As Europe takes a crucial step in its energy transition, the sustainable bond market is undergoing a period of profound change.

From the promising emergence of "transition bonds" which are redefining the rules of the game for the most carbon-intensive sectors, to the energy explosion of data centers which is disrupting our sustainability paradigms, and the new regulatory requirements which are redistributing the playing field, 2026 promises to be an intense year.

This analysis reveals the profound changes in a market at the height of its effervescence: which sectors will fare well? How will new transition bonds revolutionize the financing of de-carbonization? And why could artificial intelligence paradoxically become the biggest environmental challenge of the decade?

Delve into the workings of a financial ecosystem that is rewriting the rules to shape the economy of tomorrow.

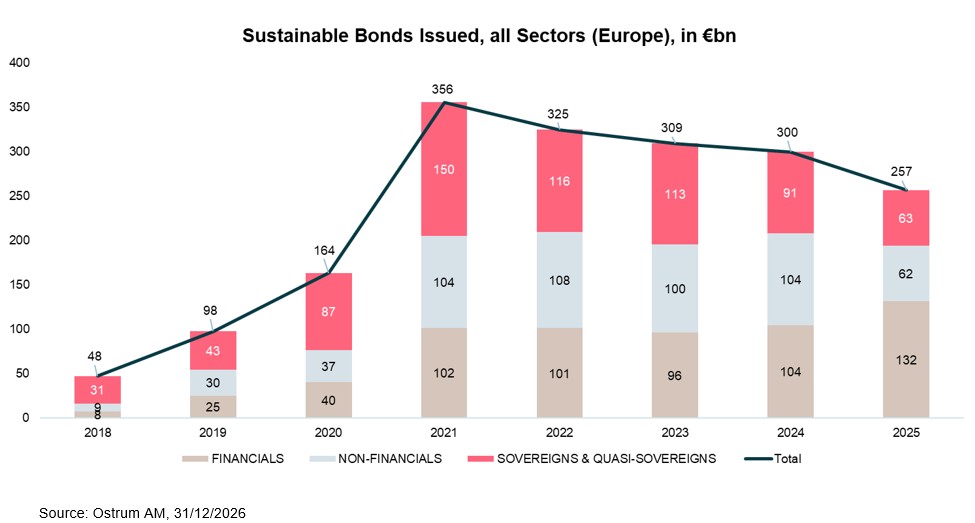

European Sustainable bonds market, as of end of 2025

Between stability and uncertainty: the 2026 sector map for sustainable bonds

Non-Financial Sectors

Leading the primary market, the Utilities sector (public services) has a stable outlook for 2026 overall. Although the implementation of the EU GBS (European Green Bond Standard) should stimulate green issuance, this dynamic is tempered by a possible reduction in capital expenditure (CAPEX) in renewable energies, particularly on assets located in the United States.

In contrast, the transport sector, and the automotive industry in particular, is facing a less favourable outlook. These are clouded by regulatory uncertainties, illustrated by recent adjustments from the European Commission regarding the 2027 and 2035 deadlines, as well as a US market showing a slowdown in the adoption of hybrid and electric vehicles.

Financial Sectors

Banks are massively favouring green bonds and taking advantage of the integration of European green bond standards (EU GBS) into their issuance frameworks. This trend is being driven by initiatives such as ABN Amro, which has already completed three new deals in line with these new standards. The outlook for issues from the banking sector remains favourable, driven by the arrival of new issuers who are gradually adopting this standardised format.

Sovereign and quasi sovereign issuers

Green bonds format: sustainable bond issuances by sovereign and quasi-sovereign entities (regions, departments or cities) in the European Union are showing less robust dynamics compared to other global regions (especially Asia). However, as with Energy (or "Utilities") companies or Banks, supranational issuers are accelerating their issuances aligned with activities recognised by the European Taxonomy, or "EU GBS" (e.g., Ile de France Mobilités, European Investment Bank - EIB). The same dynamic can be seen for cities (e.g., Madrid). Government issuers (governments) are also adopting this standard. Several other states are likely to follow this trend, to the detriment of different issuance formats, such as Social Bonds or Sustainability-Linked bonds (SLBs), which are expected to remain flat or decline.

Social bonds format: most sovereign issuers and quasi sovereign issuers are already active on this market segment and we do not expect any new issuers in 2026. Furthermore, the peak in social issuance in Europe occurred following the financing needs of supranational organisations and agencies to offset the financial losses of SMEs and public services due to the COVID-19 pandemic. To conclude, we expect a slight downward trend for this market segment in Europe.

