Each month we share the conclusions from the monthly strategy investment committee which provides a summary of Ostrum AM's views on the economy, strategy and markets.

The CIO letter

End of Statistical Fog but Warning Signals for the Markets

Initial doubts are emerging regarding the sustainability of valuations for U.S. stocks linked to artificial intelligence. The opacity of private financing, the rise in credit default swap (CDS) premiums for major players in the sector, and recurring tensions in the U.S. repo market are all warning signs. The current economic situation remains difficult to interpret due to the lack of data caused by the longest shutdown in U.S. history. However, the deterioration in the labor market seems to be confirmed, with announced layoffs and an increase in payment delays on household credit. In the Eurozone, growth and recent PMI surveys appear to show a more positive outlook. Growth in 2026 is expected to be close to potential. In contrast, China's anti-involution policy, aimed at reducing overcapacity and deflationary pressures, has resulted in a significant decline in investment.

In this context, central banks are hesitant to ease further. The European Central Bank (ECB) is likely to maintain a status quo at 2% until the end of 2026. The Federal Reserve must navigate monetary tensions, leading to the end of quantitative tightening, although a rate cut in December is still under discussion. U.S. inflation is expected to hover around 3% in the coming months. The Bank of England (BoE) will mitigate the effects of fiscal consolidation by reducing its rate in December, despite inflation remaining very high. Long-term rates are under pressure, particularly due to budgetary concerns. The Bund is projected to approximate 2.80% by the end of 2025, while the T-note will likely remain around 4%. Measured profit-taking is probable in the credit markets, although fundamentals remain favorable in the Eurozone. The high yield segment remains expensive but contained default rates provide support. European equity markets are expected to retain their gains until the end of the year.

Economic Views

THREE THEMES FOR THE MARKETS

-

Growth

In the United States, the confidence shock and tariff impact are expected to continue weighing on household consumption and investment (excluding AI) in the first half of 2026. In the eurozone, growth will strengthen driven by Germany and the continued robust growth of peripheral countries. This will contrast with a weak cyclical dynamic in France due to the persistence of political and budgetary uncertainty. Chinese growth in 2026 will be supported by a strengthening of consumption, investment in AI, and service exports.

-

Inflation

In the United States, the decline in oil prices and the reduction in rental inflation are expected to offset the impact of tariffs. The inertia in services will keep inflation above target in 2026. In the eurozone, inflation is expected to remain close to the ECB's target of 2%. Inflation in services is likely to moderate only gradually due to a slow adjustment of wages to inflation. The fight against deflation is a priority objective for the Chinese government with its anti-involution policy. Underlying inflation is expected to continue rising in 2026 in the wake of consumption.

-

Monetary policy

The Fed has resumed its rate-cutting cycle due to the significant slowdown in the labor market. It is expected to reduce the federal funds rate to around 3% during 2026. The ECB is likely to maintain the status quo at 2% until the end of 2026, confident in achieving the medium-term inflation target of 2%. The PBoC continues its accommodative policy. The bias among other major global central banks remains toward easing.

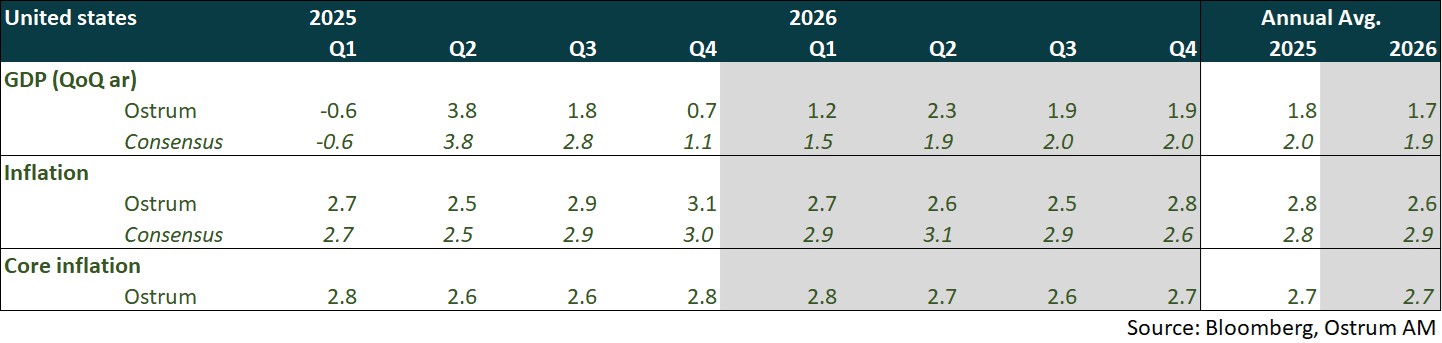

ECONOMY: UNITED STATES

Two Years Below Potential: Continued Deterioration of the Labor Market, Significant Risks to Real Estate, and Financial Bubble Threats.

