Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum’s views on the economy, strategy and markets.

The CIO Letter

The steepening of the curves is derailing the markets

Growth and employment remain very well oriented in the United States. US GDP even accelerated between July and September, erasing fears of recession. Conversely, weak consumption is weighing on European growth. The Chinese situation raises fears of a Japanese-style stagnation despite encouraging data recently. In this three-speed world, the dollar remains the safe haven. The yen has fallen to record lows and rumors of intervention abound in currency markets. Some emerging currencies weakened at the end of the quarter.

The third quarter close led to profit-taking on many markets as tensions intensified on long-term rates. The restrictive bias of Central Banks continues as risks to price stability increased with the bounce in oil prices. Monetary authorities will maintain high interest rates until mid-2024.

That, the tragic events in the Middle-east have caused a rally on risk-free bonds. The run-up in Long-term bond yields thus paused in the United States. Leaving aside the difficult geopolitical situation, the US federal deficit above 7% of GDP justifies a higher term premium, which weighs on all financial assets. The T-note is driving the yield on the 10-year Bund higher despite a lackluster economic situation in the euro area. Credit spreads, including high yield and emerging markets, are starting to respond to monetary tightening. European stocks are also hit by the rise in long-term rates. The upcoming third quarter earnings publications will set the tone for the end of the year.

Economic Views

Three themes for the markets

-

Monetary policy

The Fed postponed its last rate hike until November. However, the median dot indicating the Fed funds level for 2024 was revised upwards by 50 bps to 5.1%. The restrictive bias will be maintained as long as inflation does not converge sustainably towards the 2% target. In the euro area, the status quo on rates should prevail but it is worth bearing in mind that ECB balance sheet policies will continue to restrict liquidity. The BoJ intervenes to stem upward pressure on 10-Yr yields. The strength of the dollar forces emerging market central banks to remain cautious.

-

Inflation

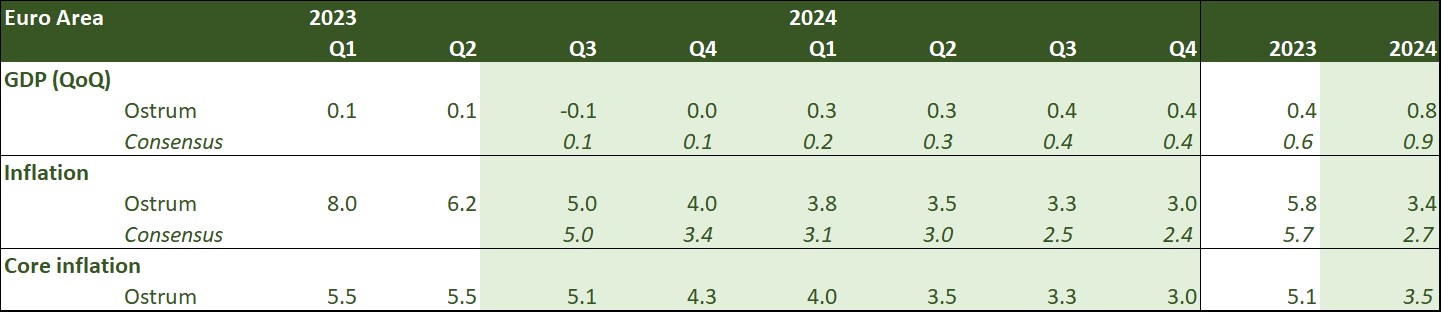

The surprise came from the euro area, where inflation decelerated to 4.3% in September after 5.2% in August, driven by service prices. In the United States, energy prices are delaying the return to the 2% objective. Furthermore, the housing shortage still weighs on the cost of living. The “input prices” components are on the rise again in the September surveys with the rebound in energy prices. Saudi Arabia has drastically tightened crude supply (by 2 m/bpd), helping to keep prices high.

-

Growth

The tightening of financial conditions should weigh on the provision of credit to the real economy. This is particularly the case for the euro area, where the latest publications indicate a slowdown in domestic demand. Growth is more sustained in the United States, thanks to household consumption. In China, activity stabilized at the end of the quarter, thanks to fiscal measures. However, real estate remains the main obstacle to a stronger Chinese recovery.

Key macroeconomic signposts : United States

- The US economy is moving towards a soft landing between October and March after a very strong 3Q 2023.

- Growth is expected to exceed 3% in 3Q 2023 thanks to consumption. Disinflation is now limited by the rise in gasoline prices even if wage increases allow for gains in purchasing power. Employment is slowing. Household demand will be weaker in 4Q 2023 with the resumption of student debt repayments (-0.2/0.3 pp of disposable income). The revised data shows a savings rate (5.2%) slightly higher than the first estimate.

