Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum’s views on the economy, strategy and markets.

The CIO Letter

The Fed’s pivot

The monetary status quo announced by the Fed may seem premature given sustained growth and inflation above target. The political backdrop in the United States, and the risk of government shutdown, may have weighed on this decision, especially as fears about American debt resurface with the downgrade of the rating outlook communicated by Moody's. The question of debt does not spare the euro area, especially as economic stagnation is expected to continue into the 4th quarter. In China, it is the real estate debt overhang which requires public intervention to correct, or limit, the structural slowdown in growth.

On bond markets, the quarterly refinancing of the US Treasury was well received by market participants. The 10-year yield around 4.50%, however, remains subject to the risk of fiscal slippage. The Bund is partly driven by the T-note despite the reduced net supply of German bonds and a mediocre economic growth in the euro area. Swap spreads have tightened significantly, even as the looming year-end may fuel the search for collateral. Sovereign spreads have increased. In Japan, the Bank of Japan is leaning against the rise in 10-year bond yields towards 1% but market intervention comes at the cost of a weaker yen.

On risky assets, the surprising absence of volatility in a troubled international context (Middle East, Ukraine) is a boon for carry strategies. Credit spreads have stabilized around 100 bps against swap. High yield benefits from a low default rate. On the other hand, Q3 profit publications reveal significant disappointments in turnover, undoubtedly a harbinger of a deterioration in pricing power.

Economic Views

Three themes for the markets

-

Monetary policy

“Pause” for the main Central Banks, but dovish bias in the Central Banks of emerging countries. Jerome Powell does not rule further rate hikes if necessary. In the euro area, in addition to the status quo on rates, the debate is shifting to the size of the balance sheet. The winding down of the APP continues but the ECB may aim at keeping ample reserves in the banking system. The BoJ will now tolerate 10-year JGB yields slightly above 1%.

-

Inflation

The disinflation process continues, especially in the euro area. Inflation slowed to 2.9% in October from 4.2% a month ago, reflecting favorable base effects from energy prices. On the other hand, core inflation showed greater persistence at 4.2% versus 4.5%. In the US, inflation is also trending down as the CPI rose 3.2% from a year ago in October and core inflation slowed to 4%. It is worth noting that some food prices have picked up. Food inflation could rebound further due to a strong El Nino effect.

-

Growth

US GDP growth was strong at 4.9% annualized in Q3, driven by household consumption and housing investment. On the other hand, euro zone GDP contracted by -0.1% in Q3, led by Germany, whose GDP contracted by 0.1%. French GDP recorded a modest increase of 0.1% GT. Tighter financial conditions are weighing on European domestic demand. In China, the government announced a 1 trillion-yuan issue to allow real estate developers to repay their debts.

Key macroeconomic signposts : United States

- The US economy is moving towards a soft landing between October and March after a very strong 3Q 2023.

- Growth reached 4.9% in the 3rd quarter. The stock effect boosts growth by 1.3 pp, but restocking should be reversed at the end of the year. Consumption is very strong and the gain for the 4th quarter is already 1%. The slowdown in employment, the resumption of student debt payments and a lull in demand for durable goods should bring consumption back towards 2% growth.

- The public deficit is very significant, around 7% of GDP for the 2023 fiscal year. Another stop-gap bill has postponed the risk of shutdown to mid-January.

- Investment is less well oriented despite the high level of self-financing. Equipment spending has contracted, R&D is less dynamic. Spending on structures has stabilized after the sharp increase linked to federal support (IRA, CHIPS).

- The outside world has zero contribution thanks to exports. Internal demand does not create an excessive deficit as in the past.

- Housing investment is on the rise again. Despite the tightening of credit conditions, the lack of stock on the existing market is stimulating demand for new homes.

- Inflation is showing signs of persisting as housing costs rebound. Salary increases range between 4 and 6% according to surveys, which is probably incompatible with inflation at 2%.

Key macroeconomic signposts : Euro area

- Growth in the euro area is sluggish. Internal demand is affected by the increasingly significant impact of the ECB's strong monetary tightening and the continued high inflation while foreign trade is suffering from weak global demand.

- Surveys carried out among business leaders reveal the continued contraction of activity in the manufacturing sector and the spread of this weakness to the services sector.

