Private Credit has moved to the forefront of market discussions, often associated with concerns over liquidity, asset quality and underwriting standards, as well as investor behaviour.

Yet behind the headlines lies a heterogeneous asset class whose risks and dynamics demand further investigation.

Importantly, not all Private Credit segments face the same challenges, nor do they carry the same risk profile. Recent scrutiny has focused on redemption risk from so called “semi-liquid” funds, further exacerbated by growing concerns around the asset class exposure to the software sector.

This analysis aims to cut through the noise and restore perspective. It also assesses the specific implications for insurance companies and banks on both sides of the Atlantic given the specific roles they play in the Private Credit value chain.

Private Debt, Private Credit, Direct Lending: mind the gap

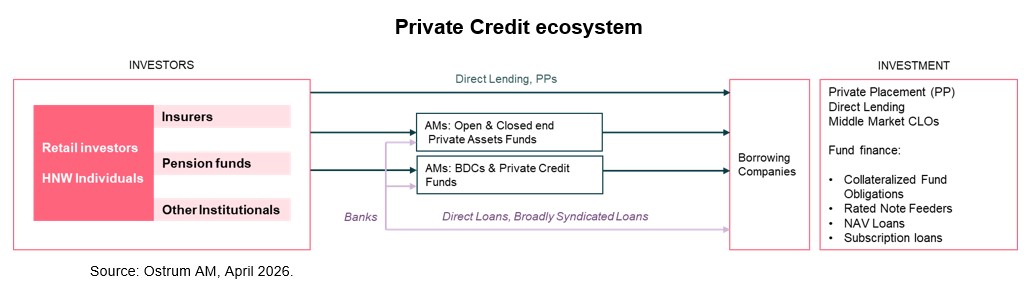

Private Credit is a subset of the Private Debt asset class, a much broader space, which also includes real assets financing such as commercial real estate, infrastructure, among many others.

There is no unique definition for Private Credit.

- Certain market participants limit its definition to direct lending to middle-market companies, asset-backed finance, and bespoke lending solutions to Investment Grade companies (Private Placements)

- Whereas others use a broader definition including any fixed-income security not traded on the public bond market, and not publicly rated (generally bearing a Private Letter Rating - PLR). Certain market participants would also include Broadly Syndicated Loans (BSLs).

Direct lending is the particular segment of Private Credit which makes the current headlines. It means private loans to middle market, Private Equity (PE) sponsored portfolio companies with sub-Investment Grade ratings (PLRs).

Direct lending goes a long way back, since the 80s, but it has significantly developed in the aftermath of the global financial crisis when banks, subject to more stringent regulation, partially stepped back from the space, and Alternative Asset Managers (Alt AM) stepped in, by partnering up with the Private Equity sponsors. The decade long low-interest rate environment until 2022 made the asset class even more attractive given returns were increased through additional leverage.

Their “more liquid peers” on the market are the Broadly Syndicated Loans (BSLs), also called leveraged loans or senior loans, and originated as part of private equity deals and invested by institutional investors. During the 2000s this corporate debt was securitised in structured credit vehicles such as CLOs (Collateralized Loan Obligation). Strong institutional investor demand for CLOs and the profits available to banks for structuring them fuelled demand for loans, thus increasing BSLs issuance.

In the Private Credit ecosystem, the relationships between end investors and the borrowing companies are numerous and multifaceted. Insurance companies and banks play a key role as transmission channel to the overall market of any real or perceived risk.

For one, insurers, namely life insurers, are seasoned underwriters of certain types of private debt such as Private Placements, or commercial real estate loans and these portfolios have been successfully tested through cycle. These illiquid, long-term assets have their place in a life insurer’s asset allocation as a natural match for its long term liabilities.

As far as Direct Lending is concerned, the Alternative Asset Managers (Alt AM) play now a central part as the middlemen between end investors, of which institutional investors such as insurance companies and pension funds are the most natural recipients for the asset class, and the borrowing companies to the other end. The most direct way for the alternative asset managers to source such loans is by nurturing strong relations with the private equity sponsors.

