The risk of escalating inflation is increasingly shaping our current economic era, compelling investors to fundamentally adapt their strategies. Inflationary episodes, spurred by events like the pandemic, the war in Ukraine, and the more recent crisis in the Middle East, have revealed that inflation surges are characterized by complex dynamics.

In terms of allocation, real assets and commodities have long been cited as solutions for investors and in 2023, the phenomenon of 'greedflation'1 gave investors a good incentive to favor equities as companies could capitalize on profit margin expansion by raising prices faster than costs. Now, with supply chain disruptions resurfacing due to the crisis in the Middle East, we face a potential amplification of these same inflationary dynamics. Beyond corporate 'greedflation,' the economy is increasingly exhibiting a 'rockets and feathers' effect: prices surge rapidly with rising costs, yet demonstrate a stubborn reluctance to fall, if at all, when input costs decline.

In this increasingly unpredictable inflationary landscape, Inflation-Linked Bonds (ILBs) offer a direct, built-in mechanism to revalue both principal and coupon payments according to inflation rates, presenting a crucial, yet potentially underutilized, hedge. The inherent reliance on the Consumer Price Index (CPI) for ILBs transforms into a strategic advantage: while falling producer prices might bolster equity returns, persistent CPI inflation directly translates into more favorable and consistent coupon payments – a dynamic further amplified by the sticky nature of consumer prices.

This publication focuses on the unique characteristics of ILBs, as a direct inflation hedge, reviews the main issuers, and examines their effectiveness in the face of these complex and dynamic inflationary pressures.

1Greedflation: A situation in which certain companies raise prices beyond underlying cost increases to protect or expand margins, leveraging the broader inflationary environment.

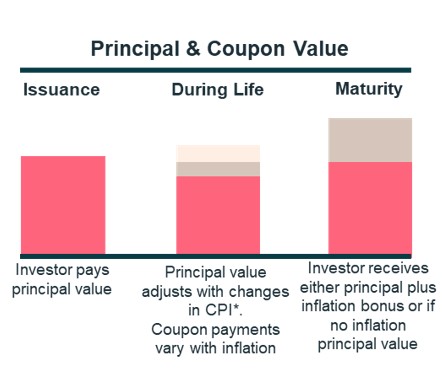

Inflation-Linked Bonds: Built-in Inflation Protection

LBs are structured to provide investors with a direct hedge against inflation. ILBs have two key features that adjust with inflation: the coupon payments and the principal amount (or redemption value).

Coupon Payments: coupons paid are calculated based on a fixed rate applied to an inflation-adjusted principal. Therefore, the actual cash received from coupon payments will fluctuate with inflation. Coupon payments are priced to Consumer Price Indexes (CPI), meaning they are directly linked to mainstream inflation measures.

Principal Revaluation: a defining characteristic of ILBs is that their principal amount is adjusted over the life of the bond according to movements in a designated inflation index, most commonly the CPI.

- Inflationary Environment: If there is positive inflation over the bond's term, the principal repayment at maturity will be higher than the original nominal value, reflecting an 'accumulated inflation bonus.' This ensures that the investor receives back the real value, or purchasing power, that was initially invested.

- Deflationary Environment: If inflation turns negative (deflation) over the bond's life, most ILBs provide a crucial 'deflation floor.' This means the redemption value at maturity will be at least 100% of the nominal value. In effect, investors are protected from losing principal due to deflation, offering a valuable safety net. Exceptions to this deflation floor exist (e.g., the UK and Canada have different structures for some of their issuances), but the principle of protection against purchasing power erosion remains central.

Source: Ostrum AM. *CPI: consumer price index. For illustrative purpose.

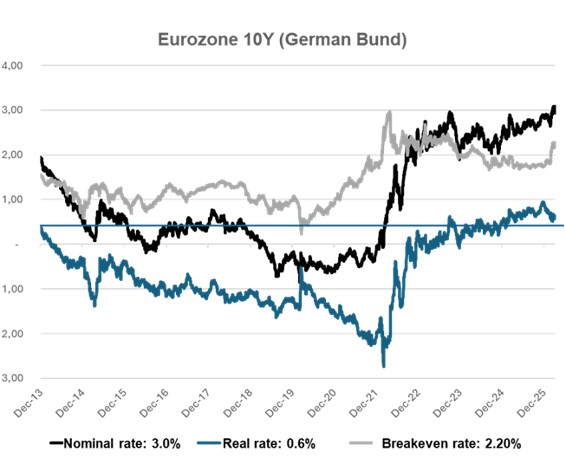

Reading the Yield of an Inflation Linked Bond

The yield on ILBs is calculated excluding inflation indexation. This ‘real’ yield (or rate) can be compared to the nominal yield of a fixed rate bond with an equivalent maturity. The difference between the two yields (real and nominal) is called the breakeven. The breakeven rate represents the market’s expectations for inflation for a given maturity. It also represents the level at which an investment in an ILB is equivalent to a nominal bond for the same issuer.

Source: Ostrum AM, Bloomberg as at end-march 2026

Two Centuries of History, a Deep Market Dominated by Sovereign Issuers

The ILB market is dominated by sovereign issuers. The genesis of these instruments can be traced back to 1780, during the US War of Independence, aimed to compensate soldiers for declining purchasing power.

Later, in 1966, Brazil pioneered its issuance to attract long-term financing for infrastructure and agricultural projects amidst high inflation. (Other Latam issuers include Chile, Colombia, Mexico and South Africa).

