Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum’s views on the economy, strategy and markets.

Economic Views

Three themes for the markets

-

Monetary policy

The stress of the banking crisis seems to be fading. A systemic crisis seems very unlikely. The consequence, however, is a tightening of bank credit conditions which therefore helps to limit the need for central bank rates to rise. So, the Fed and ECB are back to fundamentals. The Fed is close to the end of the upswing cycle, we’re just expecting another upswing. The ECB is a little further ahead, three increases. Persistent inflationary pressures will not allow banks to reduce rates by the end of the year.

-

Inflation

Inflation continues to moderate due to lower energy prices. The problem remains underlying inflation, which crystallizes domestic tensions. It accelerated to a historic high in the Eurozone (5.6%) and remains high in the United States (4.7% for the PCE). This reflects the continued diffusion of higher energy prices within the economy as well as wage pressures. The strong inertia means underlying inflation will remain high at the end of the year. The reopening of China will weigh on the price of raw materials.

-

Growth

The Eurozone has escaped recession, thanks to government support measures and the sharp drop in gas prices. Available data suggest a moderate growth in Q1 and a limited acceleration in Q2. The rise in wages should allow consumption to hold. In the United States the beginning of the year is much more dynamic but the monetary tightening should lead the American economy to close the recession in the second half of the year.

Key macroeconomic signposts : euro area

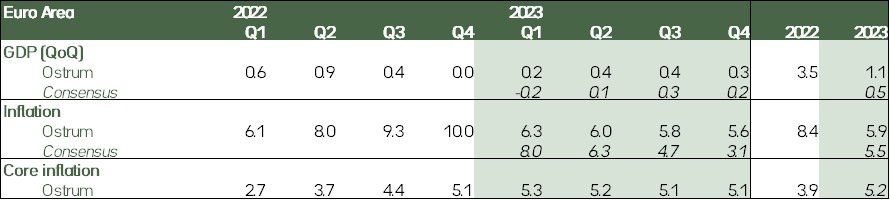

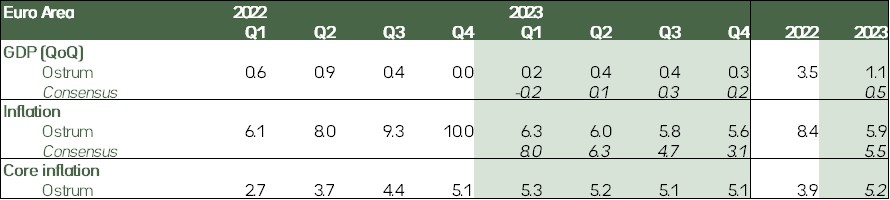

- We expected a very moderate recession in Q4 2022 and Q1 2023. The figures published for Q4 actually show a stabilization of the economy. On the other hand, the evidence for this year’s Q1 shows growth, albeit low, but in all probability positive.

- As a result, the growth carry-over at the end of 2022 was already 0.4%. With moderate growth, average growth over the rest of the year should therefore be in the 0.5/1.0% range.

- The relative decline in inflation and the rise in wages, but also in government subsidies, should keep the purchasing power of wages at a very slightly positive level. Consumption would then be slightly upward over the year. Similarly, the accumulated investment lag should allow capex to progress, again moderately.

- As a result, we have a GDP trajectory that is still mediocre but displays a little acceleration at mid-year. This puts us on the high side of the consensus.

- A fundamental point in our forecast is the inflation trajectory. It’s declining rapidly until this summer, largely because of the basic effects on the energy component. But the underlying part remains very stable and should not fall below 5% by the end of the year. This leads to a high year-end landing, 5% over the last quarter. This is fundamental to monetary policy.

Key macroeconomic signposts : USA et al.

- Rising rates are a drag on growth, with the most directly exposed sectors, including real estate, showing very strong signs of slowing. While the figures available for the first quarter show, once again, a very resilient economy, on the other hand we think that the economy will approach recession at the end of the year.

- The U.S. economy has shown an unusual ability to absorb rate hikes. We believe that structural changes explain this resistance. As a result, we think the “soft landing” scenario is more likely than the “hard landing” scenario.

- The bankruptcies of SVB and Signature are a warning shot: we do not think this constitutes the beginning of a systemic crisis, the much more pessimistic alternative scenario can however be ruled out, even if its probability is limited.

- Finally, continued inflation above the Fed target remains the most likely scenario. Wage pressures in particular remain high. Again, this is a structuring element for the Fed.

- It should also be noted that China is rapidly reopening. This implies more sustained global growth, an improvement in the latest production problems related to supply chains, but also new potential inflationary pressures on raw materials. The reopening of China therefore bears out the idea of growth that surprises upward, as well as inflation.