Many alternative asset managers are vertically integrated, in order to capture both the asset origination capability and the end investment platform. However, the move to private assets is not limited to asset manager-backed insurers (Apollo, Brookfield, Carlyle, Blackstone, KKR). Traditional life insurers are also expanding the asset origination capabilities either by investing in their direct platform or by setting up joint ventures with alternative asset managers.

Finally, banks continue to be at every level of the ecosystem: they are directly involved in broadly syndicated loans, and they are also involved in structuring increasingly complex investment vehicles, and of course, providing leverage to all participants.

Private Credit shift: rapid growth and expansion of semi-liquid funds

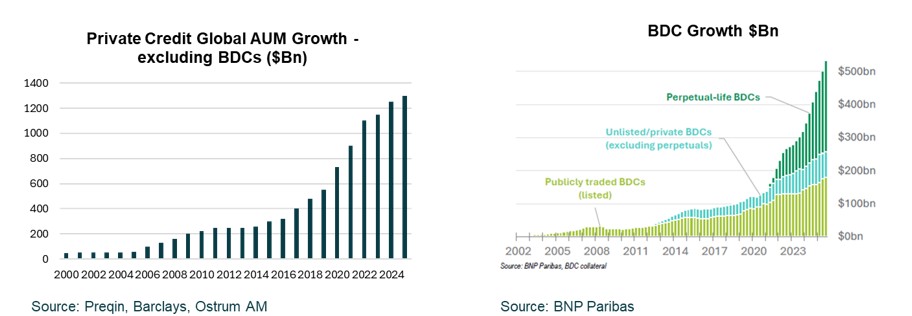

Growth in Direct Lending is positively correlated with the private equity funds growth during the low-interest rate decade. Many asset management firms (AMs) have effectively entered the Private Credit market in the aftermath of the global financial crisis, meaning they have not been tested through the cycle. Further, BDCs recent exponential growth, also helped by the expansion of investor base from institutional to individuals has moved AM focus from investing to deploying investors’ capital relatively quickly, rising risk for potentially more questionable underwriting standards.

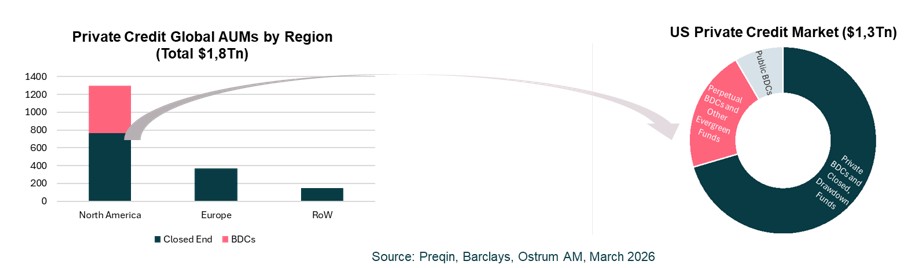

According to Preqin the Private Credit market including BDCs has reached a global size of around $1.8 trillion at in 2025, with growth overwhelmingly concentrated in North America, which now accounts for the bulk of global assets under management (≈ $1.3 trillion).

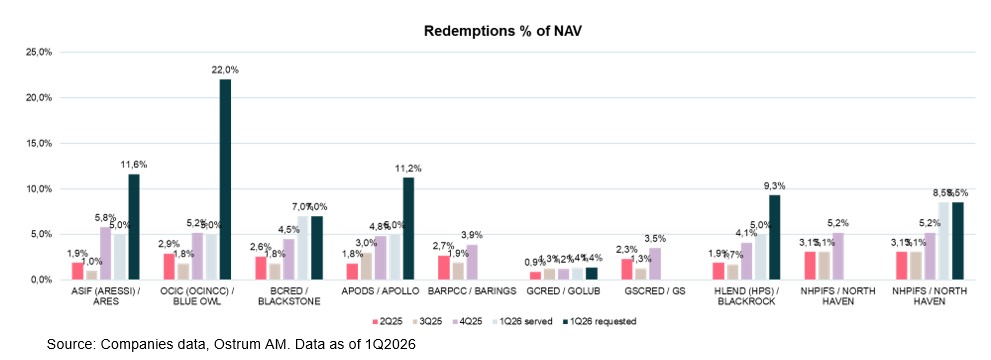

Beyond scale, the composition of the investor base has shifted. Private Credit has progressively opened to retail investors, who now represent around 20% of the investor base, particularly through perpetual BDCs and other semi liquid vehicles – which by their design offer periodic liquidity against hard to sell assets.

