the EuGBs format has resulted in 7 issuances from banks, utilities, as well as an agency and a supranational issuer. Issuance amounts, mainly around €500–600 M), have also reached levels of €1 bn up to €4 bn, demonstrating the market's capacity to absorb significant volumes. In total, €7.9 bn was issued in the first quarter of 2026, indicating the visibility and readability of this market segment.

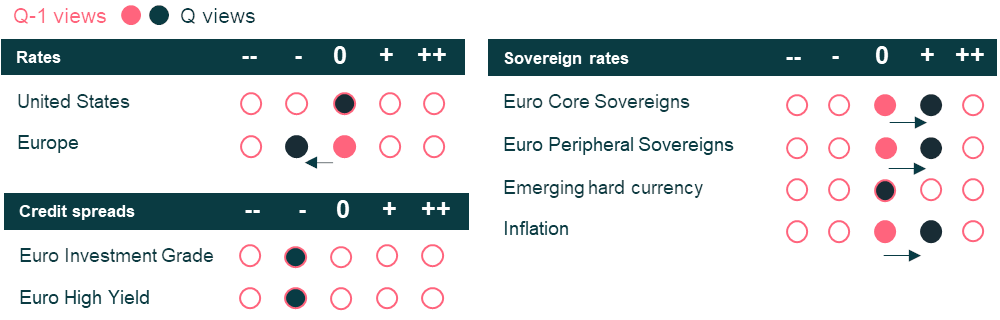

DASHBOARD - OSTRUM AM VIEWS

MACROECONOMIC OUTLOOK • EUROZONE AND UNITED STATES

MARKET VIEWS