Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum’s views on the economy, strategy and markets.

The CIO letter

- Central banks ease up on the gas pedal

With the meetings of the Fed, BoE and then BCE less than 24 hours apart, we changed our monthly investment committees. This publication presents the impact of decisions on our views.

This year out of the 53 global central banks that we look out for, 19 have raised their rates for only 3 drops. The movement does not stop there, the Bank of Canada has stopped its QE, the Fed has announced a tapering and the ECB has announced a step-by-step reduction of its QE.

Growth remains strong, it is necessary to go back very far to find inflation figures similar to those published today, a time that those under twenty years cannot know. Financial or real estate assets are highly valued in many cases. The argument for an extremely lax monetary policy gradually disappears and the central banks reduce their stimulus. However, monetary conditions remain very accommodative and a global monetary tightening is still far from being achieved.

Beyond this upward trend, we must also take into account the growing lack of visibility, and therefore the very high uncertainty that should be the common denominator of markets in 2022. Central banks are caught between a need to normalize their policy to avoid the risk of inflation setting in for even longer, but must be careful not to derail markets where certain situations look like bubbles.

It is a very narrow path between on the one hand a risk of overheating, which implies the need to accelerate standardization, and a risk of accident on the markets which conversely calls for caution.

Summary

Strategic views

A more ambiguous support from central banks

Synthetic market views: more complex

The year 2022 should be characterized by two market trends: a monetary tightening, even if the central banks remain accommodating, and a sharp drop in visibility on the future trajectory of this monetary policy, which should stress the markets. On the other hand, economic fundamentals should remain positive and bear risk assets.

A monetary tightening and a sharp drop in visibility on the future trajectory of this monetary policy.

Allocation recommendations: where to find value ?

Sovereign market. (1) Inflation should remain a major theme. (2) Invest in the sustainable bond market: to benefit from the evolution of greenium. (3) Emerging countries: an asset class offering an interesting carry with improved risk resilience.

Credit. Improving fundamentals, “rising stars” versus “falling angels”. And so looking for yield via credit risk (Crossover, high yield) rather than duration. Rate risk management is critical. The US HY is too expensive compared to Europe.

Stockmarket. Two main themes. (1) Look for interesting growth prospects: Financial, Media, Technology, Travel & Leisure, Health (resistance to inflation), Energy & basic resources, Luxury & Upscale. (2) If inflation increases, pay attention to the sectors: Automotive, Air transport, Food, Consumer discretionary.

Central Banks

Fed - acceleration

Decision:

- Accelerating the “tapering” from $15 billion per month to $30 billion, so QE will end in March.

- The dot-chart shows three rate increases in 2022, and three more in 2023.

Our view:

- This decision is not really a surprise, the Fed had, as usual, leaked the announced changes in advance. The decision is therefore not a major surprise for the markets.

- However, this acceleration is in line with a gradual but continuous change in the Fed’s tone over the past 6 months, with a more restrictive FOMC in June and September, Powell acknowledging that inflation is not “temporary”, “dots” migrating upward, etc.

- By the beginning of Q2, the Fed will have finished its QE, inflation will still be close to, or even higher than 6%, unemployment will have returned to 3.5%, the lowest level pre-COVID. Under these conditions, an increase in rates before the summer is very plausible, which indeed leaves the possibility of three increases before the end of 2022.

Market implications:

- The increase in rates is also expected to have an impact on the long part of the curve which is in line with our Treasury target of 2.00% at the end of the year. The flattening of the curve should therefore continue, a typical dynamic of this phase of the monetary cycle.

- The interest rate differential has contributed to the recent appreciation of the dollar. This trend is expected to continue.

- Monetary tightening can also have an impact on equity markets, in particular interest rate sensitive sectors.

- Emerging markets have withstood recent rate hikes very well, the EMBIG index for example has made very little headway. If we wait for this trend to continue, the cumulative effect of Fed decisions could become problematic.

ECB - Gradual decline in asset purchases

Decision: With progress on growth and inflation, the ECB is gradually reducing its asset purchases

End of net purchases of the PEPP at the end of March – Reinvestments extended until at least the end of 2024

- Slowdown in net purchases of the Pandemic Emergency Procurement Program (PEPP) in Q1 2022, halted at the end of March 2022.

- The period of reinvestment of PPGTP falls was extended by 1 year to at least the end of 2024. Flexibility in the event of a period of stress (particularly linked to the pandemic) will be achieved through reinvestments that can be adjusted over time, between asset classes and countries.

- The statement explicitly states that the ECB will be able to make purchases of Greek securities in excess of redemption renewals in order to avoid a sudden interruption of its purchases.

- Net purchases under the PEPP will be able to resume, if necessary, to counter the negative shocks associated with the epidemic.

To avoid a sharp reduction in asset purchases, the PPA is temporarily increased

- Starting in Q2 2022, net asset purchases under the APA are doubled to €40 billion, rising to €30 billion in Q3 and returning to €20 billion in October 2022.