- Housing investment is resuming after a long period of contraction. This creates consumption needs (equipment, furniture).

- The public deficit increases with the reduction in taxes paid by households (lower capital gains realized in 2022). The deployment of the CHIPS Act also leads to an increase in federal spending and investment in structures (factories). Spending on business equipment is growing limited with the exception of technology. Accelerating investment in AI should translate into more investment in R&D.

- The external balance is much better than expected in the context of solid internal demand.

- Oil production responds to rising prices (+400k bpd in September).

Key macroeconomic signposts : Euro area

- Growth was almost sluggish in the first half and should remain subdued in the second part of the year.

- Internal demand is affected by the increasingly strong impact of the significant monetary tightening carried out by the ECB and the continued high inflation while foreign trade is suffering from weak global demand.

- In this context, August retail sales raise fears of a negative contribution of consumption to GDP growth in Q3.

- Surveys carried out among business leaders reveal the continued contraction of activity in the manufacturing sector and the spread of this weakness to the services sector.

- The labor market remains well oriented with an unemployment rate at a historic low of 6.4% in August in the Euro zone.

- However, job creation is starting to slow down and the employment component of surveys carried out among business leaders has declined significantly. Faced with the drop in their orders, business leaders are becoming more cautious when it comes to hiring.

- Business investment should nevertheless continue to benefit from NextGeneration EU funds and the need to invest in renewable energy.

- Inflation continues to slow: 4.3% in September, after 5.2% in August, and 4.5% for core inflation, after 5.3% in August.

- Wages are slowing more slowly than inflation, which should support purchasing power and partly offset the impact of weaker dynamics in the job market. Negotiated wages increased by another 4.3% in T2 compared to 4.4% in T1.

Key macroeconomic signposts : China

- Chinese economic activity is showing encouraging signs. Economic policies have helped stabilize activity, although weaknesses persist in the export sector (geopolitical tensions) and the private sector.

- The recent data of the Golden Week, show a recovery of domestic and international tourism.

- However, real estate remains the main drag on the consumption recovery.

- Real estate is no longer a countercyclical factor on which the authorities rely to stimulate activity. However, the sector is expected to stabilize thanks to support measures for the sector.

- The new economy now represents 1/3 of the Chinese economy according to the Caixin indicator.

- The PBoC is expected to continue lowering its minimum reserve rates to further support the recovery.

- Adding the previous rate cuts, the effect on Chinese growth is expected to materialize in the coming quarters.

- We have revised our Q3 growth forecast downwards and expect a gradual rebound in growth.

- However, to significantly raise our growth forecasts, China must restructure the debt of local government financing vehicles.

- A new finance minister has been appointed to manage local government debt. This is a positive signal of the authorities' willingness to reform fiscal policy.

Monetary Policy

Last Fed hike in November before a prolonged status quo

- Fed: +25 bp expected in November and status quo until Q2 2024

On September 20, the Fed kept its rates unchanged and left the door open for a final increase by the end of the year. Growth prospects have been revised sharply upwards, the unemployment rate has been revised downwards and inflation is expected to remain high. In this context, the median forecasts of FOMC members continue to signal a rate hike by the end of the year. More importantly, smaller rate cuts are expected in 2024 and 2025 signaling rates will remain higher for longer. The Fed is expected to raise rates by 25 bps in November. - ECB: A prolonged status quo

On September 14, the ECB raised rates by 25 bps and suggested that the cycle of rate hikes was over. She insisted on the need to maintain rates at this restrictive level for a certain period of time to cope with inflation that will remain “too high for too long”. If the status quo remains in place, monetary policy will become more restrictive through balance sheet reduction. This will take place via the continuation of TLTRO repayments (525 billion euros by the end of 2024) and the end of reinvestments within the framework of the APP (332 billion euros between October 2023 and September 2024). The ECB reiterated that it will continue reinvestments under the PEPP at least until the end of 2024. - Incomprehensible policy of the BoJ

While the BoJ brought more flexibility to the fluctuation band governing the 10-year rate at the end of July, by allowing daily purchases at a fixed rate of 1%, it is increasing purchases of government bonds to limit the increase in the 10 year to 0.80%. This takes place at the risk of putting more pressure on the yen and justifying intervention on the part of the Ministry of Finance to limit its depreciation. The yen occasionally crossed 150 against the $ on October 3.

