Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum’s views on the economy, strategy and markets.

The CIO letter

Inflexion point?

We are probably at an inflection point where the debate will no longer focus on inflation, but rather on growth. Over the past year, market attention has focused primarily on the inflation outlook. The polemics fade before the evidence: high inflation, sustained pressures and Central Banks who dig the hatchet to fight the problem. So this debate is running out of steam.

There is a good chance that the market, so often monomaniac, is changing its obsession and focusing on the issue of growth. The uncertainty associated with the outlook is very high. For now, the results season, as well as the leading macroeconomic indicators, show a surprising resilience. But the accumulation of shocks raises fears of a sudden loss of speed.

The Central Banks say have as a priority the fight against inflation. But how far are they willing to slow down the economy or risk a financial shock? The Fed’s famous «put» disappeared, but until when? The end of the ECB’s QE restores a degree of freedom to peripheral spreads, which brings back old fears of the sustainability of public finances. But where is the ECB’s pain threshold? This is yet another uncertainty on the growth trajectory.

A very difficult environment for risky assets in the near future. The policy mix put in place during the Covid crisis was of unprecedented magnitude. If these policies were fully justified and welcome, standardization was inevitable. We are in the middle of this process. Risk premiums are increasing again, but according to our models, this is so far more a return to normal than an overage. But the lack of visibility should lead to an extension of this trend, even though rising rates do not allow a bond portfolio to play its usual role of diversification.

To be more constructive on risky assets, we will probably have to wait for the “pivot”, that is to say when the Central Banks will tell us that they have reached their pain point and are stepping aside from the monetary tightening. In the meantime, be careful.

Economic views

Three themes for the markets

-

Growth

While economic data hold for the time being, the difficulties are mounting and suggest a marked slowdown. A recession is becoming more and more likely. This dynamic should become the main preoccupation of the markets in the coming months.

-

Monetary policy

Central banks are unusually univocal: they are concerned, above all, about inflation. But until when can they ignore market corrections and especially the risks associated with growth? The question is when the Central Banks will ease the pace of their tightening.

-

Inflation

Signs of persistence are accumulating, and more and more sectors are affected. The impact on the real disposable income of households is being felt, as are pressures on the margins of businesses, especially SMEs. For markets, this also contributes significantly to increasing nominal volatility.

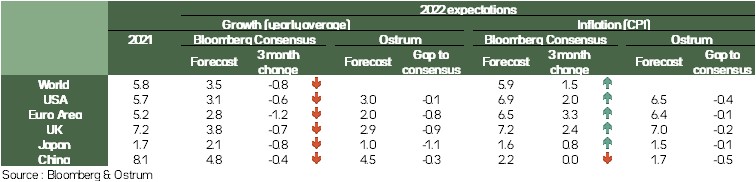

Key macroeconomic signposts

- The macroeconomy remains robust in terms of business surveys. That’s what the first graph shows. In the Eurozone, Asia excluding China and the US, the indices are higher than the 50 separator. The components of these synthetic indices are also positive.

- The only really negative indicator is China’s because of the lockdown. In view of the tensions between the Shanghai authorities and the central government, it is likely that the Chinese economy will remain under tension until October at the Chinese PC conference which must validate the re-election of Jin Ping.

- Job indicators are also reassuring. American employment has returned to its pre-pandemic level in April. In Europe, employment in the Eurozone, France and Germany is well above pre-pandemic levels. Only the British situation is worrying since employment has been flat since autumn 2021.

- On the other hand, if we look at the macroeconomy through the perception of households, then there is a real risk of recession.

- Falling purchasing power and geopolitical uncertainty have pushed confidence indicators down with concerns about employment and geopolitics.

- The gap with consumption indicators is very large and if the crisis and worries then household spending will adjust downward. This is generating recession.

The macroeconomy remains robust in terms of business surveys.

Key macroeconomic signposts

- Inflation indicators continue to deteriorate.