Decarbonizing the real economy: the bet on transition bonds

Transition bonds are designed for economic actors whose activities are highly carbon-intensive and who cannot issue bonds through traditional green bonds. These instruments aim to support financing for reducing issuers' carbon footprints as part of their energy transition. Unlike green activities and projects, which are clearly defined and recognized by the markets, transition bonds have, since their inception, sparked debate: do they have a real positive environmental impact? Are they sufficient to effectively finance issuers' energy transitions? How exactly do we define which assets or projects are truly "transitional"?

In January 2026, the International Capital Market Association (ICMA) published its new guidelines for issuers wishing to use this new format. This disclosure is an important first step towards the standardization of this instrument and establishes a definition that should be progressively accepted by the markets, both by issuers and investors, just like the Green Bond Principles, published in 2014. Unlike green bonds, for which strong and immediate environmental materiality is expected, assets financed by transition bonds only make sense if they are part of an ambitious decarbonization strategy by their issuer.

These "transition" bonds open up new perspectives for responsible investors: beyond financing "consensual" green activities, they now make it possible to support the energy transition of high-emitting companies and thus have a greater overall impact.

Data Centers and the Energy Transition: A New Sustainability Challenge

Driven by the expansion of cloud computing, artificial intelligence, and ever-growing data processing needs, the data center industry has established itself as essential infrastructure for the global economy. However, the sector's rapid growth is accompanied by mounting environmental challenges, positioning data centers as a key theme within sustainable finance.

Structurally High Energy Intensity

Power consumption remains the primary environmental concern for data centers. Their high energy intensity makes them particularly sensitive to electricity availability, grid constraints, and shifts in energy prices. According to the International Energy Agency (IEA, World Energy Outlook Special Report, April 2025), global electricity demand from data centers could more than double by 2030 to reach approximately 945 TWh—a level comparable to the current electricity consumption of Japan.

A Rapidly Evolving Global Regulatory Landscape

Data centers operate in an increasingly structured regulatory environment. In Europe and Australia, reporting requirements for energy efficiency and sustainability are becoming more stringent. In countries such as Germany and China, regulations are encouraging operators to source a portion of their consumption from decarbonized electricity sources.

In the United States, while the federal framework remains fragmented, concerns are emerging at the state level regarding the impact of data centers on electricity bills and power grids.

Water: An Increasingly Critical Sustainability Challenge

Beyond energy, water consumption for cooling systems is drawing growing attention. According to the IEA (World Energy Outlook Special Report, April 2025), a 100 MW hyperscale data center in the United States can consume 2 million liters of water per day, equivalent to the daily usage of 6,500 homes. These figures illustrate the growing materiality of water risk for the sector, particularly in regions already facing water stress.

The Role of Sustainable Finance in the Data Center Transition

Some operators are issuing green bonds to finance investments aimed at making their data centers more energy-efficient. However, the credibility of these instruments is closely tied to the robustness of the issuer's transition plan.

In parallel, utilities companies are central to financing the energy transition, especially through the investments required to upgrade electricity networks and roll out storage capacities.

Conclusion

As we enter 2026, the European sustainable bond market is maturing, characterized by increased selectivity, greater standardization, and heightened demands for environmental credibility.

Within this evolving landscape, Ostrum Asset Management leverages its recognized expertise in sustainable bond analysis and management, overseeing over €43 billion in assets under management with dedicated portfolio managers and analysts.

This structure enables us to identify the most relevant opportunities, transcending traditional formats. The progressive integration of European standards, notably the EU Green Bond Standard, enhances market transparency and supports an approach founded on in-depth analysis of issuance frameworks, transition pathways, and the materiality of financed projects. Ostrum Asset Management utilizes a proprietary methodology and tool for sustainable bond analysis, assessing both the issuer and the financed projects, to ensure the durable quality of each issuance.

Convinced that the energy transition cannot be limited to financing only already virtuous actors, Ostrum Asset Management pays particular attention to transition bonds, provided they are part of credible, measurable decarbonization strategies aligned with long-term climate objectives. This approach, combining rigorous selection, proprietary ESG analysis, and active dialogue with issuers, aims to support the transformation of the real economy while meeting the growing needs of investors with ESG-focused strategies.