Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum’s views on the economy, strategy and markets.

The CIO letter

When the Fed and the ECB go all-in

Since our last letter, there have been three developments. On the one hand, growth has tended to hold up a little better than expected. On the other hand, inflation, despite our high expectations, remains and continues to surprise upward. As a result, the tone of the central banks has tightened considerably, especially for the two main ones, the ECB and the Fed.

The first consequence is regional disparity. The overall movement towards higher rates persists but is becoming more disparate. While the Fed and the ECB are still very aggressive, many central banks, especially in emerging countries, are slowing the uptrend. We are therefore witnessing the emergence of divergence in monetary policy.

Second consequence, a permanently higher trajectory. The persistence of inflation also means that the central banks will be patient next year before declaring victory. A rapid fall in inflation next year, plausible in view of the large base effects, would not induce immediate easing of monetary policy. The consequence is important for the curves since in this case the long rates should therefore be established at a higher equilibrium level in a sustainable way.

Risk assets remain, risk premiums are clearly high, even very high in some cases. This is probably excessive in view of our central scenario, a limited recession at the end of the year. There is therefore an important pool of medium-term performance. The catalyst will, in all likelihood, be the “pivot” of the Fed and ECB, a sign that inflation is finally on the downside and the monetary tightening is behind us.

In the meantime, the feeling should nevertheless remain very cautious by this winter with an energy crisis that can worsen, become much more serious and impact the growth profile much more. An extreme scenario that is not our central scenario, but obviously plausible. Such a shock, as long as it is not certain that it has been avoided, will weigh on investors' risk appetite and limit any marked rebound.

Economic views

Three themes for the markets

-

Monetary policy

Fed and BCE are still on a very fast tightening pace. This raises the issue of the terminal rate, and therefore the duration of the tightening. The other question is whether the central banks will backtrack next year if inflation subsides. Given the shock we’re going through, it’s unlikely.

-

Inflation

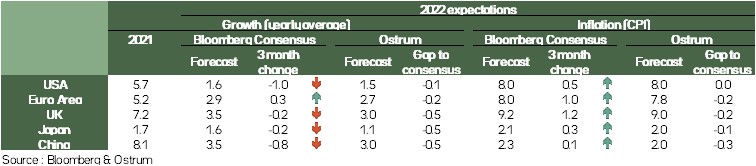

Once again, inflation surprised by its level and resilience on both sides of the Atlantic. While inflation is expected to decline, the underlying trend remains too dynamic to be consistent with the central bank target. In Europe, the trend will be towards 3 % by the end of next year, giving an average of more than 5 % over the year as a whole

-

Winter is coming

A sword of Damocles, the energy risk in Europe remains very worrying, even if it is not our central scenario. A Russian gas shutdown and harsh winters could lead to a loss of 2-4% of European GDP. This potential risk will continue to weigh on the markets until this winter.

Key macroeconomic signposTS : activity

- The main source of concern at the macroeconomic level is the sharp decline in purchasing power resulting from the surge in inflation since spring 2021.

- Europe is more affected than the US, primarily because of a greater sensitivity of inflation to energy prices but also because nominal wages have not risen in a similar way.

- In the US, tensions on the productive apparatus and on the labour market after the Biden recovery were such that wages increased strongly (currently almost 7% or -1.7% excluding inflation). In the Eurozone, there was no revival or similar tensions, nominal wages rose by 2.4% and real wages fell by nearly 6%.

- This is also why many measures have been announced in Europe to limit the impact of rising energy prices.

- The immediate consequence of this decline in purchasing power is the significant change in orders sent to enterprises, both in the euro zone and in the US, while stocks have recovered. This is the reverse of spring 2021. The pressures on activity are being reduced and should eventually translate into lower nominal pressures and a reduction in labour market imbalances.

- That’s what Jay Powell, the head of the US central bank, wants. The Fed will continue to raise rates in order to keep activity below trend and reduce labour market and wage pressures. The aim is to limit the persistence of inflation, which mainly involves wages.

- This translates into lower production expectations. We have here the ingredients of a likely recession in the developed countries at the turn of the years 2022-2023.

Key macroeconomic signposts : inflation and budgetary policy

The acceleration of inflation has been marked since spring 2021. The price rise is now close to the 8-10% segment. France is an exception. This reflects the early introduction of the energy shield. Japan is also on a particular trajectory. This is a result of Japan’s structurally low inflation rate, observed well before the energy crisis. This also reflects the government’s constraints on certain prices, including mobile subscriptions, whose impact has been dramatic since spring 2021.

In the short term, we see that the price of raw materials is falling. We see it in the price of oil. The 2022 price is close to the 2021 price. This will significantly reduce its contribution to inflation. We can also see it on the price of industrial metals, whose price in dollars is now below that of 2021.

Prices paid in manufacturing tend to go down. That’s what the US price index shows. This indicator is now below the average seen in the previous cycle. This is a major change.

Such a situation is not observable in Europe because of the very strong tensions on the price of energy, mainly the price of gas and electricity, much less marked in the US. The equivalent chart in the Eurozone is much less in decline and companies are still experiencing significant upward pressures. This is why discussions are intensifying on a change in the rules in force in the setting of electricity prices.

Demand is slowing and commodity prices are slowing. This is a good signal for a future reduction in inflation. In the United States, there remain the tensions on wages that the Fed wants to fight and in Europe the tensions on the price of energy that the European Commission is attacking. In both cases, the objective is to limit the persistence of inflation over time in order to reduce its cost.