- The Markit surveys for the Eurozone and ISM in the US do not show a downward reversal in inflation over the coming months.

- Pressures from raw materials and transportation costs continue to push inflation rates to high levels.

- In the US, in the Eurozone, we can see that the underlying indicators continue to grow rapidly. This reflects the contagion of these costs to business operating accounts. Businesses adjust their prices to maintain their margins.

- This is a major incentive for central banks to get tough. Monetary policies will be restrictive to constrain economies and influence price dynamics.

- On the other hand, energy prices remain high and the contribution of energy to the inflation rate is strong and will continue to be strong in the coming months.

- The other major point is the rise in food prices and contributions to the rate of inflation, which are now well above 1% in the Euro zone and the United States. This phenomenon is not going to be resolved quickly because heat waves, in India for example, will not make it possible to loosen the supply constraint on cereals. This will put upward pressure on the prices of Western countries accentuating the decline in purchasing power.

Pressures from raw materials and transportation costs continue to push inflation rates to high levels.

Budgetary policy

Governments of Developed Countries and the Impact of Ukraine

- United States: Major fiscal tightening

While the $13.7 billion aid envelope for Ukraine was almost exhausted, Joe Biden asked Congress for an additional $33 billion. The House of Representatives went further by voting for an additional $40 billion in aid for the supply of weapons, economic support, humanitarian and food aid. This comes at a time when the budget deficit has fallen by $1.57 trillion over the current fiscal year. High growth has resulted in higher tax revenues and public spending has slowed following the end of support measures to address the Covid crisis. The structural deficit, according to the OECD, will fall from 8.8% of GDP in 2021 to 4.7% this year, which would represent an unprecedented fiscal tightening.

- EU: Ukraine weakens public finances

The reduction in government deficits and debts expected this year, with the rebound in growth and the end of measures to address Covid, will be less significant than expected, due to the consequences of the war in Ukraine. It affects tax revenues through lower growth and generates additional spending as a result of government actions to reduce the impact of the sharp rise in energy prices on households. The EU wants to reduce its heavy reliance on Russian energy well before 2030. In order to achieve this, the European Commission is drawing up a plan of €195 billion over five years.

- China promises to suport the economy

The government promised to increase support for the economy to meet its growth target of 5.5% this year. Few details were provided, but the statements suggest a significant increase in infrastructure spending.

Monetary policy

Rate hikes to contain inflation expectations

- The Fed raises its rates quickly

With “far too high” inflation and an “extremely tight” labour market, the Fed raised its rates by 50 basis points on May to [0.75%-1%]. It also announced a “significant” reduction in its balance sheet effective June 1. This will be done at the rate of 47.5 billion dollars per month over the first three months, then at 95 billion dollars per month thereafter. At the press conference, Powell said that rate hikes of 50 basis points could be adopted in June and July, if the economy progressed as expected. He ruled out a 75 bps rate hike. We expect Fed Funds to hit 2.0% at year-end.

- ECB: Towards a rate hike in July

In view of the strong acceleration of inflation and the need to contain inflation expectations, the ECB should announce at the meeting on 9 June the end of its asset purchase program (APP) at the end of June and prepare the markets for an imminent increase in key interest rates. This should take place as soon as the July 21 meeting and will be followed by a second one, probably in September. The rate of deposit in negative territory is no longer appropriate: it should return to 0% by the end of the year.

- Risk situation in emerging markets

The divergence in monetary policy between China and developed countries is increasing. It reiterated its desire to support small businesses, sectors and households affected by the Covid-19 crisis. In addition, the situation is becoming more risky in emerging countries. The sharp rise in US rates and the acceleration of inflation could lead them to raise their rates, in order to preserve their financial stability at the risk of weighing more heavily on their economy.