This introduces a new dynamic: higher sensitivity to investor sentiment and redemption requests. In periods of real or perceived stress, this mismatch between illiquid underlying assets and more frequent liquidity expectations namely from retail investors could amplify negative sentiment, thus fuelling further redemption requests.

In other words, even in absence of asset quality blow up, the design of the semi liquid investment wrappers may create a problem when the fund liabilities run out faster than any assets inflows.

Asset quality under pressure: Software concentration and portfolio markdowns

While we do not anticipate a massive asset quality blow up, signs of pressure do exist beyond most commented defaults of autumn 2025, and the most recent ones, the software maker Medallia and the dental service provider Affordable Care.

It is a fact that private equity backed portfolios exhibit a proportionally larger concentration to the Technology and Software sector, where there is growing concern about AI disruption risk. At a minimum, certain of these companies will see their earnings prospects downwards, thus impacting their equity values and their ability to fund at acceptable conditions over time.

For perspective, while technology sector accounts for only 4–5% of the US High Yield bond market, its share rises to 10–15% in the Broadly Syndicated Loans (BSL) market and reaches between 20–40% in direct lending according to Oaktree Capital, April 2026.

This shift has also coincided with more accommodative lending practices, including increased financing of unprofitable companies through ARR based loan structures (Annual Recurring Revenues) and a broader use of Payment in Kind (PIK)1 features, blurring the line between flexibility and delayed risk recognition.

With 2028 marking the next maturity wall for private equity portfolio companies, risks are likely to materialise unevenly. In an opaque market where public disclosure is limited, sentiment continues to dominate, making wider spreads and portfolio mark downs a more likely adjustment path in front of additional redemptions, than widespread defaults.

1Payment‑in‑Kind (PIK): interest capitalised instead of paid in cash.

Private Credit: A US centric risk for insurers today; may change in the future

Given their natural allocation to long term, illiquid assets in front of their long-term liabilities, life insurers could be seen as the first in line to be involved in any transmission channel of Private Credit risk to the rest of the financial system. However, there is a big offsetting factor in favour of insurance companies: if their asset - liability matching is done right, they are not expected to have a liquidity problem. They may just incur additional capital needs should the asset quality of the underlying loans deteriorate, whose real impact on insurer capital is a function of the size of the exposure at individual companies.

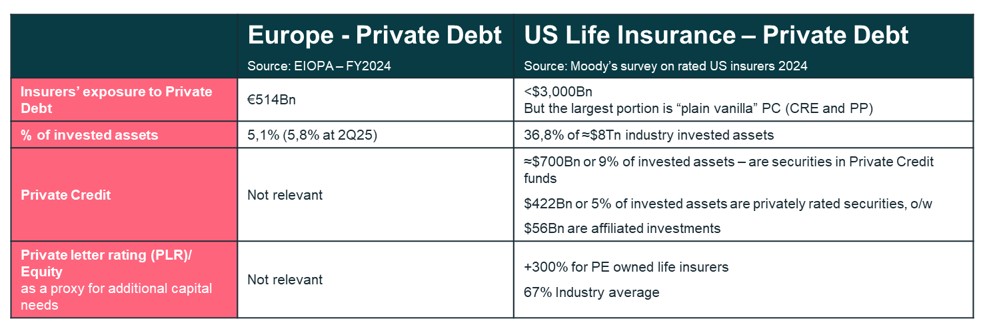

Starting with US. On the face of it, US life insurers’ exposure to private debt may be perceived as very large, in excess of $3tn, or close to 37% of industry invested assets. The largest share is “plain vanilla” though, well originated and tested through multiple economic cycles—most notably Private Placements (PP) and Commercial Real Estate (CRE) lending. This relative resilience was illustrated in 2023, when US insurers’ CRE portfolios displayed roughly half the delinquency rate observed in the broader market.