- Purchases will continue as long as necessary to strengthen the accommodative impact of monetary policy. They will end shortly before the rates are raised.

Rates remain unchanged

- 0% for the refinancing rate, 0.25% for the marginal lending facility and -0.50% for the deposit rate.

- Christine Lagarde reiterated that an increase in interest rates in 2022 was highly unlikely.

No TLTRO decision – ECB monitors banks’ financing conditions.

ECB – Views

ECB growth and inflation forecasts

- GDP: 5.1% in 2021 (5% announced in September), 4.2% in 2022 (4.6%), 2.9% in 2023 (2.1%) and 1.6% in 2024

- Inflation: 2.6% in 2021 (2.2% in September), 3.2% in 2022 (1.7% in September), 1.8% in 2023 (1.5%) and 1.8% in 2024. Core inflation: 1.4% in 2021 (1.3%), 1.9% in 2022 (1.4%), 1.7% in 2023 (1.5%), 1.8% in 2024

- Inflation forecasts have been significantly revised upwards. The 2/3 revision of the inflation outlook in 2022 is linked to the contribution of energy.

- Inflation is close to its symmetrical target of 2 per cent in 2024 but remains below that, which justifies the maintenance of an accommodative monetary policy.

Our view :

- The ECB avoids a sharp reduction in these asset purchases through the temporary increase in the APP while providing flexibility in the event of stress. A surprise is the visibility provided, as the ECB has accurately described the path of QE throughout 2022.

- These purchases will absorb the States' net emissions in 2022, estimated at 480 billion. The QE of the ECB is of the order of 1,088 billion euros in 2021, of which 1,020 are sovereign. It would increase to 480 billion of which 420 are sovereign.

- De facto, the ECB is setting up a much slower “tapering” than the Fed and insists on the need to keep key rates historically low, unlike the Fed. As a result, there is a growing divergence in the monetary cycle. The ECB will thus limit tensions on sovereign rates and spreads.

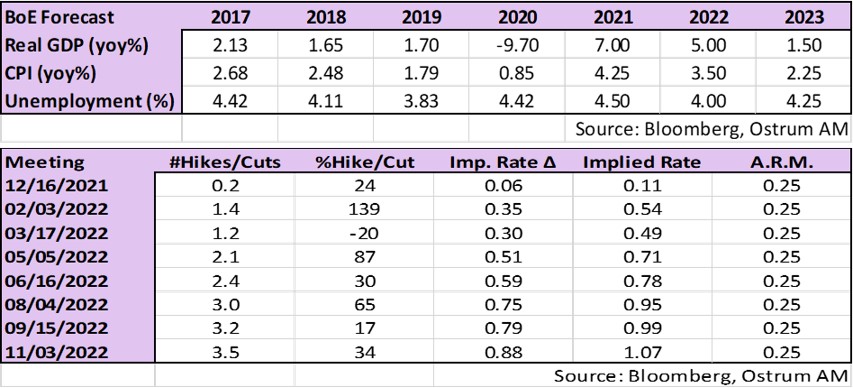

Bank of England - Surprise

Decision: November December Hike

- Repo hiked from 0,1 % to 0,25 % (vote 8-1).

- L’APF unchanged (9-0)

Our view:

- The Bank of England faces a dilemma between economic numbers that require tightening monetary policy and fears about Covid.

- Labour market: 4.2% unemployed with 149k jobs created in three months. Inflation (Nov): RPI 7.1%, CPI 5.1%, PPI output 9.1%. Activity: PMI Service 53.2 in Dec, Manufacturing 57.6

- Covid “The Omicron variant presents downside risks to business in early 2022, although the net effect (…) on overall medium-term inflationary pressures is unclear. Global cost pressures have remained strong.”

- The 3m GBP LIBOR (or SONIA) will reach 1.25% (1%) in 2023, meaning there will be no increase after 2022.

- According to BoE forecasts, real rates will therefore remain negative forever.

PBoC – Glaring Divergence with the Fed

Decision:

- Glaring divergence between the Fed’s and PBoC’s monetary policies, reflecting two different economic situations in terms of inflation and level of recovery.

- If the Chinese economic recovery was the fastest in 2020, it was undermined in 2021 by the delta variant (and Omicron) as well as the real estate and energy crisis.

- This led to a reversal in Chinese monetary policy that became less restrictive in order to stabilize growth, as did social finance (a broad measure of credit in China), whose growth has become positive.

Our view:

- The tighter the Fed, the more the PBoC will soften to support domestic demand

- The tightening of the Fed’s monetary policy should result in a strengthening of the dollar.

- Companies exporting intermediate goods are the most sensitive to a strong dollar.

- The strong dollar has the effect of penalizing world trade, China should further relax its monetary policy to support domestic demand.

Market implications:

- Monetary policy differences also exist in emerging countries. Asia is not affected by inflation problems like other emerging countries being a big consumer of rice and not wheat.

- The stabilization of Chinese growth also requires a stable yuan against the dollar.

- Chinese local rates therefore appear to be the most attractive and less volatile.