Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum’s views on the economy, strategy and markets.

The CIO letter

From « transitory » to « fragmentation »

Faster, Higher, Stronger ! The frenetic activity of central banks has shifted curves and market expectations at a breakneck pace. At the beginning of the year, the markets were expecting three Fed rate hikes in 2022, they are now at fourteen! Regarding the ECB we went from a rate increase to seven. The SNB, the RBA, the BoE among many others followed.

For the moment, central banks are monomaniac, they are only concerned about inflation and have set aside the problems of growth or even financial stability. In the short term, therefore, the path seems to be all mapped out with rates that can only rise.

In economic terms it seems obvious to us that a slowdown is inevitable. This is the goal of central banks, which must reduce demand for inflation to fall. They are helped in this by risky assets which, having lost the support of lax monetary policies, see their risk premiums rebound. So it’s a general tightening of monetary conditions, and the market, with its very rapid adjustment there as well, is somehow making of the work of the central banks.

How far to go? If the short term, let’s say until the end of this summer, seems marked, the landing at the end of the year is much more difficult to apprehend. We make two assumptions for the end of the year, which condition our medium-term scenario.

First hypothesis, the economy should suffer before the end of the year. A recession, both in the United States and in the Eurozone now, seems very likely as it seems difficult for economies to absorb so many simultaneous negative shocks. A market accident also seems to us a possibility that cannot be ruled out.

Second, in this case, central banks will abandon their “monomaniac” attitude and take growth into account in their decision. In this scenario, the pace of tightening is expected to ease and market expectations are likely too high. This would then lead to a relaxation of the rates at the end of the year.

Economic views

Three themes for the markets

-

Growth

If the data remain resilient for the time being, it seems to us increasingly likely that a recession will emerge in the Eurozone and in the United States. However, the latest information shows that T2 may be resilient, especially in Europe, even if for temporary reasons.

-

Monetary policy

The pace of monetary tightening has accelerated further. It is very global with a very generalized rate hike wave around the world. The near future seems to be on track: more increases, always at a steady pace. The question is more about the inflection point: when do banks step aside.

-

Inflation

Signs of persistence are accumulating and more and more sectors are affected. Companies have decided to shift the cost increase to the final consumer. The impact on the real disposable income of households is being felt. For markets, this also contributes significantly to increasing nominal volatility.

Key macroeconomic signposts

- Spring survey indicators, until May, suggest a shift in activity in most developed countries. Nevertheless, no break is observed. This is the meaning of the first graph. The indices converge towards 50 but at a moderate pace.

- The Eurozone appears resilient even if Germany is affected by developments in Ukraine and the Chinese slowdown. This short-term optimism should not mask questions about the impact of the decline in household purchasing power and its consequences on consumption and therefore on growth.

- In this respect, the American situation sheds light on the debate with detailed statistics on the household side. Though businesses, on reading the surveys (ISM and Markit), are still doing well, the situation of households is deteriorating. On the second graph, the Michigan Consumer Confidence Index (the red curve) is at an all-time low in June. Households note the fall in purchasing power, measured here by wages excluding inflation. On the basis of the Atlanta Fed’s wage measures, the figure is at its lowest level over the period as a whole.

- This negative perception of the environment finds its source in the price of gasoline, now above 5 dollars per gallon This is the highest figure ever recorded. As long as there is no inflection on this price, households will remain cautious in their spending. This situation on the purchasing power and price of gasoline is not specific to the US and can extend to many developed countries. In the short term, this is a threat to the dynamics of household consumption.

- On the global scale, the risk is still China with its resumed containment and the impact on the dynamics of production processes for developed countries.

On the global scale, the risk is still China with its resumed containment and the impact on the dynamics of production processes for developed countries.

Key macroeconomic signposts

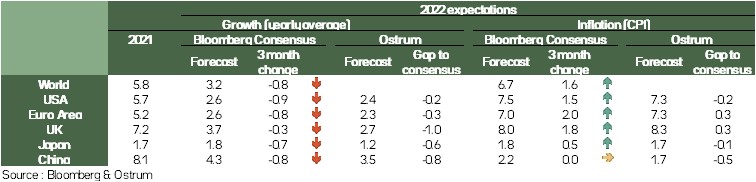

- Inflation accelerated again in May in the Eurozone and the US. It is now 8.1% in Europe and 8.6% across the Atlantic.