- Demand: The confidence shock and tariff burden will continue to weigh on household consumption and investment in the first half of 2026. The credit quality of households is deteriorating, but an increase in transfers to households could mitigate the negative impact on consumption. The trade balance is expected to worsen, following the trend of the second half of 2025. Housing investment is projected to contract further in 2026, posing a recession risk. Productive investment will primarily be driven by AI (data centers, software, and R&D).

- Labor Market: Hiring is slowing down. The unemployment rate is expected to remain above 4.5% in 2026 despite weak participation (driven by constrained immigration). Job openings are trending downward, but labor shortages persist.

- Fiscal Policy: The federal deficit has somewhat decreased in 2025; however, the situation remains concerning. The Supreme Court could rule the tariffs illegal, which would necessitate refunds of overcharges to importers. Transfers to households are likely in 2026 in anticipation of the mid-term elections.

- Inflation: The decline in oil prices and the reduction in rental inflation should offset the impact of tariffs. However, the inertia in service prices (healthcare, auto insurance) will keep inflation above target in 2026.

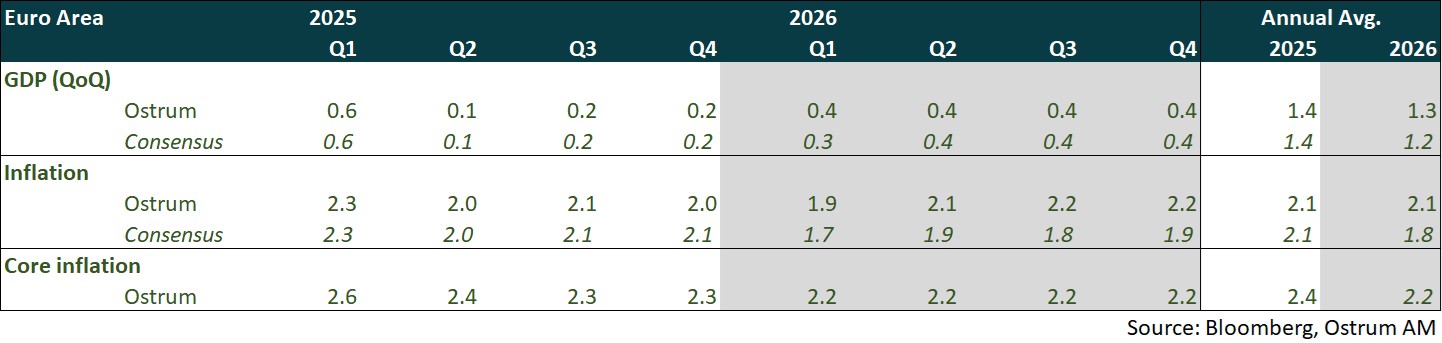

ECONOMY: EURO AREA

Strengthening of growth in 2026 driven by Germany (infrastructure plan and military spending) and continued robust growth in the peripheral countries. In France, growth will be very moderate due to the persistence of political and budgetary uncertainty.

- Domestic demand: Consumption is expected to be somewhat stronger due to gains in purchasing power (albeit more moderate) and a low unemployment rate that is likely to remain stable. Investment will be better oriented with the implementation of infrastructure and defense plans in Germany, the increase in military spending in Europe, and the payments from NextGeneration EU, primarily aimed at the peripheral countries, which will conclude at the end of 2026. In France, political uncertainty will continue to be a drag on growth (wait-and-see approach).

- External demand: The trade agreement between the eurozone and the United States, as well as the one-year truce between the United States and China, reduce uncertainty and help stabilize foreign trade.

- Fiscal policy: Germany, after years of fiscal prudence, is set to significantly increase its spending on infrastructure and defense. In France, the budget deficit is expected to remain high due to the divided National Assembly, which greatly limits the government's ability to act.

- Inflation: Inflation is expected to remain close to the ECB's target of 2%. Inflation in services is likely to moderate only gradually due to a slow adjustment of wages to inflation.

ECONOMY: CHINA

Chinese growth in 2026 will be supported by a strengthening of consumption, investment in AI, and service exports. The U.S. midterm elections are expected to reignite tensions with Washington.

- Global scenario for 2026: We expect growth of 4.5% next year and a gradual recovery of inflation to 1%. The 15th Five-Year Plan demands immediate results. Tensions with the White House are likely to be reignited as the U.S. midterm elections approach, which could hinder growth in Q3.