Monetary Policy

More limited rate hikes due to the risk of tighter credit conditions

- The uncertainty linked to banking stress only pleads for a single rate hike

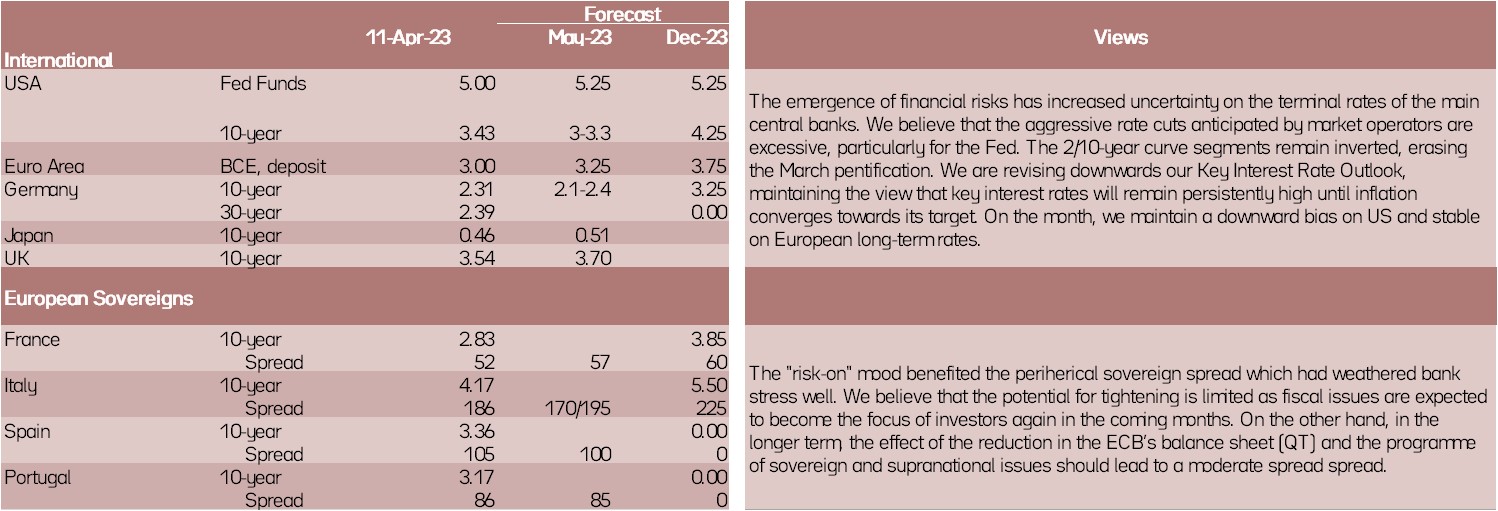

While J. Powell had signaled on March 7 that the Fed was ready to accelerate the pace of its rate hikes to deal with stronger than expected inflation, banking stress, linked to the bankruptcy of SVB and Signature Bank a few days later, came to limit its extent. The Fed raised rates by 25 bps on March 22, after taking sweeping measures to avoid contagion to the entire banking system. The Fed's communication became more evasive: "some additional tightening may be appropriate." The risk is a greater tightening of credit conditions likely to weigh on demand and therefore inflation. We therefore anticipate a single rate hike in May: +25 bps and a status quo until the end of 2023. - ECB: "Inflation should remain too high, for too long"

As it reported in February, the ECB raised rates by 50 bps on March 16 to bring the deposit rate to 3%. This time, the Bank was careful not to indicate what it intended to do at the next meeting, insisting that it would depend on the data. However, core inflation accelerated again to a historic high in March (5.7%) and the results of wage negotiations presage a stronger contribution from wages to domestic inflation, even though those from the unit profits do not show significant signs of moderation. This argues for continued ECB rate hikes but at a more moderate pace due to the risk of tighter credit conditions. We therefore now anticipate 3 rate hikes by the ECB of 25 bp in May, June and July to bring the deposit rate to 3.75%. - Very reactive central banks to limit the contagion effect

The Fed, via the creation of a new loan facility accepting as collateral bonds valued at par, therefore without any loss in value linked to the rise in interest rates, and the Swiss National Bank, by providing all the necessary liquidity to Credit Suisse, have been very reactive in stabilizing the banking system.

Strategic Views

Markets arm wrestling central banks

Synthetic market views: The aborted systemic crisis

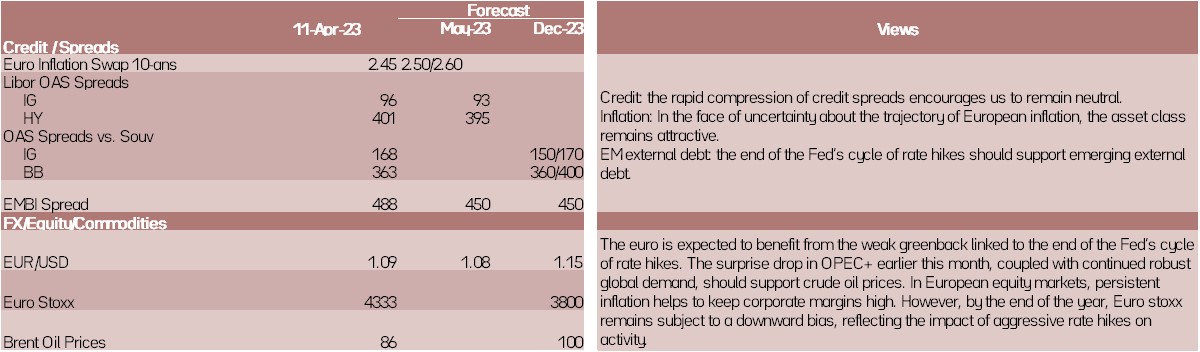

The financial stress in March seems to be fading even if interest rate volatility or swap spreads remain high. The banking crisis is dissipating so that even Tier 1 bonds are regaining momentum. The decline in headline inflation fosters expectations of monetary easing, which nevertheless seem premature given wage pressures and more generally the inertia of underlying inflation. A fight is underway between markets and central banks as data comes in on the soft side in the US and a recovery unfolds in Europe. The depreciation of the greenback also spurs long bets on risky assets. Credit and sovereign debt weathered this bout of volatility unscathed. However, this is not the case for securitizations of commercial real estate.

Allocation recommendations: A conditional risk-on bias

The favorable risk bias and low equity volatility are de facto conditioned to hypothetical rate cuts. Sovereign and credit spreads are in fact less volatile than the asset deemed to be (default) risk-free. This rare situation creates a vacuum for stocks that offer protection against inflation. High yield also offers a comfortable premium amid low default rates. In this context, the status quo on rates would be almost harmful by erasing the relief demanded by the markets.

Market views

Asset classes