Market views

Asset classes

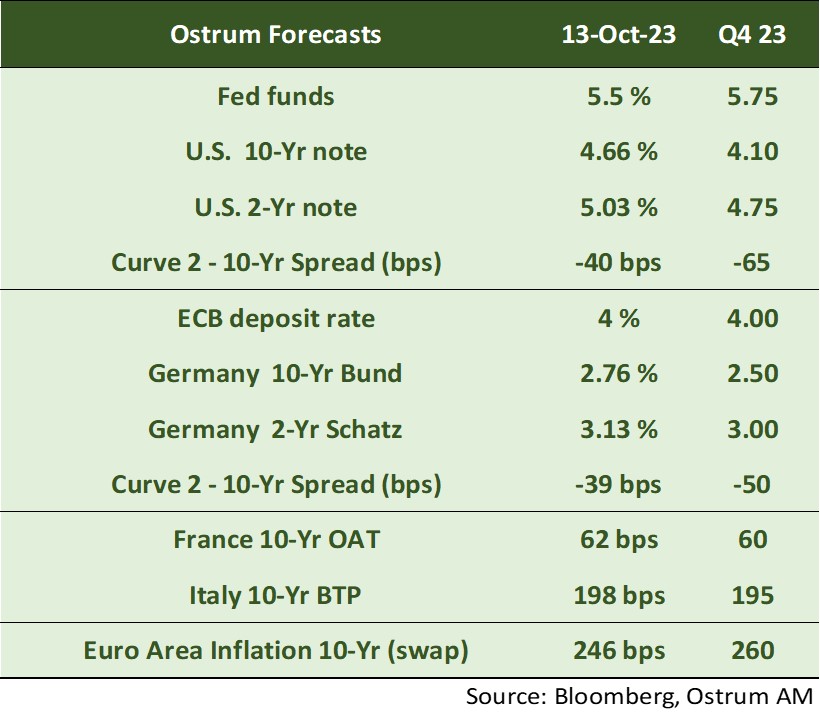

- US rates: The Fed is likely to raise rates to 5.75% and leave rates unchanged through mid-2024. T-note note yields are forecasted to drift lower to 4.10% by year-end.

- European rates: the ECB will maintain status quo at 4% on the deposit rate until mid-2024. The Bund yields should trade sideways amid slower economic growth.

- Sovereign spreads: valuations are rich considering the challenging backdrop for public finances in both France and Italy. Ratings could be under pressure.

- Euro zone inflation: ECB monetary tightening and lower medium-term inflation forecasts should weigh on breakeven inflation over the months to come.

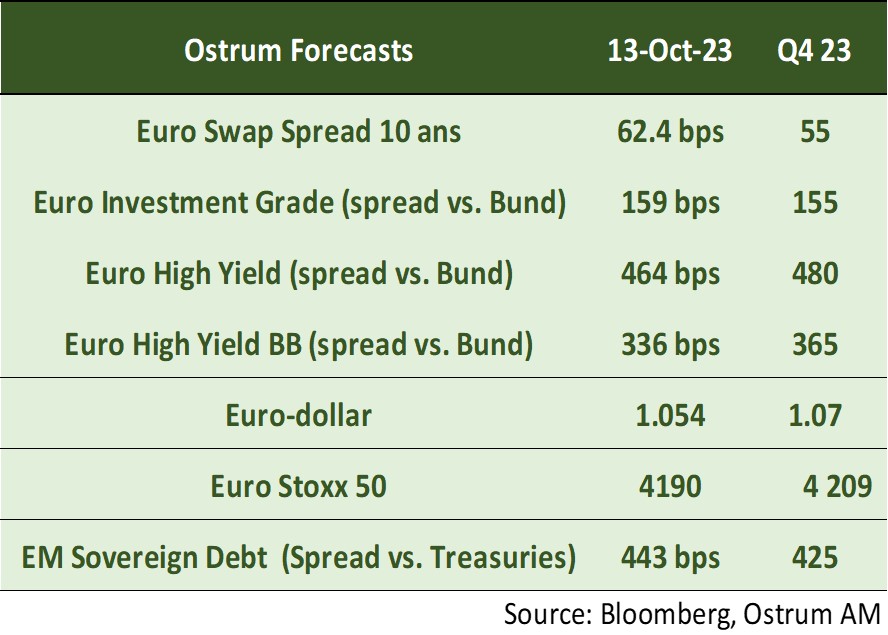

- Euro credit: IG credit spreads should remain broadly stable. High yield spreads are forecasted to widen given the richness of the single-B segment.

- Foreign exchange: the euro should trade sideways around 1.07 as ECB tightening is offset by slower growth and declining terms of trade.

- Equities: sideways drift at the end of the year reflecting slightly lower margins.

- Emerging debt: spreads have been under some pressure but remain near our year-end target.