Within private debt, Private Credit is however a non negligeable portion. Around $700bn, or 9% of invested assets, is invested through Private Credit funds, while approximately $422bn (around 5% of invested assets or 67% of insurers equity) consists of privately rated securities (Source: Moody’s survey on rated US insurers 2024). This matters because privately rated (PLR) securities are the closest we can get to estimating the exposure to direct lending. Of note, the size of PLR is significantly higher, around 300% of their equity, for life insurers with strong ties to private equity platforms.

Private Credit does not represent a material risk for European insurers today. In Europe, insurers’ exposure to private debt remains limited, at about +€500bn, corresponding to roughly 5% of invested assets. Moreover, this exposure is concentrated among a small number of countries—mainly Dutch, French and German insurers - and is predominantly composed of traditional private debt instruments such as mortgage loans rather than Private Credit funds (source: EOPIA, 2024).

However, this may change in the future as Solvency 2 rules evolve to encourage insurers (through lower capital charges) to increase their allocation to securitisations – which are by construction the most common wrappers for Private Credit.

All in all, as of today, US life insurers are more exposed to valuation risk in a scenario of market stress than their European peers. While Private Credit has so far avoided widespread defaults, a tightening financial environment is more likely to translate into portfolio mark downs and therefore higher capital requirements for insurers, rather than immediate credit or liquidity events. This may change in the future, as European insurers may increase their allocation, as supported by the Solvency capital regulation.

US banks & Private Credit: less risk than the headlines suggest

Banks may be the other key transmission channel of any Private Credit related stress to the financial system. They effectively lend to all players within the Private Credit ecosystem, and they also face Private Credit funds as main credit counterparts when they transfer tranches of risk of their loan books through the so-called Synthetic Risk Transfers (SRT).

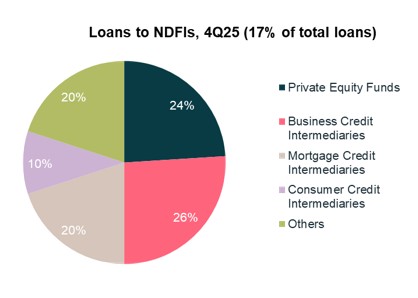

Again, starting with the US banks. The rise of Private Credit in the US has increased banks’ indirect exposure to the asset class, primarily through what is being regrouped under banks reporting, as loans to non depository financial institutions (NDFIs). Rather than lending directly to corporates, banks add leverage at the intermediary levels of the ecosystem, namely by financing vehicles such as private equity funds, Private Credit funds, business credit intermediaries and other specialised lenders.

As of Q4 2025, loans to NDFIs account for around 17% of total US bank loans, reflecting this structural shift in credit intermediation. However, this exposure should be put into perspective. NDFI lending is highly diversified across a wide range of counterparties with heterogeneous risk profiles, and exposures are generally well secured. Within NDFIs, Private Credit and BDCs fall under “business credit intermediaries”, which represent about 26% of NDFI lending, or roughly 4.4% of total bank loans on average.

As a result, US banks’ direct exposure to BDC related Private Credit remains limited, while underwriting standards and collateralisation continue to act as important mitigating factors. The key unknown remains however any unforeseen second order effects in case the leveraged wrappers do not perform as models assume, since so far they have not been tested in real conditions of stress.

European banks: Private Credit stays contained

In Europe, banks’ direct loan exposure to Private Credit and non bank financial institutions remains limited, reflecting a still highly intermediated financial system where banks continue to dominate corporate lending. The most exposed institutions include the large German, UK and French universal banks, with Private Credit exposure representing between 3% - 5% of their total lending —levels that remain manageable.

