Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum’s views on the economy, strategy and markets.

The CIO Letter

The other side of the valley?

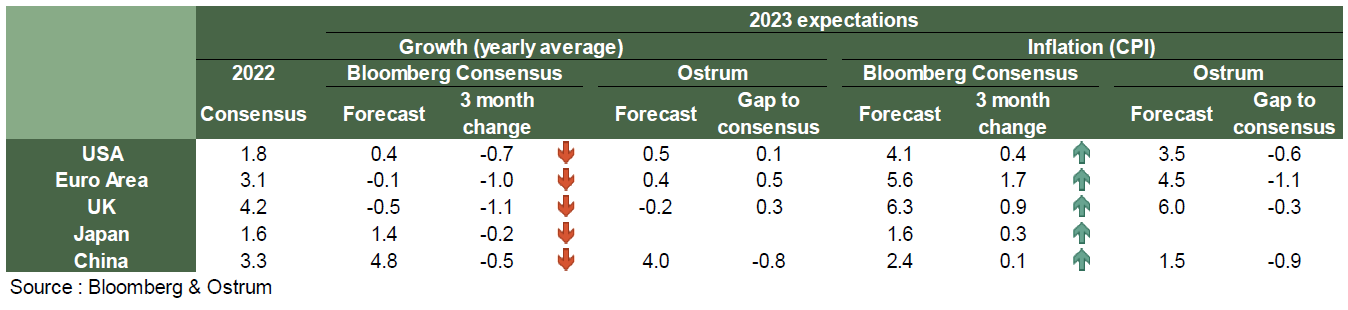

The economic data tend to validate our economic scenario. Activity, if it goes down, doesn’t collapse. The idea of a recession of limited magnitude, less than a point of decline still seems relevant. Inflation figures, on the other hand, still show considerable inertia and suggest a slow decline next year. Therefore, a mediocre economic situation.

In this gloomy context, the recent good performance of risky assets may surprise.

The first reason is the famous central bank pivot. As expected, the pace of increases is slowing in the world, especially with the Fed and ECB signaling smaller future increases. However, the persistence of inflation will not help to rebase rates quickly, so the “pivot” is only the expectation of a future rate stabilization, not a decline.

The second reason is related to the much more pessimistic implicit market scenario than ours, notably with risk premiums at very high levels, particularly on credit. Mediocre economic news is also better news than expected by the market, and therefore paradoxically a support.

Where are we going? The question then is whether the market will be short-sighted and look at the recession we are entering, or whether it will look at “the other side of the valley”, the recovery expected next year after a limited recession.

We think that the rise in long rates is largely behind us the curve should remain very flat next year and volatility should finally come down with the end of the rate hikes. Meanwhile we remain cautious, the upward adjustment is not yet finished. On risky assets our argument of a very comfortable risk premium has eroded with the recent rally while the sword of Damocles of a serious crisis this winter is not excluded. In the short term, therefore, caution should be exercised even if current levels are still entry points in the future.

Economic Views

Three themes for the markets

-

Monetary Policy

Central banks are signaling a slowdown in rate hikes, which has partly reassured markets. However, we remain focused on our vision: the increases are not over even if they slow down. And rates will remain persistently high over the next year. The “pivot” is therefore all mild one.

-

Inflation

Some very early signs tend to show a possible inflection point: raw materials, industrial prices in China, etc… All this will take a long time and the European figures in particular remain far too dynamic for the comfort of the central banks.

-

Recession

Economic data continues to show some resilience, although a recession seems inevitable. The question then becomes the extent of this recession, when markets have valuations consistent with an extremely black scenario. It is unlikely that we will have a clear answer to this question before the end of the year.

Key Macroeconomic Signposts: Activity

- The business cycle continues to shift. On a global scale, in the manufacturing sector, the ratio of orders to inventories is below unity.

- Tensions that had been strong in the spring and summer of 2021 have quickly subsided since late spring 2022.

- This change in the overall dynamic can also be seen in the price of transport. The rental price of the containers has dropped for the journeys between China and the US.

- We also note that tensions within the productive apparatus are also being reduced very rapidly.

- In other words, the global economy is readjusting after the period of euphoria and tension that followed the end of the pandemic. We can see it on the activity indicators in the SP Global and ISM surveys.

- This adjustment will result in a reduction in tensions and a recession around the end of 2022 in both the US and Europe.

Key Macroeconomic Signposts: Inflation and budgetary policy

- Tensions are easing with the slowdown in activity.

- This point is very visible on the development of production prices. The decline in commodity prices in particular can be seen first in China and are beginning to be observed in the US.

- This is a strong signal that pressure on consumer prices will ease in the US. The Fed may no longer have to be as restrictive in its rate hikes as in the recent past.

- They are already low in China due to domestic demand constraints.

Europe does not have those same prospects. Production prices continue to rise sharply. This still reflects the energy crisis that the old continent is going through. - The recent decline in gas prices keeps prices well above pre-pandemic levels. Prices will remain high as gas supply is limited and European needs are still very high.

- The question of the persistence of inflation is therefore more relevant in Europe than elsewhere.