- Net exports: The trade truce is expected to stabilize goods exports. Institutional openness, one of the three objectives of the 15th five-year plan, should accelerate service exports, particularly in the technology sector, allowing China to diversify its export base.

- Consumption: The strengthening of service consumption is expected to continue, supported by household-centered policies (childcare, education, and access to homeownership), which are a priority of the new five-year plan. The rebalancing of growth towards consumption is underway.

- Investment: The goal of technological self-sufficiency involves accelerating investment in the fields of AI, where China aims to become the global leader. The anti-involution policy is expected to quickly improve the margins of private enterprises.

- Inflation: Underlying inflation is expected to continue rising in the wake of consumption. This is the main focus of the Chinese authorities.

Monetary Policy

Divergence between the Fed and the ECB

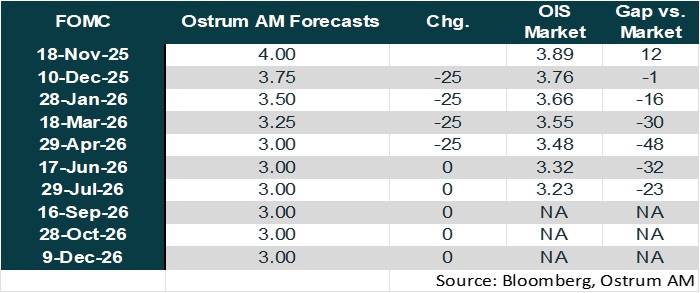

- The Fed has resumed its rate-cutting cycle and is leaving uncertainty for December.

After 9 months of status quo, the Fed cut its rates for the second consecutive time by 25 basis points during the meeting on October 29, bringing the federal funds rate to the range of [3.75 – 4.00%]. Despite the lack of data due to the shutdown, the available indicators revealed greater downside risks to employment, which motivated the decision to lower rates again. The risks to inflation remain tilted to the upside, but the impact of tariffs is considered to be transitory. Jerome Powell revealed at the press conference that there were significant divergences within the FOMC regarding the December meeting and warned that a rate cut was far from guaranteed. The Fed also announced the end of its balance sheet reduction starting December 1. Given the continued deterioration of the labor market and significant risks in the real estate market, we anticipate another rate cut in December, followed by three more in 2026, to return to the neutral rate.

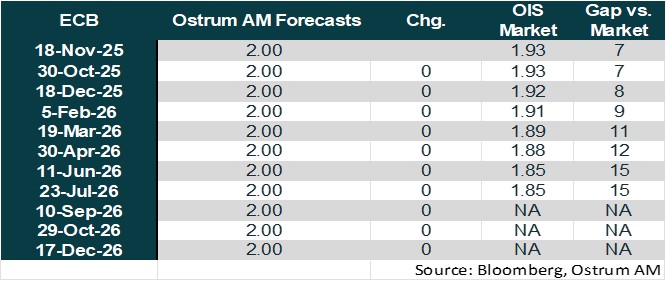

- Extended status quo of the ECB.

The ECB kept its rates unchanged for the third consecutive time during the meeting on October 30. It believes it is in a comfortable position ("We are in a good place") due to resilient growth, a strong labor market, and inflation expected to remain close to the 2% target in the medium term. Downside risks to growth have diminished again following the trade agreement between the EU and the United States this summer, the ceasefire in the Middle East and the trade truce between China and the U.S. The ECB continues to emphasize that it will determine its interest rate policy on a meeting-by-meeting basis depending on the data. The balance sheet reduction continues through the non-reinvestment of maturing securities. We anticipate rates to remain unchanged until the end of 2026. A final rate cut would only occur in the event of a negative shock to growth.