- The risk of persistence can be read through 4 indicators :

○ The first one is wages. If they are rising rapidly in the United States, that is not the case in Europe. This difference explains the Fed’s greater willingness to quickly tighten its monetary policy.

○ The second factor is the continuing impact of rising energy prices. Prices are strong, they will probably remain around 120 dollars per barrel of oil because of the decline in Russian supply not offset by the other producers. But the lingering effect will subside except to imagine a new energy crisis that would push the price of a barrel beyond 150 or 180 dollars.

○ Food prices are increasingly contributing to the rate of inflation. This will not abate quickly as harvests for 2022 will be poor on cereals due to adverse weather conditions in Europe, the US and India. Prices in the food industry will continue to rise rapidly, penalizing purchasing power.

○ The contribution of the price of goods, which has been very low over the last 20 years, is increasing sharply. Trade dynamics have been disrupted and developed countries no longer import disinflation. This will weigh on medium-term inflation rates. (Graph 2)

- Faced with these risks of persistence, central banks are more restrictive. Investors are integrating this break as suggested by the third chart for the Euro area.

Faced with these risks of persistence, central banks are more restrictive.

Budgetary policy

Governments in the face of rising energy prices

- US: Biden weakened

As the mid-term elections approach, Joe Biden is weakened by high inflation, at its highest in 40 years. This weighs on the purchasing power of households and particularly affects the least privileged. The war in Ukraine and the sanctions against Russia have accentuated the rise in energy prices, taking gasoline prices to historic highs: $5.1 per gallon, on June 13, as the summer season begins. Joe Biden will make his first trip to the Middle East in July to ask them to increase their oil supply.

- UE: New suspension of budgetary rules

The EU has extended the suspension of the rules of the stability pact for another year, until the end of 2023, in order to give governments room for maneuver to deal with the consequences of the war in Ukraine. Governments are taking new measures to limit the impact of the sharp rise in energy prices on the most vulnerable households and businesses. They will also have to take steps to rapidly reduce their dependence on Russian energy. To achieve this, the European Commission has published its roadmap: REpowerEU. It aims to become independent of Russian energy well before 2030 while respecting climate objectives. To make the massive investments in renewable energy, governments will be able to use the loan envelope that has not yet been requested under Next Generation EU.

- Emerging countries: Pay debt or feed yourself

Emerging countries that are net oil importers and highly indebted are very weakened by the rise in energy and food prices, which increases the risk of social tensions in Africa and Latin America.

Monetary policy

Central banks accelerate rate hikes

- Very strong Fed tightening

Faced with a further acceleration in inflation deemed "far too high", a sharp rise in household inflation expectations and an "extremely tight" labor market, the Fed raised its rates by 75 basis points on 15 June, to bring the Fed funds range to [1.50%-1.75%]. Powell indicated that 50 or 75bp hike would be needed in July, followed by continued hikes. The reduction in the balance sheet continues. The top priority is inflation and the Fed is rapidly tightening monetary policy so that it becomes restrictive. Members anticipate Fed funds at 3.4% at the end of 2022 and 3.8% in 2023.

- ECB: +25 bp in July and +50 bp in September?

The ECB was unusually very explicit at the June 9 meeting. It announced that it would raise rates by 25 bps on July 21 and left the door open for a 50 bp hike at the September 22 meeting, depending on medium-term inflation expectations. Thereafter, it will proceed with a sequence of gradual but lasting rate hikes. While the ECB announced as expected the end of asset purchases under the APP from 1 July, it did not provide any information on the new measures that could be taken in the event of a risk of fragmentation. Strong tensions thus took place on the spreads of the peripheral countries which justified an exceptional meeting of the ECB, on June 15th. It decided to use the flexibility of reinvestments under the PEPP and asked to speed up the finalization of a new anti-fragmentation instrument.

- Overall tightening of monetary policies

Faced with the risk linked to the sharp acceleration in inflation, central banks are raising their rates sharply around the world, with the notable exception of China where inflation remains moderate, internal demand being affected by the lockdowns adopted.