Strategic Views

Light at the end of the tunnel

Synthetic market views: leaning towards fine-tuning of monetary policy

The pace of global monetary tightening seems to be easing, contributing to an upturn in risky assets over the past month. Energy prices have come down, which arguably reduces the risk of a sharp recession in Europe. However, uncertainty remains about the extent of the inflation slowdown. The inertia of inflation could justify additional rate hikes in 2023, particularly in the United States.

Bond yields should adjust further, but in an environment of lower volatility, which favors spread products. Despite a solid earnings season in Q3 there is still a risk of margin compression going forward.

Allocation recommendations: light at the end of the tunnel

Credit and equity valuations already appear to price in deteriorating fundamentals, so a “small” recession would not prevent outperformance of risky assets. Risk aversion is decreasing. The balance of flows into European equities and US high yield funds suggest a more constructive market set-up. A cheaper dollar would prove to be a powerful catalyst for a recovery in world markets.

Monetary Policy

Ever-higher rates to counter high inflation

- Fed: Higher terminal rate

The Fed raised its rates by 75bp for the 4th consecutive time and hinted at a slowdown in the pace of monetary tightening from December or February. The Fed will take into account cumulative rate hikes as well as the lag with which monetary policy affects activity and inflation. However, Jerome Powell indicated that to curb high inflation, rates would probably have to rise to a higher level than what was expected in September. We anticipate +50bp in December 2022 followed by two rate hikes of 25bp. - ECB: Announcement of QT in december

The ECB raised its rates by 75bp for the second time in a row and plans to continue to raise them in order to deal with inflation that is far too high. To be in line with the normalization of monetary policy and to ensure its proper transmission, the ECB has also modified the conditions applicable to TLTROs 3 in order to make them less attractive. Christine Lagarde has also indicated that the main lines concerning the reduction in the size of its balance sheet will be presented in December for a later application. - Other central banks

After the strong turbulence created by the ephemeral government of Liz Truss, having forced the Bank of England to intervene urgently, the latter proceeded to its largest rate hike for 30 years: +75 bp, to raise its policy rate at 3% (7 votes against 2). It has also started reducing its balance sheet. On the other hand, the Bank of Canada and the Bank of Australia slowed the pace of monetary tightening (+50 bps and +25 bps respectively).

Asset Classes

G4 rates

-

The Fed will probably reduce its pace of monetary tightening, but the peak in rates may be higher given the strength of the labor market. A short duration bias in Treasuries remains appropriate.

- In the euro area, high inflation requires further monetary tightening. The ECB is expected to raise rates to 3% next spring. The financing needs in Germany will increase in 2023, which adds to upside risk on yields.

- The announcement of the UK budget in mid-November could revive volatility on Gilts which the BoE is trying to rein in whilst fighting inflation at the same time. We recommend a short Gilt position.

Other sovereigns

- The volatility on Bunds seems to have had little effect on sovereign spreads, which have rather narrowed despite the prolonged budgetary support in France or Italy. The spreads evolve in their low average on the main markets. OAT and BTP seem expensive.

- The swap spread has eased, which benefits the core fixed income asset class in general. The scarcity of collateral has been less problematic for several weeks.

- In the G10 universe, the downshift in rate increases has been observed in Australia, Canada and Norway. However, the adjustment is not complete in Sweden and New Zealand where we opt for a short duration bias.

Inflation

- Inflation is slowing in the United States thanks to energy, but underlying inflation remains sustained (6.3%). The Fed's policy keeps a lid on in long-term breakevens (neutrality).

- In the euro area, inflation tops 10% and upside surprises are piling up. Breakeven inflation rates have rebounded but still have the potential to widen by the end of the year.

- In the United Kingdom, the ambiguity of the BoE as regards inflation risks is perplexing and conducive of high volatility. Neutrality remains warranted on UK breakeven inflation rates.

Credit

- The expected slowdown has had a limited impact so far on the balance of rating reviews. Sentiment improved. We expect spreads to slightly widen further in the short run.

- Primary bond issuance resumed after the blackout period in the wake of the easing in spreads, but new issue premiums remained elevated, particularly in the financial sector.

- The fundamentals are deteriorating in high yield, despite the low default rate observed. Limited supply has offset fund outflows, which have been easing lately due to attractive spread valuations.

Stock market

- Taking advantage of inflation and the weakness of the euro, earnings expectations are showing resilience. We think the deterioration expected by investors is to be relatively small compared to previous recessions.

- Valuation multiples are low (11.5x at 12 months) and the median PE is back in line with long-term average. The expected dividend yield is elevated at 3.7% although it dipped below Euro IG spread.

- Markets are hesitant between monetary tightening, energy crisis and attractive valuations. However, by the end of 2023 we are more positive, with a Euro Stoxx 50 to 3,800.

Emerging

- The EMBIGD spread against Treasuries narrowed towards 508bp. We estimate the fair value of the spread at 442 bps, which points to short-term outperformance potential.

- Redemptions from emerging bond funds remain strong, but new issues of small size are attracting high investor demand..

- High yield has a historical premium against the IG of 733 bps. The countries most in difficulty (Kenya, Ghana) may obtain assistance from the IMF.