Developed markets began their significant adoption later; the United Kingdom, under Margaret Thatcher in 1981, was the first developed country to issue ILBs, setting a precedent followed by nations like Australia (1985 initially then restarted again in 2009), Canada (1991), Sweden (1994), New Zealand (1995), the United States (1997), France (1998), Greece and Italy (2003), Japan (2004), Germany (2006), South Korea (2007), Hong Kong (2011), Denmark (2012), Spain (2014)….

In terms of market size, the stock in the UK is around 25% of the total debt portfolio (£620 billion). For 2025-2026 refinancing, UK ILB issuance is planned at around 10% of total bond issuance which compares to around 10% in France and 9% in the US.

Two previous issuing countries: Canada (2022) and Germany (2023) decided to leave the ILB market. German and Canadian finance ministers have indicated that the issuance of these bonds implies that the state assumes the financial risk of an increase in inflation, which can become an increasing liability. Germany currently has 66 billion euros of ILBs in circulation as at March 2026. These bonds will continue to trade in the market.

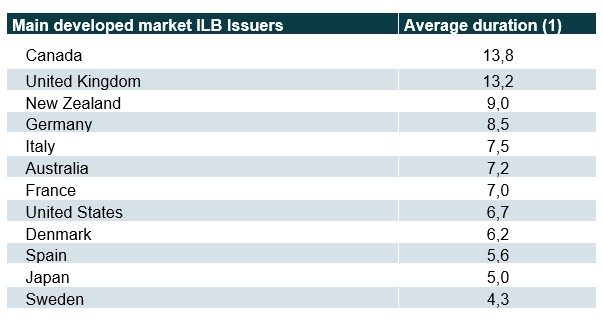

While the number and size of issuance vary by market, a number of countries now have developed deep and liquid inflation linked yield curves extending from 2 through to 30 years.

(1) Duration of a bond: Average life of its financial flows weighted by their present value.

Source: Ostrum AM, Bloomberg as at 24/04/2026

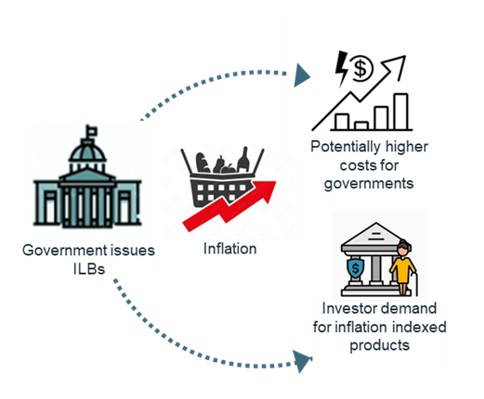

The Paradox of Public Debt

Issuing ILBs can potentially imply increased costs and thus increase the country's debt burden in times of inflation. The decisions of Canada and Germany are evidence that the debate has been launched. So why are other countries continuing to issue them if there is such a danger to the finances of a state? First, some countries like the UK, USA or France, have local investor base, such as insurance companies or pension funds that seek inflation protection. A second argument is that countries that issue ILBs send a signal to the markets that the fight against inflation is a priority (when inflation falls, the cost of debt can be reduced through these instruments).

France: A Pioneer in Inflation-Linked Green Bonds

On 25 May 2022, France launched its first inflation linked green bond (Green OAT€i 0.10% 25/07/2038) for a nominal value of 4 billion euros. After tapping the bond, the size has since increased to over 8 billion euros. This issuance program demonstrates France's strong willingness to be a pioneer in green bonds and targeting responsible investors.

Sustainable inflation: a new paradigm for portfolios

Given the potential for inflation to endure, investors are compelled to consider how best to adapt. ILB’s offer a direct and transparent mechanism for preserving purchasing power, serving a wide array of investors, from pension funds managing liabilities to endowments safeguarding capital and entities engaged in asset-liability matching or seeking insurance against unexpected inflation. The strategic advantage of CPI-linked ILBs, where sticky consumer prices ensure favorable coupon payments even if producer prices fall, further enhances their appeal.

As with any asset class, ILBs are subject to short-term market fluctuations. However, the prevailing long-term structural arguments for their inclusion are compelling. Geopolitical influences, supply chain disruptions, demographic shifts, the persistent challenge of rising food prices, and the undeniable influence of climate change are structural forces with the capacity to drive inflation for years to come. As these factors increasingly take prominence on a longer time horizon, a strategic allocation to ILBs offers a vital hedge against sustained price increases and the erosion of purchasing power.

Ostrum AM: Navigating Inflation with Performance and ESG

Ostrum AM offers two ILB strategies, Euro and Global, both classified in SFDR Article 8, implying ESG commitments. ESG performance is analyzed, relying on the SDG Index, which assesses countries' achievement of the 17 United Nations Sustainable Development Goals (SDGs). The ILB investment strategies aim to have higher scores than their reference universes. Ostrum AM’s Euro and Global ILB strategies are actively managed, combining core (real rates, breakeven rates, carry, relative value) and diversification (nominal rates) strategies to capture opportunities throughout market cycles.

2These ILB strategies promote environmental or social characteristics but do not have a sustainable investment objective. They may partially invest in assets with a sustainable objective, for example classified as sustainable under the EU classification.

3The SDG Index is a numerical score ranging from 0 (lowest score) to 100 (highest score). It is published by SDSN (Sustainable Development Solutions Network, a global UN initiative) and Bertelsmannstiftung (a German foundation). https://www.sdgindex.org/.