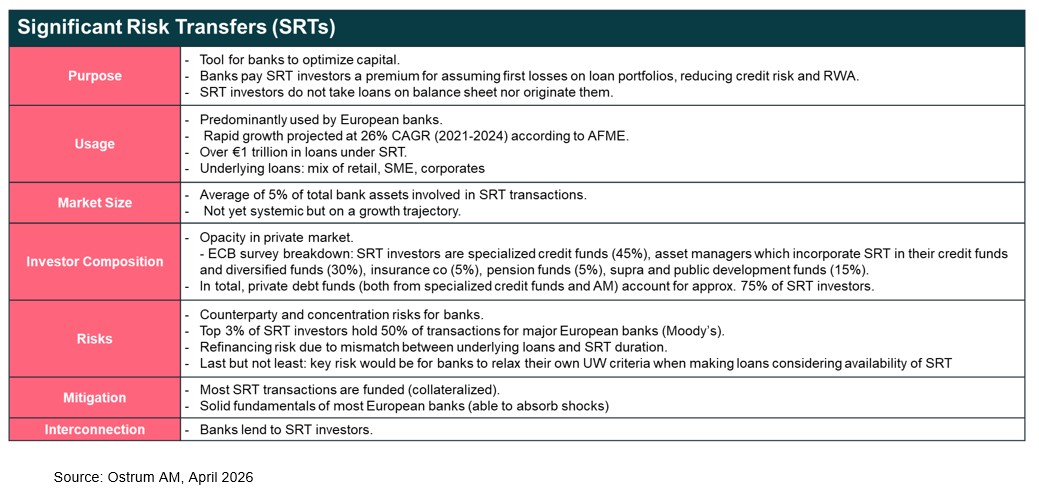

Beyond direct lending, European banks are increasingly exposed through counterparty risk in significant risk transfers also known as Synthetic Risk Transfer (SRT), where private debt funds act as major risk counterparties.

SRTs: Europe’s quiet risk transfer engine

Synthetic Risk Transfers (SRTs) are primarily a European phenomenon and play a growing role in banks’ capital management.

Structurally similar to CDS type instruments, SRTs allow banks to transfer the first losses of risk of loan portfolios to external investors, while retaining the assets on their balance sheets. These transactions are largely dominated by a relatively concentrated group of specialised Private Credit funds, with limited transparency at the market level.

Usage of SRTs varies significantly across European banks. While certain large European universal banks do use it, it is more curious to note that the largest users relative to their capital base, are second and third tier sized European banks, with more than 8% of their total loan books involved in SRT transactions. On average, SRTs provide around 45 basis points of regulatory capital relief, although the dispersion across banks is wide. Importantly, current data suggest that European banks are not overly reliant on SRTs as a primary capital management tool.

The underlying loan portfolios covered by SRTs are diversified, spanning retail, mortgages, SMEs and corporate exposures, which helps limit concentration risk. However, the investor base remains highly skewed toward Private Credit funds and specialised asset managers, raising counterparty and concentration considerations. While SRTs are typically funded and collateralised, their rapid growth and increasing interconnection with Private Credit markets warrant close monitoring - particularly as banks may be tempted to ease underwriting standards if risk transfer capacity remains readily available.

Conclusion

Private Credit is entering a phase of adjustment rather than disruption. While recent headlines have amplified concerns around liquidity, underwriting standards and valuation risk, the underlying dynamics point to a more nuanced reality. Stress in the asset class is likely to materialise through portfolio mark downs and higher spreads, rather than through a wave of defaults.

For banks, both in the US and in Europe, direct exposure to Private Credit remains limited and manageable. In the US, indirect exposure through NDFIs and BDCs represents only a small fraction of total loan books, while European banks continue to operate within a more intermediated credit model. Even in the growing SRT market, usage remains selective and capital relief modest, with no evidence of over reliance at this stage.

Insurers, namely US, as long term holders of private assets, are more directly exposed to valuation volatility than to immediate credit deterioration. Here again, dispersion matters: risks are concentrated in specific segments, structures and geographies. Europe, by contrast, appears structurally more resilient at this point but this may change in the future.

As Private Credit continues to mature and broaden its investor base, transparency, selectivity and disciplined underwriting will become key differentiators. Beyond the noise, the asset class remains an important component of long term portfolios, but one that now requires a sharper focus on structure, liquidity and capital implications. Private Credit in its current forms has not been tested at scale and it remains to be seen if assets ultimately owned by the end investor will behave as models currently assume.