- Although the unemployment rate has remained close to the historic low (6.5% in September) in the Eurozone, job creation is slowing, and the employment component of surveys carried out among business leaders has declined significantly. Faced with the drop in their orders, business leaders are becoming more cautious when it comes to hiring.

- However, wages should slow down more slowly than inflation, which will help to partly offset the impact of weaker dynamics in the job market.

- Business investment should nevertheless continue to benefit from NextGeneration EU funds and the need to invest in renewable energy.

- A slow recovery should begin in 2024 and more particularly in the 2nd half of the year due to a less significant impact of the monetary tightening carried out by the ECB, the increase in real incomes and a strengthening of world trade.

- Inflation will continue to slow down and remain high. It stood at 2.9% in October, after 4.3% in September, and 4.2% in October for underlying inflation, after 4.5% the previous month.

Key macroeconomic signposts : China

- GDP growth rebounded in Q3 to 1.3% GT, or 4.9% GA, allowing China to approach its 5% target for this year. We were rightly more optimistic than the consensus and we are not changing our forecasts at this stage.

- Indeed, the latest S&P global PMI and Caixin surveys for the month of October indicate a stabilization of activity. Foreign trade data indicate a rebound in imports, particularly in raw materials, likely reflecting a recovery in the manufacturing sector supported by massive investment.

- The measures announced at the Central Working Conference on the financial sector aim to avoid a systemic financial risk related to the real estate crisis. This involves maintaining ample liquidity to allow for low financing costs and optimizing the debt structure of local and central governments. The issue of 1 trillion yuan for local governments will allow them to repay their debts. On the other hand, this could lead to tensions in the interbank market. We continue to expect a decline in the reserve requirement rate by the end of the year that should support activity.

- To avoid contagion to other real estate developers, the government has for the first time provided financial support to a good quality developer, Vanke.

- The Chinese authorities want to replace the real estate sector with the manufacturing sector, as a new engine of growth. Authorities are targeting green and emerging technology sectors, such as semiconductors.

- However, the United States, Europe and Asia have also invested heavily in these sectors limiting the country’s growth potential.

- China needs to strengthen its domestic consumption to return to higher growth rates.

Monetary Policy

The Fed and the ECB have probably finished their rate hike cycle

- Fed: Status quo extended

On November 1, the Fed left its rates unchanged for the second time in a row, leaving the door open to a possible final increase. Despite stronger than expected growth, a still robust job market and high inflation, the Central Bank is giving itself time to understand the effects of the strong monetary tightening (+525 basis points) on the real economy. Monetary policy also continues to become more restrictive through the continued reduction in the size of the balance sheet. The status quo on rates should remain in effect in the first half of 2024. - ECB: Maintaining rates at this restrictive level sufficiently long enough

After 10 consecutive rate increases (+450 bp in total), to bring the deposit rate to the historic high of 4%, the ECB left its rates unchanged on October 26. Christine Lagarde reiterated the need to maintain rates at this restrictive level for a certain time to cope with inflation that must remain “too high for too long”. Monetary policy will continue to become more restrictive through balance sheet reduction with TLTRO repayments and the end of reinvestments under the APP. The ECB has reiterated that it will continue to reinvest redemptions coming due under the PEPP at least until the end of 2024. We do not expect a rate cut before the second half of 2024. - The BoJ: one of a kind – RBA: a test case ?

The BoJ is the only major central bank to maintain an ultra-accommodative monetary policy. However, it made a new technical adjustment to its yield curve control policy. The RBA (Reserve Bank of Australia) for its part raised its rates after opting for the status quo for 4 consecutive meetings. Inflation that was more persistent than expected led it to make this new increase.