Monetary policy

Central banks determined to fight inflation

- Fed: restrictive policy for a while

The Fed is raising its key rates sharply to quickly bring them back into restrictive territory to combat "way too high" inflation and a tight labor market. The Fed should thus raise its rates for the third consecutive time by 75 bp, on September 21, to bring the Fed funds range to [3%-3.25%] and continue to raise them between now and the end of the year to a slightly more moderate pace. During the Jackson Hole speech, Jerome Powell made it clear that to contain inflation expectations, the Fed was going to maintain a restrictive policy for some time at the risk of weighing on growth. It will also accelerate the reduction in the size of its balance sheet. We anticipate rate hikes of 75bp, 50bp and then 25bp by the end of 2022.

- ECB: again +75bp in October?

The ECB raised rates by 75bp on September 8, after +50bp in July, and expects to continue raising them in future meetings due to "far too strong" inflation expected to remain above the 2% target for an extended period. While the growth outlook has been revised downwards, the inflation outlook has been revised sharply upwards with, in particular, an expected inflation rate of 2.3% in 2024, against 2.1% expected in June. With the deposit rate now at 0.75%, the ECB has abandoned the tiering mechanism on bank reserves. It also temporarily suspended the 0% cap on government deposit remuneration. The size of the balance sheet remains unchanged with continued reinvestments under the APP and flexibly for the PEPP. We anticipate a deposit rate of 1.75% at the end of 2022. Discussions regarding a possible reduction in the size of the balance sheet via lower reinvestments concerning the APP could start in October.

Strategic views

Change of world?

Synthetic market views: the end of a trend?

After the violent rate movement we have experienced, it seems to us that a very large part of the cycle of rate hikes is now anticipated by the markets. As such, the long part of the curve should not rise very sharply. We neutralize the majority of our positions with a slightly negative view.

Similarly, the recent sharp drop in inflation breakeven points on the short end of the curve, especially in the United States, encourages us to take minor bets on linkers that present a smaller opportunity.

As a result, several heavy trends in rates are fading.

Allocation recommendations: the unknown

While valuations as a whole are attractive, especially in light of our limited recession scenario, the prospect of a much darker trajectory should keep pressure on risk premiums.

However, some asset classes seem attractive. We are constructive on the HY which will be supported by technical factors. Similarly on emerging markets, we are already seeing a compression of spreads on certain names that were heavily penalized.

Asset classes

G4 rates

- At Jackson Hole, the Fed talked tough on inflation, so that a 75bp move on Sept. 21 is fully priced in by markets. Fed funds should reach 4% in coming quarters and gradually raise the floor for long-term rates.

- The ECB hiked rates by 75 bps in September and expects further hikes in the near future. The shortage of collateral weighed on Bund yields, but high inflation and the resilience of growth argue for higher bond yields.

- The BoE is projecting double-digit inflation and will continue to tighten, notably by selling Gilts. A short position is justified. The BoJ is still resisting market pressure to change its monetary policy.

Other sovereigns

- In addition to the interest rate policy, the TPI and the flexibility offered by the reinvestments of the PEPP made it possible to control sovereign spreads. Italian political risk does not seem to be integrated and militates for an underweighting of construction and public works.

- The spreads on the core countries show some stability which argues for a neutral position vis-à-vis the risk-free Bund benchmark.

- The trend reversal on rates since August has become widespread in the G10 where central banks are fighting inflation. Swiss and Swedish rates are most underweighted.

Inflation

- Inflation (8..3% in August) is slowing in the United States thanks to energy, but underlying inflation remains sustained (>6%). The Fed's offensive tone is nevertheless weighing on inflation breakevens.

- In the euro zone, inflation exceeds 9%. Monetary tightening and the desire to control electricity prices have however reduced inflation expectations. Current dead spots are good entry points.

- In the UK, the new government will seek to limit the impact of energy. Double-digit inflation is priced in by the markets. We favor neutrality.

Credit

- The credit market offers attractive valuations, but the caution of investors and the competition from higher sovereign bond yields point to further widening in spreads.

- The primary market activity heated up in mid-August. New issue premiums are very high. The outflows from credit funds and the end of CSPP purchases since July have created an unfavorable backdrop for credit spreads.

- Volatility on high yield is considerable, the crossover oscillates wildly between 500 and 600 bp. The primary market remains closed and risk appetite is uncertain. Spreads should nevertheless tighten from high levels.

Stock market

- Slowing growth is not preventing resilience in profit margins. Earnings revisions remain mostly positive in Europe despite the caution of companies and equity investors.

- Valuation multiples are low (11.8x at 12 months) below their long-term average but the median or cyclically adjusted PE is higher. The expected dividend yield is elevated at 3.8%. US investors continue to sell European stock markets.

- Markets are jolted by monetary tightening, the energy crisis and resilient earnings. The low implied volatility is somewhat paradoxical. We forecast Euro Stoxx 50 to be around 3,600 at the end of the year.

Emerging

- The EMBIGD spread has tightened well below 500 bp against Treasuries. Attractive valuations have enabled an improvement in EM fund inflows into the asset class. We are shifting the expected spread range down to between 460 and 530 bps.

- Fund outflows have eased somewhat, and primary market activity remains low, but market liquidity is improving at the margin. High yield commands a very high premium against the IG.

- The countries in difficulty are supported by the IMF and the WB, so that the credit metrics are maintained. We expect the gap between EM HY and EM IG spreads to narrow.