Strategic views

Very challenging in the short term

Synthetic market views: when everything goes wrong at the same time

In the short term, upward pressure on rates is expected to continue, while at the same time risk premiums continue to tighten. The expected profitability is therefore negative, both for risk-free assets and for risky assets. A situation unprecedented since the beginning of the century and which constitutes a major problem for recipients.

Central Bank uncertainty, economic slowdown and aggressiveness are not expected to reverse over the next month and are therefore expected to maintain markets on a recent trend.

Allocation recommendations: Bell shaped trajectory

We remain underweight on nominal rates as all the conditions are present in the short term for the trend to continue with a neutral position on inflation. We remain underweight on credit, with HY in particular expected to suffer. Finally, on equities, if we remain confident in the medium term, a downturn is possible in the shorter term.

Looking ahead to the end of the year, however, the economic slowdown, or excessive adjustment of risky assets, should push Central Banks to be more cautious and lower long-term rates. A bell profile, therefore, where long rates have probably already made a large part of their upward adjustment.

In the short term, upward pressure on rates is expected to continue, while at the same time risk premiums continue to tighten.

Asset classes

G4 rates

- The Fed will raise its rates in steps of 50 bp over the next FOMCs and will start reducing its balance sheet in June. High inflation still argues for a short bias in Treasuries, despite weakness in equities.

- Given the high inflation, a consensus is emerging within the ECB for a rate hike in July immediately after the end of QE. A short duration stance is recommended on the Bund.

- The BoE is tightening its policy at the cost of a probable recession in 2023. The QT will start at the end of Q3, which will exert upward pressure on yields. In Japan, the firm hand of the BoJ is capping 10-year yields at 0.25%.

Other sovereigns

- All peripheral spreads are under pressure. The slowdown and the expected end of QE contribute to spread widening. The market is also testing the ECB's willingness to intervene to limit asymmetric risks.

- Neutrality, on the other hand, prevails in core sovereign countries. The outcome of the French elections allowed for stabilization in OAT spreads around 50bp. Core countries are relatively cheap against swap and Bunds.

- Monetary tightening argues for a reduction in duration positioning in the G10 universe. The short bias is larger in Canadian and Swedish markets.

Inflation

- Inflation (8.3% in April) remains very high in the United States, but the strength of the dollar and monetary tightening could weigh on inflation breakevens. We maintain neutrality.

- In the euro area, inflation remained at an historic high of 7.5% in April. The ECB is concerned about inflation. Demand for index-linked securities has fallen given the weakness in risky asset markets. We are neutral on the European breakeven points.

- In the UK, inflation is expected to reach 10% in the short term. Further tightening will aim to raise real rates. The view is more constructive on Japanese inflation due to the weak yen.

Credit

- IG spreads under pressure with the rise in risk-free rates. The termination of the APP soon and credit fund outflows are deteriorating liquidity on the secondary market.

- The primary market reopened with higher new issue premiums. Risk aversion overshadows cheaper valuations, which is particularly detrimental to the high-beta segments.

- Sentiment deteriorated in high yield space, despite a default rate at rock bottom. Low primary issuance activity did not prevent spreads from widening, amplified by hedging flows.

Stock market

- The economic context is generally unfavorable to equities, but Q1 publications are better than expected and 2022 EPS are revised upwards. The risk of profit warnings is significant.

- PE contraction accelerated to just 12.2x now. On the other hand, the potential for shareholder payouts remains high (the dividend yield stands at 3.4% for 2022), thanks to healthy balance sheets.

- High volatility continue to fuel outflows from European equity funds. Low volumes highlight investor caution. We forecast Euro Stoxx 50 at 3650 on a 1-month horizon.

Emerging

- The EMBIGD spread should move in a range of 430-480 bps. We remain cautious, despite improving valuation levels.

- Flows remain unfavorable to the asset class and market liquidity is low. Competition from higher risk-free rates in the United States works against emerging debt.

- Countries in difficulty due to the consequences of the war in Ukraine are supported by the IMF and the WB, so that credit metrics are holding up.