Market views

Asset classes

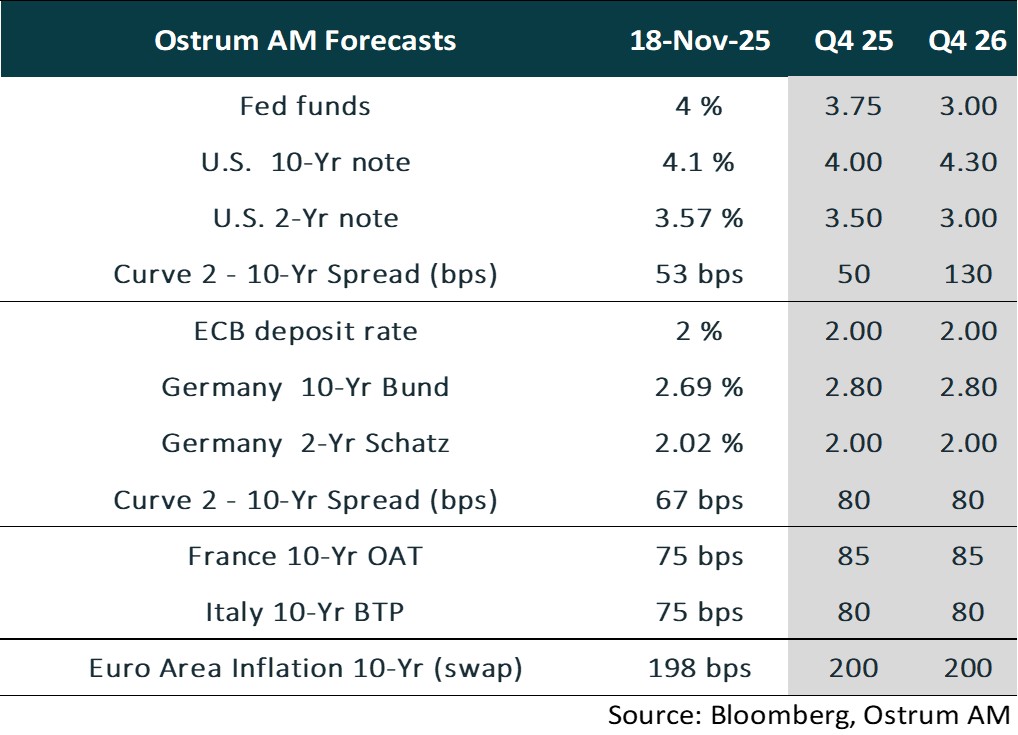

- U.S. Rates: The Federal Reserve responded to the deterioration in employment starting in September, despite upside risks to inflation. Fiscal risks may continue to weigh on long-term yields.

- European Rates: The ECB will keep rates unchanged at 2% until 2026. The 10-year Bund forecasted at 2.80% reflects a more ambitious fiscal policy in Germany.

- Sovereign Spreads: OAT spread forecasts reflect both political and fiscal woes. BTP spreads should be more stable.

- Eurozone Inflation: Inflation expectations remain anchored around the 2% target.

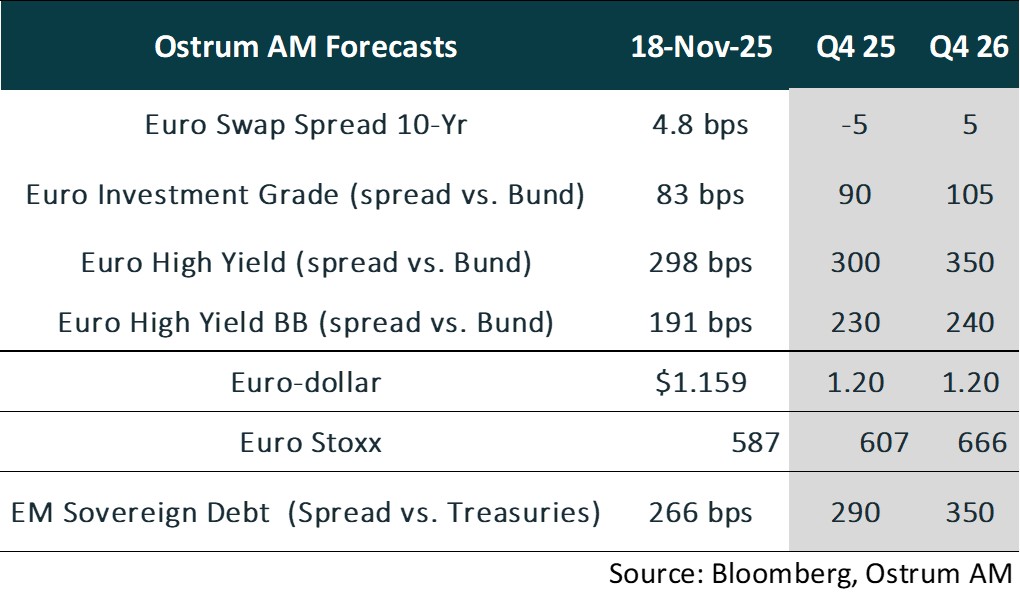

- Euro Credit: Investment-grade credit spreads have tightened significantly. A modest widening from current rich levels appears likely.

- Euro High Yield: Valuations in the high-yield sector are expected to normalize over the coming year. However, the default rate remains low and below the historical average.

- Exchange Rates: Distrust in the dollar has propelled the euro higher, with the single currency expected to approach $1.20.

- European Equities: Tariffs are likely to weigh on margins, but the positive sentiment factor is likely to propel valuation multiples higher.

- Emerging Debt: Emerging market spreads may remain close to current tight levels in the near term.