Strategic views

Paradoxically, the end of the year on the markets could be better

Synthetic market views: inflation again…

In the short term, the rise in rates can only continue. On the other hand, the inflation outlook now seems reasonable and should therefore not move much. The rise in rates is therefore mainly driven by the real part, and the spread of spreads.

On the other hand, valuations seem interesting to us. The current trend forces us to be cautious but entry points are emerging. Any additional increase in the risk premium could be a signal to reposition itself.

Allocation recommendations: A reversal

By the end of the year, the majority of asset classes should have a positive return. A pink scenario? Not necessarily: since the beginning of the year all asset classes have had a negative performance, with an unusual uniformity, performance often in the range 10-15%. Typical configuration of an economy with excessive inflation accompanied by central banks tightening their monetary policy quickly. In this case the rates go up and the risk premiums too.

Conversely, an end to tightening or at least a clear slowdown would reverse this logic. The carry on fixed-income products, which has recovered since the beginning of the year, would then help generate positive asset returns. At the same time, stock markets would benefit from more optimistic prospects.

The current trend forces us to be cautious but entry points are emerging.

Asset classes

G4 rates

- The Fed tightened policy by raising its rate by 75 bp in June. In the short term, the persistence of high inflation maintains a bearish environment for Treasuries, despite the weakness in equities and downside risks to activity.

- A rate hike is expected in July, but the subsequent tightening package remains conditional on inflation. The Bund should accelerate towards 2%.

- The BoE hiked rates by 25bp in June and is poised to accelerate the move. In Japan, the 10 is capping at 0.25% thanks to massive BoJ intervention each day. The market is also trying to crack the BoJ.

Other sovereigns

- The lack of detail on the ECB's anti-fragmentation mechanism maintains a high level of uncertainty on spreads. The ECB's commitment nevertheless constitutes verbal support at this stage.

- The intense selling pressure on peripheral debt as a whole is not sparing core countries, including France, which is trading around 60 bp spreads to Bunds. The Italian 10-year BTP spread is hovering around 220 bp.

- Monetary policy is becoming more restrictive across the G10. The RBA is catching up with stronger than expected increases. A seller's bias is recommended, and even accentuated on Australian debt.

Inflation

- Inflation (8.6% in May) remains too high in the United States. The strength of the dollar and monetary tightening should weigh on inflation breakeven. We maintain neutrality.

- In the euro zone, inflation remains at an historic high of 8.1% in May. The ECB now conditions the extent of rate hikes on inflation. The expected rise in real rates encourages us to remain neutral on the European breakeven point.

- In the UK, inflation is expected to reach 10% in the short term. Further tightening will aim to raise real rates. The view is more constructive on Japanese inflation due to the weak yen.

Credit

- IG spreads are under pressure with the rise in risk-free rates. The termination of the APP and redemptions on the funds amplified the deterioration of liquidity conditions on the secondary market.

- The primary market is functioning but requires ever-higher new issue premiums (the highest since March 2020). Risk aversion overshadows cheap valuations.

- Sentiment remains unfavorable to high yield, despite a record low default rate. The lack of bond supply does not reduce tensions on spreads, fueled by hedging flows.

Stock market

- The economic slowdown is accompanied by price pressures. EPS for 2022 are revised upwards, but this is mainly due to sectors linked to raw materials. Operating margins, historically very high, are in danger of shrinking.

- The reduction in PE multiples continues (11.7x at 12 months). The yield advantage between equities and credit has narrowed significantly, the TINA effect is dissipating. Nevertheless, balance sheets are sound and cash flow generation is high.

- High volatility causes redemptions from European equity funds. The volumes are significant, but capitulation levels have not been reached. We expect a Euro Stoxx 50 to 3.500 on a 1-month horizon.

Emerging

- The EMBIGD spread should move in a range of 440-500 bps. We remain cautious and shift the target range higher. We opt for a slight seller bias.

- Fund outflows continue in the EM bond asset class and market liquidity is reduced. The primary market will remain very calm for several months to come.

- Countries in difficulty due to the consequences of the war in Ukraine are supported by the IMF and the WB, so that credit metrics are holding up.