Market views

Asset classes

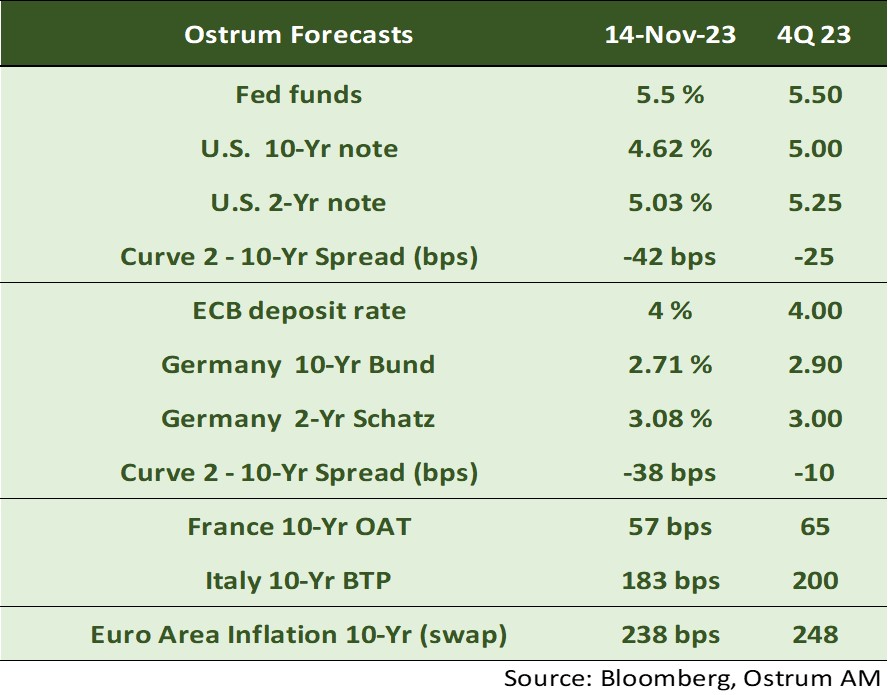

- US rates: The Fed will likely leave rates unchanged at 5.50% through mid-2024. T-note note yields may resume rising by year-end.

- European rates: the ECB will maintain status quo at 4% on the deposit rate until mid-2024. The Bund yields should drift higher despite economic stagnation.

- Sovereign spreads: spread valuations are rich considering the challenging backdrop for public finances in both France and Italy. Ratings could be under pressure.

- Eurozone inflation: breakeven inflation rates should rise as long-term yields rebound towards the end of the year.

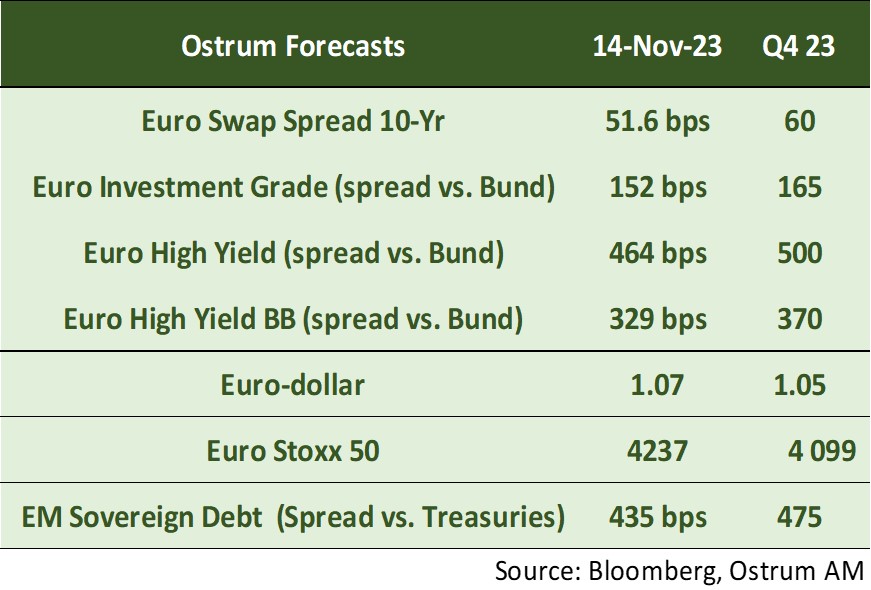

- Euro credit: IG credit spreads should remain broadly stable. High yield spreads are forecasted to widen given the richness of the single-B segment.

- Foreign exchange: the euro should trade lower around $1.05 due to slower growth.

- Equities: weaker sales growth should weigh on equity prices in the final month of the year.

- Emerging debt: spreads have been under some pressure as bond yields resume rising.